|

市場調查報告書

商品編碼

1693726

美國和歐洲光纖電纜-市場佔有率分析、行業趨勢和成長預測(2025-2030年)United States And European Fiber Optic Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

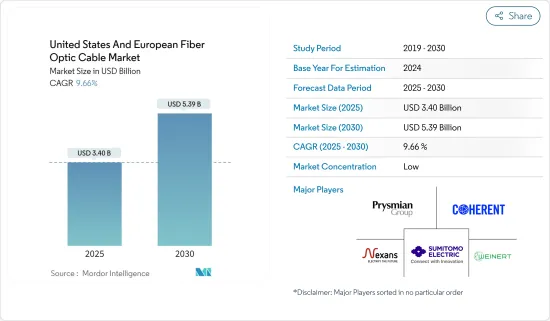

預計 2025 年美國和歐洲光纖電纜市場規模為 34 億美元,到 2030 年將達到 53.9 億美元,預測期內(2025-2030 年)的複合年成長率為 9.66%。

關鍵亮點

- 5G網路和光纖基礎設施的演進正在推動各行各業的數位轉型。光纖電纜比銅纜具有更高的安全性、可靠性、頻寬和安全性。光纖電纜與銅線的區別在於,光纖電纜利用光脈衝透過光纖線傳輸訊息,而不是利用電子脈衝透過銅線傳輸訊息。

- 隨著線上交易和虛擬會議的興起,企業需要 5G 和光纖電纜來保持競爭力。例如,根據歐洲央行的數據,付款非經常性消費者付款的佔有率將從 2019 年的 6% 增加到 2022 年的 17%。因此,為了支持這種趨勢,需要高速網路等強大的基礎設施,這有望為所研究的市場創造機會。

- 此外,光纖電纜是眾多工業應用的經濟高效、方便且簡單的解決方案,包括照明和裝飾、數據傳輸、手術和機器檢查。在家工作和混合工作模式的興起也推動了美國和歐洲對 FTTH 的需求。

- 資料流量的成長,尤其是網際網路通訊協定(IP),正倍增對高網路頻寬的需求。領先的服務供應商每六到九個月就會將主幹頻寬頻寬加倍。由於網路流量的成長,頻寬每 6 到 9 個月就會加倍。

- 美國和歐洲市場綜合光纖基礎設施的擴張也推動了對光纖電纜的巨大需求,尤其是在電訊業。光纖網路和光纖線路也顯著改善了寬頻設施。這些架構包括 FTTH、FTTP、FTTC 和 FTTB。

- 開發中國家光纖生產商日益成長的連接需求帶來了巨大的商業前景。然而,無線解決方案需求不斷增加以及鋪設光纖電纜的困難等因素對市場的成長構成了若干營運挑戰。

- 此外,由於美國和歐洲都正在經歷新冠疫情後的景氣衰退,宏觀經濟因素也將對研究市場的成長產生重大影響。此外,俄羅斯與烏克蘭的戰爭以及美國與中國的衝突等地緣政治問題也為市場持續成長帶來了挑戰。

美國和歐洲光纖電纜市場趨勢

光纖和 5G 部署的投資增加將推動市場

- 美國和歐洲市場是最早採用先進通訊技術的市場之一,至今仍是如此。發達的生態系統和數位技術在消費者中的高滲透率等因素正在推動產業相關人員增加對光纖和通訊基礎設施的投資。例如,通訊服務供應商康寧最近透露了在 2023 年設計亞利桑那州首個光纖網路的計畫。

- 例如,康普是光纖技術創新領域的領導者,不斷突破最具挑戰性的網路高效能光纖連接的界限。該公司還制定了行業標準,因此其光纖佈線系統始終超出要求。

- 美國和歐洲市場對 5G 的日益普及也推動了所研究市場的成長。例如,愛立信最近宣佈到2025年將在德國推出3.5GHz(5G)。至2025年,3.5GHz頻段的5G網路將佔德國網路總量的43%,高於2023年預期的42%。然而,預計到2025年,只有7%的德國地理區域將被覆蓋。

- 同樣,美國國家科學基金會(NSF)也致力於加速5G解決方案,以確保美國關鍵基礎設施和政府營運商能夠隨時隨地安全通訊。例如,2022年9月,NSF宣布與國防部建立合作關係。美國國家科學基金會投資 1,200 萬美元,為其 2022 年融合加速器計畫挑選了 16 個團隊。這些團隊被選為「G 軌道:透過 5G 基礎設施安全運作」團隊。 G軌道將加速技術進步,為美國聯邦政府和軍隊開發5G通訊。

- Adtran 是一家美國網路和通訊解決方案供應商,利用無源光纖網路技術創建全光纖網路,為企業和家庭提供Gigabit和基礎設施回程傳輸。 2023年1月,該公司宣布推出SDX 6330 10Gbit/s組合無源光纖網路光纖接取平台。該平台使服務供應商能夠以經濟高效的方式快速地將企業和家庭與光纖寬頻連接起來。這項新解決方案提供了業界最高的連接埠密度,並率先推出了具有 400 Gbit/s 上行鏈路的光線路終端。

- 此外,數據消費的成長也透過鼓勵對新的光纖電纜網路的投資來支持數據連接,為研究市場創造了機會。例如,2022年11月,瑞典連線供應商Arelion宣布計畫在墨西哥和美國之間透過德克薩斯建立兩條高容量光纖路線。新的密集分波多工路由將滿足對高容量、可擴展頻寬傳輸日益成長的需求,並簡化來自美國、亞洲和歐洲的Over-The-Top供應商進入墨西哥國內市場的途徑。

通訊終端用戶產業佔較大市場佔有率

- 光纖電纜(OFC)是通訊基礎設施的重要組成部分。在過去的十年中,光纖已經成為首選的傳輸介質,特別是因為它滿足了電信業者對頻寬的巨大需求。研究區域是 AT&T、Verizon、Sprint 和沃達豐集團等主要電信業者的所在地,這些公司正在不斷擴展其光纖網路以增強其全球和區域影響力。

- 來自網際網路、電子商務、電腦網路和多媒體(語音、數據和視訊)等各種來源的數據流量的快速成長表明,需要能夠管理更高頻寬的傳輸媒體來處理這些海量資訊。根據歐盟統計局的數據,歐盟每日網路使用者比例將從 2028 年的 74.07% 成長至 2022 年的 84%。光纖電纜以其相對無限的頻寬,是解決此問題的重要解決方案之一,因此在可預見的未來,其需求預計仍將保持高位。

- 在通訊網路中,光纖電纜連接不同的網路節點,例如手機訊號塔、資料中心和網路服務供應商,從而允許大量資料在不同位置之間傳輸。光纖電纜也非常適合高速網路連線和視訊會議、線上遊戲和雲端運算等先進通訊技術的發展。因此,預計美國和歐洲 5G 網路的擴張將推動所研究的市場機會。

- 此外,選擇光纖電纜還因為其安全性、可擴展性和無限頻寬潛力,可以處理產生的大量回程傳輸流量,以支援5G、巨量資料和物聯網等不斷發展的技術所需的頻寬水平,這些技術嚴重依賴即時數據收集和傳輸。 5G的推出可望提高網路容量並減少延遲。

- 網際網路是研究區域內突出的變革性和快速發展的技術之一,隨著光纖電纜廣泛應用於數據和通訊行業,它正在推動市場機會。例如,愛立信表示,其覆蓋地區的每部智慧型手機數據流量持續增加,預計北美每部智慧型手機的數據流量將從 2021 年的每月 13GB 成長到 2028 年的每月 58GB。同樣,西歐預計將從 2021 年的每月 16GB 成長到 2028 年的每月 56GB。

美國和歐洲光纖光纜產業概況

美國和歐洲光纖電纜市場主要由耐克森公司、普睿司曼集團、威納特工業股份公司、相干公司和住友公司等主要參與者組成。該市場中的參與企業正在採用夥伴關係、收購和合併等策略來加強其產品供應並獲得永續的競爭優勢。

- 2023 年 3 月 - 全球網路連接解決方案公司康普宣布擴大光纖電纜生產,以加速美國寬頻部署並連接更多社區和服務不足的地區。該公司表示,此舉將增加美國的光纖電纜產量,並加速向服務不足的地區推出寬頻。此外,該公司的 HeliARC 線路預計每年將支援 50 萬個家庭的 FTTH 部署。

- 2023 年 3 月—歐盟宣布,根據其 2030 年數位十年政策計劃,有義務在建築物中安裝光纖電纜。根據新規定,新契約的建築物和正在進行大規模維修的建築物必須配備無源基礎設施(微型管道)和室內光纖電纜(光纜),一直到公寓/單元內的網路終端點。歐盟還計劃為「光纖就緒」建築提供認證。預計這些趨勢將推動對光纖電纜的需求。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 關鍵宏觀經濟主題的影響

第5章市場動態

- 市場促進因素

- 數據流量的增加帶來了對光纖電纜網路的需求

- 增加對光纖和5G部署的投資

- 市場問題

- 對無線解決方案和複雜安裝流程的需求不斷增加

第6章市場區隔

- 按最終用戶產業

- 通訊

- 電力公共產業

- 國防/軍事

- 產業

- 醫療保健

- 其他

- 按國家

- 美國

- 德國

- 奧地利、瑞士

第7章競爭格局

- 公司簡介

- Nexans SA

- Prysmian Group

- Weinert Industries AG

- Coherent Corporation

- Sumitomo Corporation

- Corning Inc.

- Finisar Corporation

- Leoni AG

- Folan

- Molex LLC

- Fujikura Ltd

- Sterlite Technologies

- Furukawa Electric Co. Ltd

- Smiths Interconnect(Smiths Group PLC)

第8章:光纖在工業上的現狀

第9章:未來市場展望

The United States And European Fiber Optic Cable Market size is estimated at USD 3.40 billion in 2025, and is expected to reach USD 5.39 billion by 2030, at a CAGR of 9.66% during the forecast period (2025-2030).

Key Highlights

- The evolution of fifth-generation networks & fiber optic infrastructure has driven digital transformation across industries. Optic fiber cable presents better security, reliability, bandwidth, and security than copper cables. The distinction between a fiber optic cable and a copper wire is that the fiber optic cable utilizes light pulses to transfer information down the fiber lines rather than electronic pulses to transmit information through the copper lines.

- With increasing online transactions & virtual meetings, companies need 5G and optic fiber cable to remain competitive. For instance, according to the European Central Bank, online payments share in consumers' non-recurring payments increased to 17% in 2022 from just 6% in 2019. Hence, to support such trends robust infrastructure such as high-speed internet is required which is anticipated to create opportunities in the studied market.

- Furthermore, fiber optic cables are cost-effective, convenient, & easy solutions for numerous industrial applications, like lighting and decorations, data transmission, surgeries, and mechanical inspections. The growing work-from-home & hybrid work model also drives the need for FTTH throughout the United States and Europe.

- Data traffic growth, specifically Internet Protocol (IP), drives the surge in need for high network bandwidth. Prominent service providers registered bandwidth doubling on their backbones every six to nine months. Due to growing internet traffic, bandwidth doubles every 6 to 9 months.

- The expansion of fiber-integrated infrastructure in the US and the European market has also immensely raised the need for fiber-optic cables, particularly in the telecom industry. Fiber-optic networks and fiberoptic wires have also greatly improved owing to broadband installations. These architectures include FTTH, FTTP, FTTC, & FTTB.

- The increase in the need for connectivity in developing nations for fiber-optic producers offers significant business prospects. Yet factors like the advancement in wireless solution demand & the difficulty of deploying fibreoptic cables provide several operational difficulties for the market's growth.

- Macroeconomic factors also influence the studied market's growth significantly as both the United States and the European regions have been witnessing economic downturns post-covid. Furthermore, geopolitical issues such as the Russia-Ukraine war, and the US-China disputes also creates a challenging environment for an uninterrupted growth of the market.

US & European Fiber Optic Cable Market Trends

Rising Investment in Fiber Optic and 5G Deployment Drives the Market

- The US and European markets have been among the early adopters of advanced telecom technologies and continue to remain so. Factors such as the presence of developed ecosystems and higher consumer penetration of digital technologies support encourage the industry stakeholders to increase investments in fiber optic and telecom infrastructure. For instance, Corning, the telecom service provider, recently disclosed plans to design Arizona's first fiber network in 2023, anticipated to serve over 100,000 residences.

- Additionally, the studied regions also have the presence of some of the biggest fiber optic cable companies who continue to expand their regional presence; for instance, CommScope is among the leaders in fibreoptic innovation and drives the boundaries of high-performance fiber connectivity for the most challenging networks. Since the company also sets industry standards, its fiber-optic cabling systems always transcend requirements.

- The growing deployment of 5G in the US and European markets also favors the studied market's growth. For instance, Ericsson, recently stated that the 3.5 GHz (5G) roll-out will be conducted in Germany by 2025. The 3.5 GHz 5G network would constitute 43% of the total German population by 2025, up from 42%, which is anticipated in 2023. However, only 7% of the geographical region in Germany is expected to be covered in 2025.

- Similarly, the US National Science Foundation (NSF) concentrates on accelerating 5G solutions to support US critical infrastructure and government operators to communicate securely anytime and anywhere. For instance, in September 2022, NSF announced a partnership with the Department of Defense Office. With an investment of USD 12 million, NSF selected 16 teams for the Convergence Accelerator program in 2022. These teams were chosen for "Track G: Securely Operating Through 5G Infrastructure". Track G promotes technology advancement to develop 5G communications for the US federal government & military.

- Adtran, the US-based networking & communications solutions provider, enables the building of full-fiber networks employing passive optical network technologies that provide gigabit access to businesses and homes and for infrastructure backhaul. In January 2023, the company established its SDX 6330 10 Gbit/s combo passive optical network fiber access platform, which allows service providers to cost-effectively and quickly connect businesses & homes with fiber-based broadband. The new solution provides the highest port density in the industry and is the foremost optical line terminal incorporated with 400 Gbit/s uplinks.

- Furthermore, the growing data consumption is also creating opportunities in the studied market by driving investment in new optical fiber cable networks which supports the data connectivity. For instance, in November 2022, Arelion, a Swedish connectivity provider, unveiled a plan to create two high-capacity fiber optic routes through Texas between Mexico & the United States. The new dense wavelength division multiplexing routes will meet the increasing demand for high-capacity, scalable bandwidth transport & simplify access to Mexico's local markets for over-the-top suppliers in the United States, Asia, and Europe.

Telecommunication End-user Industry Holds Significant Market Share

- Optical fiber cable (OFC) is a vital building block in the telecommunication infrastructure. Over the last decade, fiber optics have been catering to forceful bandwidth needs, especially from telecommunication companies, and have become the choice of transmission medium. The Studied regions have the presence of some of the biggest telecommunication companies, such as AT&T, Verizon, Sprint, Vodafone Group, etc., who are continuously expanding their optical fiber network to increase their global and regional presence, which creates opportunities in the studied market.

- The eruption of data traffic from different sources, like the internet, e-commerce, computer networks, and multimedia (voice, data, and video), has shown the requirement for a transmission medium capable of managing higher bandwidth to handle such vast amounts of information. According to Eurostat, the share of daily internet users in the European Union had increased to 84% in 2022, compared to 74.07% in 2028. As fiber-optic cables, with comparatively infinite bandwidth, are among the key solutions to this problem, the demand is anticipated to remain high.

- In telecommunication networks, fiber optic cables join different network nodes, like cell towers, data centers, and internet service providers, allowing the exchange of extensive amounts of data between different locations. Fiber-optic cables also have suitable for developing high-speed internet connections & other advanced communication technologies such as video conferencing, online gaming, and cloud computing. Hence, the expanding 5G network footprint in the United States and the European region is anticipated to drive opportunities in the studied market.

- Moreover, owing to their security, scalability, and the unlimited bandwidth potential to handle the vast amount of backhaul traffic being generated, fiber-optic cables are also being selected to support the bandwidth levels catering to evolved technologies like 5G, Big Data and IoT that rely heavily on real-time data gathering and transfer. The launch of 5G is predicted to improve the capacity and lower latency straight to networks.

- The internet has been one of the significantly transformative and fast-growing technologies in the studied regions which is driving opportunities in the studied market as optical fiber cables are widely used in the data and the telecommunication industry. For instance, according to Ericsson, datatraffic per smartphone continues to grow in the studied regions, for instance, in North America, data traffic per smartphone is anticipated to growth from 13 GB/month in 2021 to 58 GB/month in 2028. Similarly, in Western Europe, it is anticipated to grow from 16GB/month in 2021 to 56GB/month by 2028.

US & European Fiber Optic Cable Industry Overview

The United States and European fiber optic cable market is fragmented, with major players like Nexans SA, Prysmian Group, Weinert Industries AG, Coherent Corporation, and Sumitomo Corporation. Players in the market are embracing strategies like partnerships, acquisitions, and mergers to enhance their product offerings and gain sustainable competitive advantage.

- March 2023 - CommScope, a global network connectivity solution, announced expansions to its fiber-optic cable production to accelerate broadband rollout across the U.S., connecting more communities and underserved areas. According to the company, this initiative will increase fiber-optic cable output in the U.S., hastening broadband deployment to underserved communities. Additionally, the company's HeliARC lines are expected to support 500,000 homes per year in FTTH deployments.

- March 2023 - European Eunion announced obligations to equip buildings with fiber-optic cables in line with its 2030 policy program for the digital decade. As per the new regulation, it will be mandatory to keep passive infrastructure (mini ducts) and in-building fiber wiring (fiber optic cables) in newly contracted buildings or buildings undergoing major renovations, up to the network termination point in the apartment/unit. EU is also planning to provide certification to the buildings that are 'fiber ready. Such trends are anticipated to drive the demand for fiber optic cables.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Impact of Key Macro-economic themes

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The Increased Data Traffic Creates the Demand for Fiber Optic Cable Network

- 5.1.2 Rising Investment in Fiber Optic and 5G Deployment

- 5.2 Market Challenges

- 5.2.1 Rising Demand For Wireless Solutions and Complex Installation Process

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Telecommunication

- 6.1.2 Power Utilities

- 6.1.3 Defence/military

- 6.1.4 Industrial

- 6.1.5 Medical

- 6.1.6 Other End-user Industries

- 6.2 By Country

- 6.2.1 United States

- 6.2.2 Germany

- 6.2.3 Austria and Switzerland

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nexans SA

- 7.1.2 Prysmian Group

- 7.1.3 Weinert Industries AG

- 7.1.4 Coherent Corporation

- 7.1.5 Sumitomo Corporation

- 7.1.6 Corning Inc.

- 7.1.7 Finisar Corporation

- 7.1.8 Leoni AG

- 7.1.9 Folan

- 7.1.10 Molex LLC

- 7.1.11 Fujikura Ltd

- 7.1.12 Sterlite Technologies

- 7.1.13 Furukawa Electric Co. Ltd

- 7.1.14 Smiths Interconnect (Smiths Group PLC)

8 STATE OF FIBRE OPTICS IN INDUSTRIES

9 FUTURE OUTLOOK OF THE MARKET

光纖電纜市場:依產品、產品類型、電纜安裝方式、光纖類型、交付方式及買家分類-2026-2032年全球市場預測

光纖電纜市場:依產品、產品類型、電纜安裝方式、光纖類型、交付方式及買家分類-2026-2032年全球市場預測 全球光纖電纜市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球光纖電纜市場規模、佔有率、趨勢和成長分析報告(2026-2034) 光纖電纜市場分析及預測(至2035年):類型、產品類型、技術、應用、材料類型、部署模式、最終用戶、安裝模式、傳輸模式

光纖電纜市場分析及預測(至2035年):類型、產品類型、技術、應用、材料類型、部署模式、最終用戶、安裝模式、傳輸模式 2026年全球超低損耗光纖市場報告光纖電纜市場:按光纖類型、電纜類型、組件、纖芯數量、應用和最終用戶分類,全球預測,2026-2032年全球多模光纖擾碼器市場(按光纖類型、通道數、速度、連接器類型和最終用戶分類)預測(2026-2032年)

2026年全球超低損耗光纖市場報告光纖電纜市場:按光纖類型、電纜類型、組件、纖芯數量、應用和最終用戶分類,全球預測,2026-2032年全球多模光纖擾碼器市場(按光纖類型、通道數、速度、連接器類型和最終用戶分類)預測(2026-2032年) 光纖電纜組件市場規模、佔有率和成長分析(按產品類型、模式類型、電纜長度、最終用戶和地區分類)—2026-2033年產業預測2026年全球多芯光纖推入式(MPO)或機械式傳輸推入式(MTP)光纜組件市場報告全球多芯室內配線光纜市場(以芯數、光纖類型、護套材料、結構類型和應用分類)預測(2026-2032)

光纖電纜組件市場規模、佔有率和成長分析(按產品類型、模式類型、電纜長度、最終用戶和地區分類)—2026-2033年產業預測2026年全球多芯光纖推入式(MPO)或機械式傳輸推入式(MTP)光纜組件市場報告全球多芯室內配線光纜市場(以芯數、光纖類型、護套材料、結構類型和應用分類)預測(2026-2032) 光纖電纜組件市場-全球產業規模、佔有率、趨勢、機會及預測(按模式類型、產品類型、最終用戶、地區和競爭格局分類,2020-2030 年預測)

光纖電纜組件市場-全球產業規模、佔有率、趨勢、機會及預測(按模式類型、產品類型、最終用戶、地區和競爭格局分類,2020-2030 年預測)