|

市場調查報告書

商品編碼

1836502

智慧聚合物:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030)Smart Polymers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

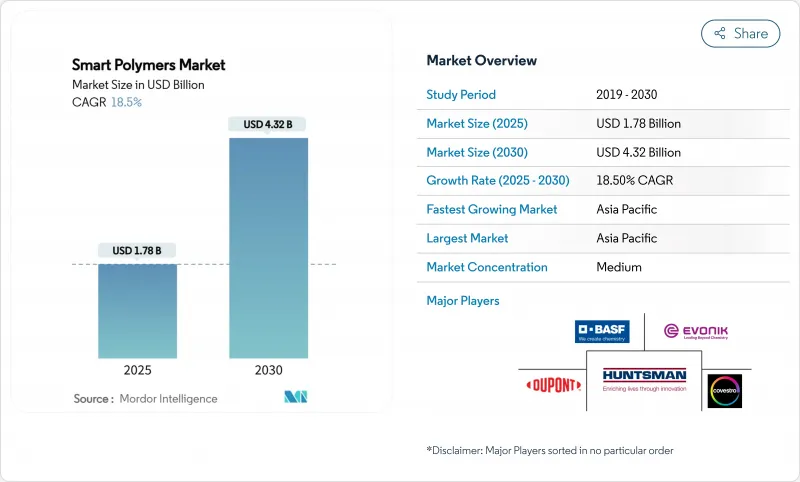

智慧聚合物市場規模預計在 2025 年達到 17.8 億美元,預計到 2030 年將達到 43.2 億美元,預測期內(2025-2030 年)的複合年成長率為 18.5%。

這一發展勢頭的推動因素包括材料化學領域的快速突破、微創醫療解決方案需求的激增,以及消費性電子、紡織品和移動領域中響應性聚合物加速取代被動塑膠。由於中國、日本和韓國強大的製造業基礎和政府支持的研發支出,亞太地區已成為重要的生產和消費中心。供應商正在將產品系列從單觸發系統擴展至多觸發系統,以滿足業界對可調剛度、自主修復和內建導電性的需求。同時,資本高效的規模化技術(連續流反應器、精密擠出和人工智慧引導的複合)正在縮小與傳統工程塑膠的成本差距,從而擴大其在包裝和服裝等價值驅動型應用中的應用。

全球智慧聚合物市場趨勢與洞察

形狀記憶聚合物在紡織業的應用不斷擴大

紡織品製造商正在將形狀記憶聚合物 (SMP) 嵌入織物中,透過隨溫度變化而收縮和舒張來主動調節舒適度。休閒品牌現在指定使用 SMP 混紡布料,這種布料在高溫條件下吸濕排汗,並在環境溫度下降時增加編織密度,從而穩定穿著者周圍的微氣候。 SRTX 實驗室展示了一種重新設計的用於針織品的彈道級 SMP,其強度是鋼的 10 倍,重量比水輕,並整合了抗菌功能,無需局部塗層。不列顛哥倫比亞大學的一個團隊正在印製低成本的壓敏電阻陣列,用於捕捉步態動態和生命徵象,將連帽衫和壓縮袖改造成醫療設備。

自修復塗層的需求

電子、汽車和工業原始設備製造商 (OEM) 正在從手動重新噴漆和過度工程轉向能夠自主修復刮痕、微裂紋和針孔的塗層。在 Cicoira 的突破性研究中,摻雜乙二醇和單寧酸的 PEDOT:PSS 薄膜在 90% 拉伸應變下恢復電氣完整性,即使經過反覆切割也能保持接近 17 S cm-1 的電導率。此配方可黏附在金屬、聚烯和熱塑性聚氨酯上,為共形感測器、軟性電池和耐腐蝕建築面板的研發鋪平了道路。

製造成本高且規模擴大複雜

實驗室批量製程依賴精密催化劑、低溫進料和多級淨化。由於黏度變化和副反應,噸級反應器的放大會降低重現性,導致單位成本高於工程聚合物。連續流合成和反應擠出生產線有望節省成本,但對於中小型公司來說仍然是資本密集的,這減緩了它們進入低利潤包裝和鞋類市場的速度。

報告中分析的其他促進因素和限制因素

- 亞洲穿戴式電子產品熱潮

- 歐盟強制汽車使用輕質複合材料

- 臨床核准的監管不確定性

細分分析

儘管目前銷售額較小,但生物刺激響應類產品正以22.7%的複合年成長率加速成長,因為藥物傳輸專家利用酵素、葡萄糖和抗原觸發劑進行標靶釋放。物理刺激響應類產品仍佔智慧聚合物市場佔有率的41%,其中以用於航太整流罩和智慧窗戶的形狀記憶合金和感溫變色塗層為主導。

透過將pH值和氧化還原敏感性整合到單一聚合物骨架中,調查團隊旨在實現化療藥物僅在腫瘤微環境中局部釋放,從而降低全身毒性。此混合平台採用印跡識別基團,可模擬抗體,同時經受滅菌循環。這種可客製化吸引了診斷公司將這些聚合物整合到即時診斷生物感測器中。

區域分析

亞太地區佔智慧聚合物市場的35%,成長最快,複合年成長率達19.6%。中國的「中國製造2025」計畫已將反應性材料列為戰略支柱,並為國內生產線提供稅收優惠。一家日本企業集團正在開發基於離聚物的SEBS共混物,用於遊戲服中的觸覺回饋致動器,而一家領先的韓國電子公司正在聯合開發用於折疊式顯示器的可拉伸電路油墨。

北美津貼了美國國立衛生研究院 (NIH) 和美國國防高級研究計劃局 (DARPA) 的資助,用於生物可吸收支架和智慧縫合線,波士頓和舊金山灣區則是醫療設備新興企業和專門從事 GMP 級智慧聚合物擠壓的受託製造廠商的叢集。

歐洲嚴格的永續性指令正在推動對可回收和可生物分解等級的需求,而「地平線歐洲」計劃支持生物基熱可塑性橡膠實現閉合迴路回收,符合汽車製造商的脫碳目標。

雖然南美洲和中東和非洲市場仍在發展中,但巴西的整形外科植入製造商和阿拉伯聯合大公國的智慧城市計劃已率先採用濕度響應密封劑和溫度調節建築幕牆面板。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場狀況

- 市場概況

- 市場促進因素

- 形狀記憶聚合物在紡織業的應用不斷擴大

- 自修復塗層的需求

- 穿戴式電子產品的繁榮推動了導電智慧聚合物的發展(亞洲)

- 歐盟汽車輕量化指令

- NASA 和 ESA 在航太採用 4D 列印

- 市場限制

- 製造成本高且規模擴大複雜

- 臨床核准的監管不確定性

- 多組分智慧聚合物缺乏回收途徑

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模及成長預測(金額)

- 按類型

- 身體刺激反應類型

- 化學刺激反應類型

- 對生物刺激有反應

- 自修復聚合物

- 其他智慧聚合物類型

- 按最終用戶產業

- 生物醫學保健

- 電氣和電子

- 紡織品

- 車

- 其他產業(能源與電力、包裝、石油與天然氣、建築)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲地區

- 亞太地區

第6章 競爭態勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF

- Covestro AG

- Dow

- DuPont

- Evonik Industries, AG

- Huntsman International LLC

- Mitsubishi Chemical Group Corporation

- SABIC

- SMP Technologies Inc

- Spintech Holdings Inc.

- The Lubrizol Corporation

第7章 市場機會與未來展望

The Smart Polymers Market size is estimated at USD 1.78 billion in 2025, and is expected to reach USD 4.32 billion by 2030, at a CAGR of 18.5% during the forecast period (2025-2030).

Momentum comes from rapid breakthroughs in materials chemistry, surging demand for minimally invasive healthcare solutions, and the accelerating replacement of passive plastics with responsive polymers in consumer electronics, textiles, and mobility. Asia-Pacific's strong manufacturing base and government-backed research and development spending in China, Japan, and South Korea position the region as the primary production and consumption hub. Suppliers are diversifying product portfolios from single-trigger to multi-trigger systems to meet industry calls for tunable stiffness, autonomous healing, and embedded conductivity. Concurrently, capital-efficient scale-up technologies-continuous flow reactors, precision extrusion, and AI-guided formulation are narrowing the cost gap with conventional engineering plastics, widening adoption prospects in value-conscious sectors such as packaging and apparel.

Global Smart Polymers Market Trends and Insights

Increasing Application of Shape-Memory Polymers in the Textile Industry

Textile producers are embedding shape-memory polymers (SMPs) into fibers that actively regulate comfort by contracting or relaxing with temperature changes. Athleisure brands now specify SMP-blended yarns that wick moisture in high-heat conditions and tighten weave density when ambient temperatures fall, maintaining a stable microclimate around the wearer. SRTX Labs demonstrated ballistic-grade SMPs re-engineered for knits that are 10 times stronger than steel and lighter than water, integrating antimicrobial functionality without topical coatings. Universities are coupling SMP substrates with flexible sensor threads; a University of British Columbia team printed low-cost piezoresistive arrays that capture gait dynamics and vital signs, turning hoodies and compression sleeves into medical devices.

Self-Healing Coatings Demand

Electronics, automotive, and industrial OEMs are shifting from manual repainting and over-engineering toward coatings that autonomously repair scratches, micro-cracks, and pinholes. A landmark study by Cicoira produced PEDOT: PSS films doped with ethylene glycol and tannic acid that recover electrical integrity after 90% tensile strain, sustaining conductivity near 17 S cm-1 even after repeated cuts. The formulation adheres to metals, polyolefins, and thermoplastic polyurethanes, opening pathways in conformal sensors, flexible batteries, and corrosion-resistant architectural panels.

High Production Cost and Scale-up Complexity

Laboratory batches rely on precision catalysts, cryogenic feeds, and multi-step purification. When scaled to tonne-level reactors, viscosity changes and side reactions hamper reproducibility, inflating unit costs beyond engineering polymers. Continuous-flow synthesis and reactive-extrusion lines promise cost compression, yet capital intensity remains high for SMEs, slowing entry into low-margin packaging and footwear markets.

Other drivers and restraints analyzed in the detailed report include:

- Wearable-Electronics Boom in Asia

- EU Lightweight-Composites Mandates in Automotive

- Regulatory Uncertainty for Clinical Approvals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Though smaller in revenue today, the biological stimuli-responsive category is accelerating with a 22.7% CAGR as drug-delivery specialists exploit enzyme, glucose, and antigen triggers for targeted release. Physical stimuli-responsive grades still dominate 41% of the Smart Polymers market share, anchored by shape-memory alloys and thermochromic coatings specified in aerospace fairings and smart windows.

Researchers are merging pH and redox sensitivity into a single polymer backbone, enabling localized chemotherapeutic release only in the tumor micro-environment, reducing systemic toxicity. Hybrid platforms employ imprinted recognition sites that emulate antibodies yet withstand sterilization cycles. Such customizability is attracting diagnostics firms that embed these polymers into point-of-care biosensors.

The Smart Polymers Market Report Segments the Industry by Type (Physical Stimuli-Responsive, Chemical Stimuli-Responsive, Biological Stimuli-Responsive, Self-Healing Polymers, and Others), End-User Industry (Biomedical and Healthcare, Electrical and Electronics, Textile, Automotive, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific leads with 35% of Smart Polymers market revenue and exhibits the fastest regional growth at 19.6% CAGR. China's "Made in China 2025" program earmarks responsive materials as a strategic pillar, granting tax rebates for domestic production lines. Japanese conglomerates scale ionomer-based SEBS blends for haptic feedback actuators in gaming suits, while South Korean electronics giants co-develop stretchable circuit inks for foldable displays.

North America is backed by NIH and DARPA grants, funding bioresorbable stents and smart sutures. Collaborative clusters around Boston and the San Francisco Bay Area pair medical-device start-ups with contract manufacturing organizations that specialize in GMP-grade smart polymer extrusion.

Europe enforces stringent sustainability directives, catalyzing demand for recyclable and biodegradable grades. Horizon Europe projects sponsor bio-based thermoplastic elastomers designed for closed-loop recovery, aligning with automotive OEM decarbonization targets.

South America and MEA markets remain nascent, yet Brazil's orthopedic-implant makers and the UAE's smart-city initiatives are early adopters of moisture-responsive sealants and temperature-modulating facade panels.

- BASF

- Covestro AG

- Dow

- DuPont

- Evonik Industries, AG

- Huntsman International LLC

- Mitsubishi Chemical Group Corporation

- SABIC

- SMP Technologies Inc

- Spintech Holdings Inc.

- The Lubrizol Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Application of Shape Memory Polymer in Textile Industry

- 4.2.2 Self-Healing Coatings Demand

- 4.2.3 Wearable-Electronics Boom Accelerating Conductive Smart Polymers (Asia)

- 4.2.4 EU Lightweight-Composites Mandates in Automotive

- 4.2.5 4-D Printing Adoption in Aerospace by NASA and ESA

- 4.3 Market Restraints

- 4.3.1 High Production Cost and Scale-up Complexity

- 4.3.2 Regulatory Uncertainty for Clinical Approvals

- 4.3.3 Lack of Recycling Pathways for Multi-Component Smart Polymers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Physical Stimuli-Responsive

- 5.1.2 Chemical Stimuli-Responsive

- 5.1.3 Biological Stimuli-Responsive

- 5.1.4 Self-Healing Polymers

- 5.1.5 Other Smart Polymer Types

- 5.2 By End-User Industry

- 5.2.1 Biomedical and Healthcare

- 5.2.2 Electrical and Electronics

- 5.2.3 Textile

- 5.2.4 Automotive

- 5.2.5 Other Industries (Energy and Power, Packaging, Oil and Gas, Construction)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Covestro AG

- 6.4.3 Dow

- 6.4.4 DuPont

- 6.4.5 Evonik Industries, AG

- 6.4.6 Huntsman International LLC

- 6.4.7 Mitsubishi Chemical Group Corporation

- 6.4.8 SABIC

- 6.4.9 SMP Technologies Inc

- 6.4.10 Spintech Holdings Inc.

- 6.4.11 The Lubrizol Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

智慧聚合物市場:按類型、形態和應用分類-2026-2032年全球市場預測

智慧聚合物市場:按類型、形態和應用分類-2026-2032年全球市場預測 2026年全球智慧聚合物市場報告

2026年全球智慧聚合物市場報告 智慧聚合物市場規模、佔有率和成長分析(按類型、最終用途產業和地區分類)—產業預測(2026-2033 年)

智慧聚合物市場規模、佔有率和成長分析(按類型、最終用途產業和地區分類)—產業預測(2026-2033 年) 智慧紡織聚合物市場規模、佔有率和趨勢分析報告:按產品類型、最終用途、地區和細分市場預測(2025-2033 年)

智慧紡織聚合物市場規模、佔有率和趨勢分析報告:按產品類型、最終用途、地區和細分市場預測(2025-2033 年) 全球智慧聚合物市場-2025-2030年預測溫度響應聚合物市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)濕度響應型聚合物市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)

全球智慧聚合物市場-2025-2030年預測溫度響應聚合物市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年)濕度響應型聚合物市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2025-2033 年) 智慧聚合物市場規模、佔有率、趨勢及預測(按類型、刺激因素、應用和地區),2025 年至 2033 年

智慧聚合物市場規模、佔有率、趨勢及預測(按類型、刺激因素、應用和地區),2025 年至 2033 年 智慧聚合物市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用途、地區和競爭情況細分,2020-2030 年)

智慧聚合物市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用途、地區和競爭情況細分,2020-2030 年) 智慧聚合物市場:產業趨勢·全球預測 (~2035年):聚合物類型·刺激類型·終端用戶·各地區

智慧聚合物市場:產業趨勢·全球預測 (~2035年):聚合物類型·刺激類型·終端用戶·各地區