|

市場調查報告書

商品編碼

1694009

薄膜電池-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Thin Film Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

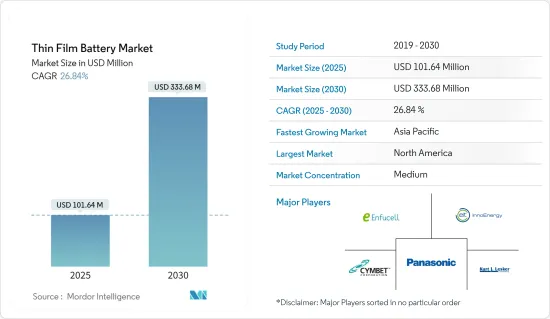

薄膜電池市場規模預計在 2025 年為 1.0164 億美元,預計到 2030 年將達到 3.3368 億美元,預測期內(2025-2030 年)的複合年成長率為 26.84%。

關鍵亮點

- 從中期來看,家用電子電器領域對薄膜技術的需求不斷增加,加上物聯網(IoT)應用的滲透,預計將推動薄膜電池市場的需求。

- 然而,替代電池技術的出現預計將阻礙市場成長。

- 該電池重量輕、設計緊湊等特點非常適合軍事應用,預計將為薄膜電池市場創造巨大的機會。

- 亞太地區佔據市場主導地位,並可能在預測期內實現最高的複合年成長率。這種成長主要歸因於人們對折疊式電子產品和穿戴式裝置的日益關注,尤其是在中國、韓國和日本等經濟體。

薄膜電池市場趨勢

消費性電子主導的市場細分

- 由於家用電子電器對小型、輕巧、高效電源的需求不斷成長,預計該領域將主導薄膜電池市場。智慧型手機、穿戴式裝置和平板電腦等行動裝置的普及正在迅速增加對緊湊、靈活的能源解決方案的需求。

- 此外,由於智慧型手錶、穿戴式健康監測設備和智慧眼鏡等消費性電子產品的出貨量不斷增加,預計在預測期內可攜式電池在全球範圍內將顯著成長。根據國際數據公司(IDC)的數據顯示,自2009年以來,全球智慧型手機出貨量成長了5.7倍。

- 家用電子電器小型化的趨勢要求高效率的電源供應器能夠適應各種特性和設計要求。薄膜電池因其薄度、靈活性和可自訂的尺寸完美地滿足了這一需求,並有助於無縫整合到綜合家用電子電器產品中。

- 例如,2023年8月,德國和英國大學的一群科學家宣布他們完成了T-Nb2O5薄膜的開發。這項突破意味著電池的潛在改進、計算和照明技術的進步以及消費性電子產品的重大進步。預測顯示電池能量密度和充電週期將有所改善,為消費性電子產業帶來了巨大的前景。

- 此外,不斷變化的消費者偏好強調了對便利性、更長的設備壽命和更永續的能源解決方案的渴望。薄膜電池具有提高能量密度和延長循環壽命的潛力,與傳統笨重電池相比,它可以延長設備的使用壽命並減少對環境的影響,從而滿足消費者的需求。

- 家用電子電器的市場主導地位也受到這些設備在全球範圍內日益普及的推動,尤其是在新興經濟體中。這些地區不斷成長的消費者群體要求設備的電源不僅價格實惠,而且可靠耐用。

- 因此,鑑於上述情況,預計消費性電子市場部分將在預測期內佔據市場主導地位。

亞太地區可望成為成長最快的地區

- 預計亞太地區薄膜電池市場將顯著成長。其中一個關鍵促進因素是中國、日本、韓國和印度等國家快速成長的家用電子電器產業。

- 含有陶瓷電解質的薄膜電池稱為陶瓷電池。陶瓷材料具有強共用鍵,使其具有高熔點,使這些電池能夠在極高的溫度下運作。與其他電池技術相比,電動車中使用陶瓷電池具有多種優勢。根據國際能源總署的預測,2022年電動車總銷量將達到1,000多萬輛,主要集中在亞太地區。到 2022 年,電動車將佔所有新車銷量的 14%,高於 2021 年的約 9% 和 2020 年的不到 5%。

- 穿戴式裝置可能成為薄膜電池的重要消費者,其中中國市場將顯著成長。例如,根據國際數據公司(IDC)的數據顯示,2023年第三季中國穿戴裝置出貨量年增7.5%,達到3,470萬台。其中,7-9月耳掛型設備出貨量年增9.8%,超過1,924萬台。

- 此外,亞太地區的快速工業化和技術進步為薄膜電池技術相關研發活動的重大創新和投資鋪平了道路。

- 過去幾年,穿戴式裝置在印度的普及取得了顯著進展,預計將繼續成為一個有吸引力的終端使用產業。例如,根據國際數據公司(IDC)的預測,到2023年,印度穿戴式裝置市場預計將成長34%,達到1.342億台。穿戴式裝置的平均售價下降了15%以上,至21.2美元。這種情況可能會導致此類設備的採用率增加,並繼續為許多軟小型電池帶來一個有吸引力的市場。

- 2023年4月,印度政府核准了《2023年國家醫療設備政策》。該措施將促進醫療設備產業的發展,以實現醫療設備的可及性、品質、可負擔性和創新性的公共衛生目標。此外,透過重點建立強力的法規結構和創新、制定發展製造業生態系統的策略以及透過培訓和能力建設計劃提供支持,該行業有望發揮其潛力。鼓勵國內投資和醫療設備製造是對印度政府「自力更生印度」和「印度製造」計畫的補充。

- 例如,2023年2月,日本政府公佈了總額為25.5億美元的電池戰略預算,用於研發多種新型電池技術,包括全固體鋰電池、薄膜電池以及各種新興電池技術。預計舉措將加強日本在電池技術領域的地位。

- 此外,亞太地區強大的製造能力,加上良好的法規環境和強大的供應鏈基礎設施,使其成為薄膜電池製造的中心。具有成本效益的製造流程、不斷增加的技術進步投資以及對環保能源來源的日益重視,正在加強該地區在薄膜電池市場中的地位。

- 因此,鑑於上述情況,預計亞太地區在預測期內將顯著成長。

薄膜電池產業概況

薄膜電池市場正朝向半固體發展。該市場的主要企業(不分先後順序)包括 Enfucell OY Ltd.、EIT InnoEnergy SE、Cymbet Corporation, Inc.、Kurt J. Lesker Company 和 Panasonic Corporation。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究範圍

- 市場定義

- 調查前提

第2章調查方法

第3章執行摘要

第4章 市場概述

- 介紹

- 至2029年的市場規模及需求預測(單位:美元)

- 近期趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 消費性電子領域對薄膜技術的需求不斷成長

- 物聯網應用的成長

- 限制因素

- 替代電池技術的可用性

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場分類

- 電池類型

- 可充電的

- 不可充電

- 科技

- 印刷電池

- 陶瓷電池

- 鋰聚合物電池

- 其他

- 應用

- 消費性電子產品

- 醫療設備

- 穿戴式科技

- 智慧卡

- RFID

- 其他

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 北歐的

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 卡達

- 埃及

- 其他中東和非洲地區

- 南美洲

- 巴西

- 哥倫比亞

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- Companies Profiles

- EIT InnoEnergy SE

- Enfucell OY Ltd.

- Kurt J. Lesker Company

- Cymbet Corporation, Inc.

- Imprint Energy, Inc.

- Ilika Plc

- STMicroelectronics

- BASQUEVOLT

- The Batteries Sp. z o. o

- Panasonic Corporation

- 市場排名分析

第7章 市場機會與未來趨勢

- 擴大軍事和國防應用

簡介目錄

Product Code: 50001739

The Thin Film Battery Market size is estimated at USD 101.64 million in 2025, and is expected to reach USD 333.68 million by 2030, at a CAGR of 26.84% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, increasing demand for thin film technology in the consumer electronics sector, coupled with the penetration of Internet of Things (IoT) applications, is expected to increase the demand for the thin film battery market.

- On the other hand, the availability of alternate battery technologies is expected to hinder market growth.

- Nevertheless, the characteristics of these batteries, such as lightweight and compact designs, make them suitable for military applications, which is expected to create enormous opportunities for the thin film battery market.

- The Asia-Pacific region dominates the market and is also likely to register the highest CAGR during the forecast period. The growth is mainly due to the increasing emphasis on foldable electronics and wearables, especially across economies such as China, South Korea, and Japan.

Thin Film Battery Market Trends

Consumer Electronics Segment to Dominate the Market

- Consumer electronics are anticipated to dominate the thin film battery market due to the increasing demand for smaller, lighter, and more efficient power sources in this sector. The proliferation of portable devices, such as smartphones, wearables, and tablets, has led to a burgeoning need for compact and flexible energy solutions.

- Moreover, with the increased shipments of consumer electronics, such as smart watches, wearable health monitoring devices, and smart glasses, portable batteries are expected to witness tremendous growth globally during the forecast period. According to International Data Corporation (IDC), smartphone Shipments across the globe increased 5.7 times compared to 2009.

- The tendency toward miniaturization in consumer electronics has resulted in a need for efficient power sources that can adapt to diverse characteristics and design requirements. Thin-film batteries, with their thinness, flexibility, and customizable shapes, perfectly meet this demand, facilitating their seamless integration into a comprehensive array of consumer electronic gadgets.

- For instance, in August 2023, a group of scientists from German and British universities announced that they had completed the development of T-Nb2O5 thin films, facilitating the accelerated movement of Li-ion, a noteworthy stride forward. This breakthrough holds the potential for enhanced batteries and progress in computing and lighting, signifying a considerable advancement in consumer electronics. Forecasts suggest a boost in battery energy density and recharge cycles, offering substantial prospects in the consumer electronics sector.

- Moreover, the evolving landscape of consumer preferences emphasizes convenience, longer device lifespans, and a desire for more sustainable energy solutions. Thin film batteries, with their potential for improved energy density and longer cycle life, meet these consumer demands by offering extended device usage and reduced environmental impact compared to traditional bulky batteries.

- The market's dominance by consumer electronics is also influenced by the expanding global penetration of these devices, especially in emerging economies. The increasing consumer base in these regions demands devices that are not only affordable but also equipped with reliable and durable power sources.

- Therefore, as per the points mentioned above, the consumer electronics market segment is expected to dominate the market during the forecast period.

Asia-Pacific to be the Fastest-Growing Region

- The Asia-Pacific region is poised to witness remarkable growth in the thin film battery market, attributed to various factors contributing to its expanding dominance in this sector. One of the primary driving forces is the burgeoning consumer electronics industry in countries like China, Japan, South Korea, and India.

- Thin film batteries, which contain ceramic electrolytes, are known as ceramic batteries. Ceramic materials have high melting points due to their strong covalent bonds, which allows these batteries to operate at very high temperatures. Using ceramic batteries in electric vehicles has several advantages compared to other battery technology. According to IEA, the total electric car sales reached more than 10 million in 2022, led by the Asia Pacific region. A total of 14% of all new cars sold were electric in 2022, up from around 9% in 2021 and less than 5% in 2020.

- Wearable devices will likely emerge as significant consumers of thin film batteries and are witnessing substantial growth in China. For instance, according to the International Data Corporation (IDC), China's shipments of wearable devices went up 7.5% year on year to reach 34.7 million units in the third quarter (Q3) of 2023. In July-September, China shipped over 19.24 million units of ear-worn devices, an expansion of 9.8% year on year.

- Furthermore, the rapid industrialization and technological advancements in the Asia Pacific region have paved the way for substantial innovations and investments in research and development activities related to thin film battery technologies.

- Wearable devices have been experiencing considerable adoption over the past few years in India, and it is anticipated they will remain an attractive potential end-use application industry. For instance, according to the International Data Corporation (IDC), the Indian wearable market saw a 34% growth, recording 134.2 million units in 2023. The average selling price of wearables dropped over 15% to USD 21.2. This scenario will likely increase the adoption of such devices and remain an attractive market for many flexible small batteries.

- In April 2023, the Government of India approved the National Medical Devices Policy, 2023, which will likely facilitate the growth of the medical device sector to meet the public health objectives of access, quality, affordability, and innovation. Further, this sector is expected to realize its potential, with strategies for developing an enabling ecosystem for manufacturing, focusing on creating a robust regulatory framework and innovation and offering support through training and capacity-building programs. Encouraging domestic investments and medical device production complements the Indian government's Atmanirbhar Bharat and Make in India programs.

- For instance, the Japanese government revealed in February 2023 a battery strategy budget totaling USD 2.55 billion designated for the research and development of new battery technologies, encompassing diverse types such as all-solid-state lithium batteries, thin film batteries, and a range of emerging battery technologies. This initiative is anticipated to bolster Japan's position in the realm of battery technology.

- Moreover, the Asia-Pacific region's strong manufacturing capabilities, coupled with a favorable regulatory environment and a robust supply chain infrastructure, position it as a hub for thin-film battery production. Cost-effective manufacturing processes, increasing investments in technological advancements, and a growing emphasis on environmentally friendly energy sources reinforce the region's foothold in the thin-film battery market.

- Therefore, as per the points mentioned above, the Asia-Pacific Region is expected to witness significant growth during the forecast period.

Thin Film Battery Industry Overview

The thin film battery market is semi-consolidated. Some major players in the market (in no particular order) include Enfucell OY Ltd., EIT InnoEnergy SE, Cymbet Corporation, Inc., Kurt J. Lesker Company, and Panasonic Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand For Thin Film Technology in Consumer Electronics Sector

- 4.5.1.2 Growing Internet of Things Applications

- 4.5.2 Restraints

- 4.5.2.1 Availability of Alternate Battery Technologies

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGEMENTATION

- 5.1 Battery Type

- 5.1.1 Rechargeable

- 5.1.2 Non-Rechargeable

- 5.2 Technology

- 5.2.1 Printed Battery

- 5.2.2 Ceramic Battery

- 5.2.3 Lithium Polymer Battery

- 5.2.4 Other Technologies

- 5.3 Application

- 5.3.1 Consumer Electronics

- 5.3.2 Medical Devices

- 5.3.3 Wearable Technology

- 5.3.4 Smart Card

- 5.3.5 RFID

- 5.3.6 Other Applications

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 United Kingdom

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Nordic

- 5.4.2.7 Turkey

- 5.4.2.8 Russia

- 5.4.2.9 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Malaysia

- 5.4.3.6 Thailand

- 5.4.3.7 Indonesia

- 5.4.3.8 Vietnam

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 Nigeria

- 5.4.4.4 Qatar

- 5.4.4.5 Egypt

- 5.4.4.6 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Colombia

- 5.4.5.3 Argentina

- 5.4.5.4 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Companies Profiles

- 6.3.1 EIT InnoEnergy SE

- 6.3.2 Enfucell OY Ltd.

- 6.3.3 Kurt J. Lesker Company

- 6.3.4 Cymbet Corporation, Inc.

- 6.3.5 Imprint Energy, Inc.

- 6.3.6 Ilika Plc

- 6.3.7 STMicroelectronics

- 6.3.8 BASQUEVOLT

- 6.3.9 The Batteries Sp. z o. o

- 6.3.10 Panasonic Corporation

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Adoption in Military and Defense Application

02-2729-4219

+886-2-2729-4219

薄膜電池市場規模、佔有率、趨勢和預測:按技術、電池類型、電壓類型、應用和地區分類,2026-2034年

薄膜電池市場規模、佔有率、趨勢和預測:按技術、電池類型、電壓類型、應用和地區分類,2026-2034年 薄膜電池市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年)

薄膜電池市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年) 軟性、印刷和薄膜電池市場分析及預測(至2035年):按類型、產品類型、技術、應用、材料類型、裝置、製程、最終用戶、功能和安裝類型分類全球薄膜電池市場規模、佔有率、趨勢和成長分析報告(2026-2034)

軟性、印刷和薄膜電池市場分析及預測(至2035年):按類型、產品類型、技術、應用、材料類型、裝置、製程、最終用戶、功能和安裝類型分類全球薄膜電池市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球印刷薄膜電池市場報告

2026年全球印刷薄膜電池市場報告 薄膜電池市場-全球產業規模、佔有率、趨勢、機會和預測,按電池類型、電壓、應用、地區和競爭格局分類,2021-2031年預測軟性印刷薄膜電池市場-全球產業規模、佔有率、趨勢、機會及預測(按電池類型、應用、地區和競爭格局分類,2021-2031年預測)

薄膜電池市場-全球產業規模、佔有率、趨勢、機會和預測,按電池類型、電壓、應用、地區和競爭格局分類,2021-2031年預測軟性印刷薄膜電池市場-全球產業規模、佔有率、趨勢、機會及預測(按電池類型、應用、地區和競爭格局分類,2021-2031年預測) 可充電薄膜電池市場規模、佔有率及成長分析(按技術、電解液類型、應用和地區分類)-2026-2033年產業預測

可充電薄膜電池市場規模、佔有率及成長分析(按技術、電解液類型、應用和地區分類)-2026-2033年產業預測 全球軟性、印刷和薄膜電池市場:市場規模、市場佔有率、趨勢分析(按類型、應用和地區)、展望和未來預測(2024-2031 年)

全球軟性、印刷和薄膜電池市場:市場規模、市場佔有率、趨勢分析(按類型、應用和地區)、展望和未來預測(2024-2031 年) 可充電薄膜電池市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

可充電薄膜電池市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

▼