|

市場調查報告書

商品編碼

1693687

鋁鍛造-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Aluminium Forging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

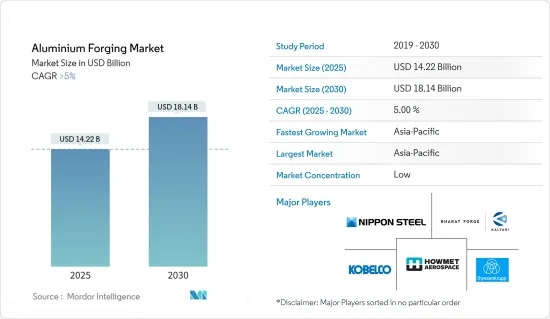

預計 2025 年鋁鍛造市場規模為 142.2 億美元,到 2030 年將達到 181.4 億美元,預測期內(2025-2030 年)的複合年成長率將超過 5%。

受新冠疫情影響,鋁鍛造市場遭遇挫折。全球封鎖和嚴格的政府監管導致大面積製造工廠關閉。然而,預計市場將在 2021 年復甦,並在未來幾年經歷顯著成長。

關鍵亮點

- 短期內,工業領域輕量材料的使用日益成長以及汽車和運輸行業的需求不斷成長是推動研究市場需求的關鍵因素。

- 然而,鋁價波動和嚴格的品質標準預計會阻礙市場成長。

- 鍛造和模擬技術的進步有望為該市場帶來新的機會。

- 預計亞太地區將主導全球市場,其中中國和印度的需求將佔據大部分市場佔有率。

鋁鍛造市場趨勢

汽車和運輸領域佔據市場主導地位

- 鋁在汽車領域有著廣泛的應用。它們對於引擎散熱器、車輪、保險桿、懸吊元件、引擎汽缸體、變速箱體以及包括引擎罩、車門和車架在內的車身部件至關重要。鋁因其重量輕、耐用和美觀而成為一種受歡迎的選擇,尤其是對於外部組件。

- 此外,鍛造鋁零件在汽車領域至關重要。隨著汽車產業越來越注重燃油效率、輕量化和減少二氧化碳排放,鋁在現代汽車中的重要性日益凸顯。每使用一公斤鋁,就會減輕一輛汽車的重量,這導致汽車零件對鋁的依賴增加,從而增加了市場需求

- 鋁的減震能力是鋼的兩倍,因此是首選。這種效應促使製造商在保險桿中更廣泛地使用鋁。此外,鋁製車身增強了安全性。即使鋁部件變形,與保持整體形狀的鋼不同,這種變化只局部撞擊區域,從而確保了乘員的安全。

- 2023年,在強勁的經濟擴張和不斷變化的消費者偏好的推動下,汽車產業經歷了強勁成長。根據國際汽車製造商組織(OICA)的數據,2019年全球汽車產量(包括乘用車和商用車)約為9,355萬輛。這將較2022年的產量約8,483萬輛有顯著成長,成長率約為10.26%。

- 2023年,亞太地區新商用車銷量將較2022年成長10.9%,達796萬輛,而2022年為717萬輛。

- 然而,在印度,商用車 (CV) 銷量在 2024 會計年度實現 2-5% 的小幅成長後,預計 2024-25 年 (FY25) 將會下降。根據印度投資資訊和信用評等機構(ICRA)的數據,預計2025會計年度將下降4-7%。

- 預計2023年北美汽車銷量將達到1,919萬輛,較2022年的1,693萬輛成長13.4%。其中,乘用車398萬輛,商用車1521萬輛,其餘為重型貨車、客車及長途客車。

- 此外,根據歐洲汽車工業協會的數據,2023年歐洲新車註冊量將成長18.7%,乘用車銷售量將達到1,500萬輛,商用車銷售量將達到290萬輛,分別高於2022年的1,264萬輛和2,44萬輛。

- 2024年第一季,英國貿易和工業部記錄了104,000輛商用車註冊,比去年同期顯著增加了59%。

- 根據OICA數據,2023年巴西輕型商用車產量將達42.2萬輛,與前一年同期比較成長20%,證實了市場成長。

- 此外,沙烏地阿拉伯的商用車市場正在經歷轉型。經濟多樣化和基礎設施現代化正在推動對先進商用車的需求,尤其是在 NEOM 和紅海計劃等大型企劃的實施過程中。

- 沙烏地阿拉伯商用車產業正朝著「2030願景」目標快速發展。美國沙烏地阿拉伯商務委員會預測,受基礎設施快速發展和對先進物流解決方案日益成長的需求的推動,到 2025 年,該市場規模將達到 67 億美元。

- 鑑於這些動態,市場預計在預測期內大幅成長。

亞太地區佔市場主導地位

- 預計亞太地區將引領鋁鍛造市場,並成為預測期內成長最快的地區。這種快速成長主要歸因於航太和國防、汽車和運輸、工業機械和建築等領域的需求不斷成長,尤其是在中國、印度、韓國、日本和東南亞各國。

- 鋁鍛件具有強度高、重量輕、耐腐蝕等特點,是高層建築、辦公大樓等高層建築中不可或缺的材料。這些零件可以承受惡劣的環境條件,最大限度地減少維護和維修的需要。隨著該地區建築業的擴張,未來幾年對鋁鍛件的需求將會上升。

- 中國的都市化進程旨在2030年使都市化達到70%,這凸顯了住宅需求和中階改善生活水準的願望。這些趨勢將推動住宅市場和住宅,從而使鋁鍛造市場受益。

- 到2024年,印度的經濟適用住宅預計將成長70%。據投資印度 (Invest India) 稱,到 2025 年,建築業的估值預計將達到 1.4 兆美元。預計到 2030 年,超過 30% 的人口將成為居住者,因此迫切需要超過 2,500 萬套中型和經濟適用住宅。近期推出的《房地產法》、《商品及服務稅》和《房地產投資信託》等旨在加快核准速度和加強建築業的改革正在推動市場成長。

- 鋁鍛件在航太領域發揮至關重要的作用,用於機身、機翼和控制面等結構部件。這些部件透過減輕引擎和結構部件的重量來提高飛機和太空船的性能。隨著該地區航太部門的擴張,對鋁鍛件的需求也預計會成長。

- 中國在全球航太領域脫穎而出,引領飛機製造和國內航空旅行。該國的飛機零件和組裝產業正在迅速擴張,擁有超過 200 家小型零件製造商。

- 根據國際貿易管理局(ITA)的數據,中國是世界第二大民用航太市場。根據中國國家統計局和中國民航局報告,截至2024年1月,全國民航機7,351架,比2022年增加550多架。

- 鋁鍛件對於減輕車輛重量、提高燃油效率和減少排放氣體起著至關重要的作用。除了減輕重量之外,這些部件還可以減輕車身重量和加強底盤,從而使汽車更加安全。該地區汽車產量的成長預計將推動對鋁鍛件的需求。

- 根據印度汽車製造商工業(SIAM)的數據,2024年1月至3月,印度的乘用車、商用車、三輪車、二輪車和四輪車產量為739萬輛。其中,乘用車銷售114萬輛,商用車銷售26.8萬輛。

- 鋁鍛件因其強度重量比、耐腐蝕性和耐用性而備受推崇,廣泛應用於工業機械。典型應用包括齒輪、變速箱、幫浦、閥門、軸承和襯套。隨著工業機械需求的增加,鋁鍛件的市場需求也預計將增加。

- 印度商務部數據顯示,2023會計年度出口額中,電子機械設備位居首位,緊隨其後的是酪農、食品加工和紡織等工業機械,出口額超過80億美元。展望未來,預計2024年電子機械和設備出口將達到近124億美元。

- 鍛造鋁零件透過減輕重量和降低能耗來提高電子和儀器零件的性能。亞太地區的電子產業正在蓬勃發展,這可能會刺激該領域對鋁鍛造件的需求。

- 根據日本電子情報技術產業協會數據顯示,2024年1月至6月,日本電子產業生產產品價值5,452.56億日圓(約33.86億美元),較去年同期大幅成長104.7%。

- 鑑於這些動態,預測期內亞太地區對鋁鍛件的需求將快速成長。

鋁鍛造業概況

鋁鍛造市場較為分散。主要企業(不分先後順序)包括 Howmet Aerospace、Bharat Forge、蒂森克虜伯股份公司、神戶製鋼所和新日鐵株式會社。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 工業領域擴大使用輕量材料

- 汽車和運輸業的需求增加

- 其他促進因素

- 限制因素

- 鋁價波動

- 嚴格的品質標準

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 鍛造造型

- 自由鍛造

- 密閉式模具模鍛

- 環輥鍛造

- 最終用戶產業

- 航太和國防

- 汽車和運輸

- 工業機械

- 建造

- 其他終端用戶產業(電子及測量儀器、能源電力、農業農村)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Accurate Steel Forgings(INDIA)Limited

- Al Forge Tech Co., Ltd.

- All Metals & Forge Group

- Aluminum Precision Products

- Anchor Harvey

- Anderson Shumaker Company

- Bharat Forge

- Ellwood Group Inc.

- Howmet Aerospace

- ILJIN Co., Ltd.

- Kobe Steel, Ltd.

- Nippon Steel Corporation

- Norsk Hydro ASA

- Ramkrishna Forgings Ltd

- Scot Forge Company

- Thyssenkrupp AG

- Wheel India Limited

第7章 市場機會與未來趨勢

- 先進的鍛造和模擬技術

- 其他機會

The Aluminium Forging Market size is estimated at USD 14.22 billion in 2025, and is expected to reach USD 18.14 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The aluminum forging market faced setbacks due to COVID-19. Global lockdowns and stringent government regulations led to widespread shutdowns of production hubs. However, the market rebounded in 2021 and is projected to see significant growth in the upcoming years.

Key Highlights

- Over the short term, the growing use of lightweight materials in the industrial sector and increasing demand from the automotive and transportation industries are the major factors driving the demand for the market studied.

- However, fluctuations in aluminum prices and stringent quality standards are expected to hinder the market's growth.

- Nevertheless, advanced forging techniques and simulation technologies is expected to create new opportunities for the market studied.

- Asia-Pacific region is expected to dominate the market across the world, with the majority of demand coming from China and India.

Aluminum Forging Market Trends

Automotive and Transportation Segment to Dominate the Market

- Aluminum is extensively used in the automotive sector. It's integral to components like engine radiators, wheels, bumpers, suspension elements, engine cylinder blocks, gearbox bodies, and body parts, including hoods, doors, and frames. Valued for its lightweight nature, durability, and aesthetic appeal, aluminum is especially favored for exterior components.

- Moreover, forged aluminum components are pivotal in the automotive realm. With the industry's emphasis on fuel efficiency, weight reduction, and curbing CO2 emissions, aluminum's significance in contemporary vehicles has surged. Every kilogram of aluminum reduces the vehicle's weight, prompting a growing reliance on aluminum for car parts and subsequently boosting market demand.

- Aluminum's shock-absorbing capabilities, being twice as effective as steel, make it a preferred choice. This efficacy has led manufacturers to use aluminum in bumpers consistently. Additionally, aluminum bodies offer enhanced safety; when aluminum parts deform, the change is localized to the impact area, unlike steel, which maintains the overall shape, ensuring passenger safety.

- In 2023, the automotive industry experienced significant growth, buoyed by robust economic expansion and evolving consumer preferences. Data from the Organisation Internationale des Constructeurs d'Automobiles (OICA) reveals a production of approximately 93.55 million units of vehicles worldwide, encompassing both passenger cars and commercial vehicles. This marked a notable uptick from the roughly 84.83 million units of vehicles produced in 2022, translating to a growth rate of about 10.26%.

- In 2023, the Asia Pacific region witnessed 10.9% increase in new commercial vehicle sales compared to 2022, with 7.96 million units registered in 2023, compared to 7.17million units in 2022.

- However, in India, commercial vehicle (CV) sales are projected to dip in the financial year 2024-25 (FY 25) after a modest 2-5% growth in FY24. As per the data from ICRA (Investment Information and Credit Rating Agency of India Limited) forecasts a 4-7% decline in FY25.

- North America saw motor vehicle sales reach 19.19 million units in 2023, a 13.4% rise from 2022's 16.93 million units, as reported by OICA. Of the total, passenger cars comprised 3.98 million units, commercial vehicles accounted for 15.21 million units, with the remainder being heavy trucks, buses, and coaches.

- Furthermore, as per the data from the European Automobile Manufacturers Association highlights an 18.7% surge in new motor vehicle registrations in Europe for 2023. Passenger car sales hit 15 million units, while commercial vehicles reached 2.90 million units, both up from 2022's 12.64 million and 2.44 million units, respectively.

- In the first quarter of 2024, the United Kingdom's trade industry recorded 104,000 commercial registrations, a notable 59% increase year-on-year, bolstered by the Ministry of Commerce's issuance of 65,363 permits in the same quarter of 2023.

- OICA data highlights Brazil's light commercial vehicle production at 422 thousand units in 2023, a 20% increase from the previous year, underscoring the market's growth.

- Moreover, Saudi Arabia is witnessing a transformation in its commercial vehicle market. As the nation diversifies its economy and modernizes its infrastructure, there's a growing demand for advanced commercial vehicles, especially with mega projects like NEOM and the Red Sea Project underway.

- Racing towards its Vision 2030 goals, Saudi Arabia's commercial vehicle sector is rapidly evolving. Projections suggest the market will reach USD 6.7 billion by 2025, driven by swift infrastructure developments and a rising demand for advanced logistics solutions, as per the U.S.-Saudi Arabian Business Council.

- Given these dynamics, the market is poised for significant growth during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is poised to lead the aluminum forging market, emerging as the region with the fastest growth during the forecast period. This surge is primarily fueled by rising demands in sectors like aerospace and defense, automotive and transportation, industrial machinery, and construction, particularly in nations such as China, India, South Korea, Japan, and various Southeast Asian countries.

- Owing to their high strength, lightweight nature, and corrosion resistance, forged aluminum parts are integral to high-rise buildings, including skyscrapers and office towers. These parts can endure harsh environmental conditions, minimizing maintenance and repair needs. With the region's construction sector expanding, the demand for aluminum forging is set to increase in the coming years.

- China's urbanization drive, targeting a 70% urban rate by 2030, underscores the demand for housing and the middle class's aspirations for improved living standards. These trends are poised to invigorate the housing market and residential construction, benefiting the aluminum forging market.

- In 2024, India is set to witness a 70% surge in the availability of affordable housing. According to Invest India, the construction sector is projected to attain a valuation of USD 1.4 trillion by 2025. With forecasts suggesting that over 30% of the population will be urban dwellers by 2030, there's a pressing need for 25 million more mid-end and affordable housing units. Recent reforms, such as the Real Estate Act, GST (Goods and Services Tax) and REITs (Real Estate Investment Trusts), aim to expedite approvals and strengthen the construction industry, driving market growth.

- Forged aluminum parts play a crucial role in aerospace, being used in structural components like fuselages, wings, and control surfaces. These parts enhance aircraft and spacecraft performance by lightening engine and structural components. As the aerospace sector expands in the region, the demand for aluminum forging is projected to grow.

- China stands out in the global aerospace arena, leading in aircraft manufacturing and domestic air travel. The nation's aircraft parts and assembly sector is rapidly expanding, boasting over 200 small parts manufacturers.

- As per the data from the International Trade Administration (ITA), China is the second-largest civil aerospace market globally. As of January 2024, the National Bureau of Statistics of China and the Civil Aviation Administration of China reported 7,351 civil aircraft, an increase of over 550 airplanes from 2022.

- Forged aluminum parts play a pivotal role in reducing vehicle weight, which in turn boosts fuel efficiency and curtails emissions. Beyond weight reduction, these components enhance vehicle safety by lightening the body and reinforcing the chassis. Given the uptick in vehicle production in the region, the demand for aluminum forging is set to rise.

- In India, data from the Society of Indian Automobile Manufacturers (SIAM) indicates that from January to March 2024, the production of passenger vehicles, commercial vehicles, three wheelers, two wheelers and quadricycle reached 7.39 million units. Specifically, sales for passenger and commercial vehicles were 1.14 million and 268 thousand units, respectively.

- Aluminum forging finds extensive application in industrial machinery, prized for its strength-to-weight ratio, corrosion resistance, and durability. Common applications include gears, gearboxes, pumps, valves, bearings, and bushings. As demand for industrial machinery rises, so too will the market's demand for aluminum forging.

- Data from India's Department of Commerce highlights that in the 2023 fiscal year, electric machinery and equipment topped the export value charts, followed closely by industrial machinery for dairy, food processing, and textiles, exceeding USD 8 billion. Looking ahead, exports of electrical machinery and equipment are expected to reach nearly USD 12.4 billion in the 2024 fiscal year.

- Forged aluminum parts enhance the performance of electronic and instrumentation components by reducing weight and energy consumption. With the electronics sector booming in Asia-Pacific, the demand for aluminum forging in this domain is set to escalate.

- Data from the Japan Electronics and Information Technology Industries Association reveals that Japan's electronics industry produced goods worth JPY 5,452,56 million (~USD 3,386 million) from January to June 2024, marking a remarkable 104.7% growth compared to the same period the previous year.

- Given these dynamics, the Asia-Pacific region is poised for a surge in aluminum forging demand during the forecast period.

Aluminum Forging Industry Overview

The aluminum forging market is fragmented in nature. The major players (not in any particular order) include Howmet Aerospace, Bharat Forge, Thyssenkrupp AG, Kobe Steel, Ltd., and Nippon Steel Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Use of Lightweight Material in Industrial Sector

- 4.1.2 Increasing Demand from the Automotive and Transportation Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Fluctuations in Aluminum Prices

- 4.2.2 Stringent Quality Standards

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Forging Type

- 5.1.1 Open Die Forging

- 5.1.2 Close Die Forging

- 5.1.3 Ring Rolled Forging

- 5.2 End-User Industry

- 5.2.1 Aerospace and Defense

- 5.2.2 Automotive and Transportation

- 5.2.3 Industrial Machinery

- 5.2.4 Construction

- 5.2.5 Other End-user Industries (Electronics and Instrumentation, Energy Power, Agriculture and Farming)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Accurate Steel Forgings (INDIA) Limited

- 6.4.2 Al Forge Tech Co., Ltd.

- 6.4.3 All Metals & Forge Group

- 6.4.4 Aluminum Precision Products

- 6.4.5 Anchor Harvey

- 6.4.6 Anderson Shumaker Company

- 6.4.7 Bharat Forge

- 6.4.8 Ellwood Group Inc.

- 6.4.9 Howmet Aerospace

- 6.4.10 ILJIN Co., Ltd.

- 6.4.11 Kobe Steel, Ltd.

- 6.4.12 Nippon Steel Corporation

- 6.4.13 Norsk Hydro ASA

- 6.4.14 Ramkrishna Forgings Ltd

- 6.4.15 Scot Forge Company

- 6.4.16 Thyssenkrupp AG

- 6.4.17 Wheel India Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advanced Forging Techniques and Simulation Technologies

- 7.2 Other Opportunities

2026-2030年全球熔模鑄造市場

2026-2030年全球熔模鑄造市場 消失模鑄造市場規模、佔有率和趨勢分析報告:按金屬、最終用途、地區和細分市場分類(2026-2033 年)

消失模鑄造市場規模、佔有率和趨勢分析報告:按金屬、最終用途、地區和細分市場分類(2026-2033 年) 鋁鑄造市場:2026-2032年全球市場預測(依鑄造製程、合金類型、最終用途產業及應用分類)

鋁鑄造市場:2026-2032年全球市場預測(依鑄造製程、合金類型、最終用途產業及應用分類) 全球鋁鑄件市場規模、佔有率、趨勢和成長分析報告(2026-2034年)複雜鋁鑄件市場:依製程、合金、生產方式、終端用戶產業和應用分類-全球預測,2026-2032年

全球鋁鑄件市場規模、佔有率、趨勢和成長分析報告(2026-2034年)複雜鋁鑄件市場:依製程、合金、生產方式、終端用戶產業和應用分類-全球預測,2026-2032年 2026年全球鋁鑄造市場報告全球永久鋁鑄件市場(按製程、合金類型、最終用途產業和應用分類)預測(2026-2032年)

2026年全球鋁鑄造市場報告全球永久鋁鑄件市場(按製程、合金類型、最終用途產業和應用分類)預測(2026-2032年) 鋁鑄造市場規模、佔有率及成長分析(按製程、原料、應用、最終用戶及地區分類)-產業預測(2026-2033)

鋁鑄造市場規模、佔有率及成長分析(按製程、原料、應用、最終用戶及地區分類)-產業預測(2026-2033) 鋁鑄件市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區、競爭細分,2020-2030 年)鋁鑄件市場規模、佔有率、趨勢分析報告:按工藝、按最終用途、按地區、細分市場預測,2025-2030 年

鋁鑄件市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區、競爭細分,2020-2030 年)鋁鑄件市場規模、佔有率、趨勢分析報告:按工藝、按最終用途、按地區、細分市場預測,2025-2030 年