|

市場調查報告書

商品編碼

1692523

越南金屬罐包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Vietnam Metal Can Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

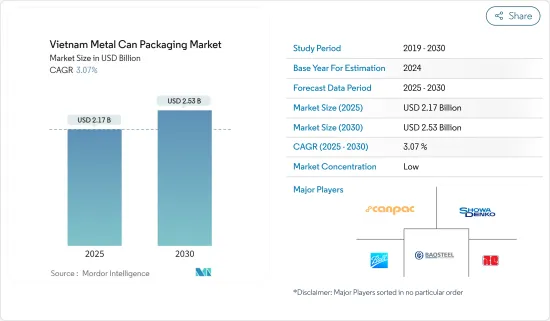

越南金屬罐包裝市場規模預計在2025年為21.7億美元,預計到2030年將達到25.3億美元,預測期內(2025-2030年)的複合年成長率為3.07%。

啤酒和碳酸飲料等酒精和非酒精飲料的消費量不斷增加,導致該國對金屬罐的需求增加,進而影響越南金屬罐包裝市場的成長。

主要亮點

- 金屬罐具有剛性、穩定性、阻隔性等優點,因此常用於遠距儲存和運輸貨物。鋼製和鋁製金屬罐在越南最受歡迎。這些材料具有柔軟、輕巧的寶貴特性,可以幫助製造商降低與物流相關的成本。

- 金屬罐的簡單性使其成為該地區許多消費者所追求的移動生活方式的理想包裝選擇。玻璃一般是禁止攜帶的,因為玻璃很容易破碎。罐頭的價格實惠、可回收性、能量飲料的日益普及以及新產品的推出都促進了市場的成長。

- 此外,越南生活方式的改變促使消費者選擇易於準備的食物。年輕人和獨居者消費更多的罐頭食品。這些消費者時間緊迫、預算有限,因此選擇成本更低、更方便的產品。

- 隨著環境問題成為焦點,飲料公司必須採用永續包裝來提供其產品。永續性是飲料行業的關鍵關注點。許多製造商正在轉向更環保的包裝替代品。 寶特瓶、由纖維素纖維材料製成的紙瓶和玻璃瓶被用作金屬罐的替代品,可能會對產業成長構成挑戰。

- 食品和飲料行業佔金屬罐包裝市場的大部分佔有率,在新冠疫情期間需求龐大。疫情導致人們的消費習慣發生重大變化。人們對包裝食品、肉類、蔬菜和水果的需求日益成長。

越南金屬罐包裝市場趨勢

越南對簡便食品的需求不斷成長

- 越南政府計劃透過發展高效、永續的產業,到 2030 年使該國成為世界領先的海鮮加工中心之一。因此,加工產品的出口比例應該會增加,越南水產品的價值也應該會增加。水產品出口額的成長顯示全球對越南冷凍水產品包裝的高需求帶動了越南黃金罐包裝市場的成長。預計中國都市化的加速將推動對包裝食品的需求。

- 漁業是越南每年創收超過10億美元的25個產業之一。根據越南水產品出口和生產者協會(VASEP)報道,越南水產品產業預計在 2024 年迎來良好開端。第一季出口額年增8%,達到約20億美元。這一成長主要得益於美國、日本、中國和香港等重要市場不斷成長的需求。 VASEP 預測,到 2024 年底,越南水產品出口額將比前一年成長 95 億美元。

- 此外,許多以前只經營新鮮農產品的公司現在正在大力投資加工食品,增加了對金屬罐包裝的需求。越南不斷成長的人口、不斷變化的收入水平、文化偏好和新的貿易協定為其肉類產業的顯著成長打開了大門。

- 根據美國農業部對外農業服務局(USDA)、越南統計總局和越南工業貿易部的調查,越南食品製造業成長了102.9%。越南加工食品業有近6000家企業。大部分市場佔有率由 Vissan、CJ Cau Tre 和 Ha Long Canfoco 等老字型大小企業佔據。

- 根據越南包裝協會報告,越南包裝產業約有1.4萬家企業,其中專注於塑膠包裝的企業有9,200家。越南有900多家包裝工廠,其中70%集中在南部,尤其是胡志明市、平陽、同奈等重點省份。在經濟和社會快速進步、電子商務產業蓬勃發展以及有利的自由貿易協定(FTA)的推動下,越南包裝產業有望實現顯著成長。

飲料業佔最大市場佔有率

- 金屬飲料罐在國內飲料市場需求量大,包括包裝啤酒和葡萄酒。消費者對使用環保和永續產品的意識不斷增強、回收率不斷提高以及金屬罐的可重複使用性正在推動研究市場的發展。

- 由於多種製造塗層技術,越南的金屬飲料罐市場正在顯著擴張。鋼和鋁零件安全可靠,符合衛生飲料包裝標準。金屬飲料罐價格實惠、實用、無污染。

- 越南的葡萄酒市場正在成長,飯店、餐廳和零售商提供來自世界各地的各種葡萄酒。越南的各項自由貿易協定(FTA)使得葡萄酒市場更具競爭力,吸引外國投資者轉移生產和開展業務。自由貿易協定的主要目標是透過大幅降低或完全放寬進口商品關稅,在成員國之間建立一體化市場。

- 越南政府計劃減少其在國有企業的股份,以鼓勵該國私營部門的發展,這將為該國飲料業的前景帶來積極影響。這與越南加入世貿組織以及CPTPP和EVFTA等一系列自由貿易協定一起,旨在吸引跨國公司投資飲料產業,並為越南企業增加出口創造機會。為了滿足飲料產量的增加,企業加大了投資,金屬罐的需求也正在擴大。

- 東南亞中階的不斷壯大以及消費者對飲料罐的偏好繼續推動對金屬罐的需求。軟性飲料、沖泡茶粉、各種果汁和能量飲料佔越南飲料市場年產量和消費量的相當大比例。根據越南統計總局預測,2022年飲料製造業收益將達68.5564億美元,2023年將達76.9183億美元。

越南金屬罐包裝產業概況

越南金屬罐包裝市場較為分散,許多主要企業不斷競爭以搶佔最大的市場佔有率。主要公司包括Canpac Vietnam、Showa Aluminum Can Corporation、TBC-Ball Beverage Can VN Ltd、Ball Corporation、越南寶鋼罐頭(寶鋼集團)和Royal Can Industries Company Limited。雖然許多市場參與者已經開發出高品質的金屬罐包裝解決方案,但其他市場參與者正在努力有效回收包裝產品以滿足行業需求。

- 2024 年 1 月,越南胡志明市的精釀啤酒廠 Rooster Beers 為其廣受歡迎的金髮啤酒和黑啤酒推出了全新、更纖薄的罐體設計。公雞啤酒 (Rooster Beer) 以釀造傳統而又平易近人的啤酒而聞名,但現在它正在西方傳統之外開闢自己的道路。該品牌推出時尚罐頭設計的舉動凸顯了這一轉變。精心挑選的設計元素賦予新罐子生動活潑的現代感。

- 2024 年 4 月:在越南,生產者延伸責任 (EPR) 政策要求生產商和進口商確保其一定比例的產品和包裝得到回收。如果無法回收,他們必須向越南環境保護(VEP)基金捐款。自然資源與環境部(MONRE)在第 08/2022/ND-PC 號法令中概述了這些義務。自2024年1月起,電池、潤滑油和輪胎將受新規約束;自2025年1月1日起,電氣和電子產品將受新規約束;自2027年1月起,運輸產品將受新規約束。 MONRE也負責在2025年1月前提案運輸車輛處置法規。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響評估

第5章市場動態

- 市場促進因素

- 越南對簡便食品的需求不斷增加

- 提高回收率並增加最終用戶製造需求

- 市場限制

- 對軟塑膠等替代產品的需求不斷增加

- 市場機會

- 越南食品飲料罐進出口分析

第6章市場區隔

- 按類型

- 鋁罐

- 鋼

- 按最終用戶

- 食物

- 飲料

- 化妝品和個人護理

- 製藥

- 畫

- 汽車(潤滑油)

- 其他最終用戶

第7章競爭格局

- 公司簡介

- Canpac Vietnam Co. Ltd

- Showa Aluminum Can Corporation

- TBC-Ball Beverage Can VN Ltd(Ball Corporation)

- Vietnam Baosteel Can Co. Ltd(Baosteel Group)

- Royal Can Industries Company Limited

- Hanacan JSC

- Superior Multi-packaging Limited(SMPL)

- Kian Joo Can(Vietnam)Co. Ltd

- Nam Viet Packaging Manufacturing Co. Ltd

- My Chau Printing & Packaging Corporation

第8章投資分析

第9章:市場的未來

The Vietnam Metal Can Packaging Market size is estimated at USD 2.17 billion in 2025, and is expected to reach USD 2.53 billion by 2030, at a CAGR of 3.07% during the forecast period (2025-2030).

The rising consumption of alcoholic and nonalcoholic beverages, such as beer and carbonated drinks, is attributed to increased demand for metal cans in the country, thereby influencing the Vietnamese metal can packaging market's growth.

Key Highlights

- Due to its many advantages, such as rigidity, stability, and high barrier qualities, metal cans are frequently used to store and transport commodities across great distances. Metal cans constructed of steel and aluminum are the most popular in Vietnam. These materials have valuable qualities, such as being softer and lighter, which enable the makers to reduce logistics-related expenses.

- Because of their simplicity, metal cans are among the best packaging options for the mobile lifestyle that many consumers in the area lead. These can be carried or transported easily to outdoor sporting events, festivals, and beaches, whereas glass is typically forbidden because of its breakability. The affordability and recyclability of cans, the rising popularity of energy drinks, and the launch of new goods all contribute to the market's growth.

- Moreover, changing lifestyles in Vietnam are resulting in consumers opting for easy-to-cook food. The younger population and individually living consumers are consuming more canned food. These users have less time and are budget-restrained, thus opting for products with lower costs and higher convenience.

- With environmental concerns at the forefront, it becomes imperative for beverage companies to offer their products in sustainable packaging. Sustainability is a significant concern in the beverage industry. Many manufacturing companies are switching to eco-friendly packaging alternatives. PET bottles, paper bottles made with cellulose-fiber material, and glass bottles are used as an alternative to metal cans and can challenge their growth in the industry.

- The food and beverage industry, with a significant share in the metal can packaging market, witnessed huge demand amidst the COVID-19 pandemic. The pandemic brought a significant change in consumption habits. There has been an increasing need for packaged food products, meat, vegetables, and fruits.

Vietnam Metal Can Packaging Market Trends

Growing Demand For Convenience Food in Vietnam

- The Vietnamese government intends to make the country one of the world's leading seafood processing centers by 2030 by developing an efficient and sustainable industry. This should result in a higher export ratio of processed products and an increase in the value of Vietnamese seafood. The increasing export value of seafood has demonstrated that the high demand for packaged frozen seafood from Vietnam worldwide has led to the growth of the Vietnamese metal can packaging market. The growing urbanization in the country is expected to drive the demand for packaged food.

- The fishery is one of the 25 products that bring the country an income of more than USD 1 billion each year. The Vietnam Association of Seafood Exporters and Producers (VASEP) reported a strong beginning for Vietnam's seafood industry in 2024. Exports have surged to almost USD 2 billion in Q1, reflecting an 8% year-on-year uptick. This growth is primarily fueled by heightened demands from pivotal markets such as the United States, Japan, China, and Hong Kong. VASEP projects that by the close of 2024, Vietnam's seafood exports could hit a notable USD 9.5 billion, surpassing the previous year's figures.

- Moreover, the demand for metal can packaging is increasing with the growing investments by many businesses that previously only traded fresh agricultural products and have invested heavily in processed foods. Vietnam's rising population, income levels, changing cultural preferences, and new trade agreements opened the door to significant growth in the meat industry.

- According to the study by the USDA Foreign Agricultural Service, General Statistics Office of Vietnam, and the Ministry of Industry and Trade (Vietnam), food product manufacturing grew by 102.9 % in the country. There are nearly 6,000 enterprises operating in Vietnam's processed food industry. Most of the market share is held by well-established players such as Vissan, CJ Cau Tre, or Ha Long Canfoco.

- The Vietnam Packaging Association reports that Vietnam's packaging industry is home to approximately 14,000 enterprises, with a significant emphasis on plastic packaging, to which 9,200 enterprises are dedicated. The country boasts over 900 packaging factories, with a notable 70% concentrated in the southern region, particularly in key areas like Ho Chi Minh City, Binh Duong, and Dong Nai. Driven by swift economic and social advancements, a booming e-commerce sector, and advantageous free trade agreements (FTAs), Vietnam's packaging sector is poised for substantial growth.

Beverages Sector to Hold the Largest Market Share

- The beverage metal cans find significant demand in beer and wine packaging and other beverage markets in the country. The growing consumer awareness of the need to use green and environmentally sustainable products, the increasing recycling rate, and the reusability of metal cans are driving the market studied.

- In Vietnam, the market for beverage metal cans is expanding significantly due to the various manufacturing coating technologies. The steel and aluminum components meet secure, dependable, and hygienic beverage packaging standards. Metal beverage cans are affordable, practical, and anti-contaminating.

- The Vietnamese wine market is growing, with hotels, restaurants, and retailers offering various wines from around the world. Vietnam's diverse free trade agreements (FTAs) have made the wine market competitive, attracting foreign investors to relocate production or set up operations. The main objective of FTAs is to create an integrated market among country members by significantly reducing or fully liberalizing custom tariffs for imported products.

- Vietnam's Government has planned to decrease its stake in state-owned enterprises to encourage the country's private sector, supporting the positive outlook for Vietnam's beverage industry. This, accompanied by Vietnam's membership in the WTO and many free trade agreements such as CPTPP and EVFTA, aims to attract multinational companies to invest in the drink sector and generate opportunities for Vietnamese companies to increase exports. With the increasing investment by the companies as the production of the beverage increases, the demand for metal cans is growing.

- The growth of the middle class in Southeast Asia and consumers' preference for beverage cans continue to increase demand for metal cans. A significant percentage of the annual production and consumption of Vietnam's beverage market is soft drinks, instant teas, fruit juices of all kinds, and energy drinks. According to the General Statistics Office of Vietnam, the revenue from manufacturing beverages in 2022 was estimated at USD 6,855.64 million, and it reached USD 7,691.83 million in 2023.

Vietnam Metal Can Packaging Industry Overview

The Vietnamese metal can packaging market is fragmented owing to many key players continually trying to gain maximum market share. Some of the major players are Canpac Vietnam Co. Ltd, Showa Aluminum Can Corporation, TBC-Ball Beverage Can VN Ltd, Ball Corporation, Vietnam Baosteel Can Co. Ltd (Baosteel Group), and Royal Can Industries Company Limited. Many market players are developing high-quality metal can packaging solutions while others are making efforts toward efficient recycling of packaging products to cater to the industry requirements.

- January 2024: Rooster Beers, a craft brewery hailing from Ho Chi Minh City, Vietnam, unveiled a fresh, slim can design for its popular Blonde and Dark brews. While Rooster Beers has built its reputation on crafting traditional yet approachable beers, it is now charting a unique path, diverging from Western norms. The brand's move to introduce a sleek can design underscores this departure. With meticulously chosen design elements, the new cans exude a lively, contemporary vibe.

- April 2024: In Vietnam, the "extended producer responsibility" (EPR) policy now requires producers and importers to ensure the recycling of a set portion of their products and packaging. If they cannot recycle, they must contribute financially to the Vietnam Environment Protection (VEP) Fund. The Ministry of Natural Resources and Environment (MONRE) outlined these mandates in Decree 08/2022/ND-PC. Companies have specific deadlines to start recycling different items: batteries, lubricants, and tires from January 2024; electrical and electronic products from January 1, 2025; and means of transportation from January 2027. MONRE is also tasked with proposing disposal regulations for transportation by January 2025.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Convenience Food in Vietnam

- 5.1.2 Higher Recycling Rates Coupled with Higher End-user Manufacturing Demand

- 5.2 Market Restraints

- 5.2.1 Growing Demand for Alternative Products Such as Flexible Plastic

- 5.3 Market Opportunities

- 5.4 Import-Export Analysis of Food Cans and Beverage Cans in Vietnam

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By End User

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Cosmetic and Personal Care

- 6.2.4 Pharmaceuticals

- 6.2.5 Paints

- 6.2.6 Automotive (Lubricants)

- 6.2.7 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Canpac Vietnam Co. Ltd

- 7.1.2 Showa Aluminum Can Corporation

- 7.1.3 TBC-Ball Beverage Can VN Ltd (Ball Corporation)

- 7.1.4 Vietnam Baosteel Can Co. Ltd (Baosteel Group)

- 7.1.5 Royal Can Industries Company Limited

- 7.1.6 Hanacan JSC

- 7.1.7 Superior Multi-packaging Limited (SMPL)

- 7.1.8 Kian Joo Can (Vietnam) Co. Ltd

- 7.1.9 Nam Viet Packaging Manufacturing Co. Ltd

- 7.1.10 My Chau Printing & Packaging Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026年全球罐頭食品市場研究報告

2026年全球罐頭食品市場研究報告 複合罐市場:2026-2032年全球市場預測(依材料、產品種類、產能、製造流程、隔離層、塗層、瓶蓋/瓶蓋及最終用途分類)

複合罐市場:2026-2032年全球市場預測(依材料、產品種類、產能、製造流程、隔離層、塗層、瓶蓋/瓶蓋及最終用途分類) 全球複合紙罐市場規模、佔有率、趨勢和成長分析報告(2026-2034年)不含雙酚A的易拉罐市場:依材質、罐體尺寸、塗層類型、最終用途及通路分類-2026-2032年全球預測

全球複合紙罐市場規模、佔有率、趨勢和成長分析報告(2026-2034年)不含雙酚A的易拉罐市場:依材質、罐體尺寸、塗層類型、最終用途及通路分類-2026-2032年全球預測 複合罐市場-全球產業規模、佔有率、趨勢、機會及預測(按封蓋類型、生產類型、罐體直徑、最終用戶、地區和競爭格局分類,2021-2031年)

複合罐市場-全球產業規模、佔有率、趨勢、機會及預測(按封蓋類型、生產類型、罐體直徑、最終用戶、地區和競爭格局分類,2021-2031年) 罐裝包裝市場規模、佔有率和成長分析(按罐型、罐形、產業和地區分類)-2026-2033年產業預測

罐裝包裝市場規模、佔有率和成長分析(按罐型、罐形、產業和地區分類)-2026-2033年產業預測 全球罐頭包裝市場全球複合罐市場

全球罐頭包裝市場全球複合罐市場 複合罐市場機會、成長動力、產業趨勢分析及2025-2034年預測

複合罐市場機會、成長動力、產業趨勢分析及2025-2034年預測 2032 年馬口鐵包裝市場預測:按產品、厚度、應用、最終用戶和地區進行的全球分析

2032 年馬口鐵包裝市場預測:按產品、厚度、應用、最終用戶和地區進行的全球分析