|

市場調查報告書

商品編碼

1693831

南美氟聚合物:市場佔有率分析、產業趨勢和成長預測(2024-2029)South America Fluoropolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

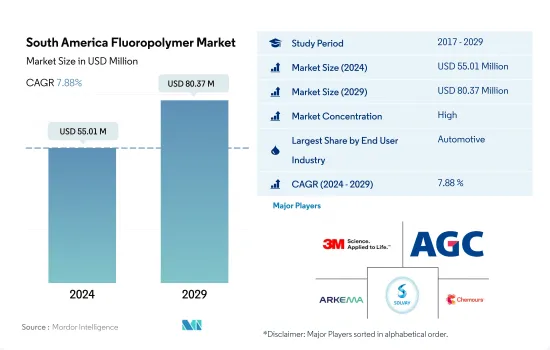

南美氟樹脂市場規模預計在 2024 年達到 5,501 萬美元,預計到 2029 年將達到 8,037 萬美元,預測期內(2024-2029 年)的複合年成長率為 7.88%。

阿根廷汽車工業主導氟聚合物市場

- 由於其多功能性和韌性,氟聚合物已在各種最終用戶行業中得到應用。 2022年,由於工業應用的不斷增加,氟聚合物已成為越來越商業性的材料。氟樹脂的常見用途包括烹調器具、電線、半導體、醫療設備、屋頂材料和防水膜。

- 2017-19年期間,氟聚合物的需求呈現穩定成長,主要受該地區電氣和電子產品成長的推動。 2020年,受疫情影響,各種業務、旅行和貿易限制導致氟聚合物的需求與前一年同期比較17.88%。在所有終端用戶產業中,汽車和工業機械產業的需求受到的打擊最嚴重,其2019年的銷售額分別下降了32.66%和28.41%。隨著限制措施的放寬,對氟聚合物的需求增加到疫情前的水平。這一成長主要受到阿根廷的推動。

- 氟聚合物的應用日益廣泛,是因為它們能夠承受高低溫和嚴重的腐蝕環境,預計大多數化學物質將推動對氟聚合物的需求成長。在南美洲所有終端用戶中,阿根廷的汽車產業預計將經歷最高成長,預測期內的複合年成長率為 10.65%。預計在預測期內,該地區對氟聚合物的需求量將以 6.21% 的複合年成長率成長,以金額為準將以 7.95% 的複合年成長率成長。

阿根廷經濟呈現高成長態勢,受汽車產業快速成長支撐

- 南美洲是全球第四大氟聚合物消費量,2022 年的消費量比重僅 1.43%。在南美洲,氟塑膠用於電氣/電子、汽車和醫療設備製造業的各種應用。

- 預計預測期內對氟聚合物的需求將穩定成長,複合年成長率為 6.19%。在該地區所有國家的所有子樹脂類型中,阿根廷對氟化乙丙烯 (FEP) 的需求成長最快。就數量而言,預計預測期內複合年成長率為 8.40%。

- 2020年,疫情期間的營運和貿易限制導致勞動力短缺、原料短缺等各種限制因素嚴重影響了各個終端用戶產業,對該地區對氟聚合物的需求產生了負面影響。其中,巴西對氟聚合物的需求受到的打擊最為嚴重。 2020年巴西需求量較去年與前一年同期比較13.20%,地區較去年與前一年同期比較下降10.18%。

- 2021 年,限制措施有所放寬,對氟聚合物的需求超過了疫情前的水準。這一成長主要得益於阿根廷等國家汽車產量的快速擴張。預計這一成長趨勢將在整個預測期內持續下去,其中阿根廷對氟聚合物的需求將成長最快。總體而言,南美洲對氟聚合物的需求預計將成長,預測期內以收益為準的複合年成長率為 7.93%。

南美洲氟聚合物市場趨勢

技術創新步伐加快推動產業成長

- 在南美洲,巴西在2017年佔據該地區電氣和電子產品製造業收益的最大佔有率,接近40%。 2017年,巴西電子產品在電商領域的滲透率接近20%。該地區的技術進步增加了對智慧電視、智慧冰箱、智慧空調等家用電子電器產品以及其他電氣和電子產品的需求。 2017-2019年期間,南美電氣和電子製造業收入的複合年成長率超過6.16%。

- 2020年,受疫情影響,遠距辦公和家庭娛樂等家用電子電器產品需求增加,該地區電氣和電子產品產量較去年與前一年同期比較成長1.1%。可支配收入的增加、奢侈品需求的不斷成長、技術進步和生活水準的提高是推動電氣和電子設備市場成長的一些關鍵因素。因此,該地區 2021 年電氣和電子設備產量銷售額也成長了 14.9%。

- 電子創新的快速步伐推動著對更新、更快的電氣和電子產品的持續需求。因此,該地區對電氣和電子設備生產的需求也在增加。 LG、三星、微軟、松下、戴爾、英特爾、東芝、索尼、飛利浦、夏普、蘋果和聯想等跨國公司的存在也對電氣和電子設備市場產生了積極影響。預計所有這些因素將在預測期內推動該地區電氣和電子設備產量增加約 7%。

南美洲氟聚合物產業概況

南美洲氟聚合物市場相當集中,前五大公司佔了79.37%的市佔率。市場的主要企業包括 3M、AGC Inc.、Arkema、Solvay、The Chemours Company 等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 電氣和電子

- 包裝

- 進出口趨勢

- 氟樹脂交易

- 法律規範

- 阿根廷

- 巴西

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 電氣和電子

- 工業/機械

- 其他

- 子樹脂類型

- 乙烯-四氟乙烯(ETFE)

- 氟化乙丙烯 (FEP)

- 聚四氟乙烯(PTFE)

- 聚氟乙烯(PVF)

- 聚二氟亞乙烯(PVDF)

- 其他子樹脂類型

- 國家

- 阿根廷

- 巴西

- 南美洲其他地區

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- 3M

- AGC Inc.

- Arkema

- Dongyue Group

- Gujarat Fluorochemicals Limited(GFL)

- Solvay

- The Chemours Company

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 5000169

The South America Fluoropolymer Market size is estimated at 55.01 million USD in 2024, and is expected to reach 80.37 million USD by 2029, growing at a CAGR of 7.88% during the forecast period (2024-2029).

The automotive industry in Argentina to dominate the market for fluoropolymers

- Fluoropolymers find applications in a range of end-user industries due to their versatile and tough nature. In 2022, the increase in industrial applications made fluoropolymers an increasingly commercial material. Common fluoropolymer applications are cookware, wires, semiconductors, medical devices, roofing materials, and waterproof films.

- During the 2017-19 period, the demand for fluoropolymers witnessed steady growth, which was majorly driven by the increase in electrical and electronics products in the region. In 2020, due to various operational, travel, and trade restrictions, because of the pandemic, the demand for fluoropolymers witnessed a Y-o-Y decline of 17.88%. Among all end-user industries, the demand from the automotive and industrial machinery industries took the worst hit, declining by 32.66% and 28.41% of their 2019 revenue. As the restrictions eased, the demand for fluoropolymers increased to pre-pandemic levels. This growth was majorly driven by Argentina.

- The increasing applications of fluoropolymers are due to their ability to resist high and low temperatures and severe corrosive environments, and most chemicals are expected to drive the growth in the demand for fluoropolymers. Among all end users in South America, the automotive industry in Argentina is expected to witness the highest growth, with a CAGR of 10.65% in volume terms during the forecast period. The regional demand for fluoropolymers is expected to register CAGRs of 6.21% and 7.95% in volume and value terms, respectively, during the forecast period.

Argentina to exhibit high growth, aided by fast-paced automobile industry

- South America ranks fourth in the consumption of fluoropolymers globally, and it occupied a share of just 1.43%, by volume, in 2022. In South America, fluoropolymers find a range of applications in the electrical and electronics, automotive, and healthcare device manufacturing industries.

- During the forecast period, the demand for fluoropolymers is expected to witness steady growth, registering a CAGR of 6.19%, mainly driven by the rapid growth in the electrical and electronics industry in countries like Argentina. Among all sub-resin types in all countries in the region, the demand for fluorinated ethylene-propylene (FEP) in Argentina witnesses the highest growth. In volume terms, its demand is expected to record a CAGR of 8.40% during the forecast period.

- In 2020, various restraining factors like worker unavailability and raw material shortages, which resulted from operational and trade restrictions during the pandemic, severely affected various end-user industries, negatively affecting the region's fluoropolymer demand. Among all countries, Brazil's fluoropolymer demand received the biggest impact. In 2020, the country's Y-o-Y demand volume declined by 13.20%, whereas the regional Y-o-Y decline was 10.18%.

- In 2021, as the restrictions eased, fluoropolymer demand outgrew its pre-pandemic levels. This growth was majorly driven by the rapid growth in automotive production in countries like Argentina. This growth trend is expected to continue throughout the forecast period, with Argentina witnessing the highest growth in fluoropolymer demand among all countries. Overall, fluoropolymer demand from South America is expected to grow, recording a CAGR of 7.93% in revenue terms during the forecast period.

South America Fluoropolymer Market Trends

Rapid pace of technological innovations to boost the industry growth

- In South America, Brazil held the major share of nearly 40% of the region's electrical and electronics production revenue in 2017. In 2017, Brazilian electronics products had a penetration of nearly 20% in the e-commerce sector. The advancement of technology in the region increased the demand for consumer electronics products, such as smart TVs, smart refrigerators, smart air conditioners, and other electrical and electronic products. South American electrical and electronics production revenue witnessed a CAGR of over 6.16% between 2017 and 2019.

- In 2020, with the rise in demand for consumer electronics for remote working and home entertainment due to the pandemic, the production of electrical and electronic products in the region increased at a growth rate of 1.1% by revenue compared to the previous year. Rising disposable income, increased demand for luxury products, technological advancements, and improvement in living standards are some of the major factors driving the electrical and electronics market's growth. As a result, in the region, electrical and electronics production also increased at a rate of 14.9% by revenue in 2021.

- The rapid pace of electronic technological innovation is driving consistent demand for newer and faster electrical and electronic products. As a result, it has also increased the demand for the production of electrical and electronics in the region. The penetration of multinational companies, like LG, Samsung, Microsoft, Panasonic, Dell, Intel, Toshiba, Sony, Philips, Sharp, Apple, and Lenovo, also positively affects the electrical and electronics market. All such factors are expected to fuel the production revenue of electrical and electronics in the region during the forecast period at a rate of around 7%.

South America Fluoropolymer Industry Overview

The South America Fluoropolymer Market is fairly consolidated, with the top five companies occupying 79.37%. The major players in this market are 3M, AGC Inc., Arkema, Solvay and The Chemours Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Fluoropolymer Trade

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Other End-user Industries

- 5.2 Sub Resin Type

- 5.2.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.3 Polytetrafluoroethylene (PTFE)

- 5.2.4 Polyvinylfluoride (PVF)

- 5.2.5 Polyvinylidene Fluoride (PVDF)

- 5.2.6 Other Sub Resin Types

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Arkema

- 6.4.4 Dongyue Group

- 6.4.5 Gujarat Fluorochemicals Limited (GFL)

- 6.4.6 Solvay

- 6.4.7 The Chemours Company

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

高純度氟聚合物(PFA)管材和管道-2026-2032 年全球市場佔有率和排名、總銷售額和需求預測。

高純度氟聚合物(PFA)管材和管道-2026-2032 年全球市場佔有率和排名、總銷售額和需求預測。 醫用氟聚合物市場:2026-2032年全球市場預測(按產品類型、形態、技術、應用和最終用途產業分類)氟聚合物市場:按類型、形態、製程和最終用戶分類-2026-2032年全球市場預測半導體氟聚合物管材市場:管材類型、材質、製造流程、直徑範圍、應用及最終用途-2026-2032年全球市場預測5G含氟聚合物市場:依產品類型、形態、製造流程和最終用途產業分類-2026-2032年全球預測

醫用氟聚合物市場:2026-2032年全球市場預測(按產品類型、形態、技術、應用和最終用途產業分類)氟聚合物市場:按類型、形態、製程和最終用戶分類-2026-2032年全球市場預測半導體氟聚合物管材市場:管材類型、材質、製造流程、直徑範圍、應用及最終用途-2026-2032年全球市場預測5G含氟聚合物市場:依產品類型、形態、製造流程和最終用途產業分類-2026-2032年全球預測 全球高通量纖維增強塑膠(HPF)市場(至2030年):按類型(PTFE、FEP、PFA/MFA、ETFE)、形狀、應用(塗層和襯裡、組件、薄膜、添加劑)、終端用戶產業(電氣和電子、工業流程、交通運輸、醫療)和地區分類

全球高通量纖維增強塑膠(HPF)市場(至2030年):按類型(PTFE、FEP、PFA/MFA、ETFE)、形狀、應用(塗層和襯裡、組件、薄膜、添加劑)、終端用戶產業(電氣和電子、工業流程、交通運輸、醫療)和地區分類 氟聚合物加工助劑市場分析與預測(至2035年):類型、產品類型、應用、技術、材料類型、最終用戶、製程、功能

氟聚合物加工助劑市場分析與預測(至2035年):類型、產品類型、應用、技術、材料類型、最終用戶、製程、功能 全球氟聚合物市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球氟聚合物市場規模、佔有率、趨勢和成長分析報告(2026-2034) 熔融加工型氟素樹脂的市場規模、成長與預測(至2034年)功能性保護套管市場按產品類型、材質、應用、最終用途產業、分銷通路、安裝類型和直徑分類-2026年至2032年全球預測

熔融加工型氟素樹脂的市場規模、成長與預測(至2034年)功能性保護套管市場按產品類型、材質、應用、最終用途產業、分銷通路、安裝類型和直徑分類-2026年至2032年全球預測

▼