|

市場調查報告書

商品編碼

1693752

北美生物防治劑:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)North America Biocontrol Agents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

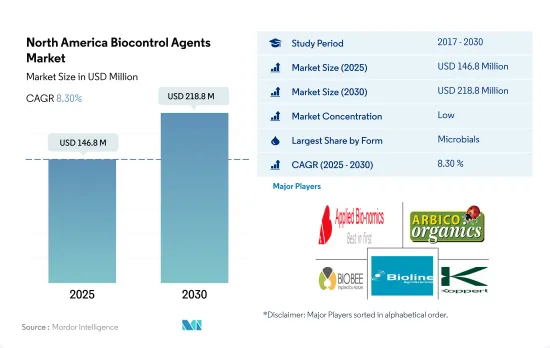

北美生物防治劑市場規模預計在 2025 年為 1.468 億美元,預計到 2030 年將達到 2.188 億美元,預測期內(2025-2030 年)的複合年成長率為 8.30%。

- 生物防治是一種害蟲管理策略,包括利用天敵或生物防治劑減少害蟲數量。捕食者、寄生蟲、細菌生物防治劑、真菌生物防治劑和昆蟲病原線蟲是作物保護中使用的主要生物防治劑。

- 2022 年北美生物防治劑市場以微生物領域為主。在 2022 年北美生物防治劑市場中,真菌生物防治劑子子區隔佔據主導地位,以金額為準微生物領域的 59.7% 的佔有率。真菌子子區隔在生物防治劑市場中的主導地位主要是因為真菌生物防治劑的作用方式複雜,不會損害環境,且在大多數情況下不會導致昆蟲、害蟲和病原體產生抗藥性。

- 由於微生物在種子處理、田間處理和收穫後應用等各種應用中的使用日益增多,微生物領域預計將以更快的速度成長。

- 宏觀營養學部分價值 5,450 萬美元,佔 2022 年北美生物防治劑市場的 45.8%。捕食者在大型生物領域佔據主導地位,以金額為準,2022 年的佔有率為 97.8%。捕食者子子區隔在北美生物防治劑市場的主導地位主要歸功於其能夠攻擊不同生命階段的害蟲,甚至不同種類的害蟲。它們也比其他生物防治劑更貪婪。

- 由於大量研究致力於提高功效並實現商用作物與環境更安全的相互作用,北美生物防治劑市場預計將在 2023 年至 2029 年間成長。

- 北美生物防治劑市場以美國為主,2022年佔市場價值的29.0%。這項優勢主要得益於該國豐富的可耕地。在美國,微生物生物防治劑最為普遍,佔以金額為準佔有率的 89.1%,其中真菌生物防治劑佔據美國市場的主導地位。

- 加拿大佔據北美生物防治劑市場第二大佔有率,2022 年以金額為準計算的佔有率為 19.1%。加拿大對生物防治劑的需求受到有機農業、農藥法規的變化以及低風險害蟲防治產品的普及的推動。農藥的高成本也導致生物防治產品的使用增加。

- 墨西哥將佔據北美生物防治劑市場的最大佔有率,到 2022 年將佔以金額為準的 50.0% 和數量 27.7%。該國已在聯邦和州政府層級正式確立了生物防治職能,國家生物防治參考中心則作為國際參考中心。

- 北美生物防治劑市場主要由美國主導,其中微生物生物防治劑是最受歡迎的類型。加拿大和墨西哥也是北美市場的重要參與企業,擁有自己的需求促進因素和政府措施。儘管市場具有成長潛力,但產品保存期限和農民缺乏意識等挑戰可能會阻礙其發展。

北美生物防治劑市場趨勢

美國等主要國家對有機農產品的需求正在成長,政府的支持也有助於增加有機農產品的種植面積。

- 根據FibL統計的數據,2021年北美有機種植農作物面積達到創紀錄的150萬公頃。該地區有機種植面積在過去一段時間(2017-2022年)增加了13.5%。在北美國家中,美國佔據主導地位,有62.3萬公頃農地實行有機農業,其中加州、緬因州和紐約州是實行有機農業的主要州。

- 緊隨美國之後的是墨西哥,2021年有機農業面積達531,100公頃。墨西哥是全球前20大有機食品生產國之一。根據世界咖啡大師的數據,墨西哥是世界上最大的有機咖啡出口國。這裡是全國有機咖啡生產面積最大的地區,也是全國有機咖啡種植者最多的地區。

- 該國主要的有機食品生產州包括恰帕斯州、瓦哈卡州、米卻肯州、奇瓦瓦州和格雷羅州,佔2021年全國有機種植面積的80.0%。全國有機農業協會等組織正在該國推廣有機農業,預計將激勵更多農民從事有機農業。除了資金支持,墨西哥政府也支持有助於推廣有機農業的研發活動。

- 加拿大作物作物面積從2017年的40萬公頃增加到2021年的40萬公頃,其中2021年將達40萬公頃,佔比最大。加拿大政府宣布,將於2021年向有機發展基金提供297,330美元,用於支持有機農民。這些努力有望增加該地區有機種植的面積。

國內外市場對有機農產品的需求不斷成長,人均有機食品支出不斷增加

- 2021年北美人均有機食品支出為109.7美元。美國的人均支出是北美國家中最高的,2021年平均支出為186.7美元。 2021年美國有機產品銷售額超過630億美元。有機塔爾德協會的數據顯示,2021與前一年同期比較成長2.0%,達575億美元。有機水果和蔬菜佔有機產品總銷售額的15.0%,2021年價值210億美元。

- 根據加拿大有機聯盟報告的數據,2020 年加拿大有機食品銷售額達到 81 億美元。加拿大是全球第六大有機產品市場,據報道,其有機產品供應未能滿足國內需求。 2021年有機食品人均支出為142.6美元。政府加強對零售商的支持力度預計將提高該國有機產品的供應量、可近性和可負擔性。有機塔爾德協會估計,加拿大有機產品市場將在 2021 年至 2026 年間成長,複合年成長率為 6.3%。

- 2021年,墨西哥有機產品市場規模為6,300萬美元,全球排名第35。預計墨西哥在 2021 年至 2026 年期間的複合年成長率為 7.2%。然而,該國 2021 年的人均有機產品支出為 0.49 美元,與該地區的其他國家相比較低。隨著越來越多的參與企業進入墨西哥市場,預計該國對有機產品的需求將會增加。

北美生物防治劑產業概況

北美生物防治劑市場細分,前五大公司佔15.38%。市場的主要企業有 Applied Bio-nomics Ltd、Arizona Biological Control Inc.、Biobee Ltd、Bioline AgroSciences Ltd、Koppert Biological Systems Inc. 等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 有機種植區

- 有機產品人均支出

- 法律規範

- 加拿大

- 墨西哥

- 美國

- 價值鍊和通路分析

第5章市場區隔

- 形式

- 大型生物

- 按生物體

- 昆蟲病原線蟲

- 寄生蟲

- 鐵血戰士

- 微生物

- 按生物體

- 細菌生物防治劑

- 真菌生物防治劑

- 其他微生物

- 大型生物

- 作物類型

- 經濟作物

- 園藝作物

- 耕地作物

- 原產地

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Anatis Bio Protection

- Andermatt Group AG

- Applied Bio-nomics Ltd

- Arizona Biological Control Inc.

- Beneficial Insectary Inc.

- Biobee Ltd

- Bioline AgroSciences Ltd

- Bioworks Inc.

- Crop Defenders Ltd

- Koppert Biological Systems Inc.

第7章 CEO 的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 數據包

- 詞彙表

The North America Biocontrol Agents Market size is estimated at 146.8 million USD in 2025, and is expected to reach 218.8 million USD by 2030, growing at a CAGR of 8.30% during the forecast period (2025-2030).

- Biological control is a pest management strategy based on the reduction of pest populations by natural enemies or biological control agents. Predators, parasites, bacterial biocontrol agents, fungal biocontrol agents, and entomopathogenic nematodes are the primary biocontrol agents used in crop protection.

- The microbial segment dominated the North American biocontrol agents market in 2022. The fungal biocontrol agents sub-segment dominated and accounted for a 59.7% share of the microbial segment of the North American biocontrol agents market by value in 2022. The dominance of the fungal sub-segment in the biocontrol agents market is mainly because fungal biocontrol agents do not harm the environment with their intricate mode of action and, in most cases, do not lead to the development of resistance in insects, pests, and pathogens.

- The microbial segment is projected to grow at a faster rate due to the increasing use of microbials in various applications, such as seed treatment, on-field, and post-harvest applications.

- The macrobials segment was valued at USD 54.5 million and accounted for 45.8% of the North American biocontrol agents market in 2022. Predators dominated the macrobials segment and accounted for a 97.8% share of the segment by value in 2022. The dominance of the predators' sub-segment in the North American biocontrol agents market is mainly due to their ability to attack different life stages of pests and even different pest species. They are also voracious feeders compared to other biocontrol agents.

- The North American biocontrol agents market is expected to grow between 2023 and 2029 due to numerous research efforts to improve efficacy and make interactions safer for commercial crops and the environment.

- The North American biocontrol agents market is dominated by the United States, which accounted for 29.0% of the market value in 2022. This dominance is mainly due to the abundance of arable land in the country. Within the United States, microbials are the most popular type of biocontrol agent, accounting for an 89.1% share by value, with fungal biocontrol agents dominating the US market.

- Canada held the second-largest share of the North American biocontrol agents market, accounting for a 19.1% share by value in 2022. The demand for biological control products in Canada is driven by organic agriculture, changes to pesticide laws, and the promotion of lower-risk pest control products. The high cost of pesticides also led to an increase in the usage of biological control products.

- Mexico accounts for the largest share of the North American biocontrol agents market, with a 50.0% share by value and 27.7% by volume in 2022. The country has formalized the role of biological control at the federal and state government levels, and the National Reference Center for Biological Control serves as an international reference center.

- The North American biocontrol agents market is primarily dominated by the United States, with microbial biocontrol agents being the most popular type segment. Canada and Mexico are also significant players in the North American market, with their respective demand drivers and government initiatives. Despite the market's potential for growth, challenges such as the product's shelf life and lack of awareness among farmers may impede progress.

North America Biocontrol Agents Market Trends

Organic produce demand grows in major countries like the United States, increasing cultivation area with government support

- The area under organic cultivation of crops in North America was recorded at 1.5 million hectares in 2021, according to the data provided by FibL statistics. The organic area in the region increased by 13.5% during the historical period (2017-2022). Among the North American countries, the United States was dominant, with 623.0 thousand hectares of agricultural land under organic farming, with California, Maine, and New York being the major states practicing agriculture.

- The United States is followed by Mexico, with 531.1 thousand hectares of area under organic farming in 2021. Mexico is among the top 20 organic food producers in the world. Mexico is the largest exporter of organic coffee in the world, according to Global Coffee Masters data. The country has the largest area under organic coffee production and even in terms of the number of organic coffee producers in the country.

- The major organic food-producing states in the country include Chiapas, Oaxaca, Michoacan, Chihuahua, and Guerrero, which accounted for 80.0% of the total organic area in the country in 2021. Organizations such as National Association for Organic Agriculture promote organic agriculture in the country, which is expected to motivate more farmers to take up organic agriculture. In addition to financial assistance, the Mexican government supports research and development activities to help promote organic agriculture.

- Canada's area under organic crop cultivation increased from 0.4 million hectares in 2017 to 0.4 million hectares in 2021. Row crops occupied the maximum area with 0.4 million hectares in 2021. The Canadian government announced a sum of USD 297,330 in 2021 as Organic Development Fund to support organic farmers. These initiatives are expected to increase the organic area in the region.

Growing demand for organic produce in domestic and international markets, rise in per capita spending on organic food

- North America's average per capita spending on organic food products was USD 109.7 in 2021. The per capita spending in the United States is the highest among the North American countries, with average spending of USD 186.7 in 2021. The sales of organic products in the United States crossed USD 63.00 billion in 2021. Organic Tarde Association accounted for a 2.0% increase over the previous year, with organic food sales at USD 57.5 billion in 2021. Organic fruits and vegetables accounted for 15.0% of the total organic product sales, valued at USD 21.0 billion in 2021.

- Organic food sales in Canada reached a value of USD 8.10 billion in 2020, as per the data reported by the Organic Federation of Canada. It is reported that Canada is the 6th largest market in the world for Organic products, with the supply of organic products failing to keep up with the demand in the country. The average spending on organic food per person was USD 142.6 in 2021. Increasing government support to retailers is expected to increase the availability, accessibility, and affordability of organic products in the country. Organic Tarde Association estimated the organic products market in Canada to grow and register a CAGR of 6.3% between 2021 and 2026.

- In 2021, Mexico registered a market size of USD 63.0 million for organic products with a global rank of 35. It is estimated to grow and register a CAGR of 7.2% between 2021 and 2026. However, the per capita spending on organic products in the country is less than in other countries in the region, with a value of USD 0.49 in 2021. More players entering the market in Mexico are expected to increase the demand for organic products in the country.

North America Biocontrol Agents Industry Overview

The North America Biocontrol Agents Market is fragmented, with the top five companies occupying 15.38%. The major players in this market are Applied Bio-nomics Ltd, Arizona Biological Control Inc., Biobee Ltd, Bioline AgroSciences Ltd and Koppert Biological Systems Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Macrobials

- 5.1.1.1 By Organism

- 5.1.1.1.1 Entamopathogenic Nematodes

- 5.1.1.1.2 Parasitoids

- 5.1.1.1.3 Predators

- 5.1.2 Microbials

- 5.1.2.1 By Organism

- 5.1.2.1.1 Bacterial Biocontrol Agents

- 5.1.2.1.2 Fungal Biocontrol Agents

- 5.1.2.1.3 Other Microbials

- 5.1.1 Macrobials

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Anatis Bio Protection

- 6.4.2 Andermatt Group AG

- 6.4.3 Applied Bio-nomics Ltd

- 6.4.4 Arizona Biological Control Inc.

- 6.4.5 Beneficial Insectary Inc.

- 6.4.6 Biobee Ltd

- 6.4.7 Bioline AgroSciences Ltd

- 6.4.8 Bioworks Inc.

- 6.4.9 Crop Defenders Ltd

- 6.4.10 Koppert Biological Systems Inc.

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

生物防治劑市場-2026-2031年預測

生物防治劑市場-2026-2031年預測 全球生物防治劑市場

全球生物防治劑市場 生物防治劑市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

生物防治劑市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 生物防治劑市場按類型、施用方法、劑型、作物類型、施用方式及地區分類

生物防治劑市場按類型、施用方法、劑型、作物類型、施用方式及地區分類 中國生物防治劑市場:佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太地區生物防治劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度生物防治劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)歐洲生物防治劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)美國生物防治劑:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)

中國生物防治劑市場:佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太地區生物防治劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度生物防治劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)歐洲生物防治劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)美國生物防治劑:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年) 生物防治劑市場:2033年市場分析與預測 - 依類型、產品、應用、技術、最終用戶、形式、組件、模式、階段和服務

生物防治劑市場:2033年市場分析與預測 - 依類型、產品、應用、技術、最終用戶、形式、組件、模式、階段和服務