|

市場調查報告書

商品編碼

1690859

電動汽車電池管理系統:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Electric Vehicle Battery Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

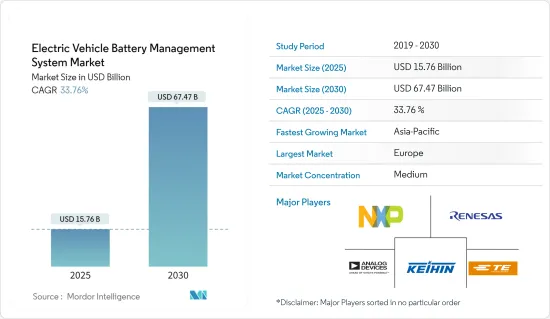

電動車電池管理系統市場規模預計在 2025 年為 157.6 億美元,預計到 2030 年將達到 674.7 億美元,預測期內(2025-2030 年)的複合年成長率為 33.76%。

儘管新冠疫情對全球汽車產業產生了負面影響,但2020年全球電動車銷量仍呈現顯著成長。這主要得益於政府補貼、電動車充電基礎設施的擴建以及燃料價格的上漲。預計 2021 年將出現類似的成長趨勢,並將在整個預測期內持續下去。疫情擾亂了全球供應鏈,導致BMS組件和系統的生產和交付出現延遲和短缺。同時,疫情加速了電動車的普及,推動了對 BMS 技術的需求。整體而言,疫情對BMS產業的長期影響可能是正面的。

從中期來看,對永續交通和清潔能源的需求不斷成長,推動了對電池式電動車的需求。消費者面臨的限制因素包括車輛行駛里程、較高的初始價格、有限的車型供應以及缺乏知識等,正在透過促銷活動和政府法規予以解決。這些變數影響電動車的需求並推動電池管理系統市場的發展。

由於電動車的普及,全球整體對電池管理系統 (BMS) 的需求預計將快速成長。然而,由於亞太地區工業化和都市化的快速發展,以及中國和印度等國家對電動車的需求不斷增加,預計 BMS 市場將由亞太地區主導。預計北美和歐洲等其他地區的 BMS 市場也將顯著成長。

電動車需求的不斷成長將推動電池化學和材料技術的進步,需要更先進、更有效率的BMS來確保電池的安全和性能。

電動車電池管理系統市場趨勢

電動車領域預計將佔據市場主導地位

世界各國政府都在積極實施鼓勵使用電動車的政策。中國、印度、法國和英國已宣布計劃在 2040 年前逐步淘汰汽油和柴油汽車。隨著電動車需求的增加,對電池管理系統的需求也預計將逐步增加。

電動車正在全球逐漸普及,因此貨運公司也將現有車輛改裝為電力驅動車輛。OEM正在重新定義他們的電動車藍圖。這可能會對目標市場的成長產生正面影響。例如

- 2022 年 12 月,專注於為商用車隊市場製造電動輕型皮卡的公司 Lordstown Motors 宣布,將在 CES 上 Mobility in Harmony (MIH) 聯盟西廳 5274 號展位展示其全尺寸 BEV 皮卡 Endurance。

- 2022年12月,洛杉磯世界機場(LAWA)宣布其首輛 Nikola Tre 大型電池電動車到來,標誌著該機場向全電動汽車過渡的重要一步。

電動車的成長趨勢預計也將推動未來市場的成長。比亞迪、Proterra、塔塔和沃爾沃等知名公司正嘗試在全部區域實現產品在地化,以減少對其他參與者和進口產品的依賴。例如

- 2022 年 12 月,沃爾沃汽車馬來西亞 (VCM) 推出了 C40 Recharge,這是該公司繼 XC40 Recharge Pure Electric 之後的第二款 BEV 車型。 C40 是剪切機南工廠生產的本地組裝(CKD) 車型,將享受政府的 CKD EV 激勵措施,直至 2025 年 12 月 31 日。

- 2022 年 12 月,豐田馬達歐洲公司 (TME) 推出了豐田 bZ 緊湊型 SUV 概念車,這是一款由法國豐田歐洲設計與開發中心 (ED2) 在歐洲設計的全電池電動車。

監管機構正在實施嚴格的規定以減少燃料排放並提高道路安全。此外,預測期內,消費者對碳排放和能源永續運輸的傾向可能會成為市場滲透的潛在機會。

預計歐洲將佔很大市場佔有率

在電動車推廣計畫方面,德國目前正在實施符合更嚴格排放標準的策略。聯邦政府的氣候保護計畫旨在主要透過交通創新實現 2030 年的氣候目標,其中重點在於電動車。為了推廣清潔汽車,該國推出了購買補貼、所有權稅和公司汽車稅等獎勵和投資。

減輕重量是電動車和產品設計的首要任務。很少有公司設計整合兩個或多個部件以減輕重量的緊湊型模組。例如

海拉於 2021 年 4 月推出了 Power Pack 48 Volt。它將電力電子和電池管理整合在一個產品中,每公里可節省 5-6 克二氧化碳。該解決方案由海拉與中國電池製造商共同開發,並計劃於 2024 年在上海投入大量生產。

各國政府也推出了更多支持性政策來支持該行業的發展,包括投資基礎設施、採取廣泛措施鼓勵人們使用現代低排放和零排放氣體汽車,以及提供長期購買激勵措施來幫助電動車佔據更大的市場佔有率。預計這將在預測期內增強電動車電池管理系統的市場前景。

- 2023 年 1 月中國汽車製造商比亞迪將於本季開始在英國銷售汽車,英國電動車的市場佔有率正在持續成長。該汽車製造商由沃倫·巴菲特的伯克希爾哈撒韋公司支持,它表示其在英國擁有四家經銷商合作夥伴:Pendragon、Arnold Clark、Lookers 和 LSH。

- 2021年6月,義法半導體宣布與Arrival合作,提供Arrival的汽車半導體技術和產品,包括汽車微控制器以及電源和電池管理設備。 Arrival 已選擇 ST 作為將連網電動車推向市場的關鍵合作夥伴之一。 Arrival 已採用 ST 的安全汽車微控制器作為其模組化 ECU 平台,以及其他 ST 技術,包括智慧電源和電池管理設備。

為了減輕車輛重量,各公司正在開發配備電池管理系統的新型電池模組。例如

2021年6月,Leclanche SA宣布開發出名為M3的新一代鋰離子電池模組。它包含一個功能安全的從屬電池管理系統 (BMS) 單元,該單元與功能安全的主電池管理系統單元通訊。

考慮到這些因素,預計在預測期內對電動車電池管理系統的需求將保持處於正向狀態。

電動汽車電池管理系統產業概況

電動車電池管理系統市場由瑞薩電子株式會社、恩智浦半導體公司、京濱株式會社、泰科電子、ADI 公司等主要企業主導。此外,該市場對新參與企業非常有吸引力,在市場上營運的公司專注於引進先進技術以獲得競爭優勢。例如

- 2022 年 5 月,博格華納公司宣布已贏得一家未公開的國際汽車製造商的契約,為該公司供應電池管理系統 (BMS)。博格華納的BMS技術提升了電池組的效能、安全性和使用壽命。

- 2022 年 1 月,FPT Industrial 推出了兩款配備根據客戶需求量身定做的電池管理系統的電軸和電池組。該公司展出了專為 Nikola Tre 設計的整合式電橋。雙馬達軸適用於總重量不超過 44 噸的車輛,可確保高性能和高效率,每個馬達的最大功率為 420kW,最大扭力為 900Nm。

- 2021 年 10 月,Ballard Power Systems 和 Forsee Power 宣布已簽署一份合作備忘錄,建立戰略夥伴關係關係,開發完全整合的燃料電池和電池解決方案,該解決方案針對大規模氫動力應用的性能、成本和可安裝性進行了最佳化。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 市場限制

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場區隔

- 按組件

- 積體電路

- 截止 FET 和 FET 驅動器

- 溫度感測器

- 電量計/電流測量裝置

- 微型電腦

- 其他組件

- 依推進類型

- 純電動車

- 油電混合車

- 按車型

- 搭乘用車

- 商用車

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東和非洲地區

- 北美洲

第6章 競爭格局

- 供應商市場佔有率

- 公司簡介

- Infineon Technologies AG

- Silicon Laboratories

- NXP Semiconductors

- Vitesco Technologies

- TE Connectivity

- Renesas Electronics Corporation

- Keihin Corporation

- Texas Instruments Incorporated

- Analog Devices Inc.

- Visteon Corporation

第7章 市場機會與未來趨勢

The Electric Vehicle Battery Management System Market size is estimated at USD 15.76 billion in 2025, and is expected to reach USD 67.47 billion by 2030, at a CAGR of 33.76% during the forecast period (2025-2030).

Despite the negative COVID-19 impact on the global automotive industry, electric vehicle sales for the year 2020 witnessed significant growth worldwide. This was primarily attributed to government subsidies, expanding electric vehicle charging infrastructure, and a rise in fuel prices. The same growth trend was witnessed for 2021 and will likely continue during the forecast period. The pandemic has disrupted global supply chains, causing delays and shortages in the production and delivery of BMS components and systems. On the other hand, the pandemic has also accelerated the adoption of electric vehicles, which has driven the demand for BMS technology. Overall, the long-term impact of the pandemic on the BMS industry is likely to be positive.

Over the medium term, rising demand for sustainable transportation and cleaner energy has engaged the demand for battery electric vehicles. Consumer constraints such as vehicle range, greater upfront prices, limited model availability, and lack of knowledge are being solved by promotional activities and government legislation. These variables will have an impact on the demand for electric vehicles, which will drive the battery management system market.

The demand for battery management systems (BMS) is expected to grow rapidly across the globe, driven by the increasing adoption of electric vehicles. However, Asia Pacific is expected to lead the market for BMS due to the rapid industrialization and urbanization in the region, as well as the increasing demand for electric vehicles in countries such as China and India. Other regions, such as North America and Europe, are also expected to experience significant growth in the BMS market.

The growing demand for electric vehicles will lead to technological advancements in battery chemistry and materials, which will require more sophisticated and efficient BMS to ensure the safety and performance of batteries.

Battery Management System for Electric Vehicle Market Trends

Battery Electric Vehicle Segment Anticipated to Dominate the Market

Governments around the world have been proactive in enacting policies to encourage the adoption of electric vehicles. China, India, France, and the United Kingdom have announced plans to phase out petrol and diesel vehicles before 2040 completely. As the demand for EVs increases, the demand for battery management systems will also increase gradually.

Electric mobility is gradually growing around the world, owing to which the goods transportation companies are also converting their existing fleets into electric propulsion-based vehicles. OEM is redefining its roadmap for electric vehicles. This will positively impact the target market growth. For instance,

- In December 2022, Lordstown Motors Corp., which focuses on building electric light-duty pickup trucks for the commercial fleet market, announced that the Endurance full-size BEV pickup truck will be on display at CES in the West Hall Booth 5274 of the Mobility in Harmony (MIH) Consortium.

- In December 2022, Los Angeles World Airports (LAWA) announced the arrival of its first Nikola Tre heavy-duty battery-electric vehicle, a significant step forward in the airport's transition to a fully electric fleet.

The increase in the trend of electric vehicles is also expected to drive market growth in the future. Prominent companies such as BYD, Proterra, Tata, Volvo, and others are trying to localize their products across the regions they operate to reduce the dependence on other players and imports. For instance,

- In December 2022, Volvo Car Malaysia (VCM) unveiled the C40 Recharge, the company's second BEV model after the XC40 Recharge Pure Electric. The C40, as a locally assembled (CKD) model from Volvo's Shah Alam plant, will also benefit from the government's CKD EV incentives until December 31, 2025.

- In December 2022, Toyota Motor Europe (TMEs unveiled the Toyota bZ Compact SUV Concept, a full-battery-electric vehicle designed in Europe by Toyota European Design and Development (ED2) in France.

Regulatory bodies have laid down stringent regulations about bringing down fuel emissions and increasing road safety. Furthermore, Consumer inclination toward carbon emission and energy-sustainable transportation will provide potential opportunities for target market penetration over the forecast period.

Europe Expected to Hold Significant Share in the Market

In terms of pro-electric plans, Germany is now implementing strategies to meet stricter emission standards. The federal government's climate protection program, which aims to meet its 2030 climate targets primarily through transportation innovation, places a premium on electric mobility. To promote clean cars, the country is introducing incentives and investments such as a purchase grant, ownership tax, and company car tax.

Weight reduction is a top priority in the design of electric vehicles and products. Few companies are designing compact modules integrating two or more components to save weight. For example,

Hella's introduced the PowerPack 48 Volt in April 2021, which combines power electronics and battery management in one product and saves 5 to 6 grams of CO2 per kilometer driven. This solution, which HELLA is developing in collaboration with a Chinese cell manufacturer, is set to enter series production in Shanghai in 2024.

The government is also aiding the industry growth with more supportive policies: investment in infrastructure; broader measures to encourage uptake of the latest, low and zero-emission cars; and long-term purchase incentives to help the country grow its share in the EV market. This is expected to bolster the market prospects for battery management systems for EVs during the forecast period.

- In January 2023, BYD, a Chinese automaker, began selling vehicles in the United Kingdom this quarter, where electric vehicles are gaining market share. According to the automaker, backed by Warren Buffett's Berkshire Hathaway, it has appointed four UK dealer partners in Pendragon, Arnold Clark, Lookers, and LSH.BYD's first model will be the Atto 3 SUV, and more dealer partners and pricing will be announced in the coming weeks.

- In June 2021, STMicroelectronics announced its collaboration with Arrival to provide semiconductor technologies and products for Arrival's vehicles, including automotive microcontrollers and power and battery-management devices. Arrival has chosen ST as one of its key partners in bringing its connected Evs to market. Arrival has selected ST's secure automotive microcontrollers for their modular ECU platform, as well as other ST technologies, including smart-power and battery-management devices.

Although companies are developing new battery modules with a battery management system to reduce the weight of the vehicles. For instance,

In June 2021, Leclanche SA announced that it had developed a new generation of lithium-ion battery modules called M3; it is fitted with a functionally safe slave battery management system (BMS) unit which communicates with a functionally safe master battery management system unit.

Considering these factors demand for Electric Vehicle Battery Management Systems is anticipated to remain on the positive side of the graph during the forecast period.

Battery Management System for Electric Vehicle Industry Overview

The Electric Vehicle Battery Management System Market is dominated by several key players such as Renesas Electronics Corporation, NXP Semiconductors, Keihin Corporation, TE Connectivity, Analog Devices Inc., and others. Moreover, the market tends to be highly attractive for new players, and companies operating in the market have been focusing on launching advanced technologies to gain a competitive advantage. For instance,

- In May 2022, BorgWarner Inc. announced that the company had got a deal from an undisclosed international vehicle manufacturer to supply its Battery Management System (BMS). Model years beginning in the middle of 2023 will be the first to come with the new BorgWarner BMS technology, which improves the performance, security, and lifespan of battery packs.

- In January 2022, FPT Industrial announced presenting two e-axles and a battery pack with a Battery Management System customized to meet customer needs. It displayed an integrated e-Axle designed for the Nikola Tre. A dual-electric motor axle for GVW vehicles up to 44 tons guarantees high performance and efficiency with a maximum power of 420 kW and a maximum torque of 900 Nm for each motor.

- In October 2021, Ballard Power Systems and Forsee Power announced signing a memorandum of understanding (MOU) for a strategic partnership to develop fully integrated fuel cell and battery solutions optimized for performance, cost, and installation for heavy-duty hydrogen mobility applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD Million)

- 5.1 By Components

- 5.1.1 Integrated Circuits

- 5.1.2 Cutoff FETs and FET Driver

- 5.1.3 Temperature Sensor

- 5.1.4 Fuel Gauge/Current Measurement Devices

- 5.1.5 Microcontroller

- 5.1.6 Other Components

- 5.2 By Propulsion Type

- 5.2.1 Battery Electric Vehicles

- 5.2.2 Hybrid Electric Vehicles

- 5.3 By Vehicle Type

- 5.3.1 Passenger Car

- 5.3.2 Commercial Vehicles

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Infineon Technologies AG

- 6.2.2 Silicon Laboratories

- 6.2.3 NXP Semiconductors

- 6.2.4 Vitesco Technologies

- 6.2.5 TE Connectivity

- 6.2.6 Renesas Electronics Corporation

- 6.2.7 Keihin Corporation

- 6.2.8 Texas Instruments Incorporated

- 6.2.9 Analog Devices Inc.

- 6.2.10 Visteon Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年全球電池性能保障市場報告

2025年全球電池性能保障市場報告 電動汽車電池管理晶片市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

電動汽車電池管理晶片市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 電動車電池自動化市場預測至2032年:按組件、工藝、電池類型、應用、最終用戶和地區分類的全球分析2032 年電動車電池回收再利用市場預測:按電池化學成分、回收流程、應用、最終用戶和地區進行的全球分析

電動車電池自動化市場預測至2032年:按組件、工藝、電池類型、應用、最終用戶和地區分類的全球分析2032 年電動車電池回收再利用市場預測:按電池化學成分、回收流程、應用、最終用戶和地區進行的全球分析 全球電動汽車電池測試市場

全球電動汽車電池測試市場 電動車電池管理系統市場(按組件、拓撲、電壓、電池類型、電池配置、充電模式和應用)- 2025-2030 年全球預測2025年全球電動車電池管理系統市場報告

電動車電池管理系統市場(按組件、拓撲、電壓、電池類型、電池配置、充電模式和應用)- 2025-2030 年全球預測2025年全球電動車電池管理系統市場報告 歐洲電動車電池管理系統:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

歐洲電動車電池管理系統:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年) 全球電動汽車電池測試與診斷服務業(2025-2034)

全球電動汽車電池測試與診斷服務業(2025-2034) 全球電動車電池測試市場:按電動車類型、按外形規格、按推進力、按電池技術、按化學、按採購類型、按測試類型、按地區 - 預測到 2030 年

全球電動車電池測試市場:按電動車類型、按外形規格、按推進力、按電池技術、按化學、按採購類型、按測試類型、按地區 - 預測到 2030 年