|

市場調查報告書

商品編碼

1836519

半拖車:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)Semi-trailer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

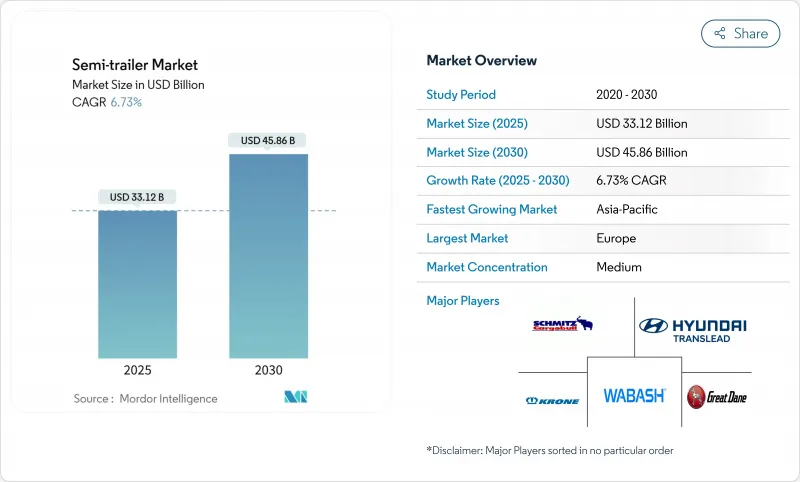

2025 年半拖車市場規模為 331.2 億美元,預計到 2030 年將達到 458.6 億美元,在此期間的複合年成長率為 6.73%。

電子商務對本地配送網路的持續影響、零排放貨運的監管推動以及以拖車為中心的自動化投資的不斷增加,共同推動了行業發展勢頭。乾貨廂型車保持了銷售領先地位,但隨著低溫運輸活動的擴展,冷凍設備的發展也正在加速。電動車軸、先進的遠端資訊處理和空氣動力學套件正日益成為購買標準,而新興經濟體的基礎設施發展計畫則正在推動基準車輛需求。

全球半掛車市場趨勢與洞察

電子商務貨運熱潮

線上銷售的成長正在改變路線密度和貨物尺寸,推動了對多功能乾貨廂式貨車的需求,這些設備既能服務於區域樞紐,又能在城市中心靈活移動。車隊管理人員正在增加模組化車身,以便在旺季靈活調整運力;遠端資訊處理技術使負責人能夠避免城市堵塞,因為卡車在密集的交通幹線上的延誤率已經超過了疫情前的水平。宅配和小包裹托運人擴大指定使用高箱拖車,以最大限度地提高內部高度;供應商則鼓勵採用複合材料面板,以在不犧牲剛性的情況下減輕自重。由於這些貨物對時間敏感,托運人更傾向於配備預測性維護感測器的設備,這些感測器可以在故障發生前發出門密封條磨損或車輪端發熱的訊號。這些變化使半拖車市場與消費者對隔日送達不斷變化的期望緊密結合。

擴大全球低溫運輸物流

可支配收入的增加和藥品分銷的擴張正在推動全球對冷藏拖車的需求。歐洲的低溫運輸生態系統已支撐著8,000億歐元的商業價值,並僱用了超過2,900萬人。與傳統系統相比,開利運輸公司(Carrier Transicold)的新型Vector HE17冷凍機組可將燃料消費量降低30%,使托運人能夠在不犧牲負載容量的情況下滿足嚴格的排放法規。像Biocoop這樣的零售商和合作雜貨商已承諾到2030年將其近三分之一的冷藏設備電氣化,利用靜音運行的優勢,充分利用隔夜送達的時段。

資金投入高、利息負擔重

借貸成本上升導致續約週期放緩,正如Wabash National公司2025年第一季銷售額下降26.1%所證實,原因是訂單不足以滿足車隊維修需求。小型承運商缺乏可負擔的信貸,這使得資金更充裕的買家得以收購陷入困境的競爭對手,並推動整合。主機廠的因應之策是提供包含維護的長期租賃,但殘值風險的上升推高了總擁有成本,限制了半拖車市場的短期成長。

報告中分析的其他促進因素和限制因素

- 新興國家基礎設施電氣化獎勵策略

- 再生軸拖車TCO降低

- 鋼鐵和鋁價格波動

細分分析

乾貨廂型車平台憑藉其與日用百貨、碼垛設備和包裝消費品的通用內部相容性,將在2024年保持半拖車市場55.21%的佔有率。乾貨廂式貨車平台支援大型零售商和合約承運商的可預測更換週期,從而保持穩定的生產率。儘管如此,受快速發展的電子商務和疫苗物流的推動,預計到2030年,冷藏行業的複合年成長率將達到9.14%。像開利冷鏈全電動式Vector eCool這樣的設備可將直接排放降至零,並允許營運商在低噪音的市中心區域運作。

在半拖車市場,平板車和低底盤車受基礎設施資金籌措週期影響,而油罐車需求則與化學品和燃料吞吐量密切相關,法律規範使設計更加複雜。雖然北美地區優先考慮全封閉式車輛以防盜竊,但側簾式車輛在歐盟仍然佔據主導地位,因為它注重側裝效率。在裝載完整性高於標價的情況下,提供具有遠端資訊處理功能和預測性溫度警報的冷凍車的原始設備製造商脫穎而出。因此,冷藏車類別正在引領整個拖車市場的規格創新。

25-50噸級拖車佔銷售額的38.26%,並維持了8.23%的成長率,這得益於其多功能性,無需特殊許可即可穿越區域車道。業者看重這些車輛與三軸牽引車和標準公路橋樑的兼容性,從而避免了重型鑽機產生的通行額外費用。由於其均衡的裝載效率吸引了托運人,預計到2030年,此類半拖車的市場規模將達到203億美元。

重量在51噸至100噸之間的低底盤供應能源和建築大型企劃,但受週期性商品支出的影響。 100噸以上的模組雖然對風力發電機葉片和煉油容器至關重要,但仍屬於利基市場。歐盟提案將零排放卡車重量限制提高至44噸,這可能會重塑需求曲線,但對基礎設施成本的擔憂可能會推遲全面協調。因此,在整個預測期內,半拖車市場可能仍將由中重型平台主導。

區域分析

到2024年,歐洲將佔全球收益的35.22%,這得益於成熟的公路網路、密集的跨境貿易以及早期的排放法規刺激了輪調更新。歐盟二氧化碳排放標準要求在2025年將拖車的效率提高15%,到2040年提高90%,促使買家轉向空氣動力學裙邊、低滾動阻力輪胎和電動軸。自2010年以來,半拖車市場成長了59%,並繼續受益於同步的鐵路公路聯運,這降低了跨境停留時間。然而,電動聯合收割機的重量增加提案引發了關於基礎設施成本和潛在公路模式轉換的討論,為採購週期注入了謹慎的情緒。

受中國持續的高速公路建設和印度貨運走廊的擴張推動,亞太地區以7.68%的複合年成長率脫穎而出。中集車輛累計,2024年上半年銷售額達107億元人民幣,在其「星鏈」最佳化計畫的帶動下,半拖車銷售額成長了24.67%。印度以卡車為重點的國家物流政策旨在將物流成本壓縮至GDP的10%以下,這項變革預計將透過提高次大陸的周轉率來擴大區域半拖車市場。在日本,日野和三菱扶桑之間的原始設備製造商整合加劇了競爭壓力。

北美將保持強勁勢頭,這得益於預計2025年8級牽引車銷量將達到25萬至28萬輛,以及政府制定的到2030年實現零排放商用車銷量佔比30%的藍圖。佩卡公司報告稱,其售後零件銷售額創下66.7億美元的歷史新高,顯示老舊拖車市場的利用率很高。然而,計劃對進口卡車徵收25%的關稅可能會導致掛車價格上漲9%,需求減少17%。南美洲嚴重依賴公路貨運,巴西65%的貨運量透過卡車運輸。同時,隨著開發銀行向交通走廊注入資金,中東和非洲市場正在獲得發展動力,塑造全球各地區半拖車市場的微妙前景。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 電子商務貨運熱潮

- 擴大全球低溫運輸物流

- 北美採用 60 英尺乾貨車規則

- 利用電動再生軸拖車降低總擁有成本

- 採用拖車遠端資訊處理及即時可視性

- 新興國家基礎設施獎勵策略

- 市場限制

- 資金投入高、利息負擔重

- 鋼鐵和鋁價格波動

- 歐盟重量和長度法規

- 缺乏電動TRU和電動軸的充電基礎設施

- 價值/供應鏈分析

- 監管狀況

- 技術展望

- 五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場規模與成長預測:價值(美元)

- 按車輛類型

- 平板

- 乾貨車

- 冷藏(冷藏箱)

- 低底盤

- 油船

- 側簾式

- 其他類型

- 按噸位

- 少於25噸

- 25噸-50噸

- 51噸至100噸

- 超過100噸

- 腳長

- 28至45英尺

- 超過 45 英尺

- 按最終用途行業

- 運輸/物流

- 飲食

- 建築和採礦

- 農業

- 製造業和工業產品

- 零售與電子商務

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太地區

- 中東和非洲

- 土耳其

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Wabash National Corporation

- Great Dane LLC

- Hyundai Translead

- Utility Trailer Manufacturing Company

- Schmitz Cargobull AG

- Krone GmbH & Co. KG

- China International Marine Containers Co., Ltd.

- Manac Inc.

- MAC Trailer Manufacturing Inc.

- East Manufacturing Corporation

- Stoughton Trailers LLC

- Vanguard National Trailer Corp.

- Kogel Trailer GmbH

- Wielton SA

- Fontaine Trailer Co.

- Pitts Trailers

- Premier Trailer Mfg. Inc.

- Kassbohrer Fahrzeugwerke

- Schwarzmuller Gruppe

第7章 市場機會與未來展望

The semi-trailer market size is valued at USD 33.12 billion in 2025 and is forecast to reach USD 45.86 billion by 2030, translating into a 6.73% CAGR over the period.

Industry momentum stems from e-commerce's relentless pull on regional distribution networks, regulatory pushes for zero-emission freight, and rising investments in trailer-centric automation. Dry van units uphold volume leadership, yet refrigerated equipment sets the pace as cold-chain activity broadens. Electrified axles, advanced telematics, and aerodynamic packages increasingly shape purchase criteria, while infrastructure programs across emerging economies lift baseline fleet demand.

Global Semi-trailer Market Trends and Insights

E-commerce freight boom

Online sales growth reshapes route density and shipment size, intensifying call-off rates for versatile dry-van equipment that can service regional hubs while maneuvering in urban cores. Fleet managers add modular bodies to flex capacity for peak seasons, and telematics enable crew schedulers to avoid city-center congestion as truck delays in dense corridors exceed pre-pandemic levels . Courier and parcel operators increasingly spec high-cube trailers that maximize internal height, prompting suppliers to adopt composite panels to trim tare weight without sacrificing stiffness. Because this freight is time-critical, carriers favor equipment with predictive-maintenance sensors that flag door seal wear and wheel-end heat before failures occur. Together, these changes keep the semi-trailer market in close alignment with shifting consumer expectations for next-day delivery.

Expansion of global cold-chain logistics

Rising disposable incomes and pharmaceutical distribution push refrigerated trailer demand worldwide. Europe's cold-chain ecosystem already supports EUR 800 billion in commerce and employs over 29 million people, underscoring the structural scale of temperature-controlled freight . New Vector HE 17 refrigeration units from Carrier Transicold cut fuel burn by 30% relative to legacy systems, letting shippers meet tightening emission ceilings without sacrificing payload. Retailers and cooperative grocers such as Biocoop have pledged to electrify nearly one-third of reefer equipment by 2030, leveraging whisper-quiet operations to access night-time delivery slots.

High capex & interest-rate burden

Elevated borrowing costs delay replacement cycles, evidenced by Wabash National's 26.1% revenue drop in Q1 2025 as orders fell below fleet sustainment needs. Smaller carriers lack inexpensive credit facilities, prompting consolidation as buyers with superior capital access scoop distressed competitors. OEMs respond with extended-term leases bundled with maintenance, though higher residual-value risk inflates the overall cost of ownership, tempering near-term semi-trailer market growth.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure stimulus in emerging economies

- Electrified regenerative-axle trailers cut TCO

- Volatile steel & aluminum prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dry van platforms kept a 55.21% share of the semi-trailer market in 2024 as their universal interior fits general merchandise, palletized machinery, and packaged consumer goods. They anchor predictable replacement cycles among big-box retailers and contract carriers, sustaining steady build rates. Nevertheless, the refrigerated segment is charting a 9.14% CAGR to 2030, catalyzed by rapid grocery e-commerce and vaccine logistics. Equipment such as Carrier Transicold's all-electric Vector eCool cuts direct emissions to zero, letting operators enter low-noise downtown zones.

The semi-trailer market also sees flatbeds and lowboys ride infrastructure funding cycles, whereas tanker demand tracks chemical and fuel throughput, with regulatory oversight adding design complexity. Curtain-sider adoption remains pronounced in the EU for side-loading efficiency, though North America prioritizes full-enclosure bodies for theft deterrence. OEMs that deliver telematics-ready reefers with predictive temperature alerts differentiate in a landscape where load integrity trumps sticker price. As a result, the refrigerated category steers overall specification innovation within the semi-trailer market.

Trailers rated 25-50 ton hold 38.26% of revenues and maintain an 8.23% expansion rate, underpinned by versatility across cross-regional lanes without special permits. Operators prize these units for matching three-axle tractors and standard highway bridges, cutting toll surcharges that heavier rigs attract. The semi-trailer market size for this class is set to reach USD 20.3 billion by 2030 as shippers gravitate toward balanced payload efficiency.

Heavier 51-100 ton lowboys serve energy and construction megaprojects but hinge on cyclic commodity spending. Above-100-tonne modules remain niche, albeit critical for wind-turbine blades and refinery vessels. EU proposals to lift zero-emission truck combos to 44 tonnes could reshape demand curves, yet infrastructure cost concerns may delay full harmonization. Consequently, mid-weight platforms will continue to anchor volume in the semi-trailer market through the forecast horizon.

The Semi-Trailer Market Report is Segmented by Vehicle Type (Flat Bed, Dry Van, and More), Tonnage (Below 25 Ton, 25 Ton - 50 Ton, and More), Foot Length (28-45 Ft and Above 45 Ft), End-Use Industry (Transportation and Logistics, Food and Beverage, and More) and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe anchored 35.22% of global revenue in 2024 as mature road networks, dense cross-border trade, and early emissions legislation stimulate rotational renewals. EU CO2 standards mandate trailer efficiency improvements of 15% by 2025 and up to 90% by 2040, channeling buyers toward aerodynamic skirts, low-rolling-resistance tires, and electrified axles. The semi-trailer market continues to benefit from synchronized rail-road combined transport, which has expanded 59% since 2010, keeping cross-border dwell times low. However, weight increases proposed for electric combinations trigger infrastructure cost debates and potential modal shifts back toward road, injecting cautious sentiment into procurement cycles.

Asia-Pacific stands out with a 7.68% CAGR, propelled by China's sustained highway build-out and India's freight-corridor rollouts. CIMC Vehicles booked 10.7 billion RMB revenue in H1 2024 and logged a 24.67% lift in semi-trailer sales under its Starlink optimization program, underscoring local production agility. India's truck-focused National Logistics Policy aims to compress logistics costs to under 10% of GDP-a change expected to swell the regional semi-trailer market by lifting asset turnover on the subcontinent. Japan's push for OEM consolidation between Hino and Mitsubishi Fuso adds competitive tension.

North America retains a solid base, buoyed by 250,000-280,000 projected Class 8 tractor sales in 2025 and a policy blueprint that targets 30% zero-emission commercial vehicle sales by 2030. PACCAR reports record USD 6.67 billion aftermarket parts turnover, signaling strong utilization of aging trailer pools. Yet prospective 25% tariffs on imported trucks could drive trailer price inflations of 9% and dent demand by 17%. South America relies heavily on road freight-Brazil moves 65% of goods by truck-while Middle East and Africa markets gain momentum as development banks funnel capital into transport corridors, altogether shaping a nuanced outlook for the semi-trailer market across global regions.

- Wabash National Corporation

- Great Dane LLC

- Hyundai Translead

- Utility Trailer Manufacturing Company

- Schmitz Cargobull AG

- Krone GmbH & Co. KG

- China International Marine Containers Co., Ltd.

- Manac Inc.

- MAC Trailer Manufacturing Inc.

- East Manufacturing Corporation

- Stoughton Trailers LLC

- Vanguard National Trailer Corp.

- Kogel Trailer GmbH

- Wielton S.A.

- Fontaine Trailer Co.

- Pitts Trailers

- Premier Trailer Mfg. Inc.

- Kassbohrer Fahrzeugwerke

- Schwarzmuller Gruppe

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce freight boom

- 4.2.2 Expansion of global cold-chain logistics

- 4.2.3 Adoption of 60-ft dry-van rules in North America

- 4.2.4 Electrified regenerative-axle trailers cut TCO

- 4.2.5 Trailer telematics & real-time visibility adoption

- 4.2.6 Infrastructure stimulus in emerging economies

- 4.3 Market Restraints

- 4.3.1 High capex & interest-rate burden

- 4.3.2 Volatile steel & aluminium prices

- 4.3.3 EU weight/length regulatory limits

- 4.3.4 Sparse charging infra for electric TRUs & e-axles

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 Flatbed

- 5.1.2 Dry Van

- 5.1.3 Refrigerated (Reefer)

- 5.1.4 Lowboy

- 5.1.5 Tanker

- 5.1.6 Curtain-Sider

- 5.1.7 Other Types

- 5.2 By Tonnage

- 5.2.1 Below 25 Ton

- 5.2.2 25 Ton - 50 Ton

- 5.2.3 51 Ton - 100 Ton

- 5.2.4 Above 100 Ton

- 5.3 By Foot Length

- 5.3.1 28 - 45 ft

- 5.3.2 Above 45 ft

- 5.4 By End-Use Industry

- 5.4.1 Transportation and Logistics

- 5.4.2 Food and Beverage

- 5.4.3 Construction nd Mining

- 5.4.4 Agriculture

- 5.4.5 Manufacturing and Industrial Goods

- 5.4.6 Retail and E-commerce

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Wabash National Corporation

- 6.4.2 Great Dane LLC

- 6.4.3 Hyundai Translead

- 6.4.4 Utility Trailer Manufacturing Company

- 6.4.5 Schmitz Cargobull AG

- 6.4.6 Krone GmbH & Co. KG

- 6.4.7 China International Marine Containers Co., Ltd.

- 6.4.8 Manac Inc.

- 6.4.9 MAC Trailer Manufacturing Inc.

- 6.4.10 East Manufacturing Corporation

- 6.4.11 Stoughton Trailers LLC

- 6.4.12 Vanguard National Trailer Corp.

- 6.4.13 Kogel Trailer GmbH

- 6.4.14 Wielton S.A.

- 6.4.15 Fontaine Trailer Co.

- 6.4.16 Pitts Trailers

- 6.4.17 Premier Trailer Mfg. Inc.

- 6.4.18 Kassbohrer Fahrzeugwerke

- 6.4.19 Schwarzmuller Gruppe

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

鋁合金罐式半拖車市場:依材料等級、車輪配置、裝載方式、產品類型和應用分類-全球預測,2026-2032年

鋁合金罐式半拖車市場:依材料等級、車輪配置、裝載方式、產品類型和應用分類-全球預測,2026-2032年 全球半掛車市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球半掛車市場規模、佔有率、趨勢和成長分析報告(2026-2034) 半拖車市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、負載容量、長度、地區和競爭格局分類,2021-2031年)

半拖車市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、負載容量、長度、地區和競爭格局分類,2021-2031年) 半拖車市場規模、佔有率和成長分析(按類型、長度、負載容量、軸數、最終用途行業和地區分類)—2026-2033年行業預測

半拖車市場規模、佔有率和成長分析(按類型、長度、負載容量、軸數、最終用途行業和地區分類)—2026-2033年行業預測 全球半掛車經銷市場:依經銷商類型、拖車類型、銷售通路、終端用戶產業、服務內容與地區劃分-市場規模、產業趨勢、機會分析與預測(2026-2035 年)半拖車市場按類型、材質、噸位、車軸配置和最終用戶分類-2025-2032 年全球預測

全球半掛車經銷市場:依經銷商類型、拖車類型、銷售通路、終端用戶產業、服務內容與地區劃分-市場規模、產業趨勢、機會分析與預測(2026-2035 年)半拖車市場按類型、材質、噸位、車軸配置和最終用戶分類-2025-2032 年全球預測 2025年全球拖車市場報告

2025年全球拖車市場報告 半拖車市場規模、佔有率和趨勢分析報告:按類型、地區和細分市場分類,預測,2025 年至 2033 年

半拖車市場規模、佔有率和趨勢分析報告:按類型、地區和細分市場分類,預測,2025 年至 2033 年 半拖車的印度市場評估:聯結車類別,車軸類別,各地區,機會,預測(2019年度~2033年度)全球半掛車市場:2034 年市場機會與策略

半拖車的印度市場評估:聯結車類別,車軸類別,各地區,機會,預測(2019年度~2033年度)全球半掛車市場:2034 年市場機會與策略