|

市場調查報告書

商品編碼

1836529

複合材料修復:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Composite Repair - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

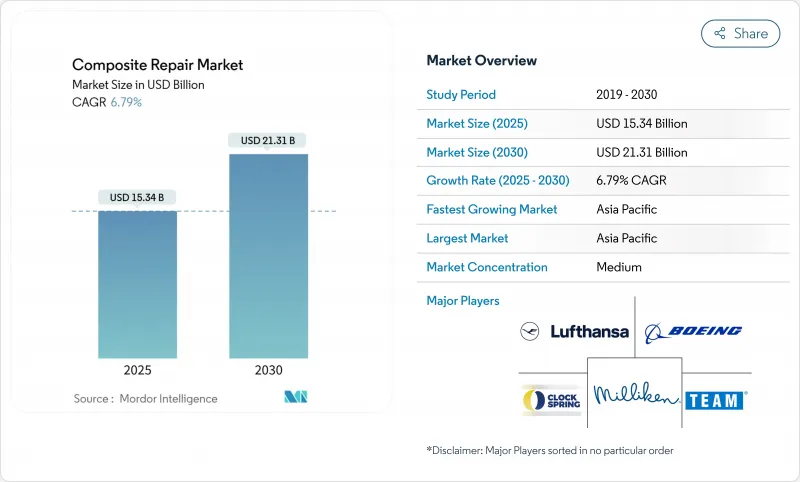

複合材料修復市場預計在 2025 年達到 153.4 億美元,到 2030 年將成長至 213.1 億美元,複合年成長率為 6.79%。

隨著資產所有者從昂貴的更換轉向高效的複合材料修復,以恢復結構性能並減少停機時間,成長持續進行。雖然結構修復仍然是由深厚的認證專業知識支撐的支柱領域,但隨著預防性保養,外觀修復正以最快的速度發展。雖然航太仍佔據最大的終端用戶佔有率,但離岸風電對無法在陸地上移動的葉片的現場維修需求日益成長。數位雙胞胎整合、自動化以及 ASME PCC-2 和 ISO 24817 等標準可確保品質、降低風險並支援其在關鍵基礎架構中的廣泛應用。

全球複合材料修復市場趨勢與洞察

老化資產壽命延長計畫投資激增

營運商正在擴展而不是更換管道、飛機和工業廠房,而複合材料纏繞材料正幫助他們在不關閉資產的情況下實施這項策略。 TD Williamson 於 2024 年 12 月收購了 Petro-Line,將 PETROSLEEVE 技術添加到其產品組合中,使現場管道加固能夠符合北美完整性義務。 HJ3 使用碳纖維纏繞材料修復公路橋柱,成本僅為更換成本的一半,證明了其對公共基礎設施的經濟效益。離岸風力發電葉片更換成本約為每片 20 萬美元,而複合材料修復平均成本為 3 萬美元,因此延長葉片壽命對業主來說是一個極具吸引力的考慮因素。

與金屬替換相比,原位複合材料修復的成本效益

與基於焊接的金屬修復相比,複合材料覆蓋層無需申請熱加工許可證,降低保險費,並減少工時。 ASME PCC-2 指南指出,複合材料可以減少 70-80% 的熱加工,顯著提高安全性和生產效率。澳洲皇家海軍報告稱,護衛艦甲板碳纖維覆蓋層的耐久性可達 15 年,證明了其在海上的長期耐用性。西卡 2024 年銷售額達 117.6 億瑞士法郎,部分原因是其基礎設施修復樹脂可最大限度地減少停機時間並延長資產壽命。由於預算有限的業主選擇複合材料,這些經濟效益為成長貢獻了 1.5 個百分點。

自修復複合材料層壓板的出現

學術突破表明,複合材料自主密封微裂紋,從而有可能降低未來的維修需求。 2025年4月,早稻田大學推出了矽氧烷薄膜,可在加熱後自行修復,同時保持1.50 GPa的硬度。德克薩斯農工大學的Diels-Alder聚合物兼具防彈性與自修復能力,引起了日本防衛省的興趣。雖然這些概念仍處於商業化前階段,但它們預示著未來可能會減少售後市場的銷售量,從2029年起,複合年成長率將下降0.7個百分點。

報告中分析的其他促進因素和限制因素

- 複合複合材料在航太和國防工業的應用日益廣泛

- 增加風力葉片的長度需要現場維修能力

- 認證複合材料修復技術人員短缺

細分分析

2024年,結構修復佔了複合材料修復市場佔有率的44.56%,因為業主優先修復飛機、管道和風電葉片。該領域受益於嚴格的認證通訊協定,這些協議有利於成熟的供應商,尤其是在航太領域,複合材料主結構需要精確的斜接幾何形狀和可控的固化曲線。營運商正在採用這些修復方案來延長安全服務間隔並推遲資本密集的更換,從而鞏固了該領域在複合材料修復市場的領先地位。

到2030年,外觀修復的複合年成長率將達到7.66%,反映出人們正轉向及早干預,以便在表面侵蝕變得更加嚴重之前進行處理。貝爾佐納(Belzona)塗層等尖端風力發電機處理技術,證明了外觀修復能夠減少氣動損耗,並避免更嚴重的結構宣傳活動。隨著預測性維護工具能夠更早發現細微的外觀缺陷,外觀修復領域複合材料修復的市場規模將不斷擴大,這將鼓勵服務供應商開發快速固化、現場友好的系統,以滿足停機需求。

手工積層方法因其便攜性和極低的設備要求,在2024年佔據了複合材料修復市場佔有率的38.55%。當天氣、地形或通道等因素導致自動化施工無法進行時,現場施工團隊通常會選擇手工積層。 CompositePatch的5分鐘緊急套件在海上事故中展現了其優勢,快速的船體密封可避免代價高昂的停機。

由於營運商對高應力零件的航太級品質要求,預計高壓釜維修的複合年成長率將達到 8.03%。航空公司正轉向高壓釜維修廠,將引擎整流罩和飛行控制面修復至與原廠製造相當的品質水準。隨著航空業的發展,透過高壓釜服務進行複合材料維修的市場規模預計將持續擴大。在英格索爾機床等設備製造商(它們為 MRO 中心提供機器人)的推動下,真空灌注和自動纖維鋪放技術持續發展。

區域分析

亞太地區憑藉其龐大的製造業基礎、不斷擴張的離岸風電項目以及雄心勃勃的基礎設施更新計劃,佔據著全球最大的複合材料修復市場。中國風電原始設備製造商正在部署15兆瓦級風力渦輪機,這推動了對葉片現場修復技術的需求。隨著公路、鐵路和港口計劃整合複合材料增強材料以滿足加速的工期,印度和東南亞地區正實現高個位數成長。

北美能源供應主要來自老化的電網和強大的民航機。管線營運商正在採用符合 ASME 標準的碳纖維外包裝來緩解腐蝕,同時保持輸送量;美國MRO 公司正在投資建造用於寬體高壓釜釜設施。該地區也在大平原地區的風電場試行數位雙胞胎配置,用於預測性葉片維修。

歐洲仍然以技術為中心,受國家獎勵的推動,這些措施促進了研發。德國航太叢集正在研發熱塑性無環縫修補技術,丹麥則在葉片機器人技術領域處於領先地位。漢莎科技公司斥資12億歐元進行的擴張,凸顯了該地區致力於成為複合材料MRO領域的領導者的承諾。隨著現有設備基礎的成熟,但對更先進的維護技術的需求不斷增加,歐洲複合材料維修市場的成長將穩定在中等個位數水準。拉丁美洲以及中東和非洲地區總體規模雖小,但發展迅速,它們在採用成熟地區成熟的技術的同時,也在培養國內技術人員隊伍。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 老化資產壽命延長計劃投資快速增加

- 現場複合材料修復和金屬零件更換的成本優勢

- 複合複合材料在航太和國防工業的應用日益廣泛

- 離岸風電葉片長度增加需要現場維修能力

- 數位雙胞胎引導的預測性維護降低了檢查成本

- 市場限制

- 自修復複合複合材料層壓板的出現

- 認證複合材料修復技術人員短缺

- 缺乏統一的海底複合材料管道修復規範。

- 價值鏈分析

- 五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 專利分析

第5章 市場規模及成長預測(金額)

- 依產品類型

- 結構

- 半結構化

- 化妝品

- 按修復流程

- 手工積層

- 真空灌注

- 高壓釜

- 其他流程

- 依材料類型

- 碳纖維增強聚合物(CFRP)

- 玻璃纖維增強聚合物(GFRP)

- 醯胺纖維複合材料

- 混合纖維和其他纖維

- 按最終用戶產業

- 航太/國防

- 風力發電

- 車

- 海洋

- 建造

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- 3M

- Belzona International Ltd.

- Boeing

- ClockSpring

- Composite Technology Inc.

- Crawford Composites LLC

- DIAB Group

- Gurit Holding AG

- HAECO Group

- Henkel AG & Co. KGaA

- Hexcel Corporation

- Lufthansa Technik AG

- Milliken Infrastructure Solutions

- ResinTech Inc.

- Sika AG

- TD Williamson Inc.

- TEAM, Inc.

- Toray Advanced Composites

- WR Composites

第7章 市場機會與未來展望

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 老化資產壽命延長計劃投資快速增加

- 現場複合材料修復和金屬零件更換的成本優勢

- 複合複合材料在航太和國防工業的應用日益廣泛

- 離岸風電葉片長度增加需要現場維修能力

- 數位雙胞胎引導的預測性維護降低了檢查成本

- 市場限制

- 自修復複合複合材料層壓板的出現

- 認證複合材料修復技術人員短缺

- 缺乏統一的海底複合材料管道修復規範。

- 價值鏈分析

- 五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 專利分析

第5章 市場規模及成長預測(金額)

- 依產品類型

- 結構

- 半結構化

- 化妝品

- 按修復流程

- 手工積層

- 真空灌注

- 高壓釜

- 其他流程

- 依材料類型

- 碳纖維增強聚合物(CFRP)

- 玻璃纖維增強聚合物(GFRP)

- 醯胺纖維複合材料

- 混合纖維和其他纖維

- 按最終用戶產業

- 航太/國防

- 風力發電

- 車

- 海洋

- 建造

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- 3M

- Belzona International Ltd.

- Boeing

- ClockSpring

- Composite Technology Inc.

- Crawford Composites LLC

- DIAB Group

- Gurit Holding AG

- HAECO Group

- Henkel AG & Co. KGaA

- Hexcel Corporation

- Lufthansa Technik AG

- Milliken Infrastructure Solutions

- ResinTech Inc.

- Sika AG

- TD Williamson Inc.

- TEAM, Inc.

- Toray Advanced Composites

- WR Composites

第7章 市場機會與未來展望

The composite repair market stood at USD 15.34 billion in 2025 and is forecast to rise to USD 21.31 billion by 2030, delivering a 6.79% CAGR.

Growth continues as asset owners pivot from costly replacements to efficient composite repairs that restore structural performance while curbing downtime. Structural repairs remain the anchor segment, supported by deep certification expertise, yet cosmetic repairs are advancing fastest as preventive maintenance gains favor across wind, marine, and transportation assets. Aerospace keeps the largest end-user share, while offshore wind drives incremental demand for in-situ blade work that cannot be moved onshore. Digital twin integration, automation, and standards such as ASME PCC-2 and ISO 24817 ensure quality, contain risk, and underpin expanding adoption across critical infrastructure.

Global Composite Repair Market Trends and Insights

Surging Investment in Ageing-Asset Life-Extension Programs

Operators extend pipelines, aircraft, and industrial plants instead of replacing them, and composite wraps help execute this strategy without shutting down assets. T.D. Williamson's purchase of Petro-Line in December 2024 brought PETROSLEEVE technology into its portfolio, enabling live pipeline reinforcement that meets North American integrity mandates . HJ3 restored a highway bridge column at half the replacement cost using carbon-fiber wraps, illustrating the economic benefit for public infrastructure. Offshore wind blade replacements cost about USD 200,000 each, yet composite repairs average USD 30,000, making life-extension compelling for owners.

Cost Advantages of On-Site Composite Repair Versus Metallic Part Replacement

Composite overwraps avoid hot-work permits, lower insurance premiums, and reduce man-hours versus weld-based metallic repairs. ASME PCC-2 guidance notes that composites can eliminate 70-80% of hot work, materially improving safety and productivity. The Royal Australian Navy reports 15-year durability on carbon-fiber overlays for frigate decks, providing a long proof record at sea. Sika logged CHF 11.76 billion in 2024 sales, partly driven by infrastructure repair resins that extend asset life with minimal downtime. These economics contribute +1.5 points to growth as budget-constrained owners choose composite solutions.

Emergence of Self-Healing Composite Laminates

Academic breakthroughs show composites that autonomously close micro-cracks, potentially lowering future repair demand. Waseda University released a siloxane film in April 2025 that heals after heating while retaining 1.50 GPa hardness. Texas A&M's Diels-Alder polymer combines ballistic resistance and self-repair functions, attracting defense interest. These concepts remain pre-commercial yet illustrate a future scenario that could reduce aftermarket volumes, trimming 0.7 points from the CAGR beyond 2029.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Use of Composites in the Aerospace and Defense Industry

- Offshore Wind Blade Length Growth Demanding In-Situ Repair Capability

- Scarcity of Certified Composite Repair Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Structural repairs accounted for 44.56% of the composite repair market share in 2024 as owners prioritize restoring load-bearing capacity on aircraft, pipelines, and wind blades. The segment benefits from rigorous certification protocols that favor established providers, especially in aerospace where composite primary structures demand precise scarf geometry and controlled cure profiles. Operators adopt these repairs to extend safe service intervals and defer capital-intensive replacements, reinforcing segment leadership inside the composite repair market.

Cosmetic repairs are rising at a 7.66% CAGR to 2030, reflecting the shift to early-stage interventions that address surface erosion before it propagates. Wind turbine leading-edge treatments, such as Belzona coatings, exemplify how cosmetic activities cut aerodynamic losses and avoid larger structural campaigns. As predictive maintenance tools flag minor surface defects earlier, the composite repair market size attached to the cosmetic category will expand, encouraging service providers to develop fast-cure, field-friendly systems that align with tight outage windows.

The hand lay-up method held 38.55% of composite repair market share in 2024 because of its portability and minimal equipment requirement. Field teams often rely on hand lay-up when weather, geometry, or access challenges rule out automated approaches. CompositePatch's five-minute emergency kits illustrate the advantage in maritime incidents where rapid hull sealing prevents costly downtime.

Autoclave repairs exhibit an 8.03% forecast CAGR as operators insist on aerospace-grade quality for highly loaded components. Airlines route engine cowls and flight-control surfaces to autoclave shops to regain qualification levels equal to original builds. As fleets grow, the composite repair market size for autoclave services will climb because airlines favor centralized, repeatable quality over field expediency. Vacuum infusion and automated fiber placement continue to advance, spurred by equipment manufacturers such as Ingersoll Machine Tools that supply robotics to MRO centers.

The Composite Repair Market Report Segments the Industry by Product Type (Structural, Semi-Structural, and More), Repair Process (Hand Lay-Up, Vacuum Infusion, and More), Material Type (Carbon-Fibre Reinforced Polymer (CFRP), Aramid-Fibre Composites, and More), End-User Industry (Automotive, Wind Energy, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commands the largest composite repair market because of its immense manufacturing base, expanding offshore wind pipelines, and ambitious infrastructure renewal plans. China's wind OEMs deploy fleets of 15-MW class turbines, fueling demand for in-situ blade servicing technologies. India and Southeast Asia register high single-digit growth as road, rail, and port projects integrate composite strengthening to meet accelerated timelines.

North America follows, underpinned by an aging energy network and a robust commercial aviation fleet. Pipeline operators apply ASME-qualified carbon overwraps to mitigate corrosion while maintaining throughput, and MRO houses in the United States invest in autoclave capacity for wide-body nacelles. The region also pilots digital twin deployments for predictive blade repairs on Great Plains wind farms.

Europe remains technology-centric with state incentives that drive R&D. Germany's aerospace cluster works on thermoplastic scarf-less patching, and Denmark pioneers blade robotics. Lufthansa Technik's EUR 1.2 billion expansion underscores local commitment to composite MRO leadership. Composite repair market size growth in Europe stabilizes at mid-single digits as the installed base matures but demands more sophisticated upkeep. Latin America, the Middle East, and Africa collectively form a smaller yet rapidly advancing bloc, adopting proven techniques from mature regions while cultivating domestic technician pipelines.

- 3M

- Belzona International Ltd.

- Boeing

- ClockSpring

- Composite Technology Inc.

- Crawford Composites LLC

- DIAB Group

- Gurit Holding AG

- HAECO Group

- Henkel AG & Co. KGaA

- Hexcel Corporation

- Lufthansa Technik AG

- Milliken Infrastructure Solutions

- ResinTech Inc.

- Sika AG

- TD Williamson Inc.

- TEAM, Inc.

- Toray Advanced Composites

- WR Composites

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging investment in ageing-asset life-extension programs

- 4.2.2 Cost advantages of on-site composite repair versus metallic part replacement

- 4.2.3 Increasing Use of Composites in the Aerospace and Defense Industry

- 4.2.4 Offshore wind blade length growth demanding in-situ repair capability

- 4.2.5 Digital twin-guided predictive maintenance lowers inspection cost

- 4.3 Market Restraints

- 4.3.1 Emergence of self-healing composite laminates

- 4.3.2 Scarcity of certified composite repair technicians

- 4.3.3 Lack of harmonised repair codes for subsea composite pipelines

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Patent Analysis

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Structural

- 5.1.2 Semi-structural

- 5.1.3 Cosmetic

- 5.2 By Repair Process

- 5.2.1 Hand Lay-up

- 5.2.2 Vacuum Infusion

- 5.2.3 Autoclave

- 5.2.4 Other Processes

- 5.3 By Material Type

- 5.3.1 Carbon-fibre Reinforced Polymer (CFRP)

- 5.3.2 Glass-fibre Reinforced Polymer (GFRP)

- 5.3.3 Aramid-fibre Composites

- 5.3.4 Hybrid & Other Fibres

- 5.4 By End-User Industry

- 5.4.1 Aerospace and Defense

- 5.4.2 Wind Energy

- 5.4.3 Automotive

- 5.4.4 Marine

- 5.4.5 Construction

- 5.4.6 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Belzona International Ltd.

- 6.4.3 Boeing

- 6.4.4 ClockSpring

- 6.4.5 Composite Technology Inc.

- 6.4.6 Crawford Composites LLC

- 6.4.7 DIAB Group

- 6.4.8 Gurit Holding AG

- 6.4.9 HAECO Group

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Hexcel Corporation

- 6.4.12 Lufthansa Technik AG

- 6.4.13 Milliken Infrastructure Solutions

- 6.4.14 ResinTech Inc.

- 6.4.15 Sika AG

- 6.4.16 TD Williamson Inc.

- 6.4.17 TEAM, Inc.

- 6.4.18 Toray Advanced Composites

- 6.4.19 WR Composites

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Automation of Composite Repair