|

市場調查報告書

商品編碼

1693782

非洲生物農藥市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Africa Biopesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

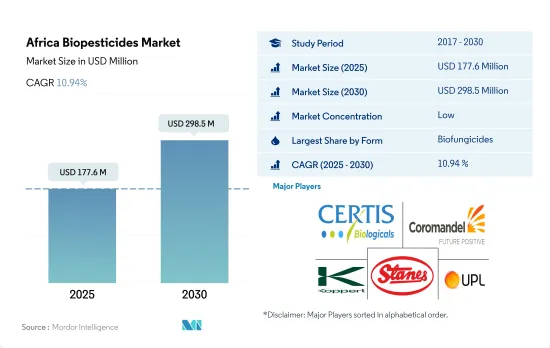

預計 2025 年非洲生物農藥市場規模為 1.776 億美元,到 2030 年將達到 2.985 億美元,預測期內(2025-2030 年)的複合年成長率為 10.94%。

- 生物農藥是從動物、植物、昆蟲或微生物(包括細菌和真菌)中提取的天然物質或藥劑,用於控制農業害蟲和感染疾病。 2017年至2022年,非洲生物農藥市場成長了23.4%。

- 該地區連作作物的生物農藥消費量高於其他作物,2022年佔總消費量的73.8%。園藝作物佔19.7%,經濟作物佔當年總消費量的6.5%。

- 綜合蟲害管理(IPM)概念是非洲生物農藥市場的關鍵。 IPM 1.0 於幾十年前建立,旨在減少農藥的過度使用。 IPM 2.0 逐漸融入了生物防治和棲地管理等生態學原理。然而在此期間,小農戶仍依賴危險的農藥作為第一道防線,而沒有提升他們的決策能力。綜合蟲害管理3.0(IPM3.0)也已在非洲地區實施。 IPM 3.0 包括三個新功能:農民可以進行即時決策;科學和自然的害蟲管理選擇;以及基因組方法、生物控制和棲息地管理實踐的整合。這些 IPM 實踐可能會推動非洲生物農藥市場的發展。

- 國際昆蟲生理學和生態學中心與 Real IPM 合作,將兩種生物防治劑宣傳活動(icipe69) 和 Achieve (icipe78) 商業化。宣傳活動(icipe69)用於防治黃瓜、芒果、木瓜、玫瑰和番茄等作物中的狨猴、薊馬和果蠅。 IPM 實踐的採用和生物農藥研發活動的增加可能會在 2023 年至 2029 年間使市場規模成長 84.7%。

- 2017 年至 2021 年間,非洲生物農藥市場成長率為 15.8%,預計到 2029 年將持續成長約 84.7%。

- 這項成長主要歸功於綜合蟲害管理 3.0(IPM 3.0)在非洲的推出。害蟲管理策略基於三大支柱:農民的即時決策、基於科學的害蟲管理方案以及遺傳技術、生物防治和棲息地管理策略的結合。這些 IPM 技術預計將在推動非洲生物農藥市場成長方面發揮關鍵作用。

- 生物殺菌劑是非洲以外生物農藥市場的領先細分市場,2022 年市場規模為 4,560 萬美元。木黴菌被廣泛用作生物殺菌劑,因為它能產生抗菌物質,透過酵素破壞其他真菌並殺死致病真菌。

- 埃及、南非和非洲其他地區是有機農業種植面積在非洲地區領先的地區。 2022 年,非洲其他地區有機農地面積達 120 萬公頃,佔非洲有機農地總面積的 95.0%。埃及佔3.5%或45,100公頃,南非佔1.0%或12,600公頃。這些國家擁有大面積的有機種植土地,提供了巨大的市場機會。

- 消費者對有機產品的興趣日益濃厚、農民意識不斷增強以及使用生物農藥的經濟效益預計將推動非洲對生物農藥的需求,預計該市場在 2023-2029 年期間的複合年成長率將達到 9.2%。

非洲生物農藥市場趨勢

該地區的有機產業擁有 834,000 個有機生產商,其中突尼斯擁有更多的有機土地。

- 2022年,非洲地區有機農地面積超過120萬公頃,佔全球有機農地面積的9.0%。

- 2020 年,非洲有機種植面積比 2019 年增加 149,000 公頃,與前一年同期比較增 7.7%,生產者約 834,000 家。突尼斯擁有最多的有機土地(2020 年超過 29 萬公頃),衣索比亞擁有最多的有機生產者(約 22 萬人)。島國聖多美和普林西比是該地區投入有機農業土地最多的國家,其農業面積的20.7%為有機作物。

- 在非洲,經濟作物在有機農地中所佔比例大,佔有機農地總面積的63.2%,達81.74萬公頃。田間作物佔非洲有機農地的第二大佔有率,約佔有機土地總面積的 25.6%,總合331,200 公頃。至2022年,園藝作物將佔非洲有機農地總面積的11.2%,達144,900公頃。

- 大面積種植有機作物的非洲國家包括非洲其他地區、埃及和南非。至2022年,非洲其他地區將佔非洲有機農業總面積的95.0%,達到120萬公頃,其次是埃及,佔4.51萬公頃,佔3.5%,南非佔1.26萬公頃,佔1.0%。

- 在非洲,2017年至2022年間,有機農業面積增加了6.9%。預計到2029年將成長約52.2%,達到200萬美元。

埃及、南非和奈及利亞是有機產品人均支出最高的國家

- 多年來,非洲的人均收入一直在持續成長,導致人們在營養食品上的支出增加。非洲各地的貨架上有機食品和飲料越來越常見。經過認證的有機農產品的國內消費量相對較低,因此大多數有機產品都用於出口。

- 在非洲,有機產品的消費量顯著增加,尤其是在埃及、南非和奈及利亞。 2021年,埃及的人均有機產品消費量為55.5美元,其次是南非,為7.1美元。有機生產者數量最多的國家是衣索比亞(近 222,000 家)、坦尚尼亞(近 149,000 家)和烏干達(超過 139,000 家)。

- 非洲地區普遍消費的有機產品包括新鮮蔬菜和水果。在非洲,人們做出了巨大努力,將有機農業納入政策、國家推廣體系、行銷和價值鏈發展的主流。所有這些因素都引起了消費者的興趣。

- 由於人均飲料消費量(尤其是果汁)的增加、健康意識的增強以及消費者轉向無化學成分的有機飲料和食品,預計 2023 年至 2029 年間非洲對有機食品的需求將會擴大。

- 然而,大量的低收入人口以及缺乏有機標準和其他當地市場認證基礎設施是該地區有機市場成長的主要限制因素。

非洲生物農藥產業概況

非洲生物農藥市場細分化,前五大公司佔14.93%。市場的主要企業包括 Certis USA LLC、Coromandel International Ltd、Koppert Biological Systems Inc.、T. Stanes, Company Limited、UPL 等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 有機種植區

- 有機產品人均支出

- 法律規範

- 埃及

- 伊朗

- 奈及利亞

- 南非

- 價值鍊和通路分析

第5章市場區隔

- 形式

- 生物真菌劑

- 生物除草劑

- 生物殺蟲劑

- 其他生物防治劑

- 作物類型

- 經濟作物

- 園藝作物

- 耕地作物

- 原產地

- 埃及

- 奈及利亞

- 南非

- 其他非洲國家

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Andermatt Group AG

- Atlantica Agricola

- Biolchim SPA

- Certis USA LLC

- Coromandel International Ltd

- IPL Biologicals Limited

- Koppert Biological Systems Inc.

- T. Stanes and Company Limited

- UPL

- Valent Biosciences LLC

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 500042

The Africa Biopesticides Market size is estimated at 177.6 million USD in 2025, and is expected to reach 298.5 million USD by 2030, growing at a CAGR of 10.94% during the forecast period (2025-2030).

- Biopesticides are naturally occurring substances or agents derived from animals, plants, insects, and microorganisms, including bacteria and fungi, used to manage agricultural pests and infections. The African biopesticides market grew by 23.4% from 2017 to 2022.

- Biopesticide consumption in row crops is higher than other crops in the region, accounting for 73.8% in 2022. Horticultural crops accounted for 19.7%, while cash crops accounted for 6.5% of the overall consumption in the same year.

- The Integrated Pest Management (IPM) concept is important in the African biopesticides market. IPM 1.0 was established decades ago to reduce the overuse of agricultural pesticides. IPM 2.0 gradually incorporated agroecological principles such as biological control and habitat management. However, throughout this period, smallholder farmers did not improve their decision-making skills and continued to rely on hazardous pesticides as their first line of defense. The African region also implemented Integrated Pest Management 3.0 (IPM 3.0), which includes three new features, i.e., real-time farmer decision-making access, pest-management options based on science and nature, and the integration of genomic approaches, biopesticides, and habitat-management practices. These IPM practices may drive the biopesticides market in Africa.

- In collaboration with Real IPM Ltd, the International Centre of Insect Physiology and Ecology commercialized two biopesticides, Campaign (icipe69) and Achieve (icipe78). Campaign (icipe69) is being used against mealybugs, thrips, and fruit flies, in crops such as cucumber, mango, papaya, rose, and tomato. Adoption of IPM practices and increased R&D activities of biopesticides may boost the market value by 84.7% between 2023 and 2029.

- The African biopesticides market has exhibited a growth rate of 15.8% between 2017 and 2021, and this growth is expected to continue with a projected expansion of about 84.7% by 2029.

- This growth is primarily attributed to the launch of Integrated Pest Management 3.0 (IPM 3.0) in Africa. This pest management strategy is based on three pillars: real-time farmer decision-making access, science-based pest-management alternatives, and the combination of genetic methods, biopesticides, and habitat-management strategies. These IPM methods are expected to play a critical role in driving the growth of the African biopesticides market.

- Biofungicides are the dominant segment of the biopesticides market in the Rest of Africa segment, and it was valued at USD 45.6 million in 2022. Trichoderma is widely used as a biofungicide as it destroys other fungi enzymatically and produces anti-microbial substances that kill pathogenic fungi.

- Egypt, South Africa, and the Rest of Africa are the primary segments in the African region regarding organic agriculture acreage. In 2022, the Rest of Africa accounted for 95.0% of total organic agricultural land in Africa, with 1.2 million hectares. Egypt contributed 3.5% with 45.1 thousand hectares, while South Africa accounted for 1.0% with 12.6 thousand hectares. The high organic agricultural acreage in these countries provides significant market opportunities.

- The increasing consumer interest in organic products, growing awareness among farmers, and the economic advantages of using biopesticides are anticipated to drive the demand for biopesticides in Africa, and the market is expected to record a CAGR of 9.2% between 2023 and 2029.

Africa Biopesticides Market Trends

8,34,000 organic producers are in the region's organic sector with Tunisia is having more organic land

- In 2022, the area of organic agricultural land in the African region amounted to over 1.2 million hectares, representing 9.0% of the global organic agricultural area.

- In 2020, Africa reported 149,000 hectares more in organic cultivation land than in 2019, recording a 7.7% increase Y-o-Y in line with the presence of nearly 834,000 producers. Tunisia had the largest amount of organic land (more than 290,000 hectares in 2020), whereas Ethiopia had the highest number of organic producers (almost 220,000). The island states of Sao Tome and Principe have the most significant amount of land committed to organic farming in the region, with 20.7% of their agricultural area dedicated to organic crops.

- In the African region, cash crops account for a significant share of organic agricultural land, amounting to 63.2% of the total organic acreage with 817.4 thousand hectares. Row crops hold the second-largest share of organic acreage in Africa, which amounts to about 25.6% of the total organic acreage, totaling 331.2 thousand hectares. Horticultural crops account for 11.2% of the total organic acreage in Africa, with 144.9 thousand hectares in 2022.

- The African countries with significant organic agricultural acreage include the Rest of Africa regional segment, Egypt, and South Africa. In 2022, the Rest of Africa accounted for 95.0% of the total organic agricultural acreage in Africa, with 1.2 million hectares, Egypt accounted for a 3.5% share with 45.1 thousand hectares, and South Africa accounted for a 1.0% share with 12.6 thousand hectares.

- Organic agricultural acreage rose by 6.9% between 2017 and 2022 in Africa. It is anticipated to increase by about 52.2% and reach USD 2.0 million by 2029.

Per capita spending on organic product predominant in Egypt, South Africa, and Nigeria countries

- Africa's per capita income has consistently increased throughout the years, encouraging people to spend more money on nutritious food. Organic foods and beverages are gaining more shelf space in the African region. Since the domestic consumption of certified organic produce is relatively small, most organic goods are produced for export.

- In Africa, consumption of organic products has increased significantly, especially in Egypt, South Africa, and Nigeria. In 2021, the per capita consumption of organic products was USD 55.5 in Egypt, followed by South Africa with USD 7.1. The countries with the highest number of organic producers were Ethiopia (almost 222,000), Tanzania (nearly 149,000), and Uganda (over 139,000).

- In the African region, commonly consumed organic products include fresh vegetables and fruits. In Africa, significant efforts have been made to mainstream organic agriculture into policy, national extension systems, marketing, and value chain development. All these factors have gained the attention of consumers.

- With the increasing per capita consumption of beverages, primarily fruit juices, growing health awareness, and consumers shifting toward organic drinks and food that do not contain chemical ingredients, the demand for the African organic food market is expected to grow between 2023 and 2029.

- However, low-income levels and a lack of organic standards and other infrastructure for local market certification are the major restraining factors for the growth of the organic market in the region.

Africa Biopesticides Industry Overview

The Africa Biopesticides Market is fragmented, with the top five companies occupying 14.93%. The major players in this market are Certis USA LLC, Coromandel International Ltd, Koppert Biological Systems Inc., T. Stanes and Company Limited and UPL (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Egypt

- 4.3.2 Iran

- 4.3.3 Nigeria

- 4.3.4 South Africa

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Biofungicides

- 5.1.2 Bioherbicides

- 5.1.3 Bioinsecticides

- 5.1.4 Other Biopesticides

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Egypt

- 5.3.2 Nigeria

- 5.3.3 South Africa

- 5.3.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Andermatt Group AG

- 6.4.2 Atlantica Agricola

- 6.4.3 Biolchim SPA

- 6.4.4 Certis USA LLC

- 6.4.5 Coromandel International Ltd

- 6.4.6 IPL Biologicals Limited

- 6.4.7 Koppert Biological Systems Inc.

- 6.4.8 T. Stanes and Company Limited

- 6.4.9 UPL

- 6.4.10 Valent Biosciences LLC

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

生物農藥市場:按類型、作物、配方、應用和銷售管道分類-2026-2032年全球市場預測

生物農藥市場:按類型、作物、配方、應用和銷售管道分類-2026-2032年全球市場預測 全球生物農藥市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球生物農藥市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球生物農藥市場報告

2026年全球生物農藥市場報告 生物製藥市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、作物類型、應用、製劑、地區和競爭格局分類,2021-2031年

生物製藥市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、作物類型、應用、製劑、地區和競爭格局分類,2021-2031年 生物農藥市場規模、佔有率和趨勢分析報告:按產品、作物類型、來源、應用、地區和細分市場分類 - 預測,2026-2033年芽孢桿菌作物保護市場按作物類型、配方類型、應用方法、最終用戶和銷售管道分類-2026-2032年全球預測農業生物農藥市場按類型、作用方式、應用、作物類型和劑型分類-2026-2032年全球預測

生物農藥市場規模、佔有率和趨勢分析報告:按產品、作物類型、來源、應用、地區和細分市場分類 - 預測,2026-2033年芽孢桿菌作物保護市場按作物類型、配方類型、應用方法、最終用戶和銷售管道分類-2026-2032年全球預測農業生物農藥市場按類型、作用方式、應用、作物類型和劑型分類-2026-2032年全球預測 生物農藥:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

生物農藥:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 日本生物農藥市場報告(按產品類型(生物除草劑、生物殺蟲劑、生物殺菌劑及其他)、應用(作物用、非作物用)和地區分類,2026-2034)

日本生物農藥市場報告(按產品類型(生物除草劑、生物殺蟲劑、生物殺菌劑及其他)、應用(作物用、非作物用)和地區分類,2026-2034) 全球生物肥料和生物農藥市場:預測至2032年-按產品類型、形態、應用方法、作物類型和地區分類的分析

全球生物肥料和生物農藥市場:預測至2032年-按產品類型、形態、應用方法、作物類型和地區分類的分析

▼