|

市場調查報告書

商品編碼

1692455

直流馬達:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Direct Current (DC) Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

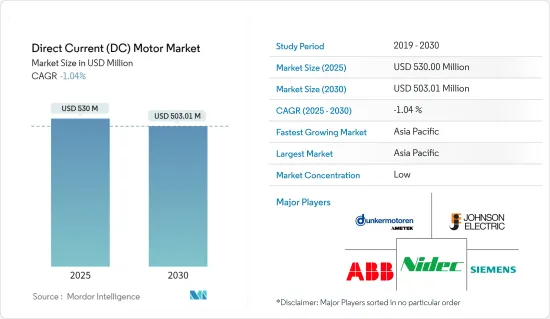

DC馬達市場規模預計在 2025 年達到 5.3 億美元,預計到 2030 年將下降至 5.0301 億美元。

工業自動化程度的提高推動了對DC馬達的需求,直流馬達透過提供精確的控制和可靠的性能在自動化系統中發揮至關重要的作用。新興經濟體的勞動力短缺導致製造業採用機器人技術,這也產生了對不同類型DC馬達,例如並聯馬達、他勵馬達和復勵馬達。

主要亮點

- DC馬達廣泛應用於汽車系統,例如雨刷馬達、電動座椅馬達、電動車窗馬達、暖通空調系統等。此外,電動車的普及率正在上升,預計這將在預測期內支持市場成長。汽車業的日產量大幅增加。

- 石油和天然氣、採礦、發電、化學和石化等行業通常涉及惡劣和易爆的環境,因此職業安全變得越來越重要,世界許多地方的政府都要求空氣品質優良。因此,HVAC 系統透過管理和控制空氣循環來幫助創造安全的工作環境。由於 HVAC 系統已成為工業領域不可或缺的一部分,對DC馬達的需求也隨之增加,因為它們用於 HVAC 系統中的鼓風機馬達、變速驅動裝置和 AHU,以提高效率並最大限度地延長鼓風機系統的使用壽命。

- 汽車產業正迅速採用無污染電動車(EV)。開發和改進電動車以取代傳統汽車對於實現客戶滿意度和高科技成果至關重要。國際能源總署表示,電動車是全球新能源經濟快速崛起的驅動力之一,正在為全球汽車製造業帶來歷史性變革。

- 有幾個障礙阻礙了DC馬達的廣泛應用。主要挑戰圍繞著所涉及的成本:能源成本、維護成本和初始購買成本。這是因為DC馬達的繞線轉子和換向器比感應感應馬達的繞線轉子和換向器複雜得多。這些是由銅和鐵製成的,而不是鋁和鐵。DC馬達的轉子更重,可能需要更昂貴的軸承。

- 新冠肺炎疫情對市場產生了影響,包括多個國家政府實施的各種遏制措施嚴重影響了工業部門的成長。因此,所研究的市場由於供應鏈問題而經歷了放緩,尤其是在初始階段。不過,隨著主要終端用戶產業全面復工,智慧DC馬達的需求預計將會增加。

直流馬達市場趨勢

石油和天然氣領域預計將強勁成長

- 在石油和天然氣領域,馬達對於向鑽機系統和設備提供穩定可靠的電源至關重要。DC馬達專門用於確保為鑽孔機系統和設備提供穩定可靠的電力供應。這些馬達有助於支援各種操作,包括原油、石油和天然氣等商品的開採、加工、儲存和運輸。

- 石油和天然氣產業依靠鑽機設備從儲存中提取石油和天然氣,包括陸上和海上鑽井活動。DC馬達被廣泛用作這些鑽孔機的動力來源。這些DC馬達的設計可承受石油和天然氣環境中常見的挑戰,包括振動、極端溫度、頻繁衝擊和腐蝕環境。直流馬達因其優異的性能,在陸上油氣工業的應用具有特別重要的意義。

- 國際能源總署(IEA)預測,儘管有現有的政策設定,但全球對石油和天然氣的需求將在2030年達到高峰。根據國際能源總署預測,到本世紀末,全球石油需求預計將增加 800 萬桶/日,這將對海上活動帶來更大的需求。因此,隨著海外業務和投資的增加,AC馬達市場預計將出現激增。這些馬達用於各種海上應用,包括為絞車和捲揚機、水泥泵、推進器和推進器提供動力。

- DC馬達非常適合海上鑽井活動,因為它們可以為泥漿泵、絞車、轉盤和頂部驅動器等關鍵設備提供可變速度。海上鑽油平臺在全球石油鑽機數量中扮演關鍵角色,貝克休斯報告稱,2023 年 11 月全球將有 272 個鑽機投入運作,其中超過 91 個位於亞太地區。重新進行海上石油探勘受到多種因素的推動,包括全球能源需求增加、烏克蘭衝突造成的供應中斷以及與疫情爆發前相比仍然較高的油價。

亞太地區預計將經歷強勁成長

- 預計未來幾年中國DC馬達市場將顯著成長。推動市場發展的因素有很多,包括對電動車的需求不斷增加、中國製造業自動化程度不斷提高以及中國對家用電器的需求不斷成長。

- 在中國,智慧製造計劃預計將推動工業DC馬達的使用。根據資訊化部消息,將在全國啟動一批智慧製造先導計畫。此外,根據「十三五」智慧製造規劃,政府計畫在2025年加強智慧製造體系建設,實現重點產業的全面轉型。透過這些努力,預計DC馬達在全國各行業的應用將會成長。

- 印度人口和工業的快速成長導致污水量大幅增加。這種驚人的成長導致該國對污水處理廠的需求增加。這一成長主要受到全國各地市政當局和污水處理廠不斷成長的需求的推動。水處理廠嚴重依賴泵浦和馬達系統來有效率、有效地完成水的處理過程。因此,全國各地對這些處理廠的需求不斷增加也將推動對DC馬達的需求。

- 此外,該領域的市場擴張主要歸功於技術進步和各個終端用戶行業對自動化技術的日益廣泛的使用。推動該國DC馬達需求的其他關鍵因素包括快速的都市化、互補的技術改進、有利的政府法規以及強勁的直接投資流入。

直流馬達市場概況

直流馬達市場分散,企業間競爭日益激烈。市場的主要參與者包括 ABB 有限公司、AMETEK 公司(Dunkermotoren GmbH)、德昌電機控股有限公司、日本電產株式會社和西門子股份公司。從市場佔有率來看,這些大公司目前佔據著市場主導地位。然而,隨著技術創新的不斷增加,許多公司正在透過贏得新契約和開拓新市場來擴大其市場佔有率。

- 2023 年 12 月 - 富蘭克林電氣公司富蘭克林電氣公司是一家為住宅、商業、農業和工業應用提供馬達、驅動器和控制設備的供應商。此次收購使該公司能夠加強和擴大其在主要地區的水處理管道和產品。

- 2023 年 7 月-Nidec 宣布已收購 TAR, LLC d/b/a Houma Armature Works 的全部所有權。該服務合作夥伴重新製造馬達和發電機,並為路易斯安那州和德克薩斯州的石油和天然氣生產商提供現場服務。此次收購使 NMC 能夠加強其服務產品,包括擴大其在美國安裝基數中的佔有率。霍馬將能夠為 NMC 的客戶提供服務。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 產業價值鏈分析

- 新冠疫情的後續影響以及其他宏觀經濟因素將影響市場

第5章市場動態

- 市場促進因素

- 無刷直流馬達的採用率不斷提高

- 電動車日益普及

- 市場挑戰

- 維護成本高

第6章市場區隔

- 按類型

- 永久磁/自勵式

- 個體激勵

- 按最終用戶產業

- 石油和天然氣

- 化工和石化

- 發電

- 用水和污水

- 金屬與礦業

- 飲食

- 離散製造業

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 北美洲

第7章競爭格局

- 公司簡介

- ABB Ltd

- AMETEK Inc.(Dunkermotoren GmbH)

- Johnson Electric Holdings Limited

- Nidec Corporation

- Siemens AG

- Franklin Electric

- Allied Motion Technologies Inc.

- Regal Rexnord Corporation

- North American Electric Inc.

- Maxon

- Buhler Motor GmbH

- MinebeaMitsumi Inc.

第8章投資分析

第9章:市場的未來

The Direct Current Motor Market size is estimated at USD 530.00 million in 2025, and is expected to decline to USD 503.01 million by 2030.

Increasing industrial automation drives the demand for DC motors, which play a vital role in automated systems by providing precise control and reliable performance. Labor shortages in emerging countries are leading to the adoption of robotics in the manufacturing industry, which is also creating demand for different types of DC motors, such as shunt motors, separately excited motors, and compound motors.

Key Highlights

- DC motors are widely used in automobile systems for wiper motors, power seat motors, power window motors, and HVAC systems. Additionally, the growing adoption of electric vehicles is expected to support the market's growth during the forecast period. The automotive sector has witnessed a significant increase in daily units produced.

- Owing to the rising importance of occupational safety in the global regions, the government has mandated quality air management as industries such as oil and gas, mining, power generation, chemicals, and petrochemicals often involve harsh and explosive atmospheres. Thus, HVAC systems aid in creating a safe working environment by managing and controlling air circulation. With HVAC systems turning out to be an integral part of the industrial sector, DC motors are also able to create a generous demand as they are used in HVAC systems' blower motors, variable speed drives, and AHUs to achieve high efficiency in airflow systems along with in maximizing their lives.

- The automotive industry has rapidly introduced pollution-free electric vehicles (EVs). The development and improvement of EVs to replace conventional vehicles has become crucial to obtaining customer satisfaction and high-tech achievements. As per the IEA, electric vehicles are one of the driving forces in the new global energy economy that is rapidly emerging, and they are bringing about a historic transformation of the car manufacturing industry worldwide.

- Several obstacles are preventing the widespread use of DC motors. The main challenges revolve around the associated expenses, including energy costs, maintenance costs, and initial purchase costs. This is because the wound rotor and commutator of a DC motor are quite a bit more complicated than the rotor of an induction motor. They are made out of copper and iron rather than aluminum and iron. The heavier rotor of the DC motor may require more expensive bearings.

- The impact of the COVID-19 pandemic was observed on the market as various containment measures taken by governments across multiple countries, such as the implementation of lockdown, significantly impacted the growth of the industrial sector. As a result, a slowdown was witnessed in the studied market, especially during the initial phase, due to supply chain issues. However, with significant end-user industries resuming operations at total capacity, the demand for smart DC motors is anticipated to increase.

Direct Current (DC) Motor Market Trends

The Oil and Gas Segment is Expected to Witness Major Growth

- Electric motors are crucial in oil and gas by delivering a steady and dependable power source to drill rig systems and equipment. DC motors are specifically utilized to ensure a consistent and reliable power supply to drilling rig systems and equipment. These motors are instrumental in supporting various operations, such as extracting, processing, storing, and transporting commodities like crude oil, petroleum, and natural gas.

- Oil and natural gas extraction from reservoirs in the oil and gas sector relies on drilling rig equipment for both onshore and offshore drilling activities. These drilling rigs extensively utilize DC motors as their power source. These DC motors are designed to withstand the challenging conditions commonly found in oil and gas settings, such as vibration, extreme temperatures, frequent impacts, and corrosive environments. Because of their exceptional performance, the utilization of DC electric motors in onshore oil and gas industries has notable significance.

- The International Energy Agency (IEA) has projected that global oil and gas demand will peak by 2030 despite the existing policy settings. According to the IEA, there will be an approximate increase of eight million barrels per day (bpd) in global demand by the decade's end, leading to a more significant requirement for offshore activities. Consequently, there is an anticipated surge in the market for AC motors due to the growth in offshore operations and investments. These motors are utilized in various offshore applications, including powering winches and windlasses, cement pumps, propulsion, and thrusters.

- DC motors are highly suitable for offshore drilling activities because they provide variable speeds to essential equipment such as mud pumps, draw works, rotary tables, and top drives. Offshore drilling rigs play a significant role in the global oil rig count, with 272 active rigs across the world in November 2023, over 91 of which are located in Asia-Pacific, as reported by Baker Hughes. The renewed search for offshore petroleum is driven by a combination of factors, including increased global energy demand, supply disruptions caused by the conflict in Ukraine, and crude oil prices that have remained elevated compared to pre-pandemic levels.

Asia-Pacific is Expected to Witness Significant Growth

- The Chinese DC motor market is poised for significant growth in the coming years. Several factors drive the market, including the increasing demand for EVs, the growing automation in the Chinese manufacturing sector, and the rising demand for consumer electronics in China.

- In China, smart manufacturing endeavors are anticipated to facilitate the utilization of industrial DC motors. The Ministry of Information Technology has reported initiating numerous smart manufacturing pilot projects in the country. Furthermore, as outlined in the 13th smart manufacturing five-year plan, the government intends to enhance its smart manufacturing system and achieve a comprehensive transformation of key industries by 2025. Such initiatives are expected to drive the adoption of DC motors across the country's sectors.

- With the rapid growth of India's population and its industrial sector, there has been a significant increase in the volume of wastewater. This alarming rise has prompted the country's need for wastewater treatment plants. The rising demand for nationwide municipal and sewage water treatment facilities primarily drives the growth. Water treatment plants heavily rely on pump and motor systems to efficiently and effectively move water through the treatment process. Consequently, the increasing demand for these treatment plants nationwide will also drive the demand for DC motors.

- Moreover, the market's expansion in this area is primarily due to technical advancements and the increased usage of automation technologies across various end-user industries. Other significant factors driving the demand for DC motors in the country include rapid urbanization, complementary technical improvements, favorable government regulations, and robust FDI inflows.

Direct Current (DC) Motor Market Overview

The direct current (DC) motor market is fragmented and is witnessing rising competitiveness among companies. The market consists of major players, such as ABB Ltd, AMETEK Inc. (Dunkermotoren GmbH), Johnson Electric Holdings Limited, Nidec Corporation, and Siemens AG. In terms of market share, these significant players currently dominate the market. However, with increasing technology innovations, many companies are increasing their market presence by securing new contracts and tapping new markets.

- December 2023 - Franklin Electric Co. Inc., which offers motors, drives, and controls for residential, commercial, agricultural, and industrial applications, announced that it had acquired the assets of Action Manufacturing & Supply Inc., a provider of control valves for commercial and industrial applications. This acquisition helps the company strengthen and expand its channels and products for water treatment in critical geographic areas.

- July 2023 - Nidec Corporation announced that it acquired full ownership of TAR, LLC d/b/a Houma Armature Works. This service partner remanufactures motors and generators and provides field service to oil and gas producers operating out of Louisiana and Texas. Through this acquisition, NMC will be able to enhance its service offering, including expanding its share within its own US installed base. Houma will be able to provide services to NMC's customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of the COVID-19 Pandemic's After effects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Adoption of Brushless DC Motor

- 5.1.2 Growing Prevalence of Electric Vehicles

- 5.2 Market Challenges

- 5.2.1 High Cost of Maintenance

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Permanent Magnet and Self-Excited

- 6.1.2 Separately Excited

- 6.2 By End-user Industry

- 6.2.1 Oil and Gas

- 6.2.2 Chemical and Petrochemical

- 6.2.3 Power Generation

- 6.2.4 Water and Wastewater

- 6.2.5 Metal and Mining

- 6.2.6 Food and Beverage

- 6.2.7 Discrete Industries

- 6.2.8 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 South Korea

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Mexico

- 6.3.4.3 Rest of Latin America

- 6.3.5 Middle East and Africa

- 6.3.5.1 Saudi Arabia

- 6.3.5.2 United Arab Emirates

- 6.3.5.3 South Africa

- 6.3.5.4 Rest of Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 AMETEK Inc. (Dunkermotoren GmbH)

- 7.1.3 Johnson Electric Holdings Limited

- 7.1.4 Nidec Corporation

- 7.1.5 Siemens AG

- 7.1.6 Franklin Electric

- 7.1.7 Allied Motion Technologies Inc.

- 7.1.8 Regal Rexnord Corporation

- 7.1.9 North American Electric Inc.

- 7.1.10 Maxon

- 7.1.11 Buhler Motor GmbH

- 7.1.12 MinebeaMitsumi Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

碳刷市場規模、佔有率及成長分析(按最終用途產業、材料類型、應用、技術及地區分類)-產業預測,2025-2032年

碳刷市場規模、佔有率及成長分析(按最終用途產業、材料類型、應用、技術及地區分類)-產業預測,2025-2032年 直流DC馬達市場:無刷直流馬達和有刷直流馬達-2025-2032 年全球預測直流馬達市場按產品類型、最終用途產業、額定功率、額定電壓、安裝方式和分銷管道分類-2025-2032年全球預測碳刷市場按最終用途產業、材料類型、應用和技術分類-2025-2032年全球預測

直流DC馬達市場:無刷直流馬達和有刷直流馬達-2025-2032 年全球預測直流馬達市場按產品類型、最終用途產業、額定功率、額定電壓、安裝方式和分銷管道分類-2025-2032年全球預測碳刷市場按最終用途產業、材料類型、應用和技術分類-2025-2032年全球預測 有刷馬達的全球市場:各零件,各類型,各輸出功率,各產業,各銷售管道,各地區- 市場規模,產業動態,機會分析,預測(2025年~2033年)

有刷馬達的全球市場:各零件,各類型,各輸出功率,各產業,各銷售管道,各地區- 市場規模,產業動態,機會分析,預測(2025年~2033年) DC馬達市場規模、佔有率、趨勢分析報告:按類型、電壓、最終用途、地區、細分市場預測,2025-2030

DC馬達市場規模、佔有率、趨勢分析報告:按類型、電壓、最終用途、地區、細分市場預測,2025-2030 全球有刷直流馬達市場全球碳刷市場有刷直流 (DC)馬達市場報告:2030 年趨勢、預測與競爭分析電動車無刷馬達市場報告:趨勢、預測、競爭分析(至 2030 年)

全球有刷直流馬達市場全球碳刷市場有刷直流 (DC)馬達市場報告:2030 年趨勢、預測與競爭分析電動車無刷馬達市場報告:趨勢、預測、競爭分析(至 2030 年)