|

市場調查報告書

商品編碼

1693798

義大利資料中心:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Italy Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

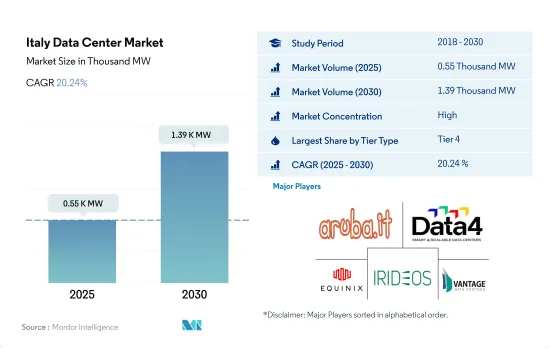

義大利資料中心市場規模預計在 2025 年達到 550MW,預計 2030 年達到 1,390MW,複合年成長率為 20.24%。

預計主機託管收益將在 2025 年達到 9.98 億美元,在 2030 年達到 26.525 億美元,預測期內(2025-2030 年)的複合年成長率為 21.59%。

預計到 2023 年,Tier 4 資料中心將佔據最大佔有率,並在整個預測期內保持主導地位。

- 早期的資料中心是為了滿足最低限度的需求而建造的。因此,所建構的資料結構設施規模很小。這些設施主要通過了 Tier 1 和 Tier 2 認證,因為它們只安裝了最低限度的機架。預計這些資料中心將佔據3%的市場佔有率,到2029年將下降到1%,該部分的IT負載能力為14.1MW。

- 在容量方面,Tier 4 資料中心引領市場。預計 Tier 4 資料中心容量將從 2023 年的 227.6MW 成長到 2029 年的 918.2MW,複合年成長率為 26.2%。義大利用戶對觀看串流內容、玩線上遊戲和網路購物的智慧型手機應用程式的需求不斷成長,促使資料中心公司增加其設施中的機架數量。

- 預計 Tier 3 設施在預測期內的成長率將位居第二,為 15.8%,該領域的 IT 負載容量預計將從 2023 年的 163.06 MW 擴大到 2029 年的 394.08 MW。此外,由於設施和基礎設施的持續發展以獲得 Uptime Institute Tier 4 認證,市場佔有率預計在 2023 年將達到 40.5%,到 2029 年將下降到 29.7%。

- 隨著越來越多的城市實施智慧系統並發展成為智慧城市,對處理數據的大型設施的需求預計將相應增加。義大利的 VOD用戶數量增加了五倍,從 2017 年的 330 萬增加到 2021 年的 1500 萬。因此,由於海量數據的產生,BFSI、媒體娛樂和製造業是預計將推動四級和三級企業成長的最終用戶群。

義大利資料中心市場趨勢

用戶滲透率的提高將刺激市場需求

- 義大利的智慧型手機使用率正在上升,預計智慧型手機普及率將從 2021 年的 77% 成長到 2025 年的 81%。儘管人口減少,但預計用戶普及率將從 2021 年的 89% 成長到 2025 年的 90%,反映出普及前景光明。

- 然而,負成長率、人口減少和平均年齡增加在決定該國的設備使用率方面發揮關鍵作用。根據義大利統計局的數據,2021 年人口平均年齡為 45.9 歲,而 2017 年為 44.9 歲。

- 義大利在數位化和採用現代通訊技術方面具有獨特的人口結構。中國是全球率先推出3G網路的國家之一,領先國際水準。政府關於「維修權」和「計畫報廢」的立法可能意味著用戶可以修理更多行動電話,避免花錢購買新智慧型手機。這可能會進一步阻礙市場上新智慧型手機數量的成長。義大利的數據生成點較少,這可能會進一步減少數據生成並影響該地區的資料中心需求。

國內對 FTTH 寬頻服務的投資將刺激市場需求

- 義大利是寬頻服務的重要消費者,有許多公司提供寬頻和超寬頻服務。該國整體寬頻連線率從2011年的約62.4%提升至2021年底的約93.5%。疫情影響了服務結構的重組,並對義大利寬頻服務基礎設施接入產生了巨大的需求。這也反映在2017年至2021年間數據流量的成長約為150%,從17,700PB成長到超過44,200PB,進一步凸顯了未來的成長前景。

- 該地區的光纖連接率從2011年的1.3%增加到2018年的64.4%,其中包括FTTH和FTTC服務。 AGCOM 數據強調,每條寬頻線路的每月數據消費量將從 2017 年的 96.6GB 成長到 2019 年的 210GB 左右。到 2021 年底,透過超寬頻服務連接住宅和商業寬頻的用戶將達到 1,870 萬,相當於每 100 人擁有約 31.7 條線路。

- 預計該國對 FTTH 寬頻服務的投資將在預測期內影響市場。基礎設施因過去的大規模投資而受益匪淺。 2022年4月,義大利電信的FiberCop與TLC Telecomunicazioni等知名公司簽署協議,共同發展FTTH接入。寬頻服務在義大利人口中的廣泛普及將有助於資料中心設施更快地傳輸數據,並利用其網路根據需要與網路交換器和通訊業者進行互動。

義大利資料中心產業概況

義大利資料中心市場高度整合,前五大公司佔89.41%的市佔率。該市場的主要企業包括 Aruba SpA、Data4、Equinix, Inc.、Irideos SpA、Vantage Data Centers LLC 等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 市場展望

- 負載能力

- 占地面積

- 主機代管收入

- 安裝機架數量

- 機架空間利用率

- 海底電纜

第5章 產業主要趨勢

- 智慧型手機用戶數量

- 每部智慧型手機的數據流量

- 行動數據速度

- 寬頻數據速度

- 光纖連接網路

- 法律規範

- 義大利

- 價值鍊和通路分析

第6章市場區隔

- 熱點

- 米蘭

- 其他中東和非洲地區

- 資料中心規模

- 大規模

- 超大規模

- 中等規模

- 超大規模

- 小規模

- 等級類型

- 1級和2級

- 第 3 層

- 第 4 層

- 吸收量

- 未使用

- 使用

- 按主機託管類型

- 超大規模

- 零售

- 批發的

- 按最終用戶

- BFSI

- 雲

- 電子商務

- 政府

- 製造業

- 媒體與娛樂

- 電信

- 其他

第7章競爭格局

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Aruba SpA

- AtlasEdge Data Centres

- CDLAN SpA

- Data4

- Equinix, Inc.

- Irideos SpA

- IT.Gate SpA

- ITnet Srl

- MIX SRL

- Seeweb Srl

- Stack Infrastructure, Inc.

- Vantage Data Centers LLC

第8章:CEO面臨的關鍵策略問題

第9章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 全球市場規模與DRO

- 資訊來源及延伸閱讀

- 圖表清單

- 關鍵見解

- 數據包

- 詞彙表

The Italy Data Center Market size is estimated at 0.55 thousand MW in 2025, and is expected to reach 1.39 thousand MW by 2030, growing at a CAGR of 20.24%. Further, the market is expected to generate colocation revenue of USD 998 Million in 2025 and is projected to reach USD 2,652.5 Million by 2030, growing at a CAGR of 21.59% during the forecast period (2025-2030).

Tier 4 data center accounted for majority share in terms of volume in 2023, and is expected to dominate through out the forecasted period

- The initial data centers were built in accordance with the minimal demand. Hence the data structure facilities created were small. These facilities were mainly Tier 1 & 2 certified due to their minimal requirements, and they had minimum racks installed. These data centers are expected to hold 3% of the market share, which is expected to decrease to 1% by 2029, with the segment accounting for an IT load capacity of 14.1 MW.

- Tier 4 data centers lead the market in terms of capacity. Tier 4 data center capacity is expected to increase from 227.6 MW in 2023 to 918.2 MW in 2029 at a CAGR of 26.2%. The increasing demand for smartphone applications to view streaming content, play online games, and shop online by Italian users has led data center companies to increase the number of racks in their facilities.

- Tier 3 facilities are expected to witness the second-highest growth of 15.8% during the forecast period, while the segment's IT load capacity is expected to grow from 163.06 MW in 2023 to 394.08 MW by 2029. It is also expected to hold a market share of 40.5% in 2023, which is expected to decrease to 29.7% by 2029, owing to the increasing development and infrastructural advancements of facilities to procure Tier 4 certification from the Uptime Institute.

- As more cities adopt smart systems and evolve into smart cities, the demand for huge facilities to process data is expected to grow proportionally. The number of subscribers to VOD in Italy increased by five times, from 3.3 million in 2017 to 15 million in 2021. Thus, BFSI, media and entertainment, and manufacturing are end-user segments expected to boost the growth of Tier 4 and Tier 3 facilities in line with huge data generation.

Italy Data Center Market Trends

Increment in the subscriber penetration rate is boosting the market demand

- Italy has increasing smartphone usage in the country, with a smartphone adoption rate expected to increase from 77% in 2021 to 81% in 2025. Despite a decreasing population, the expected increment in the subscriber penetration rate from 89% in 2021 to 90% by 2025 reflects a promising scenario for adoption.

- However, the decreasing population with a negative growth rate and higher average age play a crucial role in determining device usage in the country. The data from ISTAT highlighted the average age of the population in 2021 to be 45.9 years, compared to 44.9 years in 2017.

- Italy has a unique demographical scenario regarding digitalization and adopting the latest telecommunications technology. The country was among the initial ones to deploy a 3G network and has been ahead of the international timeline. The government legislation on the 'Right To Repair' and 'Planned Obsolescence Law' would allow users to repair their phones more, which may help them avoid expenditure on new smartphones. This may further hamper the growth of the number of new smartphones in the market. This may further lead to a decrease in data generation due to lesser data-generating points in Italy, affecting the demand for data centers in the region.

Investments in the country's FTTH broadband service is boosting the market demand

- Italy has been a significant consumer of broadband services, with companies offering broadband and ultra-broadband services. The overall broadband connections in the country increased from about 62.4% in 2011 to about 93.5% by the end of 2021. The pandemic influenced the restructuring of the services, creating significant demand to utilize the infrastructure for broadband services in Italy. This was also evident in the increase in data traffic by about 150%, from 17,700 to more than 44,200 PB from 2017 to 2021, which further highlights the future growth prospects.

- Fiber connectivity in the region increased from 1.3% in 2011 to 64.4% in 2018, including FTTH and FTTC services. The data from AGCOM highlighted the monthly data consumption per broadband line from 96.6 GB in 2017 to about 210 GB in 2019. Broadband access through residential and business ultra-broadband services by the end of 2021 reached 18.7 million units, accounting for about 31.7 lines for every 100 inhabitants.

- The investments in the country's FTTH broadband services would shape the market during the forecast period. With the significant investments in the past, the infrastructure was greatly benefitted, which would be carried forward by the operators accordingly. In April 2022, prominent players like Telecom Italia's FiberCop and TLC Telecomunicazioni signed an agreement to develop FTTH access jointly. The deep penetration of broadband services availed by the Italian population may help data center facilities to deliver data faster and leverage the network to interact with internet exchanges and telecommunication operators, as required.

Italy Data Center Industry Overview

The Italy Data Center Market is fairly consolidated, with the top five companies occupying 89.41%. The major players in this market are Aruba SpA, Data4, Equinix, Inc., Irideos SpA and Vantage Data Centers LLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 It Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 Key Industry Trends

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.6.1 Italy

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

- 6.1 Hotspot

- 6.1.1 Greater Milan

- 6.1.2 Rest of Italy

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.3.1 Aruba SpA

- 7.3.2 AtlasEdge Data Centres

- 7.3.3 CDLAN SpA

- 7.3.4 Data4

- 7.3.5 Equinix, Inc.

- 7.3.6 Irideos SpA

- 7.3.7 IT.Gate S.p.A.

- 7.3.8 ITnet S.r.l

- 7.3.9 MIX SRL

- 7.3.10 Seeweb Srl

- 7.3.11 Stack Infrastructure, Inc.

- 7.3.12 Vantage Data Centers LLC

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms

2025年全球資料中心資訊技術(IT)設備市場報告2025年全球資料中心遷移市場報告2025年全球配置自動化市場報告

2025年全球資料中心資訊技術(IT)設備市場報告2025年全球資料中心遷移市場報告2025年全球配置自動化市場報告 全球配電中心市場:依類型、應用和地區劃分 - 市場規模、行業趨勢、機會分析和預測(2025-2033 年)

全球配電中心市場:依類型、應用和地區劃分 - 市場規模、行業趨勢、機會分析和預測(2025-2033 年) 資料中心 IT 資產處置市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,以及 2024 年至 2032 年的預測

資料中心 IT 資產處置市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察,以及 2024 年至 2032 年的預測 資料中心設備及基礎設施市場:2025-2030

資料中心設備及基礎設施市場:2025-2030 高階主管簡報:2025 年第四季資料中心遷移市場-2025-2030 年預測

高階主管簡報:2025 年第四季資料中心遷移市場-2025-2030 年預測 AI資料中心的設備投資的明細和未來預測

AI資料中心的設備投資的明細和未來預測 全球資料中心服務市場按服務類型、設施服務、IT 服務、專業諮詢與認證、層級類型、資料中心規模與容量、資料中心類型、企業資料中心和地區分類 - 預測至 2030 年

全球資料中心服務市場按服務類型、設施服務、IT 服務、專業諮詢與認證、層級類型、資料中心規模與容量、資料中心類型、企業資料中心和地區分類 - 預測至 2030 年