|

市場調查報告書

商品編碼

1940878

矽電容器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Silicon Capacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

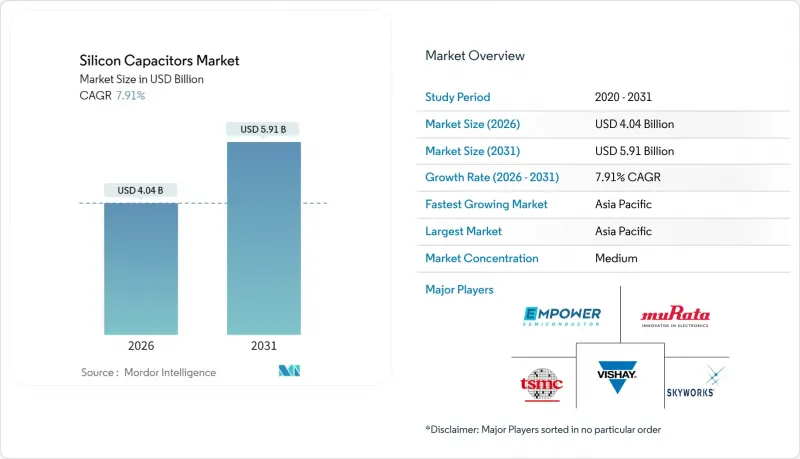

預計矽電容器市場將從 2025 年的 37.4 億美元成長到 2026 年的 40.4 億美元,到 2031 年將達到 59.1 億美元,2026 年至 2031 年的複合年成長率為 7.91%。

這一成長反映了5G和下一代6G設備對高密度射頻前端設計的快速採用、向高溫汽車雷射雷達模組的轉變,以及對具有嵌入式深溝槽電容器的基於晶片組的2.5D中介層的強勁需求。代工廠為先進被動元件分配的新生產線提高了碳奈米纖維MIM結構的供應穩定性,並緩解了先前的成本上升趨勢。亞太地區憑藉其一體化的晶圓製造基地和積極的無線基礎設施部署,保持著明顯的生產優勢。同時,北美正在搶佔來自工作頻率高於100GHz的國防級平板陣列的高階市場需求。隨著傳統被動元件供應商努力抵禦代工廠將嵌入式電容器與邏輯晶粒捆綁在一起的產品,競爭格局日益激烈。這導致大批量智慧型手機產品的毛利率下降,但惡劣環境細分市場仍保持著成長潛力。

全球矽電容器市場趨勢與洞察

加速5G/6G終端射頻前端的小型化

與4G設計相比,下一代智慧型手機將整合40-60%的電容元件,這將迫使OEM廠商從陶瓷MLCC轉向矽介質,進而降低6-40GHz頻段的寄生電感。村田製作所於2025年3月發布的數位封包追蹤平台,透過在追蹤模組中整合矽電容器,實現了寬頻5G訊號25%的功率效率提升。此方案與3GPP Release 18為6G所做的準備一致,後者透過在24個頻譜區塊上的多頻段運行,提升了緊湊型高Q值被動元件的價值。代工廠級深溝槽整合技術進一步降低了15-20%的RF-SIP封裝成本,同時滿足了主流智慧型手機品牌設定的低於8mm的Z軸高度限制。預計這些趨勢將使亞太地區——全球最大的智慧型手機ODM叢集所在地——成為近期需求中心。

用於汽車LiDAR的150°C環保矽電容器的過渡

在L3及以上等級的車輛中整合攝影機和雷射雷達(LiDAR)後,感測器模組將被放置在引擎蓋下方,使被動元件暴露在超過150°C的高溫下。矽電容器的電容特性比多層陶瓷電容器(MLCC)更穩定,後者在相同壓力下電容損失高達65%。 ROHM於2024年9月與Denso建立合作關係,旨在滿足高溫環境下模擬前端(AFE)日益成長的需求,這也加劇了AEC-Q200 0級元件漫長的設計採用週期。目前,高階電動車平台通常配備8至12個雷射雷達單元,每個單元包含20至30個矽電容器,用於偏壓、平滑和電磁干擾抑制。預計到2027年,這將推動年需求成長1.5億美元。雖然歐洲是領先的應用市場,但隨著美國聯邦新車碰撞測試(NCAP)標準的加強,美國製造商也在加速採購,因為基於雷射雷達的安全系統需要進行評估。

偏壓高於 25V 時,MLCC 的電荷洩漏狀況

當偏壓超過 25V 時,二氧化矽多層電容器的漏電流會急劇增加,這限制了它們在輕度混合動力車中新興的 48V 架構中的適用性。擊穿電壓通常約為 34V,遠低於陶瓷元件標準的 50V 額定電壓。設計人員若採用額外的穩壓級來確保其工作在安全範圍內,則成本會增加 8-12%,這限制了它們在工業驅動器和汽車轉換器中的應用。高溫會加劇這一問題,導致長期保持性能下降,迫使原始設備製造商 (OEM) 儘管存在尺寸和壓電噪聲等缺點,仍需在高壓線路中繼續使用 MLCC。

細分市場分析

到2025年,深溝槽製程將佔據矽電容器市場35.70%的佔有率,這得益於其3D側壁結構的優勢,能夠在較小的晶粒面積內實現高電容。金屬-金屬-絕緣體(MIM)矽電容器市場規模成長最快,年複合成長率達9.03%,主要得益於碳奈米纖維電極的運用,無需使用特殊材料即可將電容密度提升至200 nF/mm²。金屬-金屬-絕緣體(MOS)和金屬-金屬-絕緣體(MIS)電容器仍處於小眾市場,主要應用於電壓調節器振盪器,在這些應用中,線性度比電容密度更為重要。目前的戰略藍圖目標是將介電常數提升至60以上,到2027年將溝槽電容器的電容密度提升至500 nF/mm²,從而增強其在行動SoC緊湊型電源網路中的吸引力。

該設計主要應用於行動電話和2.5D AI加速器的電源管理積體電路(PMIC)領域,其中凹槽溝槽結構減少了去耦層的數量,從而實現了更小的封裝厚度。雖然生產規模取決於代工廠的投資,但多計劃晶圓為無晶圓廠新興企業提供了更便捷的原型製作途徑。專業IP供應商與大型代工廠之間的授權協議降低了進入門檻,從而促進了該技術在消費性電子和汽車市場的應用。

3D矽通孔結構將垂直互連和電容儲存整合於單一製程中,從而簡化高頻寬記憶體堆疊,預計到2025年將佔總收入的38.05%。同時,用於超薄電源層的尖端人工智慧封裝所採用的CNF-MIM方案,其複合年成長率將達到9.21%。在穿戴式裝置領域,成本優先於效能,因此平面設計仍將繼續應用。而矽通孔深溝槽橋接技術將填補這一空白,它比平面設計提供更高的Q值,同時又比TSV技術降低了複雜性。

下一代CNF層的認證週期正在快速推進,Smoltek在2025年的檢驗測試中實現了200nF/mm²、34V擊穿電壓的性能。隨著封裝公司對TSV和電容器的模具進行標準化,供應商可以提供針對每個晶粒區域最佳化的混合結構解決方案。這種模組化設計將有助於與伺服器和航太整合商保持業務往來,滿足他們對跨不同供電線路的客製化電阻控制的需求。

區域分析

預計到2025年,亞太地區將佔據全球矽電容器市場45.95%的佔有率,並在2031年之前維持8.84%的複合年成長率。中國將憑藉其積極的5G大型基地台部署和全球最大的電動車用戶群推動市場成長,而日本和韓國將憑藉Material-2技術和精密汽車需求做出貢獻。台灣的晶圓代工生態系能夠即時提供深溝槽和CNF-MIM生產,進而縮短無晶圓廠客戶的設計週期。印度的生產連結獎勵計畫正在吸引分立被動元件組裝,但與全部區域生產規模相比仍處於起步階段。在區域政府的支持下,新的300mm生產線正在建設中,這將直接提升矽電容器產業的產能。

北美正在整合國防、航太和高效能運算的需求,導致產量低但單價高。美國國防部的安全供應指令有利於國內先進封裝技術的發展,進而擴大了矽電容器市場。美國在亞利桑那州、德克薩斯州和俄亥俄州的晶圓廠計劃將溝槽電容器後端處理模組與邏輯晶圓生產相結合,從而減少對海外供應的依賴。密西根州和加州的電動車製造商正在為其48V子系統指定使用高溫矽電容器,從而將其產品組合擴展到汽車領域,而汽車行業傳統上一直以大型航太製造商為中心。

在歐洲,汽車可靠性和工業自動化至關重要。德國一級供應商已簽署多年期契約,供應用於LiDAR偏壓和碳化矽逆變器平滑的0級電容器,即使汽車產量出現波動,也能維持到2031年的區域需求。法國和義大利的航太叢集需要用於小型衛星載具的抗輻射加固型被動元件,這些元件為100GHz以上的高階市場提供動力。歐盟環境法規,包括將REACH和RoHS擴展至不含PFAS的材料,正在推動矽介質在陶瓷面臨合規性審查的領域中得到應用。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 5G/6G行動電話射頻前端的快速小型化

- 用於汽車LiDAR的150°C環保矽電容的過渡

- 快速採用具有嵌入式溝槽電容器的晶片組/2.5D中介層

- 毫米波衛星通訊對平板陣列的需求不斷成長

- 由於國防級IPD要求,SWaP-C有所降低

- 適用於小於 1mm² DC-DC 模組的功率 IC 整合,採用矽上去耦技術

- 市場限制

- 偏壓高於 25V 時,電荷洩漏和 MLCC 的比較

- 鑄造廠深槽加工產能限制

- 在消費品物料清單中,比較高價值產品與傳統被動元件。

- 在高濕度(相對濕度 85% 或更高)環境下可靠性的差異

- 業界バリューチェーン分析

- 監管環境

- 技術展望

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素如何影響市場

第5章 市場規模與成長預測

- 透過技術

- MOS

- MIS

- 深海溝

- MIM

- 透過電容器結構

- Planar

- 3D TSV

- シリコン貫通深溝技術

- カーボンナノファイバーMIM(CNF-MIM)

- 透過最終用戶應用程式

- 汽車與出行

- 家用電子電器

- 資訊科技和電訊

- 航太/國防

- 醫療保健和醫療設備

- 按頻段

- 低於 6 GHz

- 6-40 GHz

- 40-100 GHz

- 超過 100 GHz(亞太兆赫頻段)

- 依整合程度

- 分立式SMD

- 嵌入式PCB

- 矽中介層(2.5D)

- オンチップ(モノリシック)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Murata Manufacturing Co., Ltd.

- KYOCERA AVX Components Corporation

- Vishay Intertechnology, Inc.

- Skyworks Solutions, Inc.

- Taiwan Semiconductor Manufacturing Company Limited(TSMC)

- Empower Semiconductor, Inc.

- MACOM Technology Solutions Holdings, Inc.

- Microchip Technology, Inc.

- ELOHIM, Inc.

- Massachusetts Bay Technologies, Inc.

- Smoltek Semi AB

- Fraunhofer IPMS

- ROHM Co., Ltd.

- STMicroelectronics NV

- Onsemi Corporation

- Infineon Technologies AG

- Wolfspeed, Inc.

- Samtec, Inc.(Glass interposer Si-Cap)

- Knowles Precision Devices LLC

- Wurth Elektronik GmbH & Co. KG

- KEMET(Yageo Corporation)

第7章 市場機會與未來展望

The silicon capacitors market is expected to grow from USD 3.74 billion in 2025 to USD 4.04 billion in 2026 and is forecast to reach USD 5.91 billion by 2031 at 7.91% CAGR over 2026-2031.

This expansion tracks the rapid proliferation of high-density RF front-end designs for 5G and nascent 6G devices, the shift toward high-temperature automotive LiDAR modules, and the strong push for chiplet-based 2.5D interposers that embed deep-trench capacitors. Supply stability for carbon-nanofiber MIM structures is improving as foundries allocate new lines to advanced passive components, tempering earlier cost inflation. Asia-Pacific retains clear production leadership because of its concentrated wafer fabrication base and aggressive wireless-infrastructure roll-outs, while North America captures premium demand from defense-grade flat-panel arrays operating above 100 GHz. Competitive intensity is rising as traditional passive-component vendors defend share against foundry-level offerings that bundle embedded capacitors with logic dies, narrowing gross-margin spreads on high-volume phones yet preserving upside in extreme-environment niches.

Global Silicon Capacitors Market Trends and Insights

Accelerated RF-front-end miniaturization in 5G/6G handsets

Next-generation smartphones integrate 40-60% more capacitive elements than 4G designs, forcing OEMs to migrate from ceramic MLCCs to silicon dielectrics that mitigate parasitic inductance at 6-40 GHz. Murata's March 2025 Digital Envelope Tracking platform demonstrates a 25% power-efficiency gain in broadband 5G signals by embedding silicon capacitors within the tracker module. The approach aligns with 3GPP Release 18 preparations for 6G, where multi-band operation across 24 spectrum blocks elevates the value of compact, high-Q passives. Foundry-level deep-trench integration further eliminates 15-20% of RF-SIP assembly cost while meeting sub-8 mm z-height limits set by tier-one handset brands. These dynamics position Asia-Pacific, home to the largest smartphone ODM cluster, as the near-term demand epicenter.

Automotive LiDAR shift to >150 °C environment-grade silicon capacitors

Camera-lidar fusion in Level 3+ vehicles is pushing sensor modules under the hood, exposing passives to >=150 °C. Silicon capacitors retain capacitance far more predictably than MLCCs, which lose up to 65% under identical stress. ROHM's September 2024 tie-up with DENSO targets high-temperature analog front-ends, reinforcing the long-cycle design wins typical of AEC-Q200 Grade 0 parts. Premium electric-vehicle platforms now specify 8-12 lidar units, each embedding 20-30 Si-Caps for bias, smoothing, and EMI suppression, translating to a USD 150 million annual uplift by 2027. Europe remains the early adopter, yet U.S. makers are accelerating procurement as federal NCAP upgrades reward lidar-backed safety stacks.

Charge-leakage versus MLCC at greater than 25 V bias

Leakage current rises sharply in silicon dioxide stacks when bias surpasses 25 V, limiting suitability for the 48 V architectures emerging in mild-hybrid vehicles. Breakdown typically occurs near 34 V, well below the 50 V routine for ceramic parts. Designers adding extra regulation stages to stay within safe-operating limits report 8-12% cost penalties, constraining adoption in industrial drives and automotive converters. Elevated temperatures compound the issue, degrading long-term retention and forcing OEMs to retain MLCCs for high-voltage rails despite the volume and piezo-electric noise drawbacks.

Other drivers and restraints analyzed in the detailed report include:

- Rapid adoption of chiplet/2.5 D interposers with embedded trench capacitors

- Limited foundry capacity for deep-trench processing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Deep-Trench processes secured 35.70% silicon capacitors market share in 2025, benefiting from three-dimensional sidewalls that achieve high capacitance within tight die footprints. The silicon capacitors market size attributed to MIM variants is rising quickest, expanding at 9.03% CAGR as carbon-nanofiber electrodes lift density to 200 nF/mm2 without exotic materials. MOS and MIS remain niche, servicing voltage-controlled oscillators where linearity outweighs raw density. Strategic roadmaps now target dielectric constants above 60 to push trench parts toward 500 nF/mm2 by 2027, reinforcing their appeal for compact power-delivery networks in mobile System-on-Chips.

Design wins concentrate on handset PMICs and 2.5D AI accelerators, where embedded trench banks reduce decoupling layer count and shrink package thickness. Manufacturing scale hinges on foundry investment, yet multi-project wafers are easing prototype access for fab-less start-ups. License agreements between specialty IP providers and leading fabs lower entry barriers, supporting broader technology penetration across consumer and automotive tiers.

3D through-silicon-via structures held 38.05% revenue in 2025 by combining vertical interconnect and capacitive storage within one formation step, streamlining high-bandwidth-memory stacks. Meanwhile, CNF-MIM options post a 9.21% CAGR as bleeding-edge AI packages adopt them for ultra-thin power planes. Planar designs survive in wearables where cost trumps performance, and through-silicon deep-trench bridges the middle ground by offering higher Q than planar yet lower complexity than TSV.

Qualification cycles for next-generation CNF layers progress swiftly; Smoltek recorded 34 V breakdown at 200 nF/mm2 in 2025 validation runs. As packaging houses co-locate TSV and capacitor tooling, suppliers can deliver mixed-structure solutions optimized for each die region. This modularity fosters stickiness among server and aerospace integrators that demand tailored impedance control across a range of supply rails.

The Silicon Capacitors Market Report is Segmented by Technology (MOS, MIS, Deep-Trench, and MIM), Capacitor Structure (Planar, 3D TSV, and More), End-User Application (Automotive and Mobility, Consumer Electronics, and More), Frequency Band (Less Than 6 GHz, 6-40 GHz, and More), Integration Level (Discrete SMD, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 45.95% of the silicon capacitors market in 2025 and is projected to log an 8.84% CAGR through 2031. China anchors volume with aggressive 5G macro-cell roll-outs and the world's largest electric-vehicle base, while Japan and South Korea contribute Material-2 technology and precision automotive demand. Taiwan's foundry ecosystem enables immediate access to deep-trench and CNF-MIM production, shortening design cycles for fab-less customers. India's production-linked incentives are luring discrete-passive assembly but remain nascent relative to overall regional output. Government sponsorship across the bloc underpins new 300 mm lines that directly enhance the silicon capacitors industry capacity.

North America combines defense, space, and high-performance-compute needs, delivering high ASPs despite smaller unit counts. The region's silicon capacitors market size is bolstered by DoD secure-supply mandates favoring on-shore advanced packaging. U.S. fab announcements in Arizona, Texas, and Ohio include trench-cap back-end modules integrated with logic wafer starts, improving independence from overseas supply. Electric-vehicle OEMs in Michigan and California specify high-temperature Si-Caps for 48 V subsystems, adding automotive diversification to a portfolio historically dominated by aerospace primes.

Europe emphasizes automotive reliability and industrial automation. German Tier-1 suppliers lock multi-year commitments for Grade 0 capacitors used in lidar bias and SiC inverter smoothing, maintaining regional demand through 2031 despite vehicle-production volatility. French and Italian aerospace clusters require radiation-hardened passives for small-satellite buses, reinforcing premium segments above 100 GHz. EU environmental regulations, including REACH and RoHS extensions for PFAS-free materials, drive silicon-dielectric adoption where ceramics face compliance scrutiny.

- Murata Manufacturing Co., Ltd.

- KYOCERA AVX Components Corporation

- Vishay Intertechnology, Inc.

- Skyworks Solutions, Inc.

- Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- Empower Semiconductor, Inc.

- MACOM Technology Solutions Holdings, Inc.

- Microchip Technology, Inc.

- ELOHIM, Inc.

- Massachusetts Bay Technologies, Inc.

- Smoltek Semi AB

- Fraunhofer IPMS

- ROHM Co., Ltd.

- STMicroelectronics N.V.

- Onsemi Corporation

- Infineon Technologies AG

- Wolfspeed, Inc.

- Samtec, Inc. (Glass interposer Si-Cap)

- Knowles Precision Devices LLC

- Wurth Elektronik GmbH & Co. KG

- KEMET (Yageo Corporation)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated RF-front-end miniaturisation in 5G/6G handsets

- 4.2.2 Automotive LiDAR shift to greater than 150 °C environment-grade Si-Caps

- 4.2.3 Rapid adoption of Chiplet/2.5D interposers with embedded trench capacitors

- 4.2.4 Increased demand for mmWave SAT-COM flat-panel arrays

- 4.2.5 Defence-grade IPD mandates for SWaP-C reduction

- 4.2.6 Power-IC integration of on-silicon decoupling for sub-1 mm2 DC-DC modules

- 4.3 Market Restraints

- 4.3.1 Charge-leakage vs. MLCC at greater than 25 V bias

- 4.3.2 Limited foundry capacity for deep-trench processing

- 4.3.3 High ASPs versus legacy passives in consumer BOMs

- 4.3.4 Reliability gap in high-humidity (greater than 85 % RH) applications

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 MOS

- 5.1.2 MIS

- 5.1.3 Deep-Trench

- 5.1.4 MIM

- 5.2 By Capacitor Structure

- 5.2.1 Planar

- 5.2.2 3D TSV

- 5.2.3 Through-Silicon Deep-Trench

- 5.2.4 Carbon-Nanofiber MIM (CNF-MIM)

- 5.3 By End-user Application

- 5.3.1 Automotive and Mobility

- 5.3.2 Consumer Electronics

- 5.3.3 IT and Telecommunications

- 5.3.4 Aerospace and Defence

- 5.3.5 Healthcare and Medical Devices

- 5.4 By Frequency Band

- 5.4.1 Less than 6 GHz

- 5.4.2 6-40 GHz

- 5.4.3 40-100 GHz

- 5.4.4 Greater than 100 GHz (Sub-THz)

- 5.5 By Integration Level

- 5.5.1 Discrete SMD

- 5.5.2 Embedded-PCB

- 5.5.3 Silicon Interposer (2.5D)

- 5.5.4 On-Chip (Monolithic)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Murata Manufacturing Co., Ltd.

- 6.4.2 KYOCERA AVX Components Corporation

- 6.4.3 Vishay Intertechnology, Inc.

- 6.4.4 Skyworks Solutions, Inc.

- 6.4.5 Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- 6.4.6 Empower Semiconductor, Inc.

- 6.4.7 MACOM Technology Solutions Holdings, Inc.

- 6.4.8 Microchip Technology, Inc.

- 6.4.9 ELOHIM, Inc.

- 6.4.10 Massachusetts Bay Technologies, Inc.

- 6.4.11 Smoltek Semi AB

- 6.4.12 Fraunhofer IPMS

- 6.4.13 ROHM Co., Ltd.

- 6.4.14 STMicroelectronics N.V.

- 6.4.15 Onsemi Corporation

- 6.4.16 Infineon Technologies AG

- 6.4.17 Wolfspeed, Inc.

- 6.4.18 Samtec, Inc. (Glass interposer Si-Cap)

- 6.4.19 Knowles Precision Devices LLC

- 6.4.20 Wurth Elektronik GmbH & Co. KG

- 6.4.21 KEMET (Yageo Corporation)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment