|

市場調查報告書

商品編碼

1836514

無線射頻測試設備:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)RF Test Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

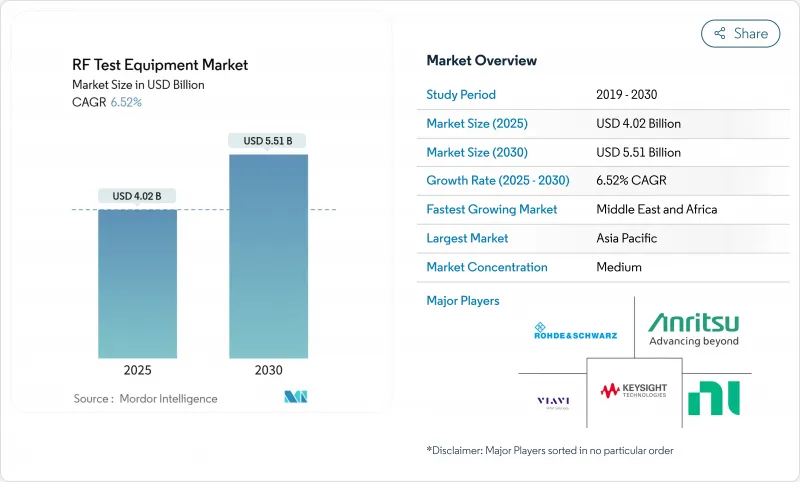

預計射頻測試設備市場規模在 2025 年將達到 40.2 億美元,在 2030 年將達到 55.1 億美元,2025 年至 2030 年的複合年成長率為 6.52%。

5G 毫米波鏈路的普及、向軟體定義實驗室的轉變以及不斷成長的雷達和衛星項目,將支撐到2024年穩定的需求。矽基氮化鎵功率元件的整合提升了擴大機的性能上限,而模組化平台則縮短了設定時間和營運成本。亞太地區的供應商繼續擴大國內網路和出口合約的產量,而北美實驗室則優先考慮雲端連接自動化,以應對工程人員短缺。以思博倫通訊兩次競標標為例,產業整合正在加劇,並正朝著承包硬體和軟體生態系統的方向轉變,這些生態系統正隨著3GPP標準的發布而不斷發展。

全球射頻測試設備市場趨勢與洞察

需要 24GHz 以上檢驗的 mmWave 5G 部署激增

24 至 39 GHz 的 5G 商業部署需要無線電暗室、相位陣列波束檢驗和寬頻頻道模擬。是德科技報告稱,其集生成、分析和衰落於一體的整合平台將測試週期縮短了 40%,並降低了研發中心的校準開銷。美國、韓國和德國的網路營運商已經批量訂購 32 和 64 通道分析儀,以便在密集的城市部署之前檢驗波束控制演算法。隨著毫米波小型基地台密度的增加,服務實驗室從單機頻譜掃描轉向自動化雲鏈路工作流程,可以在一夜之間完成數百個參數檢查。這種趨勢推動了射頻測試設備市場向模組化、富含 FPGA 的收發器發展,這些收發器能夠提供每通道 2 GHz 的瞬時頻寬。

東亞地區MIMO基地台快速成長

中國和日本正競相在大都會地區部署64T64R射頻,迫切需要能夠同時測試數十條射頻鏈路的設備。一份RF Globalnet簡報預測,2024年全球將新建或升級940萬個基地台,其中許多將採用大規模MIMO陣列。相位雜訊可實現單次無線特性分析,將塔側服務時間縮短一半。東亞OEM廠商進一步推動了對PXIe刀片組的需求,隨著3GPP版本的持續演進,工程師可以將其與軟體一起重複使用。向靈活產能的轉變支撐了生產線和現場服務供應商射頻測試設備市場的持續成長。

ETSI 和 3GPP 標準的快速發展導致過時

3GPP Release 18 於 2024 年 6 月凍結,Release 19 計畫於 2025 年底發布。每個週期都會引入新的空中介面功能,這些功能無法在傳統測試儀上輕鬆仿真,因此必須提前更換設備或進行昂貴的 FPGA 升級。面臨多標準認證的實驗室必須同時維護 NR、LTE 和 Wi-Fi 測試平台,這會導致營運預算激增。雖然模組化設計可以降低部分風險,但韌體授權費用和再培訓成本仍然抑制著射頻測試設備市場的支出。

報告中分析的其他促進因素和限制因素

- 德國和日本的汽車雷達/ADAS測試衛星

- LEO衛星群建設加速Ka波段測試

- 40GHz以上尺寸的散熱挑戰

細分分析

模組化GP儀器佔據了這一層級射頻測試設備市場的最大佔有率,到2024年將佔據35%的收益,這得益於尋求可配置系統並隨著3GPP版本發展的企業。它們的表現優於傳統的機架式分析儀,複合年成長率高達8.5%。 PXIe和AXIe刀片採用腳本化FPGA。美國國家儀器公司的PXIe-5842向量訊號收發器提供2 GHz頻寬,連續覆蓋範圍高達54 GHz,可在單一插槽中實現統一的生成和分析。租賃GP模式也得到了發展,尤其是在拉丁美洲,透過提供高級功能的訂閱訪問,無需資產攤銷,以滿足緊張的資本預算。半導體ATE雖然由於模組化工作台上分立通道數量的增加而導致市場佔有率略有下降,但對於大批量射頻設備製造商來說仍然至關重要。

傳統的通用儀器對於精密測量和需要絕對精度的政府實驗室來說仍然至關重要。但隨著軟體更新解鎖了新的調變格式,各公司開始轉向以卡片為基礎的架構,以避免堆高機式更新。供應商藍圖進一步強化了這種轉變,建議容器化的微服務,讓工程師可以按需下載測試專用程式。這種勢頭表明,模組化仍將是保持整個射頻測試設備市場競爭力的關鍵。

桌上型電腦機型在2024年將維持45%的市場佔有率,這得益於其無與倫比的動態範圍和低相位雜訊,這對於研發和校準至關重要。然而,模組化底盤的複合年成長率最高,達到9.2%,隨著服務團隊採用可擴展的通道數和小尺寸機箱,對射頻測試設備市場的整體成長做出了重大貢獻。是德科技將於2025年推出緊湊型54 GHz訊號產生器和合成器,顯示該公司在保持性能的同時,正在努力縮小傳統機箱的尺寸。

憑藉高效 GaN PA 級的整合和改進的熱路由,手持式分析儀現已支援在屋頂、石油平台和防禦靶場的安裝和維護。由於 40 GHz 以上頻段的散熱問題,其應用範圍有限,但現場工作人員對其電池供電的頻譜和雲端同步記錄功能非常欣賞,這些功能可以加速故障排除。隨著網路密集化和衛星閘道的普及,射頻測試設備市場越來越注重在精確度和移動性之間取得平衡,導致頂級供應商的產品策略趨於趨同。

區域分析

2024年,亞太地區將佔全球銷售額的39%,充分彰顯其在射頻測試設備市場的主導地位。中國的自力更生政策使其國內工具鏈煥發了活力,而日本和韓國則在雷達和半導體調查方法處於領先地位。高通、中國行動和小米使用驍龍X75展示了8.5 Gbps 5G Advanced毫米波測試平台,凸顯了該地區在擴增實境檢驗領域的領導地位。 300毫米晶圓廠的投資有所回升,台灣和中國當地的代工廠也擴大了高頻量產測試儀的生產。

北美按以金額為準排名第二。美國實驗室迅速採用雲端連接工作台來減輕射頻專家的壓力,而13億美元的國防預算分配給無人機系統對抗計劃,增加了對能夠即時威脅識別的寬頻分析儀的需求。加拿大的衛星閘道器建設進一步推動了Ka波段測試的預訂量。歐洲在汽車雷達方面的專業知識(例如德國)以及北歐地區嚴重的人才短缺,導致複雜的一致性任務活性化外包給第三方實驗室。

中東和非洲市場儘管規模較小,但複合年成長率最高,達8.7%。沙烏地阿拉伯計畫在2030年發展350億美元的太空經濟,催生了對Ka波段有效載荷和地面段檢驗的需求。阿拉伯聯合大公國的火星和小行星帶探測任務加速了頻道模擬器的採購。在南美洲,巴西通訊業者選擇短期租賃來進行700 MHz頻譜重耕計劃,這為射頻測試設備市場的供應商創造了一種自適應的市場進入模式,呈現出明顯的租賃偏好。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 毫米波 5G 部署快速成長,需要 24GHz 以上頻段檢驗

- 東亞大規模MIMO基地台部署

- 德國和日本的汽車雷達/ADAS測試需求

- 透過建構衛星低衛星群加速Ka波段測試

- 微型物聯網晶片組協助手持式射頻分析儀

- 美國轉向軟體定義、雲端連線實驗室的轉變

- 市場限制

- 由於 ETSI 和 3GPP 標準的快速發展而過時

- 40 GHz以上尺寸的散熱挑戰

- 北歐射頻測試工程師短缺

- 拉丁美洲的高資本投資與租賃偏好

- 價值/供應鏈分析

- 監管或技術格局

- 五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- 投資分析

- 宏觀經濟因素的影響

第5章市場規模及成長預測(金額)

- 按類型

- 模組化GP設備

- 常規GP測量儀

- 半導體ATE

- 租賃全科醫生

- 其他類型

- 外形規格

- 桌上型

- 可攜式的

- 模組化的

- 按頻率範圍

- 低於1 GHz

- 1-6 GHz

- 6 GHz以上

- 按組件

- 射頻分析儀

- 射頻振盪器

- 射頻合成器

- 射頻放大器

- 射頻探測器

- 其他組件

- 按最終用戶產業

- 通訊

- 航太/國防

- 消費性電子產品

- 車

- 半導體製造

- 衛生保健

- 工業和物聯網

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 瑞典

- 挪威

- 其他歐洲國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 北美洲

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Keysight Technologies Inc.

- Rohde & Schwarz GmbH & Co. KG

- Anritsu Corporation

- Viavi Solutions Inc.

- Yokogawa Electric Corporation

- Tektronix Inc.

- Teledyne Technologies Inc.

- National Instruments Corporation

- Fortive Corp.(Fluke)

- Teradyne Inc.

- Chroma ATE Inc.

- EXFO Inc.

- Cobham Ltd.

- TESSCO Technologies Inc.

- Advantest Corporation

- LitePoint Corporation

- Spirent Communications plc

- RIGOL Technologies Inc.

- Aim-TTi(Thurlby Thandar Instruments)

- Boonton Electronics

- SIGLENT Technologies

- GW Instek

- PMK Messtechnik

- Picotest Corp.

- B&K Precision Corporation

- TestEquity LLC

- Copper Mountain Technologies

- Giga-tronics Inc.

- Empirix Inc.

第7章 市場機會與未來展望

The RF test equipment market size was valued at USD 4.02 billion in 2025 and is forecast to reach USD 5.51 billion by 2030, registering a 6.52% CAGR over 2025-2030.

Uptake of 5G millimeter-wave links, the migration toward software-defined laboratories, and escalating radar and satellite programs all supported steady demand through 2024. Integration of GaN-on-Si power devices raised performance ceilings for amplifiers, while modular platforms compressed set-up times and operating costs. Asia-Pacific suppliers continued to scale output for domestic networks and export contracts, whereas North American laboratories prioritized cloud-connected automation to counter rising engineering labor shortages. Intensifying consolidation-highlighted by two separate bids for Spirent Communications-signalled an industry pivot toward turnkey hardware-software ecosystems that can evolve with 3GPP releases.

Global RF Test Equipment Market Trends and Insights

Surge in mmWave 5G Roll-outs Requiring >24 GHz Validation

Commercial roll-outs of 5G at 24-39 GHz demanded over-the-air chambers, phased-array beam verification, and wideband channel emulation. Keysight reported that integrated platforms combining generation, analysis, and fading cut test cycles by up to 40% and trimmed calibration overhead in research and development centers. Network operators in the United States, South Korea, and Germany placed bulk orders for 32- and 64-channel analyzers to validate beam-steering algorithms before dense-urban deployment. As mmWave small-cell density climbed, service labs shifted from single-box spectrum scans to automated, cloud-linked workflows that can sequence hundreds of parametric checks overnight. The trend pushed the RF test equipment market toward modular, FPGA-rich transceivers capable of 2 GHz instantaneous bandwidth per channel.

Proliferation of Massive-MIMO Base Stations in East Asia

China's and Japan's race to blanket metro areas with 64T64R radios created immediate needs for instruments that test dozens of RF chains concurrently. A 2024 RF Globalnet briefing cited 9.4 million new or upgraded sites worldwide, many of which employed massive-MIMO arrays. Multi-port vector signal analyzers with synchronized phase noise tracking enabled over-the-air characterization in a single pass, halving tower-side service times. East Asian OEMs further drove demand for PXIe blade sets that engineers can repurpose through software as 3GPP releases evolve. The swing toward flexible capacity underpinned the sustained growth of the RF test equipment market across production lines and field-service providers.

Rapidly Evolving ETSI and 3GPP Standards Creating Obsolescence

Release 18 of 3GPP entered freeze in June 2024, with Release 19 scheduled for late 2025. Each cycle introduced new air-interface features that legacy test sets could not easily emulate, forcing premature replacement or costly FPGA upgrades. Laboratories facing multi-standard certification workloads had to keep parallel benches for NR, LTE, and Wi-Fi, inflating operational budgets. While modular designs mitigated some risk, firmware licensing fees and retraining still curbed spending momentum within the RF test equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Automotive RADAR/ADAS Test Demand Across Germany and Japan

- Satellite LEO Constellation Build-outs Driving Ka-Band Tests

- Form-factor Heat-Dissipation Challenges >40 GHz

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Modular GP instruments captured 35% of 2024 revenue as organizations sought configurable systems that evolve with 3GPP releases, accounting for the largest slice of the RF test equipment market size at this layer. Their 8.5% CAGR outlook outpaced traditional rack-mount analyzers, which ceded ground to PXIe and AXIe blades housing scripted FPGAs. National Instruments' PXIe-5842 vector signal transceiver delivered continuous coverage to 54 GHz with 2 GHz bandwidth, enabling unified generation and analysis in one slot. Rental GP models also grew where capital budgets were tight, especially in Latin America, offering subscription access to advanced capability without depreciating assets. Semiconductor ATE stayed essential for high-volume RF device makers, though its share narrowed modestly as discrete-channel counts rose on modular benches.

Conventional general-purpose instruments remained vital for precision metrology and government labs requiring absolute accuracy. Yet as software updates unlocked new modulation formats, enterprises gravitated toward card-based architectures that avoided forklift refreshes. Vendor roadmaps hinted at containerized microservices that would let engineers download test personalities on demand, further reinforcing the shift. This momentum suggests modularity will stay central to maintaining competitiveness across the broader RF test equipment market.

Benchtop units retained a 45% share in 2024, underpinned by unmatched dynamic range and low phase noise-qualities indispensable for research and development and calibration. Nevertheless, modular chassis logged the fastest 9.2% CAGR as service teams embraced scalable channel counts and smaller footprints, contributing measurably to overall RF test equipment market growth. Keysight's 2025 release of compact 54 GHz signal generators and synthesizers illustrated the push to shrink conventional boxes while preserving performance.

Handheld analyzers advanced through the integration of high-efficiency GaN PA stages and improved thermal paths to support installation and maintenance on rooftops, oil platforms, and defense ranges. Although thermal concerns above 40 GHz moderated adoption, field crews valued battery-operated spectrum capture and cloud-sync logs that accelerated troubleshooting. As networks densified and satellite gateways proliferated, the RF test equipment market increasingly balanced precision with mobility, driving converged product strategies among the top suppliers.

The RF Test Equipment Market is Segmented by Product Type (Modular GP Instrumentation, and More), by Form Factor (Benchtop, Portable, and More), by Frequency Range (< 1 GHz, 1 - 6 GHz, and More), by Component (RF Analyzers, RF Oscillators, and More), by End-User Industries (Telecommunication, Aerospace and Defense, and More), and by Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific commanded 39% of global revenue in 2024, underscoring its pre-eminence within the RF test equipment market. China's self-reliance agenda fuelled domestic tool chains, while Japan and South Korea pioneered radar and semiconductor test methodologies. Qualcomm, China Mobile, and Xiaomi demonstrated an 8.5 Gbps 5G Advanced mmWave testbed using the Snapdragon X75, spotlighting regional leadership in extended-reality validation. Heavy investment in 300 mm fabs expanded pull-through for high-frequency production testers across Taiwan and mainland foundries.

North America ranked second by value. U.S. labs rapidly adopted cloud-connected benches to mitigate a tightening pool of RF specialists, and defense allocations of USD 1.3 billion for counter-UAS projects spurred demand for wideband analyzers capable of real-time threat identification. Canada's satellite gateway build-outs further lifted Ka-band test bookings. Europe followed closely, anchored by Germany's automotive radar expertise and the Nordic region's acute talent shortages, which encouraged the outsourcing of complex conformance tasks to third-party labs.

The Middle East and Africa segment, while smaller, posted the fastest 8.7% CAGR. Saudi Arabia's plan to develop a USD 35 billion space economy by 2030 created demand for Ka-band payload and ground-segment validation. The UAE's missions to Mars and the asteroid belts accelerated the procurement of channel emulators. South America exhibited distinct rental preferences as Brazilian carriers opted for short-term leases during 700 MHz refarming projects, shaping adaptive go-to-market models for suppliers within the RF test equipment market.

- Keysight Technologies Inc.

- Rohde & Schwarz GmbH & Co. KG

- Anritsu Corporation

- Viavi Solutions Inc.

- Yokogawa Electric Corporation

- Tektronix Inc.

- Teledyne Technologies Inc.

- National Instruments Corporation

- Fortive Corp. (Fluke)

- Teradyne Inc.

- Chroma ATE Inc.

- EXFO Inc.

- Cobham Ltd.

- TESSCO Technologies Inc.

- Advantest Corporation

- LitePoint Corporation

- Spirent Communications plc

- RIGOL Technologies Inc.

- Aim-TTi (Thurlby Thandar Instruments)

- Boonton Electronics

- SIGLENT Technologies

- GW Instek

- PMK Messtechnik

- Picotest Corp.

- B&K Precision Corporation

- TestEquity LLC

- Copper Mountain Technologies

- Giga-tronics Inc.

- Empirix Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in mmWave 5G Roll-outs Requiring >24 GHz Validation

- 4.2.2 Proliferation of Massive-MIMO Base-Stations in East Asia

- 4.2.3 Automotive RADAR/ADAS Test Demand Across Germany and Japan

- 4.2.4 Satellite LEO Constellation Build-outs Driving Ka-Band Tests

- 4.2.5 Miniaturised IoT Chipsets Boosting Hand-held RF Analyzers

- 4.2.6 Migration to Software-Defined, Cloud-Connected Labs in US

- 4.3 Market Restraints

- 4.3.1 Rapidly Evolving ETSI and 3GPP Standards Creating Obsolescence

- 4.3.2 Form-factor Heat-Dissipation Challenges >40 GHz

- 4.3.3 Skilled RF Test Engineering Talent Shortage in Nordics

- 4.3.4 High Cap-Ex vs. Rental Preference in Latin America

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Analysis

- 4.8 Impact of Macroeconomic factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Modular GP Instrumentation

- 5.1.2 Traditional GP Instrumentation

- 5.1.3 Semiconductor ATE

- 5.1.4 Rental GP

- 5.1.5 Other Types

- 5.2 By Form Factor

- 5.2.1 Benchtop

- 5.2.2 Portable

- 5.2.3 Modular

- 5.3 By Frequency Range

- 5.3.1 < 1 GHz

- 5.3.2 1 - 6 GHz

- 5.3.3 > 6 GHz

- 5.4 By Component

- 5.4.1 RF Analyzers

- 5.4.2 RF Oscillators

- 5.4.3 RF Synthesizers

- 5.4.4 RF Amplifiers

- 5.4.5 RF Detectors

- 5.4.6 Other Components

- 5.5 By End-user Industry

- 5.5.1 Telecommunication

- 5.5.2 Aerospace and Defense

- 5.5.3 Consumer Electronics

- 5.5.4 Automotive

- 5.5.5 Semiconductor Manufacturing

- 5.5.6 Healthcare

- 5.5.7 Industrial and IoT

- 5.5.8 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Sweden

- 5.6.3.6 Norway

- 5.6.3.7 Rest of Europe

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Rest of Africa

- 5.6.5 Asia-Pacific

- 5.6.5.1 China

- 5.6.5.2 Japan

- 5.6.5.3 India

- 5.6.5.4 South Korea

- 5.6.5.5 Rest of Asia-Pacific

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Keysight Technologies Inc.

- 6.4.2 Rohde & Schwarz GmbH & Co. KG

- 6.4.3 Anritsu Corporation

- 6.4.4 Viavi Solutions Inc.

- 6.4.5 Yokogawa Electric Corporation

- 6.4.6 Tektronix Inc.

- 6.4.7 Teledyne Technologies Inc.

- 6.4.8 National Instruments Corporation

- 6.4.9 Fortive Corp. (Fluke)

- 6.4.10 Teradyne Inc.

- 6.4.11 Chroma ATE Inc.

- 6.4.12 EXFO Inc.

- 6.4.13 Cobham Ltd.

- 6.4.14 TESSCO Technologies Inc.

- 6.4.15 Advantest Corporation

- 6.4.16 LitePoint Corporation

- 6.4.17 Spirent Communications plc

- 6.4.18 RIGOL Technologies Inc.

- 6.4.19 Aim-TTi (Thurlby Thandar Instruments)

- 6.4.20 Boonton Electronics

- 6.4.21 SIGLENT Technologies

- 6.4.22 GW Instek

- 6.4.23 PMK Messtechnik

- 6.4.24 Picotest Corp.

- 6.4.25 B&K Precision Corporation

- 6.4.26 TestEquity LLC

- 6.4.27 Copper Mountain Technologies

- 6.4.28 Giga-tronics Inc.

- 6.4.29 Empirix Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

全球射頻測試系統(雷達、敵我識別、雷達警報接收機、導航輔助設備)市場:2026-2036年

全球射頻測試系統(雷達、敵我識別、雷達警報接收機、導航輔助設備)市場:2026-2036年 射頻測試設備市場:2026-2032年全球市場預測(依產品類型、最終用戶產業、技術、頻段、測試類型和連接埠數量分類)

射頻測試設備市場:2026-2032年全球市場預測(依產品類型、最終用戶產業、技術、頻段、測試類型和連接埠數量分類) 全球射頻測試設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球射頻測試設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 5G射頻組件市場分析及預測(至2035年):類型、產品、技術、組件、應用、部署、最終用戶、模組、功能、安裝配置

5G射頻組件市場分析及預測(至2035年):類型、產品、技術、組件、應用、部署、最終用戶、模組、功能、安裝配置 2026年全球射頻測試設備市場報告雷達高度計測試設備市場按產品類型、測試類型、應用和最終用戶分類 - 全球預測 2026-2032

2026年全球射頻測試設備市場報告雷達高度計測試設備市場按產品類型、測試類型、應用和最終用戶分類 - 全球預測 2026-2032 射頻測試設備市場規模、佔有率和成長分析(按類型、外形規格、頻率範圍、最終用途和地區分類)-2026-2033年產業預測

射頻測試設備市場規模、佔有率和成長分析(按類型、外形規格、頻率範圍、最終用途和地區分類)-2026-2033年產業預測 射頻測試設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測射頻測試夾具市場按組件、類型、頻率範圍、最終用途和最終用戶分類 - 2025 年至 2030 年全球預測

射頻測試設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測射頻測試夾具市場按組件、類型、頻率範圍、最終用途和最終用戶分類 - 2025 年至 2030 年全球預測 RF試驗設備市場:各類型(頻譜分析儀,信號發電機,網路分析儀),不同形態,各頻波帶,各終端用戶(汽車,消費者電子產品,航太·防衛),各地區 - 2031年前的世界預測

RF試驗設備市場:各類型(頻譜分析儀,信號發電機,網路分析儀),不同形態,各頻波帶,各終端用戶(汽車,消費者電子產品,航太·防衛),各地區 - 2031年前的世界預測