|

市場調查報告書

商品編碼

1693970

永續發展顧問服務 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Sustainability Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

永續發展諮詢服務市場規模預計在 2025 年為 169.9 億美元,預計到 2030 年將達到 547.6 億美元,預測期內(2025-2030 年)的複合年成長率為 26.38%。

永續發展諮詢服務市場的擴張受到多種因素的推動。這些包括對環境、社會和管治(ESG) 問題的認知不斷提高、對減少碳足跡的關注度不斷提高、相關人員的壓力不斷增加、監管合規要求越來越嚴格以及公司需要採取永續的做法來滿足客戶期望並提高其聲譽。

關鍵亮點

- 此外,這種成長代表著商業環境的重大變化,永續性已成為企業策略和決策的核心。隨著企業努力適應不斷變化的氣候條件、致力於減少溫室氣體排放並實現全球永續發展基準,全球永續發展諮詢服務市場將持續擴大。因此,諮詢公司在幫助政府、企業和非營利組織制定策略、採取永續做法和應對日益複雜的氣候變遷方面發揮關鍵作用。

- 人們對減少碳排放的興趣日益濃厚,以及企業實現淨零目標的需求日益成長,推動了對永續發展諮詢服務的需求。世界各地的公司越來越致力於實現溫室氣體「淨零」排放,以配合應對氣候變遷的努力。這積極推動了企業對永續發展諮詢服務的需求,以有效實現淨零目標。

- 世界各國紛紛制定應對氣候變遷的國家目標,大大增加了對永續發展諮詢服務的需求。世界各國政府都在採取措施實現淨零排放,這刺激了對永續發展諮詢服務的需求,這些服務在製定策略和指導政府實現淨零目標方面發揮著至關重要的作用。

- 現實差距大和採用率低是阻礙全球永續發展諮詢服務市場成長的主要因素。由於各國對永續發展措施的採用仍處於停滯狀態,環境顧問公司在推動永續發展方面面臨挑戰。由於財政、技術和人力資源有限,組織往往難以解決氣候變遷調適等複雜且有爭議的問題。結果,私營和公共部門組織對永續性諮詢服務的使用有所下降。

- 持續不斷的俄烏戰爭對全球永續發展諮詢服務市場產生了重大影響。俄烏戰爭對全球經濟成長和勞動市場造成重大影響,加劇了通膨壓力,並導致供應鏈嚴重中斷。戰爭正在破壞供應鏈,特別是永續發展計劃所必需的材料和商品的供應鏈。尤其是電動車電池必不可少的鎳和鈀,在供應鏈中面臨重大挑戰。

永續發展諮詢服務市場的趨勢

氣候變遷諮詢服務佔主要市場佔有率

- 氣候變遷諮詢服務包括碳足跡和緩解分析、替代能源開發和能源效率、氣候適應和策略、緊急管理、碳補償/淨零服務、環境合規服務、廢棄物管理和循環經濟以及其他服務。

- 氣候變遷諮詢服務的需求不斷成長,因為企業和組織尋求專家建議,以減少對環境的影響、減少碳足跡、適應氣候變遷、管理風險、確保遵守法規和永續實踐。

- 世界各地的企業都在努力應對氣候變遷的影響。因此,對於希望在新的淨零模式下保持競爭力和蓬勃發展的企業來說,管理與氣候變遷相關的風險(包括物理風險、過渡風險和責任風險)變得至關重要。這種不斷變化的情況導致對一系列以氣候變遷為重點的諮詢服務的需求增加,以幫助應對複雜的情況。

- 根據全球大氣研究/聯合研究中心排放資料庫(EDGAR/JRC)發布的2024年世界各國溫室氣體(GHG)排放報告顯示,2023年全球溫室氣體(GHG)排放再創新高,達到529.6億噸二氧化碳當量(Gt CO2e),比與前一年同期比較成長2%。

- 此外,在氣候變遷議題上發揮領導作用的公司將提高其聲譽,並將自己定位為永續發展的領導者。這種積極主動的方法可以吸引客戶、人才和寶貴的夥伴關係,為您帶來顯著的競爭優勢。

- 永續發展諮詢市場的供應商正在收購氣候變遷顧問公司。該策略旨在擴大其提供的服務範圍,提高其市場佔有率並滿足日益成長的氣候變遷諮詢服務需求。

- 例如,2024 年 6 月,永續發展顧問公司 ERM 宣布已同意收購澳洲氣候風險與能源轉型顧問公司 Energetics。此舉旨在加強亞太地區企業風險管理的發展。 Energetics 專門提供客製化服務,例如製定氣候適應性策略、提供氣候風險和可再生能源轉型洞察、指導企業實現淨零目標以及監控可再生能源交易的購電協議 (PPA)。 ERM表示,此次收購將增強其為澳洲和亞太地區的客戶提供策略建議和實際實施的能力。

- 總體而言,氣候變遷諮詢服務預計將佔據全球永續發展諮詢市場的最大佔有率。隨著企業和組織越來越意識到氣候變遷的影響,面臨減少碳排放的監管壓力,以及全球氣候行動的激增,對氣候變遷諮詢服務的需求也在增加。企業尋求透過積極主動的氣候變遷風險管理來提高競爭力,這進一步推動了這項需求。

亞太地區經濟強勁成長

- 多樣化的法律規範和快速的工業化正在塑造亞太地區的永續發展諮詢市場。政府對環境標準法規的加強,特別是在製造業、石油天然氣和建設業等能源密集型行業,對該地區的擴張做出了重大貢獻。為此,亞太地區的永續發展顧問公司正在幫助企業實現合規目標、採用綠色策略並將永續實踐納入業務中。

- 中國和印度等國家正在經歷快速的都市化和工業化,並面臨環境惡化的問題。這促使政府制定了更嚴格的環境標準。在此背景下,永續發展顧問公司發揮著至關重要的作用,指導企業創建協調成長與環境管理的經營模式,同時確保遵守國家和國際永續發展基準。

- 例如,在都市化加快和國家「雙碳」目標(即2030年碳排放達到高峰、2060年實現完全碳中和)的推動下,中國正在加大建築業綠色化。根據政府數據,2020年中國77%的城鎮新建計劃被歸類為綠建築。

- 2023年10月,上海宣布了一項三年計劃,旨在加強在該市營運的外資企業的ESG能力。該計畫鼓勵企業增加研發投入,採用數位化、綠色和低碳技術,以增強創新和競爭力,並增加對永續發展諮詢解決方案的需求。

- 亞太地區越來越多的公司正在採用 ESG 原則來吸引全球投資者並提高其品牌聲譽。永續發展顧問公司正在透過確定需要加強的領域、實施 ESG 策略和準備國際永續發展報告標準來幫助這些公司。

永續發展諮詢服務市場概覽

永續發展諮詢服務市場的特點是既有參與企業企業,也有新興參與企業,形式多元。主要參與企業包括埃森哲(Accenture PLC)、波士頓顧問集團、塔塔諮詢服務有限公司、Capgemini SA顧問公司和羅蘭貝格公司。

該市場中適度的退出障礙獎勵了新參與企業,同時允許現有企業在收益較低時期退出。業界領先的公司擴大採用整合解決方案來吸引客戶。相較之下,規模較小的新進入者預計將採取具有成本效益的策略與規模較大的參與者競爭,加劇競爭。

此外,近期合資企業和收購的顯著增加證明了全球商業界對永續性的重視。因此,全球永續發展市場中競爭公司之間的敵意依然突出。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 評估市場的宏觀經濟因素

第5章市場動態

- 市場促進因素

- 更重視減少碳足跡和實現淨零目標

- 世界各國應對氣候變遷的國家目標

- 市場問題

- 採用率低,與現實狀況差距較大

第6章市場區隔

- 按服務類型

- 氣候變遷諮詢服務

- 綠建築諮詢服務

- ESG諮詢服務

- 其他永續發展諮詢服務

- 按最終用戶

- 建築和房地產

- 能源動力

- 公共部門

- 其他

- 按地區

- 北美洲

- 歐洲

- 英國

- 德國

- 比荷盧經濟聯盟

- 西班牙

- 法國

- 北歐的

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- Accenture PLC

- The Boston Consulting Group, Inc.

- Tata Consultancy Services Limited

- Capgemini SE

- Roland Berger GmbH

- Bain & Company, Inc.

- KPMG International Limited

- Ernst & Young Global Limited

- Deloitte Touche Tohmatsu Limited

- PricewaterhouseCoopers LLP

- McKinsey & Company

- Kearney

- Godrej & Boyce Mfg. Co. Ltd(Godrej Industries Limited)

- RPS Group(Tetra Tech Inc.)

- SEA Energy

第8章投資分析

第9章:未來市場展望

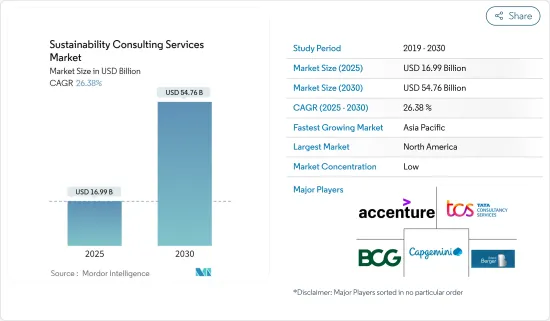

The Sustainability Consulting Services Market size is estimated at USD 16.99 billion in 2025, and is expected to reach USD 54.76 billion by 2030, at a CAGR of 26.38% during the forecast period (2025-2030).

The expansion of the sustainability consulting services market is driven by several factors. These include increased awareness of environmental, social, and governance (ESG) issues, a stronger focus on reducing carbon footprints, heightened stakeholder pressures, more stringent regulatory compliance requirements, and the necessity for businesses to adopt sustainable practices to meet customer expectations and enhance their reputation.

Key Highlights

- Moreover, this growth signifies a pivotal transformation in the business landscape, with sustainability taking center stage in corporate strategies and decision-making. As companies increasingly adapt to evolving climate conditions, aim to reduce greenhouse gas emissions, and strive to meet global sustainability benchmarks, the global sustainability consulting services market is poised for continued expansion. Consequently, consulting firms play a vital role in assisting governments, businesses, and nonprofit entities in creating strategies, adopting sustainable practices, and navigating the increasing complexities of the changing climate.

- The rising focus on carbon footprint reduction and the growing need to fulfill businesses' net zero targets drive the demand for sustainability consulting services. Companies worldwide increasingly commit to achieving "net zero" greenhouse gas emissions, aligning with initiatives to combat climate change. This positively drives businesses' demand for sustainability consulting services to achieve their net-zero targets efficiently.

- Countries worldwide are setting national goals to combat climate change, significantly boosting the demand for sustainability consulting services. Governments are implementing measures to achieve net-zero emissions, fueling the demand for sustainability consulting services, which are pivotal in guiding governments and formulating strategies toward their net-zero targets.

- Lower levels of adoption, with large gaps in reality, are a major factor hindering the growth of the global sustainability consulting services market. Environmental consulting firms face challenges in promoting sustainability due to the sluggish adoption of sustainability initiatives across various nations. Organizations frequently struggle with limited financial, technical, and human resources, making addressing intricate and contentious issues such as climate change adaptation difficult. Consequently, this dynamic results in diminished uptake of sustainability consulting services, both in the private sector and among public sector enterprises.

- The ongoing Russia-Ukraine War significantly impacts the global sustainability consulting services market. It has profoundly affected global economic growth and labor markets, intensifying inflationary pressures and causing significant supply chain disruptions. The war has disrupted supply chains, especially for materials and goods vital to sustainability projects. Notably, nickel and palladium, essential for electric vehicle batteries, have faced significant supply chain challenges.

Sustainability Consulting Services Market Trends

Climate Change Consultancy Services Type Holds Major Market Share

- Climate change consultancy services considered under the scope include Carbon Footprint and Mitigation Analysis, Alternative Energy Development and Energy Efficiency, Climate Adaptation and Strategy, Emergency Management, Carbon Offset/Net Zero Services, Environmental Regulatory Compliance Services, Waste Management and Circularity, and Other Services.

- The increasing demand for climate change consultancy services is driven by businesses and organizations seeking expert advice on reducing environmental impact, lowering carbon footprints, adapting to climate change, managing risks, ensuring regulatory compliance, and implementing sustainable practices.

- Across the globe, businesses are grappling with the repercussions of climate change. As a result, managing climate-related risks, such as physical, transitional, or liability-based, has become paramount for firms eager to maintain their competitive edge and thrive in the emerging Net Zero paradigm. This evolving landscape has spurred a heightened demand for various consultancy services centered on climate change, aiding businesses in navigating these complexities.

- According to the 2024 report on GHG emissions from all world countries, published by 'The Emissions Database for Global Atmospheric Research/Joint Research Centre (EDGAR/JRC)'' global greenhouse gas (GHG) emissions hit a record high in 2023, reaching 52.96 billion metric tons of carbon dioxide equivalent (Gt CO2e), marking a two percent year-over-year increase.

- Moreover, companies that take the initiative in confronting climate change issues bolster their reputation and position themselves as leaders in sustainability. Such a proactive stance can translate into a significant competitive advantage, drawing in customers, top talent, and valuable partnerships.

- Vendors in the sustainability consulting market are acquiring climate change consulting firms. This strategy aims to broaden their service offerings, bolster their market presence, and cater to the rising demand for climate change consultancy services.

- For instance, in June 2024, ERM, a sustainability advisory firm, announced its agreement to acquire Energetics, a climate risk and energy transition consultancy based in Australia. This move aims to bolster ERM's growth in the Asia Pacific region. Energetics specializes in tailored services, such as crafting climate resiliency strategies, offering insights on climate risks and renewable energy transitions, guiding companies towards net-zero goals, and monitoring power purchase agreements (PPAs) for renewable energy transactions. ERM asserts that this acquisition will bolster its capacity to provide clients with both strategic advice and hands-on implementation across Australia and the broader Asia Pacific region.

- Overall, climate change consultancy services are expected to hold the largest share of the global sustainability consulting market. As businesses and organizations become more aware of climate impacts, face regulatory pressures to reduce their carbon footprints, and witness a global surge in climate action initiatives, there's a rising demand for climate change consultancy services. This demand is further fueled by businesses seeking a competitive edge through proactive climate change risk management.

Asia Pacific to Register Major Growth

- Diverse regulatory frameworks and swift industrialization shape the sustainability consulting market in the Asia-Pacific region. The region's expansion is largely fueled by heightened government regulations on environmental standards, especially in energy-intensive sectors such as manufacturing, oil and gas, and construction. In response, sustainability consulting firms in the Asia-Pacific help businesses meet compliance targets, adopt green strategies, and weave sustainable practices into their operations.

- Countries like China and India, witnessing rapid urbanization and industrialization, face environmental degradation. This has led their governments to enforce stricter environmental standards. In this context, sustainability consulting firms play a pivotal role, guiding companies to craft business models that harmonize growth with environmental stewardship, all while ensuring adherence to both national and international sustainability benchmarks.

- For instance, driven by rising urbanization and its national "Dual Carbon" targets-aiming for peak carbon emissions by 2030 and full carbon neutrality by 2060-China is intensifying its efforts to green its building and construction sector. Government data reveals that in 2020, a significant 77% of China's new urban construction projects were classified as green buildings.

- In October 2023, Shanghai unveiled a three-year initiative aimed at bolstering the ESG capabilities of foreign businesses in the city. Thereby, the plan encourages companies to ramp up Research and Development investments and embrace digital, green, and low-carbon technologies, enhancing their innovation and competitiveness, and heightening the demand for sustainability consulting solutions.

- In the Asia-Pacific region, companies are increasingly adopting ESG principles to draw in global investors and bolster their brand reputation. Sustainability consulting firms assist these businesses by pinpointing areas for enhancement, executing ESG strategies, and gearing up for international sustainability reporting standards.

Sustainability Consulting Services Market Overview

The sustainability consulting services market is characterized by a diverse mix of both established and emerging players. Some of the major players in the market are Accenture PLC, The Boston Consulting Group, Inc., Tata Consultancy Services Limited, Capgemini SE, and Roland Berger GmbH, among others.

Moderate exit barriers in the market incentivize new entrants while allowing established firms to exit during low-profit periods. Leading industry players are increasingly focusing on integrated solutions to attract customers. In contrast, smaller and newer market entrants are expected to adopt cost-benefit strategies to vie with their larger counterparts, intensifying competition.

Furthermore, a notable surge in joint ventures and acquisitions recently underscores the global business community's heightened emphasis on sustainability. As a result, competitive rivalry in the global sustainability market remains pronounced.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Focus on the Reduction of Carbon Footprint and Fulfilment of Net Zero Targets

- 5.1.2 National Goals Across the Globe to Combat Climate Change

- 5.2 Market Challenges

- 5.2.1 Lower Levels of Adoption with Large Gaps in the Realistic Scenario

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Climate Change Consultancy Services

- 6.1.2 Green Building Consultancy Services

- 6.1.3 ESG Consultancy Services

- 6.1.4 Other Sustainability Consultancy Services

- 6.2 By End User

- 6.2.1 Construction and Real Estate

- 6.2.2 Energy and Power

- 6.2.3 Public Sector

- 6.2.4 Other End Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 Benelux

- 6.3.2.4 Spain

- 6.3.2.5 France

- 6.3.2.6 Nordics

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Accenture PLC

- 7.1.2 The Boston Consulting Group, Inc.

- 7.1.3 Tata Consultancy Services Limited

- 7.1.4 Capgemini SE

- 7.1.5 Roland Berger GmbH

- 7.1.6 Bain & Company, Inc.

- 7.1.7 KPMG International Limited

- 7.1.8 Ernst & Young Global Limited

- 7.1.9 Deloitte Touche Tohmatsu Limited

- 7.1.10 PricewaterhouseCoopers LLP

- 7.1.11 McKinsey & Company

- 7.1.12 Kearney

- 7.1.13 Godrej & Boyce Mfg. Co. Ltd (Godrej Industries Limited)

- 7.1.14 RPS Group (Tetra Tech Inc.)

- 7.1.15 SEA Energy