|

市場調查報告書

商品編碼

1693833

中東氟聚合物:市場佔有率分析、產業趨勢、統計數據和成長預測(2024-2029)Middle East Fluoropolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

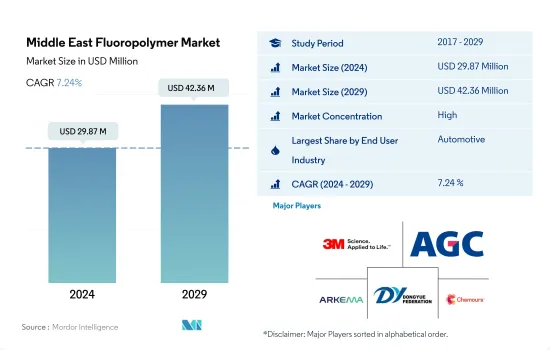

預計 2024 年中東氟聚合物市場規模將達到 2,987 萬美元,預計到 2029 年將達到 4,236 萬美元,預測期內(2024-2029 年)的複合年成長率為 7.24%。

航太和汽車產業帶來市場機會

- 氟聚合物應用於石油和天然氣、半導體和電子、化學加工、汽車、電線和電纜、建築、航太和製藥等領域。中東氟聚合物市場受建築業和汽車業的推動,2021 年的銷售佔有率分別為 9.75% 和 39.96%。

- 建築業是該地區最大的氟聚合物消費產業。 2022 年中東氟聚合物市場規模佔有率為 11.4%。該地區的新占地面積預計將從 2022 年的 42 億平方英尺增加到 2029 年的 49 億平方英尺,這將推動未來幾年對氟聚合物的需求。

- 汽車業是該地區第二大氟聚合物消費產業,2022 年佔消費量佔有率的 25.58%。該產業 2022 年的汽車產量與 2021 年相比成長了 32.8%。預計在預測期內,電動車關鍵零件鋰離子電池中氟聚合物消費量的增加將推動市場發展。

- 預計航太業將成為該地區成長最快的產業,以收益計算,預測期內(2023-2029 年)的複合年成長率為 8.42%。這種成長是由於含氟聚合物組件能夠承受侵蝕性蝕刻過程並提供製造航太工業中使用的微晶片和其他電子設備所需的純度。它也用於塗覆各種航太部件,因為它可以承受極端溫度並耐腐蝕。

阿拉伯聯合大公國的投資推動了對氟聚合物的需求

- 中東地區使用含氟聚合物作為工業機械和汽車的塗層和襯裡等。在該地區的氟聚合物市場中,沙烏地阿拉伯和阿拉伯聯合大公國佔全球氟聚合物市場總銷售額的0.83%。

- 沙烏地阿拉伯是該地區最大的氟聚合物消費國,佔以金額為準的 25.69%,受需求成長的推動,其中航太、汽車和工業機械領域是主要應用領域。汽車產量的成長推動了沙烏地阿拉伯氟聚合物市場的發展,到 2022 年全部區域佔有率將達到 1.13%。

- 阿拉伯聯合大公國是中東氟聚合物市場的第二大消費國,2022 年的銷售佔有率為 6.06%。隨著該國電子製造業收益,預計預測期內阿拉伯聯合大公國對氟聚合物的需求將會增加。

- 受汽車產量成長的推動,中東其他地區是中東最大的市場之一,佔氟聚合物市場以金額為準的 58.8%。中東其他地區佔全部區域的98.4%。

- 阿拉伯聯合大公國是該地區發展最快的國家,預計預測期內收入的複合年成長率約為 7.06%。預計這一成長是阿拉伯聯合大公國投資計畫的結果,該計畫旨在到 2033 年實現經濟規模加倍,並作為金融中心在經濟的創新驅動技術領域累計8.7 兆美元。

中東氟聚合物市場趨勢

政府和私人企業的投資增加

- 在中東,沙烏地阿拉伯已迅速崛起為電氣電子產業主要市場之一。除石油和天然氣工業外,沙烏地阿拉伯擁有龐大的消費群和廣泛的工業,這些都推動了電氣和電子工業年產量的快速成長。因此,2017年至2019年期間,該地區電氣和電子設備生產以收益為準的複合年成長率為18%。

- 2020年,新冠疫情增加了遠距辦公和家庭娛樂家用電子電器產品的需求。 2020年,沙烏地阿拉伯的智慧型手機普及率達到全球最高,約97%,約60%的沙烏地阿拉伯消費者能夠透過社群網路發現新的賣家。沙烏地阿拉伯電子商務成長近60%(2019-2020年),主要原因是受到疫情的影響。電氣和電子產品生產收益比上年度成長1.8%。

- 預計預測期內(2023-2029 年),電氣和電子製造業的複合年成長率為 8.51%。成長的主要動力可能是政府和三星等製造商的投資增加。三星也在中東推廣其 5G 無線技術。沙烏地阿拉伯已根據其「2030願景」計畫推出了5G網路。預計所有這些因素都將在預測期內促進該地區的電子產品生產。

中東氟聚合物產業概況

中東氟聚合物市場相當集中,前五大公司佔75.30%的市佔率。該市場的主要企業包括 3M、AGC Inc.、阿科瑪、東岳集團、科慕公司等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 電氣和電子

- 包裝

- 進出口趨勢

- 氟樹脂交易

- 法律規範

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 電氣和電子

- 工業/機械

- 其他

- 子樹脂類型

- 乙烯-四氟乙烯(ETFE)

- 氟化乙丙烯 (FEP)

- 聚四氟乙烯(PTFE)

- 聚氟乙烯(PVF)

- 聚二氟亞乙烯(PVDF)

- 其他子樹脂類型

- 國家

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

第6章 競爭格局

- 重大策略舉措

- 市場佔有率分析

- 商業狀況

- 公司簡介

- 3M

- AGC Inc.

- Arkema

- Dongyue Group

- Solvay

- The Chemours Company

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 5000171

The Middle East Fluoropolymer Market size is estimated at 29.87 million USD in 2024, and is expected to reach 42.36 million USD by 2029, growing at a CAGR of 7.24% during the forecast period (2024-2029).

Aerospace and automotive industries to create opportunities for the market

- Fluoropolymers have applications in oil and gas, semiconductor and electronic, chemical processing, automotive, wire and cable, building, aerospace, and pharmaceutical sectors. The Middle Eastern fluoropolymer market is led by the building and construction and automotive industries, accounting for 9.75% and 39.96% shares in 2021 in terms of revenue.

- The building and construction industry is the largest consumer of fluoropolymers in the region. It held a share of 11.4% of the Middle Eastern fluoropolymer market in 2022 by volume. The region's new floor area is expected to reach 4.9 billion sq. ft by 2029 from 4.2 billion sq. ft in 2022, which is expected to drive the demand for fluoropolymers in the coming years.

- The automotive industry is the second-largest consumer of fluoropolymers in the region, accounting for 25.58% of the consumption share in 2022 by volume. The industry witnessed a 32.8% increase in the production of vehicles by volume in 2022 compared to 2021. The increased consumption of fluoropolymers in lithium-ion batteries, the main components of an EV, is expected to drive the market during the forecast period.

- The aerospace industry is expected to be the fastest-growing industry in the region in terms of revenue, with a CAGR of 8.42% during the forecast period (2023-2029). This growth can be attributed to the fluoropolymer component's ability to withstand the aggressive etching process and provide the necessary purity required to produce microchips and other electronics used in the aerospace industry. It is also used in the coatings of various aerospace components as it can withstand extreme temperatures and resist corrosion.

Investments in UAE to boost the demand for fluoropolymer

- Fluoropolymers are used in the Middle East for applications such as coatings and liners for industrial machinery, automotive, and many others. The fluoropolymers market in the region is dominated by Saudi Arabia and the United Arab Emirates, with a share of 0.83% of the revenue of the global overall fluoropolymers market.

- Saudi Arabia is the largest consumer in the regional fluoropolymer market, with a share of 25.69% by a value in major applications in the aerospace, automotive, and industrial machinery sectors due to increasing demand. The rise in the production of automobiles drives the fluoropolymer market in Saudi Arabia, which contributed a 1.13% share of the overall region in 2022.

- The United Arab Emirates is the second-largest consumer in the Middle Eastern fluoropolymer market, with a share of 6.06% of the revenue in 2022. With a CAGR of 8.71% in terms of revenue from electronics production in the country, the demand for fluoropolymers in the United Arab Emirates is likely to increase during the forecast period.

- The Rest of the Middle East segment is one of the largest markets in the Middle East, with a share of 58.8% by value of the fluoropolymer market due to the rise in automotive production. Automotive production in the Rest of Middle East has a share of 98.4% in the overall Middle Eastern region.

- The United Arab Emirates is the fastest-growing country in the region, with an expected CAGR of around 7.06% by revenue during the forecast period. This growth is expected to be a result of the plans for investment in the United Arab Emirates' financial hub to double the size of its economy by 2033, accounting for USD 8.7 trillion in economic development technology sectors through innovation.

Middle East Fluoropolymer Market Trends

Growing investments from the government and private players

- In the Middle East, Saudi Arabia is quickly emerging as one of the key markets for the electrical and electronics industry. Aside from the oil and gas industry, the country has a sizable consumer base and a broad range of industrial pursuits, contributing to the rapid annual increase in production for the electrical and electronics industry. Thus, electrical and electronics production in the region registered a CAGR of 18% from 2017 to 2019 in revenue terms.

- In 2020, the demand for consumer electronics for remote working and home entertainment increased due to the COVID-19 pandemic. In 2020, Saudi Arabia registered the highest smartphone penetration rate, around 97%, in the world, which enabled approximately 60% of Saudi customers to discover new sellers through social networks. Saudi Arabia faced a higher rate of e-commerce growth, nearly 60% (between 2019 and 2020), mainly due to the pandemic. The revenue from electrical and electronics production increased by 1.8% compared to the previous year.

- Electrical and electronic production is expected to witness a CAGR of 8.51% in value during the forecast period (2023-2029). The major driving component behind the growth is likely to be the growing investments from the government and the manufacturers like Samsung. Samsung has also been pitching its 5G wireless technology to the Middle East. Saudi Arabia implemented a 5G network in line with the Vision 2030 initiative. All such factors are expected to boost electronics production over the forecast period in the region.

Middle East Fluoropolymer Industry Overview

The Middle East Fluoropolymer Market is fairly consolidated, with the top five companies occupying 75.30%. The major players in this market are 3M, AGC Inc., Arkema, Dongyue Group and The Chemours Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Fluoropolymer Trade

- 4.3 Regulatory Framework

- 4.3.1 Saudi Arabia

- 4.3.2 United Arab Emirates

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Other End-user Industries

- 5.2 Sub Resin Type

- 5.2.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.3 Polytetrafluoroethylene (PTFE)

- 5.2.4 Polyvinylfluoride (PVF)

- 5.2.5 Polyvinylidene Fluoride (PVDF)

- 5.2.6 Other Sub Resin Types

- 5.3 Country

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Arkema

- 6.4.4 Dongyue Group

- 6.4.5 Solvay

- 6.4.6 The Chemours Company

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

高性能含氟聚合物市場規模、佔有率及成長分析(按類型、應用、形態、最終用途產業及地區分類)-2025-2032年產業預測

高性能含氟聚合物市場規模、佔有率及成長分析(按類型、應用、形態、最終用途產業及地區分類)-2025-2032年產業預測 氟聚合物加工助劑市場分析與預測(至2034年):類型、產品、應用、技術、材料類型、最終用戶、製程、功能

氟聚合物加工助劑市場分析與預測(至2034年):類型、產品、應用、技術、材料類型、最終用戶、製程、功能 半導體氟聚合物管材市場:依最終用途、材料、應用、管材類型、製造流程和直徑範圍分類-全球預測,2025-2032年氟聚合物市場:2025-2032年全球預測(按類型、應用、形態、製造流程和最終用戶分類)醫用含氟聚合物市場依產品類型、形態、應用、終端用戶產業及技術分類-2025-2032年全球預測高性能含氟聚合物市場:依產品類型、應用、終端用戶產業、形態和製造流程分類-2025-2032年全球預測

半導體氟聚合物管材市場:依最終用途、材料、應用、管材類型、製造流程和直徑範圍分類-全球預測,2025-2032年氟聚合物市場:2025-2032年全球預測(按類型、應用、形態、製造流程和最終用戶分類)醫用含氟聚合物市場依產品類型、形態、應用、終端用戶產業及技術分類-2025-2032年全球預測高性能含氟聚合物市場:依產品類型、應用、終端用戶產業、形態和製造流程分類-2025-2032年全球預測 2032 年航太氟聚合物市場預測:按產品、飛機類型、應用、最終用戶和地區進行的全球分析

2032 年航太氟聚合物市場預測:按產品、飛機類型、應用、最終用戶和地區進行的全球分析 2025-2033年氟聚合物市場報告(依產品類型、應用、最終用途產業和地區)半導體氟聚合物市場:按類型、產品類型、應用和銷售管道- 全球預測 2025-2030氟加工助劑市場(按聚合物類型、形態、應用、最終用途產業和分銷管道)—2025-2030 年全球預測

2025-2033年氟聚合物市場報告(依產品類型、應用、最終用途產業和地區)半導體氟聚合物市場:按類型、產品類型、應用和銷售管道- 全球預測 2025-2030氟加工助劑市場(按聚合物類型、形態、應用、最終用途產業和分銷管道)—2025-2030 年全球預測

▼