|

市場調查報告書

商品編碼

1690878

流體動力設備-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Fluid Power Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

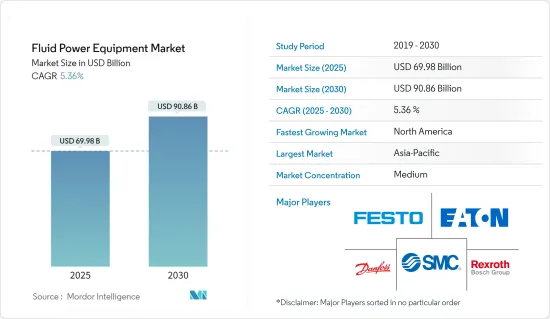

流體動力設備市場規模預計在 2025 年為 699.8 億美元,預計到 2030 年將達到 908.6 億美元,預測期內(2025-2030 年)的複合年成長率為 5.36%。

流體動力設備市場對許多行業至關重要,包括建築、農業、航太、物料輸送以及石油和天然氣。流體動力系統利用液壓和氣壓技術透過加壓流體管理能量,從而廣泛使用泵浦、馬達、汽缸和閥門等設備。這些部件對於需要高精度、高可靠性和高效率的領域至關重要。

油壓設備領先市場

關鍵亮點

- 油壓設備佔據市場主導地位,提供強大而可靠的解決方案,特別適合重型機械和工業應用。油壓缸和閥門等產品廣泛應用於建築和製造等領域,這些領域對高強度和精確控制至關重要。氣動設備的功率較小,但在速度、簡單性和安全性至關重要的行業中更受青睞,例如食品加工和汽車組裝。

技術進步推動需求

關鍵亮點

- 液壓和氣壓系統的技術發展、能源效率法規以及日益成長的自動化趨勢推動了流體動力元件的需求。流體動力技術與工業控制系統的整合正在推動創新,特別是在航太和石油天然氣等領域,因為液壓機械和流體動力控制系統正在改進,以提高效率並減少對環境的影響。

工業自動化的進步刺激了流體動力系統的需求

關鍵亮點

- 提高自動化程度:各行各業正在向自動化轉變,對流體動力設備市場產生了重大影響。液壓和氣壓系統擴大被整合到自動化工業機械中,以提供更高的精度和控制力。這種需求在工廠自動化中尤其強烈,因為高效率的製造流程和降低人事費用是首要任務。

- 液壓馬達和泵浦的擴展:工業泵浦和液壓馬達在物料輸送和航太等領域的應用越來越廣泛。自動化使操作更快、更精確,進一步增加了對提高可靠性和運作效率的流體動力設備創新的需求。

- 工業 4.0 整合:作為工業 4.0 轉型的一部分,流體動力技術正在發展,包括智慧感測器和先進的控制機制。這些可以實現即時監控和調整,從而最大限度地減少停機時間並提高工業油壓設備的性能。

- 汽車和半導體製造中的氣動技術:隨著生產過程變得越來越複雜,汽車和半導體製造等產業越來越依賴流體動力應用。氣動系統因其速度、靈活性和安全性而變得在組裝和機器人技術中不可或缺。

能源效率和環境考量塑造市場格局

關鍵亮點

- 關注能源效率:隨著環境法規變得越來越嚴格,能源效率越來越成為液壓和氣壓系統製造商的重點。這些系統經過重新設計,以最大限度地減少能源消耗和減少排放,並符合全球永續性目標。

- 重新設計的液壓閥和氣缸:液壓閥和氣缸經過大量重新設計,更加節能。流體動力傳動系統採用節能馬達和泵,有助於降低各行業的營業成本和環境影響。

- 建築業和農業領域的應用日益廣泛:節能液壓解決方案在建築業和農業等領域越來越受歡迎,在這些領域,挖土機和曳引機等設備都在惡劣的條件下運作。採用先進的控制系統來最佳化能源使用而不犧牲性能。

- 最佳化的氣動閥門:氣動閥門和致動器經常用於包裝和食品加工等行業,它們經過最佳化以實現節能。這些系統在較低的壓力水平下運行,降低了消費量,同時保持了工業應用的高速和高精度。

流體動力設備市場趨勢

閥門佔據很大市場佔有率

- 閥門佔據了很大的市場。閥門是流體動力系統中必不可少的部件,用於管理各種應用中的流體流動。氣動閥,包括電磁先導閥和空氣先導閥,廣泛應用於汽車和電動工具等行業。 Warren Controls 的 ILEA 2900E 系列電動截止控制閥等創新產品凸顯了閥門耐用性和精度的進步,鞏固了其在流體動力設備市場中的核心地位。

- 智慧閥門技術:智慧閥門技術的出現正在徹底改變工業營運,實現即時監控和控制。新型博世力士樂閥門平台使液壓控制更容易整合到多功能系統中,從而提高效率和客製化。

- 壓力保險閥保險閥透過調節氣動系統中的過壓,對於維護高壓環境中的安全性非常重要。它在建築和汽車等領域的使用凸顯了系統完整性的重要性。林德液壓的模組化閥塊等可客製化解決方案體現了提高流體動力系統適應性和操作靈活性的創新。

- 氣動閥門和工業 4.0:工業 4.0 的影響力日益增強,推動了對氣動閥門的需求,尤其是在智慧製造領域。這些閥門為自動化生產線提供精確的控制。人口成長和水資源管理技術進步等因素也導致流體動力設備市場對流體控制閥的需求不斷增加。

北美強勁成長

- 工業擴張和自動化:由於工業化的快速發展和各個領域的自動化程度提高,北美流體動力設備市場有望顯著成長。汽車、航太和建築等行業都依賴液壓和氣壓系統來實現生產流程的現代化並提高生產效率。日立和沃爾沃北美公司在將液壓系統整合到機器以提高操作能力方面處於領導企業。

- 石油和天然氣產業:北美油壓設備市場在很大程度上受到石油和天然氣產業的推動,高壓系統為流體泵送等任務提供動力。液壓升降機和其他設備對於高效的石油採集過程至關重要。美國天然氣消費量的增加意味著能源生產對液壓系統的需求增加。

- 建築業:在建築業,正在進行的基礎設施計劃正在推動對液壓機械的需求增加。依賴液壓系統的挖土機和起重機等重型機械的需求正在增加。神鋼和洋馬等公司之間的合作正在推動液壓挖土機生產的技術創新,進一步推動北美流體動力設備市場的發展。

- 節能解決方案:永續性是塑造北美流體動力市場的關鍵趨勢。降低成本和減少環境影響的節能系統越來越受歡迎。美國能源局強調了壓縮空氣系統在製造業為動力來源工具和物料輸送的重要性。最近的 FDA 指南也推動了食品加工中採用更清潔、節能的氣動系統,標誌著流體動力創新的持續成長。

流體動力設備產業概況

市場領導:流體動力設備市場呈現半整合狀態,由博世力士樂股份公司、丹佛斯公司和伊頓公司等知名全球參與企業組成。

技術創新:派克漢尼汾公司和 SMC 公司等領先公司依靠液壓和氣壓技術的進步來提高系統效率、永續性和精度。這些公司在全球範圍內營運,提供標準化和自訂的流體動力解決方案,以滿足各種各樣的工業需求。

永續性和數位化整合:未來市場成功的關鍵促進因素包括物聯網和自動化技術的整合,以及對開發永續和節能系統的關注。主要企業需要繼續投資創新和夥伴關係,以在不斷發展的流體動力市場中保持競爭力。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章全球油壓設備市場展望

- 當前市場狀況

- 主要市場促進因素與挑戰

第5章 市場洞察

- 市場促進因素

- 能源效率和環境考量塑造市場格局

- 工業自動化的進步推動了對流體動力系統的需求

- 技術進步推動需求

- 市場問題

第6章市場區隔:全球油壓設備市場

- 依產品類型

- 泵浦

- 馬達

- 閥門

- 圓柱

- 蓄能器和過濾器

- 其他產品類型(變速箱、流體連接器等)

- 按最終用戶產業

- 建造

- 農業

- 物料輸送

- 石油和天然氣

- 航太與國防

- 工具機

- 油壓工具

- 其他行業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 其他

- 供應商市場佔有率分析-油壓設備市場

第7章全球氣動設備市場展望

- 當前市場狀況

- 主要市場促進因素與挑戰

第 8 章市場區隔:全球氣動設備市場

- 依產品類型

- 閥門

- 致動器

- 纖維連接環

- 配件

- 其他

- 按最終用戶產業

- 食品加工和包裝

- 車

- 物料輸送和組裝

- 化工/塑膠/石油

- 半導體電子

- 金工

- 紙張和印刷

- 生命科學

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 其他

- 供應商市場佔有率分析-氣動設備市場

第9章競爭格局

- 公司簡介

- Bosch-Rexroth AG

- Danfoss AS

- Eaton Corporation

- Hydac

- Parker-Hannifin Corporation

- HydraForce Inc.

- Kawasaki Heavy Industries Limited

- Nachi-Fujikoshi Corp.

- Festo AG

- SMC Corporation

- Emerson Electric Co.

- Schlumberger Limited

- IMI Precision Engineering

- Parker Hannifin Corporation

- Ingersoll Rand Inc.

- Flowserve BV(Flowserve Corporation)

- Neles Oyj

- 市場展望 - 氣動設備市場

- 市場展望 -油壓設備市場

The Fluid Power Equipment Market size is estimated at USD 69.98 billion in 2025, and is expected to reach USD 90.86 billion by 2030, at a CAGR of 5.36% during the forecast period (2025-2030).

The fluid power equipment market is pivotal to numerous industries, including construction, agriculture, aerospace, material handling, and oil and gas. Fluid power systems utilize hydraulic and pneumatic technologies to manage energy via pressurized fluids, leading to the widespread use of equipment like pumps, motors, cylinders, and valves. These components are essential for sectors that require high precision, reliability, and efficiency in their operations.

Hydraulic Equipment Leads the Market

Key Highlights

- Hydraulic equipment plays a dominant role in the market, offering powerful and reliable solutions, particularly suited for heavy machinery and industrial applications. Products like hydraulic cylinders and valves are extensively used across sectors such as construction and manufacturing, where high force and precise control are critical. While pneumatic equipment is less powerful, it is preferred in industries such as food processing and automotive assembly, where speed, simplicity, and safety are key considerations.

Technological Advancements Drive Demand

Key Highlights

- Demand for fluid power components is fueled by technological developments in hydraulic and pneumatic systems, energy efficiency regulations, and growing automation trends. Integrating fluid power technology into industrial control systems has led to innovations, particularly in sectors like aerospace and oil and gas, where hydraulic machinery and fluid power control systems are being refined for enhanced efficiency and reduced environmental impact.

Advances in Industrial Automation Fuel Demand for Fluid Power Systems

Key Highlights

- Incased Automationre: The ongoing shift toward automation in various industries is significantly impacting the fluid power equipment market. Hydraulic and pneumatic systems are increasingly integrated into automated industrial machinery, offering superior precision and control. This demand is particularly strong in factory automation, where efficient manufacturing processes and reduced labor costs are prioritized.

- Hydraulic Motors and Pumps Expansion: Industrial pumps and hydraulic motors are gaining wider use in sectors such as material handling and aerospace. Automation enables faster, more precise operations, driving further demand for fluid power equipment innovations that improve reliability and operational efficiency.

- Industry 4.0 Integration: As part of the Industry 4.0 transformation, fluid power technology is evolving to include smart sensors and advanced control mechanisms. These allow real-time monitoring and adjustments, minimizing downtime and enhancing performance in industrial hydraulic machinery.

- Pneumatic Equipment in Automotive and Semiconductor Manufacturing: Industries like automotive and semiconductor manufacturing are increasing their reliance on fluid power applications due to the growing complexity of production processes. Pneumatic systems are becoming essential for assembly lines and robotics, valued for their speed, flexibility, and safety.

Energy Efficiency and Environmental Considerations Shape Market Outlook

Key Highlights

- Energy Efficiency Focus: As environmental regulations become stricter, energy efficiency is a growing concern for manufacturers of hydraulic and pneumatic systems. These systems are being re-engineered to minimize energy consumption and reduce emissions, in line with global sustainability goals.

- Redesign of Hydraulic Valves and Cylinders: Hydraulic valves and cylinders are undergoing significant redesigns to enhance energy efficiency. Fluid power transmission systems are being equipped with energy-efficient motors and pumps, which help to reduce operational costs and environmental impacts across industries.

- Increased Adoption in Construction and Agriculture: Energy-efficient hydraulic solutions are gaining traction in sectors like construction and agriculture, where equipment such as excavators and tractors operate under challenging conditions. Advanced control systems are being introduced to optimize energy use without sacrificing performance.

- Optimized Pneumatic Valves: Pneumatic valves and actuators, frequently used in industries such as packaging and food processing, are being optimized for energy savings. By operating at lower pressure levels, these systems reduce energy consumption while maintaining high-speed and precision in industrial applications.

Fluid Power Equipment Market Trends

Valves Holds a Significant Share in the Market

- Valves Hold a Significant Share in the Market: Valves are essential components in fluid power systems, managing fluid flow in various applications. Pneumatic valves, including solenoid-piloted and air-piloted types, are heavily used in industries such as automotive and power tools. Innovations such as Warren Controls' ILEA 2900E series of electrically actuated globe-control valves highlight advancements in valve durability and precision, reinforcing their central role in the fluid power equipment market.

- Smart Valve Technology: The emergence of smart valve technology is revolutionizing industrial operations, enabling real-time monitoring and control. This is critical in industries like mining and agriculture, where Bosch Rexroth's new valve platform facilitates the integration of hydraulic control into multifunctional systems, improving both efficiency and customization.

- Pressure Relief Valves: Pressure relief valves are critical in maintaining safety in high-pressure environments by regulating excess pressure in pneumatic systems. Their use in sectors like construction and automotive underscores the importance of system integrity. Customizable solutions such as Linde Hydraulics' modular valve block demonstrate innovations that improve adaptability and operational flexibility in fluid power systems.

- Pneumatic Valves and Industry 4.0: The growing influence of Industry 4.0 is driving the demand for pneumatic valves, particularly in smart manufacturing. These valves offer precise control in automated production lines. Factors such as increasing population and advancements in water management technologies are also contributing to the rising demand for fluid control valves in the fluid power equipment market.

North America to Witness Considerable Growth

- Industrial Expansion and Automation: The fluid power equipment market in North America is poised for substantial growth, spurred by rapid industrialization and increased automation across various sectors. Industries like automotive, aerospace, and construction are adopting hydraulic and pneumatic systems to modernize production processes and improve efficiency. Hitachi and Volvo North America are among the leaders in incorporating hydraulic systems into machinery, enhancing operational capabilities.

- Oil and Gas Sector: The hydraulic equipment market in North America is heavily driven by the oil and gas sector, where high-pressure systems power operations like fluid pumping. Hydraulic lifts and other equipment are vital for efficient oil extraction processes. Rising natural gas consumption in the US further signals the growing demand for hydraulic systems in energy production.

- Construction Sector: The construction industry's need for hydraulic machinery is expanding due to ongoing infrastructure projects. Heavy machinery such as excavators and cranes, which rely on hydraulic systems, are seeing increased demand. Partnerships between companies like Kobelco and Yanmar are driving innovations in hydraulic excavator production, further boosting the North American fluid power equipment market.

- Energy-Efficient Solutions: Sustainability is a key trend shaping the fluid power market in North America. Energy-efficient systems that reduce costs and environmental impacts are gaining traction. The US Department of Energy highlights compressed air systems' importance in manufacturing, where they power tools and handle materials. Recent FDA guidelines also drive the adoption of cleaner, energy-efficient pneumatic systems in food processing, indicating continued growth in fluid power innovations.

Fluid Power Equipment Industry Overview

Market Leaders: The fluid power equipment market is semi consolidated, with prominent global players such as Bosch-Rexroth AG, Danfoss AS, and Eaton Corporation commanding significant market share. These companies leverage economies of scale and R&D expertise to maintain their leadership positions.

Technological Innovation: Leading players like Parker-Hannifin Corporation and SMC Corporation emphasize technological advancements in hydraulics and pneumatics to enhance system efficiency, sustainability, and precision. These companies operate globally, offering both standardized and custom fluid power solutions to meet diverse industrial needs.

Sustainability and Digital Integration: Key factors driving future market success include the integration of IoT and automation technologies, as well as a focus on developing sustainable and energy-efficient systems. Leading companies must continue to invest in innovation and partnerships to remain competitive in the evolving fluid power market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 GLOBAL HYDRAULIC EQUIPMENT MARKET OUTLOOK

- 4.1 Current Market Scenario

- 4.2 Key Market Influencers - Market Drivers and Challenges

5 MARKET INSIGHTS

- 5.1 Market Drivers

- 5.1.1 Energy Efficiency and Environmental Considerations Shape Market Outlook

- 5.1.2 Advances in Industrial Automation Fuel Demand for Fluid Power Systems

- 5.1.3 Technological Advancements Drive Demand

- 5.2 Market Challenges

6 MARKET SEGMENTATION - GLOBAL HYDRAULIC EQUIPMENT MARKET

- 6.1 By Product Type

- 6.1.1 Pumps

- 6.1.2 Motors

- 6.1.3 Valves

- 6.1.4 Cylinders

- 6.1.5 Accumulators and Filters

- 6.1.6 Other Product Types (Transmission, Fluid Connectors, etc.)

- 6.2 By End-user Vertical

- 6.2.1 Construction

- 6.2.2 Agriculture

- 6.2.3 Material Handling

- 6.2.4 Oil and Gas

- 6.2.5 Aerospace and Defense

- 6.2.6 Machine Tools

- 6.2.7 Hydraulic Tools

- 6.2.8 Other End-user Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Rest of the World

- 6.4 Vendor Market Share Analysis - Hydraulic Equipment Market

7 GLOBAL PNEUMATIC EQUIPMENT MARKET OUTLOOK

- 7.1 Current Market Scenario

- 7.2 Key Market Influencers - Market Drivers and Challenges

8 MARKET SEGMENTATION - GLOBAL PNEUMATIC EQUIPMENT MARKET

- 8.1 By Product Type

- 8.1.1 Valves

- 8.1.2 Actuators

- 8.1.3 FRLs

- 8.1.4 Fittings

- 8.1.5 Other Product Types

- 8.2 By End-user Vertical

- 8.2.1 Food Processing and Packaging

- 8.2.2 Automotive

- 8.2.3 Material Handling and Assembly

- 8.2.4 Chemicals/Plastics/Oil

- 8.2.5 Semiconductor and Electronics

- 8.2.6 Metalworking

- 8.2.7 Paper and Printing

- 8.2.8 Life Sciences

- 8.2.9 Other End-user Verticals

- 8.3 By Geography

- 8.3.1 North America

- 8.3.2 Europe

- 8.3.3 Asia-Pacific

- 8.3.4 Rest of the World

- 8.4 Vendor Market Share Analysis - Pneumatic Equipment Market

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 Bosch-Rexroth AG

- 9.1.2 Danfoss AS

- 9.1.3 Eaton Corporation

- 9.1.4 Hydac

- 9.1.5 Parker-Hannifin Corporation

- 9.1.6 HydraForce Inc.

- 9.1.7 Kawasaki Heavy Industries Limited

- 9.1.8 Nachi-Fujikoshi Corp.

- 9.1.9 Festo AG

- 9.1.10 SMC Corporation

- 9.1.11 Emerson Electric Co.

- 9.1.12 Schlumberger Limited

- 9.1.13 IMI Precision Engineering

- 9.1.14 Parker Hannifin Corporation

- 9.1.15 Ingersoll Rand Inc.

- 9.1.16 Flowserve BV (Flowserve Corporation)

- 9.1.17 Neles Oyj

- 9.2 Market Outlook - Pneumatic Equipment Market

- 9.3 Market Outlook - Hydraulic Equipment Market

流體動力設備市場:依產品類型、組件類型、壓力等級及最終用戶產業分類-2026-2032年全球市場預測液壓動力系統市場:依產品、系統類型、壓力範圍、流量、應用、終端用戶產業、通路分類,全球預測,2026-2032年

流體動力設備市場:依產品類型、組件類型、壓力等級及最終用戶產業分類-2026-2032年全球市場預測液壓動力系統市場:依產品、系統類型、壓力範圍、流量、應用、終端用戶產業、通路分類,全球預測,2026-2032年 2026年全球氣動和液壓系統市場報告2026年全球流體動力設備市場報告

2026年全球氣動和液壓系統市場報告2026年全球流體動力設備市場報告 流體動力設備市場規模、佔有率和成長分析(按類型、組件、應用和地區分類)-2026-2033年產業預測

流體動力設備市場規模、佔有率和成長分析(按類型、組件、應用和地區分類)-2026-2033年產業預測 全球流體動力設備市場

全球流體動力設備市場 流體動力設備市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、應用、地區和競爭細分,2020-2030 年)

流體動力設備市場-全球產業規模、佔有率、趨勢、機會及預測(按組件、應用、地區和競爭細分,2020-2030 年) 全球流體動力設備的成長機會

全球流體動力設備的成長機會