|

市場調查報告書

商品編碼

1693901

Wi-Fi 路由器:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Wi-Fi Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

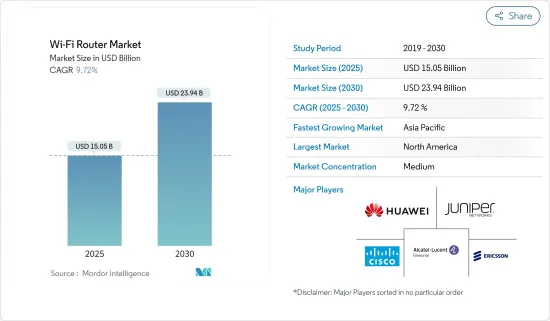

預計 2025 年 Wi-Fi 路由器市場規模為 150.5 億美元,到 2030 年將達到 239.4 億美元,預測期內(2025-2030 年)的複合年成長率為 9.72%。

還有更多。

隨著越來越多的客戶參與網頁瀏覽、行動學習和其他線上相關活動,對更快網路存取的需求也日益成長。因此,在筆記型電腦、個人電腦和平板電腦中大量使用的無線路由器已成為人類生存的必需品。無線路由器在滿足消費者對可靠網路存取日益成長的需求以及加強許多國家的網路連線方面發揮了關鍵作用。還有更多。

主要亮點

- 越來越多的客戶參與電子商務交易、網頁瀏覽、行動學習和其他線上相關活動,對更快的網路存取產生了需求。因此,在筆記型電腦、個人電腦和平板電腦中大量使用的無線路由器已成為人類生存的必需品。 Wi-Fi 路由器在加速消費者對可靠網路存取的需求以及加強許多國家的 Wi-Fi 連線方面發揮了關鍵作用。

- 醫療保健、教育、商業、金融服務和其他應用中連網裝置的使用日益增多是全球無線路由器市場的主要驅動力之一。此外,中小企業採用自備設備政策也對市場成長產生了正面影響。此外,預計預測期內政府加大對智慧城市計劃的投入將為市場擴張創造有利機會。

- 此外,通訊(ITU)預測,到2022年,全球將有53億人(佔全球人口的66%)使用網路。這比 2019 年成長了 24%,預計 2019 年將有 11 億人加入網路。網路普及率的提高將為國內外無線路由器廠商推出新產品、提高頻寬、搶佔更大市場佔有率創造機會。

- 此外,思科年度網際網路報告預測,到 2023 年,連網裝置和連線的數量將達到近 300 億,高於 2018 年的 184 億。到 2023 年,物聯網設備將佔所有連網裝置的 50%(147 億),高於 2018 年的 33%(61 億)。此外,據思科稱,固定網路 IP 流量將從 2016 年的 65,942 台裝置成長到 2021 年的 187,386 台裝置。網際網路流量的這種成長可能會推動所研究的市場。

- 此外,統計計數器顯示,在加拿大,2022 年 1 月行動流量佔所有網站流量的 38.04% 以上,低於 2020 年的 40.95%。桌上型電腦和筆記型電腦繼續主導加拿大的網路使用。網際網路連接設備的增加可能會促進市場的成長。

- 隨著數位化化技術的不斷普及,這一數字可能還會增加。城市地區的交通量比以前高很多。近年來,第四代長期演進(4G/LTE)行動寬頻網路大大促進了跨轄區和跨部門的通訊互通性。

Wi-Fi路由器市場趨勢

零售和電子商務預計將佔據很大市場佔有率

- 電子商務(electronic commerce)是透過網路購買和銷售商品和服務。它包括一系列針對線上買家和賣家的數據、系統和工具,包括用於行動購物和線上付款的加密。大多數擁有線上業務的企業都使用線上商店或平台來進行電子商務行銷和銷售活動,以及監督物流和履約。這種電子商務趨勢可能會刺激對 Wi-Fi 路由器的需求,以便消費者可以訪問任何網路購物網站。

- 越來越多的客戶參與電子商務交易、網頁瀏覽、行動學習和其他線上相關活動,對更快的網路存取產生了需求。因此,筆記型電腦、個人電腦和平板電腦中普遍使用的無線路由器已成為人類生存的必需品。 Wi-Fi 路由器在加速消費者對可靠網路存取的需求以及加強許多國家的 Wi-Fi 連線方面發揮了關鍵作用。

- 根據GSMA(全球行動通訊系統協會)的情報數據,截至2022年初,新加坡擁有870萬個活躍的行動連線。此外,到 2022 年 1 月,新加坡的行動連線將佔其總人口的 147%。該地區的網際網路普及率可能會推動電子商務市場的發展。此外,根據新加坡統計局的數據,到 2022 年,電腦和通訊設備的線上銷售額將佔總銷售額的 47.4%。相較之下,30%的家具和家電都是在網路上購買的。該地區線上購物的成長可能為新參與者進入市場創造重大機會,同時也為國際參與者機會在新加坡的業務創造重大機會。

- 根據通訊(MoTC) 的數據,卡達以平均 264 美元的交易額位居中東地區首位。此外,去年該國有 350 家電子商務企業投入營運,預計未來六個月內還將有 66 家電子商務企業開業,截至去年 12 月底,電子商務企業總數將達到 416 家。

- 此外,卡達的電子商務滲透率為62.1%。此外,以屬性看網路購物,最大的群體是卡達人(22%),其次是西方人(17%)、阿拉伯人(19%)、亞洲人(20%)和其他人群(22%)。卡達是中東和北非 (MENA) 地區 (與海灣合作理事會相比) 每位用戶年度平均電子商務支出最高的國家,其每筆線上交易的平均價值也超過了海灣合作理事會的平均水平。

- 根據 Kibo Commerce 的數據,在美國,2022 年第二季 2.3% 的電商網站流量促成了購買。在英國,線上購物者的轉換率上升至 4% 以上。儘管行動商務在頁面瀏覽量和收益方面正在迎頭趕上,但傳統的透過個人電腦進行的網路購物仍然佔據主導地位。線上用戶轉換率的提高對學生市場產生了積極影響。

預計北美將佔據很大市場佔有率

- 美國是技術發展、商業數位化和網際網路使用的領先國家之一。為了滿足國家數位轉型進程的要求,高速網路的需求已變得至關重要。根據Cisco預測,北美地區的平均Wi-Fi網路連線速度將從2020年的70.7 Mbps提升至2023年的109.5 Mbps。如此巨大的網速可能會鼓勵玩家開發能夠支援這種網速的新型Wi-Fi路由器。

- 美國政府與美國私營部門合作,致力於支持泰國4.0。 2022 年,美國和泰國政府及企業主管啟動了研討會,共用有關 6 GHz 頻譜分配和下一代 Wi-Fi 技術意義的知識。除了提高家庭 Wi-Fi 速度外,研討會還有望進一步鞏固泰國作為先進製造業和工業創新中心的地位。兩國之間的此次夥伴關係預計將推動美國Wi-Fi製造商市場的發展。

- 為了增加市場佔有率,該地區的公司正在以經濟的價格推出最新產品。例如,美國路由器製造商 Linksys 計劃於 2022 年 5 月推出雙頻 Wi-Fi 6 路由器,如 Hydra 6 和 Atlas 6。這些路由器以實惠的價格提供速度和效能,為混合工作、線上遊戲、4K UHD 串流媒體等提供可靠的連接。

- 加拿大是一個經濟發達的國家,人們有能力購買有用的智慧設備。此外,據思科稱,到2023年,加拿大的網路用戶數量預計將達到3530萬,這表明該國的Wi-Fi路由器具有巨大的成長潛力,因為網路用戶的增加將對Wi-Fi路由器產生積極影響。

- 該國對低延遲、高速網路服務的需求日益成長,許多全球參與者正在該國發布先進的 Wi-Fi 路由器和網狀 Wi-Fi 路由器。例如,2022 年 10 月,Google在加拿大推出了支援 Wi-Fi 6E 的 Nest Wi-Fi Pro,這是其首款能夠在三頻網狀網路中運作的路由器。在相容設備上,Wi-Fi 6E(E 代表擴展)使用新的、不太擁擠的 6 GHz 無線電頻寬,提供高達 Wi-Fi 6 兩倍的速度。

Wi-Fi路由器產業概況

Wi-Fi 路由器市場相當集中,有多家參與者,包括Cisco、愛立信、華為技術、Juniper Networks和阿爾卡特朗訊企業。每家公司都繼續投資於策略夥伴關係和產品開發,以大幅增加市場佔有率。還有更多。

2023 年 3 月,NETGEAR 發布了首款支援 Wi-Fi 7 的路由器 Nighthawk RS700。 NETGEAR 表示,三頻設備專為低延遲 AR(擴增實境)/VR(虛擬實境)遊戲、UHD Zoom 通話、同步 8K 串流等而設計。 RS700 具有新的塔式外形,讓人聯想到以前的 Nighthawk 路由器,並採用內建天線設計,可實現 360 度覆蓋,涵蓋範圍積達 3,500 平方英尺。還有更多。

2022 年 11 月,全球消費和商業網路產品供應商 TP-Link 宣布推出整個面向家庭和企業的 Wi-Fi 7 產品線。 TP-Link 為 ISP 市場推出全新 Wi-Fi 7 路由器、Omada EAP、Deco 產品、Aginet 產品,涵蓋所有用例。 TP-Link 的新款 HomeShield 3.0 也提供了更可靠、更智慧的網路解決方案。作為性能最佳的 Archer 系列之一,Wi-Fi 7 路由器為您的家庭帶來前所未有的體驗。此次活動發表了三款新型Wi-Fi 7路由器。其中,Archer BE900 擁有四頻 24Gbps Wi-Fi 7 速度,以及有別於傳統路由器的全新設計。還有更多。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 生態系分析

- 產業吸引力-波特五力分析

- 買家的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響評估

- 使用案例

第5章市場動態

- 市場促進因素

- 網路流量增加以及消費者對網路設備的需求

- 數位化正在推動整個企業頻寬需求呈指數級成長

- 市場限制

- 網路安全和網路管理的複雜性

- 行動寬頻使用情況

第6章市場區隔

- 按類型

- 邊緣路由器

- 核心路由器

- 按組織規模

- 中小企業

- 大型企業

- 按最終用戶產業

- 衛生保健

- 運輸和物流

- 零售與電子商務

- 製造業

- 政府

- BFSI

- 其他

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 中東和非洲

- 拉丁美洲

第7章競爭格局

- 公司簡介

- Cisco Systems Inc

- Ericsson Inc.

- Huawei Technologies Co.ltd

- Juniper Networks Inc.

- Alcatel Lucent Enterprise SAS

- ARUBA SPA

- Fortinet Inc.

- Panasonic Corporation

- Broadcom Inc

- Extreme Networks Inc.

第8章投資分析

第9章:未來趨勢

The Wi-Fi Router Market size is estimated at USD 15.05 billion in 2025, and is expected to reach USD 23.94 billion by 2030, at a CAGR of 9.72% during the forecast period (2025-2030).

A growing number of customers are engaging in web browsing, mobile learning, and other online-related activities, driving the demand for faster Internet access. As a result, the wireless router, frequently utilized in laptops, PCs, and tablets, has become essential for human existence. Wireless routers are primarily responsible for the rising need among consumers to stay linked to dependable Internet and for enhancing internet connections in numerous nations.

Key Highlights

- A growing number of customers are engaging in e-commerce transactions, web browsing, mobile learning, and other online-related activities, driving the demand for faster Internet access. As a result, the wireless router, frequently utilized in laptops, PCs, and tablets, has become essential for human existence. Wi-Fi routers are mostly responsible for the rising need among consumers to stay linked to dependable Internet and for enhancing Wi-Fi connections in numerous nations.

- The increasing use of connected devices in healthcare, education, business, financial services, and other applications is one of the critical drivers of the worldwide wireless router market. Additionally, the market growth is positively impacted by small and medium businesses adopting a bring your device policy. Further, during the projected period, a rise in government initiatives for smart city projects is anticipated to create lucrative opportunities for market expansion.

- Further, in 2022, the International Telecommunication Union (ITU) estimates that 5,300 Million people, or 66% of the world's population, will use the Internet. This marks a 24% growth from 2019, with an expected 1.1 billion individuals joining the Internet throughout that time. The advancement in Internet penetration will create opportunities for international and local Wireless router vendors to introduce new products and improve the bandwidth to capture a significant market share.

- Moreover, By 2023, there will be close to 30 billion network-connected devices and connections, up from 18.4 billion in 2018, predicts Cisco's Annual Internet Report. By 2023, IoT devices will drive up 50% (14.7 billion) of all networked devices, up from 33% (6.1 billion) in 2018. Further, according to Cisco, the fixed internet IP traffic has increased from 65,942 units in 2016 to 1,87,386 units in 2021. Such a rise in internet traffic will drive the studied market.

- Further, according to the stats counter, in Canada, mobile traffic accounted for more than 38.04 % of all website traffic in January 2022, down from 40.95% in 2020. In Canada, desktops and laptops continue to dominate web usage. Such a rise in Internet-connected devices would allow the studied market to grow.

- As digitization adaptation increases, this amount will increase even more. Traffic in metro areas has significantly increased as compared to prior years. In recent years, inter-jurisdictional and inter-disciplinary communications interoperability was greatly aided by the fourth generation Long Term Evolution (4G/LTE) mobile broadband networks.

Wi-Fi Router Market Trends

Retail and E-commerce are Expected to Hold Significant Share of the Market

- E-commerce (or electronic commerce) is the buying and selling of goods or services on the Internet. It encompasses various data, systems, and tools for online buyers and sellers, including mobile shopping and online payment encryption. Most businesses with an online presence use an online store and/or platform to conduct ecommerce marketing and sales activities and to oversee logistics and fulfillment. Such trends in E-commerce would drive the demand for Wi-Fi routers so that consumers can have access to any online shopping site.

- A growing number of customers are engaging in e-commerce transactions, web browsing, mobile learning, and other online-related activities, driving the demand for faster internet access. As a result, the wireless router, frequently utilized in laptops, PCs, and tablets, has become essential for human existence. Wi-Fi routers are mostly responsible for the rising need among consumers to stay linked to dependable Internet and for enhancing Wi-Fi connections in numerous nations.

- At the beginning of 2022, Singapore had 8.70 million active mobile connections, according to data from Groupe Speciale Mobile Association (GSMA) Intelligence. Furthermore, mobile connections in Singapore were equivalent to 147% of the total population in January 2022. Such internet penetration in the region will drive the e-commerce market. Furthermore, According to the Singapore Department of Statistics, in 2022, online computer and telecommunications equipment sales accounted for 47.4% of total sales. In comparison, 30% of furniture and household equipment were acquired online. Such a rise in online purchases in the region will significantly create an opportunity for new players to enter the market and for international players to expand their presence in Singapore.

- According to the Ministry of Transport and Communications (MoTC), Qatar leads the Middle Eastern countries in terms of the average value of a single transaction at USD 264 per transaction. Moreover, 350 e-commerce companies were operating in the country last year, and 66 more e-commerce companies opened in the next six months, bringing the total to 416 by the end of December last year.

- Further, in Qatar, e-commerce penetration is 62.1%. Also, online shoppers by demographics, Qataris (22%), are the most likely to shop online, followed by Westerners (17%), Arabs (19%), Asians (20%), and others (22%). Qatar has the most significant average yearly e-commerce spend per user in the Middle East and Northern Africa (MENA) area (relative to the GCC), and the average value per online transaction is greater than the GCC average.

- According to Kibo Commerce, During the second quarter of 2022, 2.3% of visits to e-commerce websites in the United States converted to purchases. In Great Britain, online shopper conversion rates rose to over four percent. Although mobile commerce is catching up regarding page views and revenue, traditional online shopping via PC still holds the top. Such a rise number of online users' conversion rates positively impact the student market.

North America is Expected to Hold Significant Share of the Market

- The United States is one of the leading countries in terms of technological development, digitalization of businesses, and internet usage. The requirement of high-speed internet is becoming essential to match the requirement for the country's digital transformation journey. According to Cisco Systems, the average Wi-Fi network connection speed in North America was 109.5 Mbps in 2023, an increase from 70.7 Mbps in 2020. Such huge speed internet would push the players to develop new Wi-Fi routers to support such internet speeds.

- The United States government is engaged in assisting Thailand 4.0., as they were collaborating with America's private sectors. In 2022, the United States, the Royal Thai government, and business executives started a workshop to share knowledge on the significance of 6 GHz spectrum allocation and next-generation Wi-Fi technology, which will not only make home Wi-Fi faster but also further solidify Thailand's position as a hub of advanced manufacturing and industry innovation. These partnerships between the country will drive the market for Wi-Fi manufacturers in the USA.

- Companies in the region are launching updated products with economical prices to increase their market shares. For example, in May 2022, American router maker Linksys intends to introduce dual-band Wi-Fi 6 routers, including the Hydra 6 and Atlas 6. These routers would offer reliable connectivity for hybrid work, online gaming, 4K UHD streaming, and more because they are designed for speed and performance at a reasonable price.

- Canada is an economically developed country for which people can afford smart devices for their convenience, and the number of connected devices has been increasing in the country, fueled by internet penetration. According to Cisco,In addition, by 2023, there will be 35.3 million Internet users in Canada, which shows huge growth potential for the Wi-Fi routers in the country because the growth of Internet users will positively impact the Wi-Fi routers.

- The country's need for Internet services with low latency and increasing speed is increasing, and many global players are launching advanced Wi-Fi routers or meshed Wi-Fi routers in the country. For example, in October 2022, Google launched its Nest Wi-Fi Pro with Wi-Fi 6E support in Canada, the company's first router capable of operating in a triband mesh network. On compatible devices, Wi-Fi 6E (E for Extended), which uses the new, less-congested 6 GHz radio band, provides speeds up to two times quicker than Wi-Fi 6.

Wi-Fi Router Industry Overview

The Wi-Fi router market is moderately consolidated with the presence of several players like Cisco Systems Inc, Ericsson Inc., Huawei Technologies Co. Ltd., Juniper Networks Inc., Alcatel Lucent Enterprise, etc. The companies continuously invest in strategic partnerships and product developments to gain substantial market share.

In March 2023, NETGEAR introduced its first Wi-Fi 7-capable router, the Nighthawk RS700 - possibly one of the fastest consumer-grade networking devices capable of a 19 Gbps peak data rate. NETGEAR stated the tri-band unit is designed for low-latency AR(Augmented Reality)/VR (Virtual reality) gaming, UHD Zoom calls, 8k simultaneous streaming, and many more. The RS700 has a new tower-like shape not reminiscent of the last Nighthawk routers, which is designed to house antennas for 360-degree coverage of up to 3,500 square feet.

In November 2022, TP-Link, a global consumer and business networking product provider, released an entire home and business Wi-Fi 7 product line. TP-Link launched new Wi-Fi 7 routers, Omada EAPs, Deco products, and Aginet products for ISP markets to cover all usage scenarios. TP-Link's new HomeShield 3.0 also provides more reliable and smarter network solutions. Continuing as one of the top performances of the Archer series, Wi-Fi 7 routers bring unprecedented experiences to homes. Three Wi-Fi 7 routers were unveiled at the event. Among them, Archer BE900 has quad-band 24 Gbps Wi-Fi 7 speeds and has a brand new design reimagined from previous routers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

- 4.5 Use Cases

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in Internet Traffic and Increasing Consumer Demand for Internet-enabled Devices

- 5.1.2 Exponential Increase in the Bandwidth Requirements across Enterprises owing to Digitization

- 5.2 Market Restraints

- 5.2.1 Network Security and Complexities Related to Network Management

- 5.2.2 Usage of Mobile Broadband

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Edge Router

- 6.1.2 Core Router

- 6.2 By Organization Size

- 6.2.1 SMEs

- 6.2.2 Large Enterprises

- 6.3 By End-User Industry

- 6.3.1 Healthcare

- 6.3.2 Transportation & Logistics

- 6.3.3 Retail & eCommerce

- 6.3.4 Manufacturing

- 6.3.5 Government

- 6.3.6 BFSI

- 6.3.7 Others

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Middle East and Africa

- 6.4.6 Latin America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc

- 7.1.2 Ericsson Inc.

- 7.1.3 Huawei Technologies Co.ltd

- 7.1.4 Juniper Networks Inc.

- 7.1.5 Alcatel Lucent Enterprise SAS

- 7.1.6 ARUBA S.P.A

- 7.1.7 Fortinet Inc.

- 7.1.8 Panasonic Corporation

- 7.1.9 Broadcom Inc

- 7.1.10 Extreme Networks Inc.

8 INVESTMENT ANALYSIS

9 FUTURE TRENDS

全球行動Wi-Fi(MiFi)市場:機會與策略展望(至2035年)

全球行動Wi-Fi(MiFi)市場:機會與策略展望(至2035年) 行動Wi-Fi(MiFi)市場規模、佔有率和趨勢分析報告:按設備類型、技術、連接方式、最終用途和細分市場預測(2026-2033年)2026年全球家用Wi-Fi路由器市場報告

行動Wi-Fi(MiFi)市場規模、佔有率和趨勢分析報告:按設備類型、技術、連接方式、最終用途和細分市場預測(2026-2033年)2026年全球家用Wi-Fi路由器市場報告 2026-2030年全球家用Wi-Fi路由器市場

2026-2030年全球家用Wi-Fi路由器市場 Wi-Fi適配器卡市場 - 全球產業規模、佔有率、趨勢、機會、預測:按作業系統支援、應用、速度、地區和競爭格局分類,2021-2031年家用 Wi-Fi 路由器全球市場:2033 年的機會與策略

Wi-Fi適配器卡市場 - 全球產業規模、佔有率、趨勢、機會、預測:按作業系統支援、應用、速度、地區和競爭格局分類,2021-2031年家用 Wi-Fi 路由器全球市場:2033 年的機會與策略 家用無線路由器的全球市場:市場佔有率與排行榜,整體銷售額與需求預測(2024年~2030年)

家用無線路由器的全球市場:市場佔有率與排行榜,整體銷售額與需求預測(2024年~2030年) 全球消費級 Wi-Fi 路由器市場:未來預測(2025-2030 年)

全球消費級 Wi-Fi 路由器市場:未來預測(2025-2030 年)