|

市場調查報告書

商品編碼

1690928

大豆殺菌劑種子處理:市場佔有率分析、產業趨勢與成長預測(2025-2030)Soybean Fungicide Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

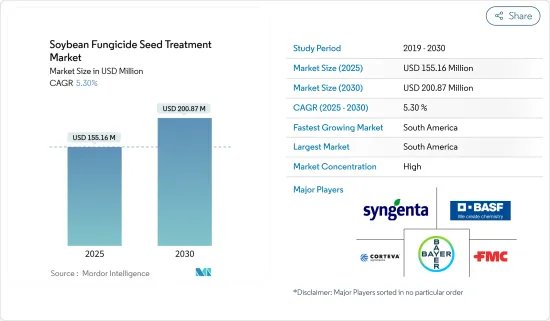

大豆殺菌劑種子處理市場規模預計在 2025 年為 1.5516 億美元,預計到 2030 年將達到 2.0087 億美元,預測期內(2025-2030 年)的複合年成長率為 5.30%。

隨著農民注重保護作物免受真菌疾病的侵害以保持健康的產量,大豆殺菌劑種子處理市場正在擴大。大豆麵臨來自土壤和種子傳播的病原體(如疫黴菌、立枯絲核菌和鐮刀菌)的嚴重風險,這些病原體會影響發芽和植物早期發育。

全球食品、飼料和工業領域的大豆消費量持續增加。大豆為豆腐、豆漿和肉類替代等植物性食品提供必需的蛋白質和脂肪,並且由於健康和永續性的考慮而變得越來越受歡迎。在畜牧業中,豆粕用於家禽、豬和牛的飼料。 2023年全球家牛隻數量將達15.757億頭,高於先前的15.577億頭。生質燃料產業也透過用於生物柴油生產的大豆油增加了需求。人口成長和飲食偏好的變化維持了這種消費成長,進一步推動了大豆殺菌劑處理市場的發展。

先進的殺菌劑配方可以增強對多種病原體的防護。這些處理可以提高幼苗的活力,確保均勻生長,並增強對環境壓力的抵抗力。該行業正在從傳統的化學噴灑轉向有針對性的種子處理,專注於最大限度地提高作物產量,同時降低投入成本和應用複雜性。

大豆殺菌劑和種子處理市場主要由南美洲主導,其中巴西和阿根廷由於大豆產量大而貢獻巨大。北美,尤其是美國,由於潮濕的環境增加了真菌感染的風險,佔據了主要的市場佔有率。由於大豆種植面積增加和種子處理技術的採用,亞太市場正在擴大,尤其是在中國和印度。根據ITC貿易地圖,印度大豆進口量從489,500噸增加至724,900噸。由於大豆需求的增加,預計預測期內大豆殺菌劑種子處理市場將會擴大。

大豆殺菌劑種子處理市場趨勢

生物種子處理劑需求激增

已開發地區的環境問題增加了對生物種子處理的需求,推動了預測期內的市場成長。化學公司正在透過擴大生物種子處理劑的供應來應對這一問題。在美國,各大公司提供經過生物和化學方法處理的大豆種子。根據糧農組織統計資料庫(FAOSTAT),加拿大大豆收穫面積將從2022年的211萬公頃增加到2023年的226萬公頃。

生物種子處理包含活性成分,如活微生物、發酵產物、植物抽取物、植物激素和化合物,以幫助植物生長。這些處理方法越來越受歡迎,因為它們能夠透過最大限度地發揮植物的遺傳潛力來促進植物生長、減少壓力並提高產量。

由於作物消費量的增加和大豆早期種植實踐,美國種子處理市場正在擴大。根據糧農組織統計資料庫 (FAOSTAT) 的數據,2023 年大豆產量將達到 1.133 億噸。早期在潮濕的土壤上種植往往會使種子和幼苗暴露在昆蟲、疾病和害蟲的侵害下,因此需要對種子進行處理以保護種子並提高產量。美國環保署 (EPA)監督化學農藥在農作物和食品中的應用,近年來許多公司已在 EPA 註冊。

越來越多的公司正在進入生物種子處理市場。 2022年,BASF歐洲公司在加拿大註冊了大豆種植的Veltyma殺菌劑。本產品結合了Fluconazole(Revysol)和Pyraclostrobin的植物健康益處以及Metconazole的鐮刀菌控制能力,可提供全面的大豆病害管理。

南美洲佔據市場主導地位

南美洲佔世界大豆產量和出口的大部分,其中巴西和阿根廷是主要貢獻者。根據糧農組織統計,巴西是全球最大的大豆生產國,佔全球產量的40%以上,而阿根廷仍是最大的大豆出口國。該地區廣闊的可耕地、適宜的氣候和現代化的農業方法使其能夠大規模生產大豆,滿足全球對食品、飼料和生質燃料的需求。根據糧農組織統計資料庫 (FAOSTAT) 的數據,大豆產量將從 2022 年的 1.212 億噸增至 2023 年的 1.521 億噸。巴西主要的大豆生產州——馬托格羅索州、巴拉那州和南里奧格蘭德州——佔全國大豆產量的大部分。阿根廷的潘帕斯地區是主要的大豆種植區,擁有完善的農業基礎設施。

南美洲佔據世界大豆出口市場的主導地位,中國是主要進口國。根據ITC貿易地圖,巴西大豆出口量將從2022年的7,890萬噸增加到2023年的1.019億噸,主要供應亞洲、歐洲和北美等市場。儘管產量不如巴西,但阿根廷專門出口豆粕和豆油等加工大豆產品。該地區的港口基礎設施,例如巴西的桑托斯港和阿根廷的羅薩裡奧港,促進了高效的全球分銷。這些出口支持了全球糧食安全和畜牧業生產,特別是在大豆產量有限的地區。

在南美洲,受永續農業和環境意識的推動,對生物基種子處理殺菌劑的需求正在增加。大豆種植者正在與影響作物產量的疫黴菌根腐病、鐮刀菌枯萎病和立枯絲核病等真菌疾病作鬥爭。由於生物基種子處理劑具有環境效益以及對種子發芽和作物早期發育有積極作用,因此傳統化學殺菌劑向生物基種子處理劑的轉變仍在繼續。這些生物殺菌劑利用天然微生物和植物抽取物來控制真菌病原體,同時改善土壤條件,並支持全球永續性努力。南美洲憑藉著強大的生產和出口能力以及生物種子處理殺菌劑等永續農業實踐的日益普及,維持了其市場地位。

大豆殺菌劑種子處理產業概況

全球大豆殺菌劑種子處理市場正在整合,主要企業包括先正達集團、BASF公司、拜耳作物科學公司、科迪華農業科學公司和富美實公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概覽

- 市場促進因素

- 大豆真菌病害發生率不斷上升

- 優質作物產量的需求不斷增加

- 政府支持和舉措

- 市場限制

- 化學種子處理殺菌劑的不良影響

- 農藥的嚴格監管

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 類型

- 化學

- 非化學/生物

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 泰國

- 越南

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 非洲

- 南非

- 其他非洲國家

- 北美洲

第6章競爭格局

- 最受歡迎的策略

- 市場佔有率分析

- 公司簡介

- Syngenta Group

- Bayer CropScience AG

- BASF SE

- UPL

- Corteva Agriscience

- Sumitomo Chemical Co. Ltd

- FMC Corporation

第7章 市場機會與未來趨勢

The Soybean Fungicide Seed Treatment Market size is estimated at USD 155.16 million in 2025, and is expected to reach USD 200.87 million by 2030, at a CAGR of 5.30% during the forecast period (2025-2030).

The soybean fungicide seed treatment market is growing as farmers focus on protecting crops against fungal diseases to maintain healthy yields. Soybeans face significant risks from soil- and seed-borne pathogens including Phytophthora, Rhizoctonia, and Fusarium, which affect germination and early plant development.

Global soybean consumption continues to rise across food, animal feed, and industrial sectors. Soybeans provide essential protein and oil for plant-based foods, including tofu, soy milk, and meat alternatives, which are increasing in popularity due to health and sustainability concerns. The livestock industry depends on soybean meal for feeding poultry, swine, and cattle. The global cattle population reached 1,575.7 million in 2023, up from 1,557.7 million previously. The biofuel industry also increases demand through soybean oil used in biodiesel production. Population growth and changing dietary preferences sustain this consumption growth further driving the soybean fungicide treatment market.

Advanced fungicide formulations provide enhanced protection against multiple pathogens. These treatments improve seedling vigor, ensure uniform growth, and strengthen environmental stress resistance. The industry is moving from traditional chemical applications to targeted seed treatments, focusing on maximizing crop productivity while reducing input costs and application complexity.

South America dominates the soybean fungicide seed treatment market, with Brazil and Argentina as major contributors due to extensive soybean production. North America, particularly the United States, represents a significant market share due to humid conditions that increase fungal infection risks. The Asia-Pacific market is expanding through increased soybean cultivation and seed treatment adoption, particularly in China and India. India's soybean imports increased to 724.9 thousand metric tons from 489.5 thousand metric tons, according to the ITC trade map. The market for soybean fungicide seed treatments is anticipated to expand during the forecast period, driven by increasing soybean demand.

Soybean Fungicide Seed Treatment Market Trends

Rapidating Demand for Biological Seed Treatment

Environmental concerns in developed regions are increasing the demand for biological seed treatments, driving market growth during the forecast period. Chemical companies are responding by expanding their biological seed treatment offerings. In the United States, major companies are providing soybean seeds treated with biological and chemical combinations. According to FAOSTAT, Canada's soybean harvested area increased from 2.11 million hectares in 2022 to 2.26 million hectares in 2023.

Biological seed treatments incorporate active ingredients such as living microbes, fermentation products, plant extracts, phytohormones, and chemical compounds to benefit plant development. These treatments are gaining popularity due to their ability to enhance plant growth, reduce stress, and increase yield by maximizing plant genetic potential.

The United States seed treatment market is expanding due to increased crop consumption and early soybean planting practices. FAOSTAT reports soybean production reached 113.3 million metric tons in 2023. Early planting in moist soils often exposes seeds and seedlings to insects, diseases, and pests, necessitating seed treatment for protection and yield improvement. The US Environmental Protection Agency (EPA) oversees chemical pesticide application on crops and food products, with numerous companies securing EPA registration in recent years.

Companies are increasingly entering the biological seed treatment market. In 2022, BASF SE registered Veltyma Fungicide for Canadian soybean farming. This product combines mefentrifluconazole (Revysol) with pyraclostrobin's plant health benefits and metconazole's Fusarium control capabilities to provide comprehensive soybean disease management.

South America Dominates the Market

South America dominates global soybean production and export, with Brazil and Argentina as major contributors. Brazil, the world's largest soybean producer, accounts for over 40% of global soybean output, while Argentina maintains its position among top exporters according to FAO. The region's extensive arable land, suitable climate, and modern farming practices enable large-scale production to meet global demand for soybeans in food, animal feed, and biofuels. According to FAOSTAT, soybean production increased from 121.2 million metric tons in 2022 to 152.1 million metric tons in 2023. Brazil's main soybean-producing states - Mato Grosso, Parana, and Rio Grande do Sul - constitute a significant portion of national output. Argentina's Pampas region serves as a primary soybean cultivation area, supported by established agricultural infrastructure.

South America controls the global soybean export market, with China as the primary importer. Brazil's soybean exports increased from 78.9 million metric tons in 2022 to 101.9 million metric tons in 2023, according to the ITC Trade map, supplying key markets in Asia, Europe, and North America. Argentina, despite lower production volumes than Brazil, specializes in exporting processed soybean products, including meal and oil. The region's port infrastructure, including Brazil's Santos Port and Argentina's Rosario Port, facilitates efficient global distribution. These exports support worldwide food security and livestock industries, particularly in regions with limited soybean production.

South America experiences increasing demand for bio seed treatment fungicides, driven by sustainable agriculture needs and environmental awareness. Soybean farmers combat fungal diseases including Phytophthora root rot, Fusarium wilt, and Rhizoctonia damping-off, which affect crop yields. The transition from conventional chemical fungicides to bio-based seed treatments continues due to their environmental benefits and positive effects on seed germination and early crop development. These biofungicides utilize natural microbes and plant extracts to control fungal pathogens while improving soil conditions, supporting global sustainability initiatives. South America maintains its market position through strong production and export capabilities, combined with increasing adoption of sustainable farming practices like bio seed treatment fungicides.

Soybean Fungicide Seed Treatment Industry Overview

The global market for soybean fungicide seed treatment is consolidated, with major players such as Syngenta Group, BASF SE, Bayer Crop Science AG, Corteva Agriscience, and FMC Corporation among others. Syngenta International AG occupies the largest market share, followed by BASF SE and Bayer Crop Science AG. Major players in the market have extended their product portfolio and taken the approach of expansion and partnerships to broaden their business and strengthen their position in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Soybean Fungal Diseases

- 4.2.2 Growing Demand for High-Quality Crop Yield

- 4.2.3 Government Support and Initiatives

- 4.3 Market Restraints

- 4.3.1 Adverse Effect of Chemical Seed Treatment Fungicides

- 4.3.2 Stringent Regulations on Agrochemicals

- 4.4 Porter's Five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Chemical

- 5.1.2 Non-Chemical/Biological

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Spain

- 5.2.2.5 Italy

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Thailand

- 5.2.3.5 Vietnam

- 5.2.3.6 Australia

- 5.2.3.7 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Africa

- 5.2.5.1 South Africa

- 5.2.5.2 Rest of Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Syngenta Group

- 6.3.2 Bayer CropScience AG

- 6.3.3 BASF SE

- 6.3.4 UPL

- 6.3.5 Corteva Agriscience

- 6.3.6 Sumitomo Chemical Co. Ltd

- 6.3.7 FMC Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

種子處理市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、功能、作物類型、應用、地區和競爭情況細分,2020-2030 年預測

種子處理市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、功能、作物類型、應用、地區和競爭情況細分,2020-2030 年預測 2025年全球種子加工機械市場報告全球種子處理市場報告(2025年)

2025年全球種子加工機械市場報告全球種子處理市場報告(2025年) 種子處理市場按產品類型、作物類型、配方類型、處理方案、認證、使用環境、最終用戶和分銷管道分類 - 2025-2030 年全球預測

種子處理市場按產品類型、作物類型、配方類型、處理方案、認證、使用環境、最終用戶和分銷管道分類 - 2025-2030 年全球預測 全球種子處理市場(至 2030 年)按類型、應用技術(塗層、敷料、製粒)、功能(種子保護、種子改良)、配方、作物類型(穀物、油籽、水果和蔬菜)和地區分類

全球種子處理市場(至 2030 年)按類型、應用技術(塗層、敷料、製粒)、功能(種子保護、種子改良)、配方、作物類型(穀物、油籽、水果和蔬菜)和地區分類 2032 年小麥種子處理市場預測:按產品、作物類型、製劑類型、功能、應用、最終用戶和地區進行的全球分析

2032 年小麥種子處理市場預測:按產品、作物類型、製劑類型、功能、應用、最終用戶和地區進行的全球分析 亞太種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印度種子處理:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

亞太種子處理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美種子處理市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印度種子處理:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)