|

市場調查報告書

商品編碼

1690924

印度導熱流體:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)India Thermic Fluid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

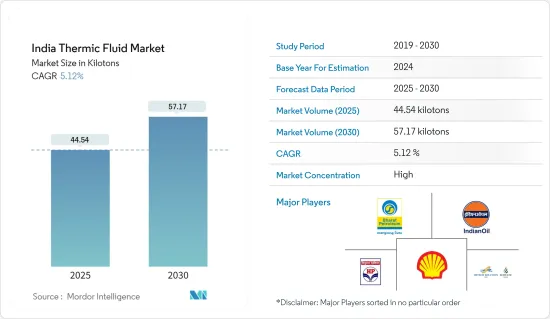

印度導熱油市場規模預計在 2025 年為 44,540 公噸,預計在 2030 年達到 57,170 公噸,預測期內(2025-2030 年)的複合年成長率為 5.12%。

2020 年,因新冠疫情導致全國封鎖,市場遭受重創。它影響了多個終端用戶產業,包括化學品、石油和天然氣。不過,對醫藥業務的需求激增,主要是因為疫情期間對各種藥物的需求增加。儘管如此,該產業在後疫情時代正在恢復速度,預計在預測期內也將如此。

關鍵亮點

- 短期內,石油和天然氣行業的廣泛需求以及聚光型太陽光電的不斷增加的使用預計將推動市場成長。

- 相反,傳熱流體(HTF)帶來的爆炸風險可能會阻礙市場成長。

- 生物基傳熱介質的巨大開發潛力預計將為所研究的市場提供巨大的成長機會。

印度傳熱介質市場趨勢

礦物油領域的需求不斷成長

- 用作傳熱流體的礦物油是從原油蒸餾尾礦獲得的石油基流體。礦物油是石蠟或環烷基本烴的異構混合物,分為石蠟油或環烷油。選擇這些油是因為它們對黏度、傳熱能力和穩定性的影響。

- 石蠟礦物油具有較高的閃點和沸點。另一方面,環烷礦物油具有優異的低溫性能和流點。

- 礦物油在高溫下具有優異的熱穩定性,所需的處理和維護較少,對環境的影響較小。它還具有蒸氣壓和粘度低的特性。

- 根據印度經濟顧問辦公室統計,22會計年度末印度礦物油批發物價指數約126,較前一年的79.2上漲近40%。

- 由於礦物油在汽車、紡織、建築、工業、醫療、製藥、電子和消費品等各領域的廣泛應用,對礦物油的需求不斷增加。在製藥業,它通常用於嬰兒乳液、冷霜、藥膏和化妝品中,以治療和預防皮膚乾燥、皸裂、鱗狀、瘙癢和輕微刺激。此外,它還可以用作動物或人類的溫和瀉藥。

- 印度製藥業預計很快將實現22.4%的複合年成長率。根據印度品牌資產基金會的報告,預計到 2030 年將達到 1,300 億美元。印度22會計年度和21會計年度的藥品和醫藥出口總額分別為246億美元和244.4億美元。這將導致對該行業至關重要的礦物油的需求增加。

- 因此,預計上述策略將在未來幾年對傳熱介質市場產生重大影響。

石油和天然氣領域佔市場主導地位

- 傳熱流體廣泛應用於石油和天然氣加工產業。傳熱流體和系統用於燃料提取、運輸、精製和回收的各個階段。

- 由於石油和天然氣作業主要在偏遠和難以進入的地方進行,因此使用具有高閃點和熱穩定性的傳熱流體對於降低爆炸風險至關重要。傳熱流體用於海上平台加熱設備、再生葡萄糖和分子篩,並有助於去除水分。在煉油廠,它們用於加熱蒸餾石油和石油基產品的塔式再沸器。

- 傳熱流體用於天然氣處理的液相中,進行脫水、萃取、脫硫、分餾,以及控制溫度、維持相態和加熱再沸器。

- 傳熱流體也用於石油管線和泵站,以調節流經管道的石油的黏度。因此,石油和天然氣領域的所有這些應用在推動傳熱介質需求方面發揮著至關重要的作用。

- 印度品牌資產基金會的數據顯示,到 2021 年,印度仍是世界第三大石油消費國。考慮到這一點,原油吞吐量將從 2020-2021 年的 2.2177 億噸增加 9% 至 2021-22 年的 2.417 億噸。印度也計劃在2030年將精製能力提高兩倍,從4.5億噸增加到5億噸。

- 據印度投資局稱,2021-22 年石油產品產量為 2.543 億噸。此外,2023年1月石油精製產量與2022年1月相比成長了4.5%。 2023年1月天然氣產量與2022年1月相比增加了5.3%。

- 印度多家石油和天然氣生產公司已採取重大措施,減少印度對其他國家進口的依賴。例如,印度石油天然氣公司(ONGC)宣布,2023 年 1 月的產量與 2022 年 1 月相比下降了 5.3%,並於 2021 年 11 月宣布打算向其石化業務 ONGC Petro Additions Ltd.(OPaL)投資高達 600 億印度盧比(8 億美元),以幫助該公司滿足其股本。

- 2021 年 9 月,印度石油有限公司 (BPCL) 宣布計劃在未來五年內投資 40.5 億美元,以提高其石化能力和精製效率。

- 此外,2022年8月,BPCL宣布計劃在未來五年內向其石化、城市燃氣和清潔能源業務投資1.4兆印度盧比(176.5億美元)。

- 因此,預計在預測期內,石油和天然氣行業的所有這些趨勢將在推動該國熱流體市場的成長方面發揮關鍵作用。

印度導熱油產業概況

印度導熱油市場已部分整合。市場的主要企業包括印度石油有限公司、殼牌公司、印度石油有限公司、印度斯坦石油有限公司和 Hitech Solution(Generation Four Engitech Ltd)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 石油和天然氣產業的廣泛需求

- 聚光型太陽熱能發電的應用日益廣泛

- 限制因素

- HTF(導熱流體)引起的爆炸危險

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 按類型

- 礦物油

- 矽和芳烴

- 乙二醇

- 其他

- 按最終用戶產業

- 飲食

- 化學品

- 製藥

- 石油和天然氣

- 太陽熱能發電

- 其他

第6章競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Bharat Petroleum Corporation Limited

- Bozzler Energy Pvt Ltd.

- Dow

- Eastman Chemical Company

- Exxon Mobil Corporation

- GS Caltex India

- Hitech Solution(Generation Four Engitech Ltd)

- HP Lubricants

- Indian Oil Corporation Ltd.

- Paras Lubricants Ltd.

- Shell plc

- Savita Oil Technologies Limited

- Tide Water Oil Co. (India) Ltd.

第7章 市場機會與未來趨勢

- 生物基傳熱介質開發潛力大

The India Thermic Fluid Market size is estimated at 44.54 kilotons in 2025, and is expected to reach 57.17 kilotons by 2030, at a CAGR of 5.12% during the forecast period (2025-2030).

Due to the nationwide lockdown caused by COVID-19, the market suffered in 2020. It influenced several end-user industries, including chemicals, oil, gas, etc. However, the pharmaceutical business saw a surge in demand, primarily due to the increased need for various medications during the epidemic. Nonetheless, the industry picked up speed in the post-pandemic era and is anticipated to keep doing so during the forecast period.

Key Highlights

- Over the short term, extensive demand from the oil and gas sector and increasing concentrated solar power usage are expected to drive the market's growth.

- Conversely, the explosion hazards posed by heat thermic fluids (HTFs) will likely hinder the market's growth.

- The high potential for developing bio-based thermic fluids will likely provide a significant growth opportunity for the market studied.

India Thermic Fluid Market Trends

Rising Demand for Mineral Oil Segment

- Mineral oils, employed as a thermic fluid, are petroleum-based fluids derived from crude oil distillation cuttings. Mineral oils are isomeric mixes of paraffin or naphthene-basic hydrocarbons classified as paraffinic or naphthenic. These oils are chosen for their viscosity, influencing heat transfer capabilities and stability.

- Paraffinic mineral oils hold a higher flash point and boiling point. On the other hand, naphthenic mineral oils include better lower temperature characteristics and pour points.

- Mineral oils provide superior thermal stability at high temperatures, need less disposal and maintenance, and include a lower environmental impact. They include features such as low vapor pressure and viscosity as well.

- According to the Office of Economic Adviser of India, the wholesale price index of mineral oil in India at the end of Fiscal Year 2022 was around 126, representing a nearly 40% increase over the previous year's WPI of 79.2.

- The mineral oil demand continues to increase due to its numerous applications in various sectors, including automotive, textile, construction, industrial, medical, pharmaceutical, electronics, and consumer products. In the pharmaceutical industry, it is commonly used in infant lotions, cold creams, ointments, and cosmetics to treat and prevent dry, rough, scaly, itchy skin and mild skin irritations. Additionally, it can be used as a mild laxative for veterinary or human purposes.

- The Indian pharmaceutical industry is predicted to register at a CAGR of 22.4% shortly. According to a report by the India Brand Equity Foundation, it is expected to reach USD 130 billion by 2030. In FY22 and FY21, Indian medication and pharmaceutical exports totaled USD 24.60 billion and USD 24.44 billion, respectively. As a result, the mineral oil demand, which is crucial to the sector, will increase.

- Therefore, the abovementioned tactics are expected to impact the thermic fluid market in the coming years significantly.

Oil and Gas Segment to Dominate the Market

- Heat transfer fluids are widely employed in the oil and gas processing industry. Heat transfer fluids and systems are used in all stages of fuel extraction, transportation, refining, and recycling.

- As the oil and gas business is primarily seen in remote and difficult-to-access locations, employing heat transfer fluids with a high flash point and thermal stability is critical to reducing the explosion risk. Thermic fluids are utilized on offshore platforms for facility heating and regeneration of glycols and molecular sieves, which aids in the water removal from the natural gas generated. These fluids are used in refineries to heat column reboilers, which are used to distill oil and oil-based products.

- Thermic fluids are employed in the liquid phase of natural gas processing for dehydration, extraction, sweetening, and fractionation, which helps control temperature, maintain phase, and heat reboilers.

- Thermic fluids are also used in oil pipelines and pumping stations to adjust the oil's viscosity as it moves through the line. As a result, all of these applications in oil and gas play an essential role in boosting the need for thermic fluids.

- According to the India Brand Equity Foundation, India remained the world's third-largest oil user in 2021. Keeping this in mind, crude oil processing grew by 9% from 221.77 million tons in 2020-21 to 241.7 million tons in 2021-22. India also intends to treble its refining capacity to 450-500 million tons by 2030.

- According to Invest India, the petroleum products production in FY 2021-22 was 254.3 MMT. In addition, petroleum refinery output grew by 4.5% in January 2023 compared to January 2022. Natural gas production increased by 5.3% in January 2023 compared to January 2022.

- Several Indian-based oil and gas-generating enterprises took significant steps to reduce India's reliance on imports from other countries. For example, Oil and Natural Gas Corp. Ltd (ONGC) announced intentions in November 2021 to invest up to INR 6,000 crore (USD 800 million) in its petrochemicals business, ONGC Petro Additions Ltd (OPaL), to assist in meeting its equity requirements.

- In September 2021, Bharat Petroleum Corporation Limited (BPCL) announced plans to invest USD 4.05 billion in improving the petrochemical capacity and refining efficiency over the next five years.

- Moreover, in August 2022, BPCL announced plans to invest INR 1.4 trillion (USD 17.65 billion) in the petrochemical, city gas, and clean energy business over the next five years.

- Hence, all such trends in the oil and gas industry are expected to play an instrumental role in driving the thermic fluid market growth in the country over the forecast period.

India Thermic Fluid Industry Overview

The thermic fluid market in India is partially consolidated in nature. Some of the key players in the market include Bharat Petroleum Corporation Limited, Shell plc, Indian Oil Corporation Ltd, Hindustan Petroleum Corporation Limited, and Hitech Solution (Generation Four Engitech Ltd), among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Extensive Demand from the Oil and Gas Sector

- 4.1.2 Increasing Use in Concentrated Solar Power

- 4.2 Restraints

- 4.2.1 Explosion Hazards Posed By HTFs (Heat Thermic Fluids)

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Volume)

- 5.1 By Type

- 5.1.1 Mineral Oil

- 5.1.2 Silicon And Aromatics

- 5.1.3 Glycols

- 5.1.4 Other Types

- 5.2 By End-user Industry

- 5.2.1 Food and Beverage

- 5.2.2 Chemicals

- 5.2.3 Pharmaceuticals

- 5.2.4 Oil and Gas

- 5.2.5 Concentrated Solar Power

- 5.2.6 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Bharat Petroleum Corporation Limited

- 6.4.2 Bozzler Energy Pvt Ltd.

- 6.4.3 Dow

- 6.4.4 Eastman Chemical Company

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 GS Caltex India

- 6.4.7 Hitech Solution (Generation Four Engitech Ltd)

- 6.4.8 HP Lubricants

- 6.4.9 Indian Oil Corporation Ltd.

- 6.4.10 Paras Lubricants Ltd.

- 6.4.11 Shell plc

- 6.4.12 Savita Oil Technologies Limited

- 6.4.13 Tide Water Oil Co. (India) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 High Potential for the Development of Bio-based Thermic Fluids