|

市場調查報告書

商品編碼

1693971

北美立式袋包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030)North America Stand-Up Pouch Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

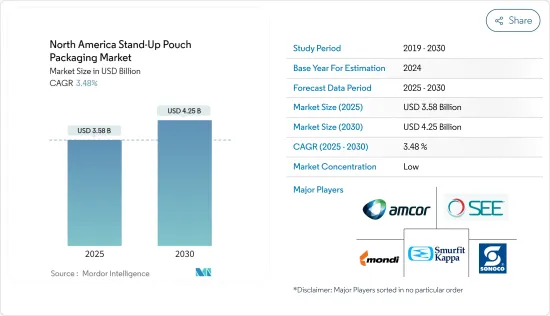

北美立式袋包裝市場規模預計在 2025 年為 35.8 億美元,預計到 2030 年將達到 42.5 億美元,預測期內(2025-2030 年)的複合年成長率為 3.48%。

預計市場規模將從 2025 年的 269.9 億台成長到 2030 年的 314.9 億台,預測期間(2025-2030 年)的複合年成長率為 3.13%。

市場研究涵蓋了標準、無菌和蒸餾等立式袋包裝產品。立式袋包裝在運輸過程中提供了理想的保護屏障,防止濕氣和污垢等外部因素與物品接觸。

關鍵亮點

- 預計全部區域冷凍包裝行業的成長將對市場產生積極影響。包裝食品和食品飲料的需求不斷增加、即食食品(RTE)的需求不斷增加、使用方便性以及包裝袋的成本效益是推動市場成長的關鍵因素。

- 此外,人們對隨時隨地吃零食的需求不斷成長,導致對可重複密封的立式袋的需求增加,這為消費者提供了便利。此外,消費者生活方式、飲食偏好的改變以及食品技術的變化正在進一步推動市場需求。

- 消費者對環境問題的意識不斷提高、監管規範不斷變化、持續推動永續性(包括用生物分解性材料取代塑膠包裝產品)以及缺乏最先進的回收設施而導致的回收率不足,這些都對市場成長構成了挑戰。

- 包裝器材正在進行技術創新,以跟上快速變化的市場需求,但這對使用傳統機械的包裝製造商提出了挑戰,因為他們無法滿足當前市場需求日益增加的工作量。參與企業必須投資新工具、備件和軟體或轉換新機器以滿足不斷變化的市場需求。

- 後新冠疫情導致包裝需求激增,這得益於食品飲料和製藥業需求的增加。

北美立式袋包裝市場趨勢

標準袋型市場預計將佔據主要市場佔有率

- 標準包裝袋,包括嬰兒食品和液體包裝(茶、咖啡、果汁),廣泛應用於食品和飲料行業。消費者期望包裝的生鮮食品能夠保留其所有天然特性和風味,這推動了標準包裝袋的採用。

- 標準立式袋正經歷來自終端用戶產業的需求激增,促使製造商努力尋求創新解決方案。該領域的特點是動態策略,公司採用合作、擴張、收購和產品發布來保持競爭力。

- 根據美國對外農業服務局的數據,2022/2023財政年度美國咖啡消費量超過2,630萬袋(每袋60公斤)。這比美國2020/2021 會計年度的咖啡總消費量(2,594 萬袋,每袋 60 公斤)略有增加。

- 隨著咖啡消費量的增加,對容納和分發咖啡的包裝解決方案的需求也將增加。標準立式袋是一種流行且用途廣泛的包裝選擇,具有便利性、保護性和可視性和可視性。隨著咖啡消費量的增加,對這些小袋子的需求也可能增加。

- 咖啡市場競爭激烈,品牌經常利用包裝脫穎而出。立式袋為品牌、標籤和行銷訊息提供了充足的空間。隨著咖啡消費量的增加,公司可能會投資包裝,以幫助他們的產品在貨架上脫穎而出,從而增加對立式袋的需求。

加拿大:預期成長顯著

- 加拿大立式袋需求不斷成長的關鍵促進因素是該國對包裝和加工食品的高度依賴。根據多倫多大學的報告顯示,加拿大約75%的食品供應來自加工食品。消費模式的改變凸顯了對便利、永續包裝解決方案的需求,使得立式袋成為加拿大市場的首選。

- 食品業正在快速擴張和變化,不斷擴大包裝選擇並尋求更有效率的運輸方式。此外,隨著更多環保和永續的包裝解決方案的出現,例如 Logos Pack、Omniplast、Canada Brown、Rootree 和 Grauman Packaging,越來越多的公司正在重新考慮他們的包裝決策。

- 加拿大的寵物食品產業正在蓬勃發展,根據加拿大農業和農業食品部 (AAFC) 的數據,加拿大寵物食品零售額預計將以 4.9% 的複合年成長率進一步成長,到 2025 年達到 53 億加元(2.2 億美元)。在寵物食品行業,立式袋通常用於包裝乾糧和濕糧。這些袋子具有撕裂槽口和易打開功能,為飼主餵養寵物提供了便利。

- 該地區消費者對包裝選擇的需求不斷成長,導致食品、食品和飲料以及製藥業的包裝採用率不斷提高。此外,日益成長的醫療問題和環境法規正在推動輕質、阻隔性包裝產品的使用。可重複密封包裝的優勢正在推動個人護理和化妝品應用的成長。

- 外國人口的不斷成長以及嘗試新產品的渴望也推動了對調理食品的需求。該地區社會和經濟模式的變化導致對快餐和簡便食品(包括預製家常小菜)的需求增加。隨著健康意識的增強,消費者也將注意力轉向植物性家常小菜。據加拿大農業食品部稱,加拿大植物性預製家常小菜(不含肉類)的零售額將在 2021 年達到 1,910 萬美元,2022 年達到 2,210 萬美元。

- 加拿大各類終端用戶需求的增加也促使企業擴張併購,以增加公司在加拿大市場的佔有率。

北美立式袋包裝產業概況

北美立式袋包裝市場主要由 Amcor PLC、Mondi Group、Sealed Air Corporation、Sonoco Products Company 和 Smurfit Kappa Group 等主要參與者組成。市場參與企業正在採取聯盟和收購等策略來增強其產品供應並獲得永續的競爭優勢。

- 2023 年 7 月 - Furutamaiki OYJ 宣布對其位於美國德克薩斯州巴黎的工廠進行重大投資。投資將包括擴大製造能力和整合外部倉庫。生產資產投資約為 3000 萬美元,將租賃倉庫和製造設施。這為我們提高北美業務的產能和支援食品服務業務的成長提供了重要的機會。

- 2023 年 1 月 - Glenroy 宣布,經過兩年的開發過程,其可回收 STANDCAP 已獲得塑膠回收再利用協會 (APR) 頒發的關鍵指導認證。作為硬質塑膠和玻璃瓶的完美環保替代品,100% 聚乙烯、可回收的 STANDCAP 對環境、消費者、品牌、零售商和食品安全來說是一個巨大的勝利。透過強調其永續的軟包裝選擇,Glenroy 正在為其生態目標做出貢獻,同時利用市場對永續解決方案日益成長的偏好來推動長期業務成長。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業生態系統分析

- 行業標準和法規

- 立式袋市場的最新創新

- 比較分析:平袋包裝與立式袋包裝

第5章市場動態

- 市場促進因素

- 北美食品和飲料需求預計將擴大,推動市場成長

- 標準包裝袋使用方便(有拉鍊、滑動和吸嘴包裝可供選擇),並且比其他包裝袋所需材料更少

- 市場問題

- 改造灌裝機以生產立式袋使轉型變得困難

第6章市場區隔

- 按包裝類型

- 標準

- 無菌

- 蒸餾

- 其他包裝類型

- 依材料類型

- 塑膠(PE、PP、PVC、EVOH、生質塑膠)

- 金屬/箔

- 紙

- 按最終用戶

- 食物

- 飲料

- 醫療藥品

- 寵物食品

- 家庭和個人護理

- 其他

- 按國家

- 美國

- 加拿大

第7章競爭格局

- 公司簡介

- Amcor PLC

- Mondi Group

- Sealed Air Corporation

- Sonoco Products Company

- Smurfit Kappa Group

- ProAmpac LLC

- Clondalkin Group

- Huhtamaki Oyj

- Dazpak Flexible Packaging

- Glenroy Inc.

- PPC Flexible Packaging LLC

第8章:市場的未來

The North America Stand-Up Pouch Packaging Market size is estimated at USD 3.58 billion in 2025, and is expected to reach USD 4.25 billion by 2030, at a CAGR of 3.48% during the forecast period (2025-2030). In terms of market size, the market is expected to grow from 26.99 billion units in 2025 to 31.49 billion units by 2030, at a CAGR of 3.13% during the forecast period (2025-2030).

Stand-up pouch packaging products such as Standard, Aseptic, and Retort are considered under the scope of the market study. Stand-up pouch packaging offers an ideal protective barrier during shipment and transit and prevents any external element, such as moisture and dirt, from coming into contact with the item.

Key Highlights

- The growth of the frozen packaged industry across the region is expected to impact the market positively. Rising demand for packaged food and beverages, increasing demand for Ready-to-Eat (RTE) food, convenience of use, and cost-effectiveness of pouches are primary factors supporting the market growth.

- In addition, the rise in the need for on-the-go snacks has led to the demand for re-closable stand-up pouches as they offer convenience to customers. In addition, the changing lifestyle and food preferences among consumers and changing food technology further boost the market's demand.

- The growing consumer attention to environmental concerns, dynamic regulatory standards, the ongoing drive for sustainability, which comprises replacing plastic-based packaging products with biodegradable materials, and inadequate recycling rates due to the lack of cutting-edge recycling facilities are challenging the market's growth.

- The ongoing technological changes in packaging machinery to cope with the rapidly changing market requirements will pose a challenge as packaging manufacturers using traditional machinery are not well equipped to take the increasing workload of current market requirements. Players must either invest in new tools, spare parts, and software to meet the changing market needs or switch to new machinery.

- The post-COVID-19 pandemic resulted in a surge in demand for packaging aided by the growing demand from the food and beverage and pharmaceutical industries, which will likely continue for the next few years.

North America Stand-Up Pouch Packaging Market Trends

Standard Pack Type Segment is Expected to Hold Significant Market Share

- Standard pouches, including baby food and liquid packaging (tea, coffee, and juices), are widely used in the food and beverage industry. Consumers' expectations for packaged fresh food to store all the natural properties and aromas drive the usage of standard pouches.

- The Standard Stand-up pouches are experiencing a surge in end-user industry demand, prompting manufacturers to strive for innovative solutions. The landscape is characterized by dynamic strategies, with companies adopting approaches such as collaboration, expansion, acquisition, and product launches to stay competitive.

- According to the USDA Foreign Agricultural Service, Coffee consumption in the United States amounted to over 26.3 million 60-kilogram bags in the 2022/2023 fiscal year. This is a slight increase from the total United States coffee consumption in the 2020/2021 fiscal year, which amounted to 25.94 million 60-kilogram bags.

- With increased coffee consumption, there is likely to be a higher demand for packaging solutions to contain and distribute the coffee. Standard Stand-up Pouches are a popular, versatile packaging option offering convenience, protection, and visibility. As coffee consumption rises, the demand for these pouches may also increase.

- The coffee market is highly competitive; brands often use packaging to differentiate themselves. Stand-up pouches provide ample space for branding, labeling, and marketing messages. As coffee consumption increases, companies will invest more in packaging that helps their products stand out on the shelves, which could boost the demand for stand-up pouches.

Canada Expected to Witness Significant Growth

- A key driving factor for the increased demand for stand-up pouches in Canada is the prevalent reliance on packaged and processed foods. University of Toronto's report indicated that approximately 75% of the nation's food supply comes from processed foods. The shift in consumption patterns underscores the need for convenient and sustainable packaging solutions, making stand-up pouches a preferred choice in the Canadian market.

- The food industry is expanding and changing swiftly, extending its packaging alternatives and looking for methods to be more productive. Additionally, more businesses, such as Logos Pack, Omniplast, Canada Brown, Rootree, and Grauman Packaging, are reconsidering their packaging decisions as more eco-friendly and sustainable packaging solutions become available.

- The pet food industry in Canada is booming, and as per Agriculture and Agri-Food Canada (AAFC) data, retail sales of pet food in Canada are expected to increase in CAGR by a further 4.9%, attaining CAD 5.3 billion (USD 0.22 billion) by 2025. In the pet food industry, stand-up pouches are a popular choice for packaging dry and wet pet food. Pouches with tear notches and easy-open features cater to the convenience of pet owners when serving their pets meals.

- The region is witnessing increased consumer demand for packaging options and rising adoption in the food, beverage, and pharmaceutical industries. Also, growing healthcare concerns and environmental regulations have increased the use of lightweight, high-barrier packaging products. The resealable benefit bolsters the growth of personal care and cosmetic applications.

- The existence of an expanding ex-pat population and the urge to try new products also drive the demand for ready meals. The region's need for quick and easy food, including prepared meals, is increasing due to shifting social and economic patterns. With rising health concerns, consumers are also focused on plant-based ready meals. According to Agriculture and Agri-Food Canada, the retail sales of plant-based ready meals (free from meat) in Canada were 19.1 million USD in 2021, reaching 22.1 million USD in 2022.

- The market also witnessed corporate expansions, mergers, and acquisitions to expand corporate presence in the Canadian market due to increased demand across various end-users in the country.

North America Stand-Up Pouch Packaging Industry Overview

The North America stand-up pouch packaging market is fragmented, with the precence of major players like Amcor PLC, Mondi Group, Sealed Air Corporation, Sonoco Products Company, and Smurfit Kappa Group. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- July 2023 - Huhtamaki OYJ announced a significant investment in its Paris, Texas, facility in the United States. The investment consists of an expansion of its manufacturing capacity as well as a consolidation of an external warehouse. The investment into production assets is approximately USD 30 million, and the warehouse and manufacturing facility will be leased. This brings significant opportunities to increase the North America business segment's capacity to support the growth of the food service business.

- January 2023- Glenroy Inc. announced that after a two-year development process, they received Critical Guidance Recognition from the Association of Plastic Recyclers (APR) for the recyclable STANDCAP. As a complete eco-friendly alternative to rigid plastic and glass bottles, the 100% Polyethylene recyclable STANDCAP is a major win for the environment, consumers, brands, retailers, and food safety. By emphasizing the company's sustainable, flexible packaging options, Glenroy contributes to ecological goals while also capitalizing on the growing market preference for sustainable solutions, driving business growth in the long term.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Ecosystem Analysis

- 4.4 Industry Standards and Regulations

- 4.5 Recent Innovations in the Stand-Up Pouch Market

- 4.6 Comparative Analysis: Flat Packaging vs Stand-Up Pouch Packaging

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Food and Beverage Expected to Grow in North America, thereby Contributing to the Market Growth

- 5.1.2 Standard Pouches Offer a High Level of Convenience (Available in Zipper, Slider, Spout Packs, Etc.) and Require Less Material Volumes as Compared to Alternative

- 5.2 Market Challenges

- 5.2.1 Filling Machinery Changes for Producing Stand-Up Pouches Make Transitions Difficult to Implement

6 MARKET SEGMENTATION

- 6.1 By Pack Type

- 6.1.1 Standard

- 6.1.2 Aseptic

- 6.1.3 Retort

- 6.1.4 Other Pack Types

- 6.2 By Material Type

- 6.2.1 Plastic (PE, PP, PVC, EVOH, Bio-Plastics)

- 6.2.2 Metal/Foil

- 6.2.3 Paper

- 6.3 By End User

- 6.3.1 Food

- 6.3.2 Beverages

- 6.3.3 Medical and Pharmaceutical

- 6.3.4 Pet Food

- 6.3.5 Home and Personal Care

- 6.3.6 Other End Users

- 6.4 By Country

- 6.4.1 United States

- 6.4.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Mondi Group

- 7.1.3 Sealed Air Corporation

- 7.1.4 Sonoco Products Company

- 7.1.5 Smurfit Kappa Group

- 7.1.6 ProAmpac LLC

- 7.1.7 Clondalkin Group

- 7.1.8 Huhtamaki Oyj

- 7.1.9 Dazpak Flexible Packaging

- 7.1.10 Glenroy Inc.

- 7.1.11 PPC Flexible Packaging LLC