|

市場調查報告書

商品編碼

1940724

諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Consulting Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

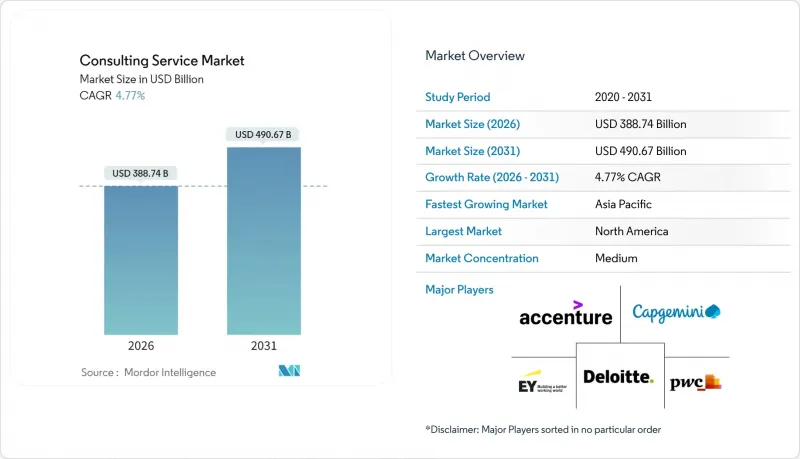

諮詢服務市場預計將從 2025 年的 3,710.4 億美元成長到 2026 年的 3,887.4 億美元,預計到 2031 年將達到 4906.7 億美元,2026 年至 2031 年的複合年成長率為 4.77%。

市場的穩定成長反映了諮詢服務模式從傳統諮詢服務轉向技術賦能、成果導向模式的重大轉變。董事會層級對數位轉型的迫切需求、監管機構對環境、社會和管治(ESG) 績效日益嚴格的審查以及不斷成長的網路風險,正推動企業將支出轉向高價值諮詢服務。大型公司正透過收購來拓展自身能力,以彌補在人工智慧 (AI)、雲端遷移和能源轉型等領域的專業知識缺口。同時,專業顧問公司憑藉其深厚的專業知識和敏捷的交付能力贏得了許多專案。結合現場和虛擬交付的混合模式正逐漸成為常態,使企業能夠獲得全球人才、降低計劃成本並減少與差旅相關的碳排放。競爭優勢的實現依賴於專有平台、數據驅動的調查方法以及將報酬與可衡量的客戶成果掛鉤的、可驗證的影響指標。

全球諮詢服務市場趨勢與洞察

加速數位轉型

企業正將多年期的現代化專案壓縮成更短的周期,這增加了對能夠大規模整合雲端遷移、資料現代化和大規模分析的諮詢顧問的需求。產業專用的雲端解決方案支援針對特定產業的客製化服務,迫使諮詢顧問將流程重塑與技術實施結合。醫療服務提供者正在部署遠端醫療生態系統,製造商正在整合感測器進行預測性維護,金融機構正在推出即時付款基礎。顧問公司也積極回應,提供涵蓋架構設計、資料遷移和合規性調整的產業專用的雲端服務,將自身定位從純粹的策略顧問轉變為執行合作夥伴。這種轉變將在初始轉型階段之後,透過託管服務帶來長期經常性收入。

疫情後更加重視營運效率

成本控制仍然是董事會的首要任務,因為供給側通膨和工資壓力導致利潤率承壓。企業要求諮詢專案能夠提供可量化的投資報酬率,這推動了與產能提升、自動化程度提高和營運資金釋放掛鉤的績效付費模式的普及。越來越多的顧問專案圍繞著流程挖掘、智慧自動化和混合型員工隊伍的精實重組。諮詢顧問會引入績效儀表板,即時追蹤關鍵績效指標,從而確保透明度並加快決策速度。這種對結果的關注使諮詢公司成為價值創造的合作夥伴,而非可有可無的支出項目,從而提升了其在注重成本的客戶中的佔有率。

降低客戶成本並提升內部能力

出於經濟審慎的考慮,企業將外部支出重新分配到策略缺口,而日常諮詢職能則擴大被內部專家中心所承擔。選擇性採購策略強調價值獲取,迫使諮詢顧問透過專有工具、產業標竿和結果保證來脫穎而出。同時,企業也開始提供協作式採購模式,將顧問顧問嵌入客戶團隊,加速知識轉移和能力成熟,在預算限制下保留業務機會。

細分市場分析

到2025年,營運諮詢將佔諮詢服務市場佔有率的28.94%,這印證了製造業、零售業和能源產業對流程最佳化的持續需求。隨著企業尋求人工智慧管治、雲端轉型和網路彈性方面的專業知識,技術諮詢正以6.29%的複合年成長率快速成長。市場受益於技術與傳統管理諮詢的整合,促使企業投資涵蓋策略制定、實施和託管服務的端到端能力。技術諮詢專案擴大將雲端遷移藍圖和資料現代化藍圖相結合。企業正在整合專有加速器以縮短時間、降低風險,並透過託管雲端營運創造經常性收入。營運諮詢透過將數位雙胞胎、流程挖掘分析和機器人流程自動化融入其傳統的精實工具包,保持了其重要性。營運和技術職能之間的交叉銷售正在推動客戶總支出佔有率的成長,這標誌著諮詢服務市場正向整合轉型解決方案轉變。

醫療保健和生命科學領域預計將超越其他垂直產業,以6.63%的複合年成長率成長,這主要得益於數位療法、遠端患者監護和人工智慧輔助藥物研發等技術正在改變商業模式。到2025年,銀行、金融和保險(BFSI)產業將佔諮詢服務市場規模的22.10%,反映出對網路安全措施、監理合規和核心銀行體系現代化計劃的持續需求。能源和公共產業領域的諮詢機會主要集中在脫碳策略、電網現代化和氫能生態系統規劃方面,凸顯了該行業對多學科諮詢的日益依賴。

資料隱私法規的加強、以患者為中心的醫療模式以及不斷變化的報銷機制正在推動醫療保健諮詢行業的發展。各公司正將監管方面的專業知識與技術實施方面的支援相結合,指導醫療服務提供者完成電子健康記錄升級和基於雲端的臨床試驗平台部署。在金融服務領域,對即時支付系統、數位身分和環境風險壓力測試的需求日益成長。 ESG(環境、社會和治理)揭露規則與資料管治標準的整合正在創造跨產業的協同效應,並擴大市場覆蓋範圍。

區域分析

北美地區預計到2025年將佔全球收入的40.62%,這得益於高技術普及率、聯邦政府對網路安全的大力投入以及嚴格的金融服務監管。美國企業正利用諮詢服務來制定人工智慧管治框架、零信任架構實施方案以及環境、社會和治理(ESG)合規藍圖。加拿大則憑藉其資源豐富的經濟優勢,透過試點碳捕獲和氫能項目,在能源轉型諮詢領域中打造自己獨特的市場定位。日益嚴格的氣候變遷相關資訊揭露要求將持續支撐兩國對諮詢服務的長期需求。

亞太地區是成長最快的地區,預計到2031年將以6.92%的複合年成長率成長,這主要得益於大規模數位基礎設施計劃、電子政府舉措以及可再生能源的擴張。中國在供應鏈最佳化和消費銀行業務數位化方面對人工智慧的應用將支撐該地區的需求。日本對工業機器人的重視以及新加坡作為金融服務創新中心的地位,為專業顧問公司創造了肥沃的土壤。在印度,醫療數位化、製造自動化和智慧城市規劃的整合正在增強該地區諮詢服務市場的發展勢頭。

在能源轉型、資料隱私法規和永續性等因素的推動下,歐洲保持穩定成長。 《企業永續性報告指令》(CSRD)要求企業尋找能夠滿足嚴格的報告時間表和保證標準的顧問。德國和法國正致力於透過工業4.0提高生產力,而北歐國家則在循環經濟戰略方面走在前列,推動了對創新營運模式的需求。中東和非洲地區正利用多元化政策和大型基礎設施計劃來吸引全球諮詢專家。同時,南美洲的自然資源生產國需要製定環境、社會和治理(ESG)以及營運效率藍圖,以保持其全球競爭力。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 主流趨勢—加速數位轉型

- 主流趨勢-疫情後更加重視營運效率

- 主流趨勢-ESG和風險管理領域監管複雜性的演變

- 主流趨勢—雲端運算和網路安全的快速普及

- 一個被忽視的領域:對生成式人工智慧管治的諮詢需求

- 一個鮮為人知的趨勢:董事會層級施壓要求對範圍 3 價值鏈進行脫碳

- 市場限制

- 主流-降低客戶成本並建立內部能力

- 主流觀點-人才短缺和薪資上漲

- 一個鮮為人知的趨勢:旅行計劃的碳足跡審查力度加大

- 一個鮮為人知的問題:供應商對專有諮詢資產的鎖定擔憂

- 產業價值鏈分析

- 監管環境

- 技術展望

- 工業4.0和數位轉型實踐的影響

- 產業生態系分析

- 主要區域的特色

- 管理諮詢中常見的經營模式

- 波特五力分析

- 買方的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按服務類型

- 營運諮詢

- 策略諮詢

- 財務諮詢

- 技術諮詢

- 人力資本諮詢

- 風險與合規諮詢

- 其他服務類型

- 按客戶產業

- BFSI

- 醫療保健和生命科學

- 能源與公共產業

- 製造業和汽車業

- 資訊與通訊科技與媒體

- 公共部門

- 消費品和零售

- 其他行業

- 按規定表格

- 現場諮詢

- 遠端/虛擬諮詢

- 混合諮詢

- 按公司規模

- 主要企業

- 小型企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 南美洲

- 巴西

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 亞太地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 非洲

- 南非

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deloitte Touche Tohmatsu Limited

- Accenture plc

- PricewaterhouseCoopers LLP

- Ernst & Young Global Limited

- KPMG International Cooperative

- Capgemini SE

- McKinsey & Company, Inc.

- Boston Consulting Group, Inc.

- Bain & Company, Inc.

- Roland Berger Holding GmbH & Co. KGaA

- AT Kearney, Inc.

- Simon-Kucher & Partners Strategy & Marketing Consultants GmbH

- OC&C Strategy Consultants LLP

- Gartner, Inc.

- Tata Consultancy Services Limited

- IBM Consulting(International Business Machines Corporation)

- Booz Allen Hamilton Holding Corporation

- CGI Inc.

- Infosys Consulting(Infosys Limited)

- Oliver Wyman Group(Marsh McLennan)

第7章 市場機會與未來展望

The Consulting Service market is expected to grow from USD 371.04 billion in 2025 to USD 388.74 billion in 2026 and is forecast to reach USD 490.67 billion by 2031 at 4.77% CAGR over 2026-2031.

The market's stable expansion reflects a decisive pivot from traditional advisory toward technology-enabled, outcome-oriented engagement models. Board-level urgency around digital transformation, heightened regulatory scrutiny on environmental, social, and governance (ESG) performance, and intensifying cyber risk are funneling enterprise spending toward high-value consulting offerings. Large firms are broadening capability sets through acquisitions that plug expertise gaps in artificial intelligence (AI), cloud migration, and energy transition, while boutique specialists win mandates by offering deep domain knowledge and agile delivery. Hybrid engagement models that combine on-site and virtual delivery are normalizing, allowing firms to access global talent, lower project costs, and reduce travel-related carbon footprints. Competitive differentiation hinges on proprietary platforms, data-driven methodologies, and demonstrable impact metrics that tie fees to measurable client outcomes.

Global Consulting Service Market Trends and Insights

Accelerating Digital-Transformation Mandates

Enterprises are compressing multi-year modernization programs into shorter cycles, driving premium demand for consultants who can orchestrate cloud migration, data modernization, and advanced analytics at scale. Industry-specific cloud solutions allow sector customization, prompting consultants to blend process redesign with technology implementation. Healthcare providers are deploying telehealth ecosystems, manufacturers are embedding sensors for predictive maintenance, and financial institutions are rolling out real-time payment rails. Consulting firms respond with dedicated industry-cloud practices that cover architecture design, data migration, and compliance alignment, repositioning themselves as execution partners rather than purely strategic advisors. The shift elevates long-term annuity revenue from managed services that follow the initial transformation phase.

Heightened Post-Pandemic Operational-Efficiency Focus

Cost containment remains a board priority as supply-side inflation and wage pressure erode margins. Organizations demand quantifiable return-on-investment from consulting engagements, spurring outcome-based fee models tied to throughput gains, automation intensity or working-capital release. Assignments increasingly revolve around process mining, intelligent automation and lean restructuring of hybrid workforces. Consultants embed performance dashboards that track key performance indicators in real time, ensuring transparency and accelerating decision-making. This results-oriented mindset cements consulting firms as value-creation partners rather than discretionary spend items, strengthening wallet share among cost-conscious clients.

Client Cost-Cutting and In-House Capability Build

Economic caution is prompting enterprises to rebalance external spend toward strategic gaps only, while internal centers of excellence absorb routine advisory functions. Selective sourcing strategies emphasize value capture, pushing consultants to differentiate through proprietary tools, industry benchmarks and outcome guarantees. Simultaneously, firms offer co-sourcing models that embed consultants within client teams to transfer knowledge and speed capability maturation, preserving engagement opportunities despite budget restraint.

Other drivers and restraints analyzed in the detailed report include:

- Growing Regulatory Complexity in ESG and Risk

- Demand for Advisory on Gen-AI Governance

- Talent Scarcity and Wage Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Operations consulting captured 28.94% of the consulting service market share in 2025, underscoring persistent demand for process optimization across manufacturing, retail, and energy sectors. Technology Advisory is expanding at a 6.29% CAGR as enterprises seek expertise in AI governance, cloud transformation, and cyber-resilience. The market benefits from the convergence of technology and traditional management advisory, prompting firms to invest in end-to-end capabilities spanning strategy, implementation, and managed services.Technology Advisory engagements increasingly bundle cloud-migration road maps with cybersecurity safeguards and data-modernization blueprints. Firms integrate proprietary accelerators to compress timelines and lower risk, creating annuity revenue through managed cloud operations. Operations consulting remains relevant by embedding digital twins, process-mining analytics, and robotic process automation into classic lean toolkits. Cross-selling between Operations and Technology practices deepens wallet share and exemplifies the consulting service market's shift toward integrated transformation solutions.

The Healthcare and Life Sciences segment is forecast to post a 6.63% CAGR, outpacing all other verticals as digital therapeutics, remote patient monitoring, and AI-assisted drug discovery reshape operating models. BFSI retained 22.10% of the consulting service market size in 2025, reflecting sustained cybersecurity, regulatory compliance, and core-bank modernization projects. Consulting opportunities in energy and utilities concentrate on decarbonization strategy, grid modernization, and hydrogen ecosystem planning, reinforcing the sector's reliance on multidisciplinary advisory.

Heightened data-privacy regulation, patient-centric care models, and reimbursement shifts underpin healthcare consulting momentum. Firms combine regulatory know-how with technology enablement, guiding providers through electronic-health-record upgrades and cloud-based clinical trial platforms. In financial services, demand centers on real-time payment rails, digital identity, and environmental risk stress-testing. Cross-vertical synergies emerge as ESG disclosure rules and data-governance standards converge, expanding the market's addressable scope.

The Consulting Service Market Report is Segmented by Service Type (Operations, Strategy, Financial Advisory, Technology Advisory, Human-Capital, Risk and Compliance, Other Service Types), Client Industry (BFSI, Healthcare and Life Sciences, and More), Delivery Model (On-Site, Remote/Virtual, Hybrid), Organisation Size, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 40.62% of 2025 revenue, buoyed by high technology adoption, federal cybersecurity funding, and stringent financial services regulation. U.S. enterprises engage consultants for AI governance frameworks, zero-trust architecture implementation, and ESG compliance road maps. Canada contributes niche growth in energy-transition consulting, leveraging its resource-rich economy to test carbon-capture and hydrogen pilot schemes. Intensifying climate-related disclosure mandates sustains long-term consulting demand across both countries.

Asia-Pacific is the fastest-growing region, set to expand at a 6.92% CAGR through 2031, propelled by large-scale digital-infrastructure projects, e-government initiatives, and renewables build-out. China anchors regional demand with AI-infused supply-chain optimization and consumer banking digitization. Japan's emphasis on industrial robotics and Singapore's status as a financial-services innovation hub create fertile terrain for specialized consulting shops. India blends healthcare digitalization, manufacturing automation, and smart-city programs, reinforcing the consulting service market's momentum in the subcontinent.

Europe maintains steady growth, driven by energy-transition imperatives, data-privacy regulation and sustainability leadership. The Corporate Sustainability Reporting Directive compels companies to seek advisors who can meet stringent reporting timelines and assurance thresholds. Germany and France focus on Industry 4.0 productivity gains, while the Nordics pioneer circular-economy strategies that elevate demand for innovative operating-model rewiring. Middle East and Africa harness diversification policies and mega-infrastructure projects to attract global consulting expertise, whereas South America's natural-resource producers require ESG and operational-efficiency road maps to remain globally competitive.

- Deloitte Touche Tohmatsu Limited

- Accenture plc

- PricewaterhouseCoopers LLP

- Ernst & Young Global Limited

- KPMG International Cooperative

- Capgemini SE

- McKinsey & Company, Inc.

- Boston Consulting Group, Inc.

- Bain & Company, Inc.

- Roland Berger Holding GmbH & Co. KGaA

- A.T. Kearney, Inc.

- Simon-Kucher & Partners Strategy & Marketing Consultants GmbH

- OC&C Strategy Consultants LLP

- Gartner, Inc.

- Tata Consultancy Services Limited

- IBM Consulting (International Business Machines Corporation)

- Booz Allen Hamilton Holding Corporation

- CGI Inc.

- Infosys Consulting (Infosys Limited)

- Oliver Wyman Group (Marsh McLennan)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream - Accelerating digital-transformation mandates

- 4.2.2 Mainstream - Heightened post-pandemic operational-efficiency focus

- 4.2.3 Mainstream - Growing regulatory complexity in ESG and risk

- 4.2.4 Mainstream - Rapid cloud and cybersecurity adoption

- 4.2.5 Under-the-radar - Demand for advisory on Gen-AI governance

- 4.2.6 Under-the-radar - Board-level pressure for Scope-3 value-chain decarbonisation

- 4.3 Market Restraints

- 4.3.1 Mainstream - Client cost-cutting and in-house capability build

- 4.3.2 Mainstream - Talent scarcity and wage inflation

- 4.3.3 Under-the-radar - Rising carbon-footprint scrutiny of travel-heavy projects

- 4.3.4 Under-the-radar - Vendor-lock-in concerns around proprietary consulting assets

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Industry 4.0 and Digital-Transformation Practices

- 4.8 Industry Ecosystem Analysis

- 4.9 Key Regional Hotspots

- 4.10 Prevalent Business Models in Management Consulting

- 4.11 Porter's Five Forces Analysis

- 4.11.1 Bargaining Power of Buyers

- 4.11.2 Bargaining Power of Suppliers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Service Type (Value)

- 5.1.1 Operations Consulting

- 5.1.2 Strategy Consulting

- 5.1.3 Financial Advisory

- 5.1.4 Technology Advisory

- 5.1.5 Human-Capital Consulting

- 5.1.6 Risk and Compliance Consulting

- 5.1.7 Other Service Types

- 5.2 By Client Industry (Value)

- 5.2.1 BFSI

- 5.2.2 Healthcare and Life Sciences

- 5.2.3 Energy and Utilities

- 5.2.4 Manufacturing and Automotive

- 5.2.5 ICT and Media

- 5.2.6 Public Sector

- 5.2.7 Consumer and Retail

- 5.2.8 Other Industries

- 5.3 By Delivery Model (Value)

- 5.3.1 On-site Consulting

- 5.3.2 Remote / Virtual Consulting

- 5.3.3 Hybrid Consulting

- 5.4 By Organisation Size (Value)

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-sized Enterprises

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.4 Asia-Pacific (APAC)

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Deloitte Touche Tohmatsu Limited

- 6.4.2 Accenture plc

- 6.4.3 PricewaterhouseCoopers LLP

- 6.4.4 Ernst & Young Global Limited

- 6.4.5 KPMG International Cooperative

- 6.4.6 Capgemini SE

- 6.4.7 McKinsey & Company, Inc.

- 6.4.8 Boston Consulting Group, Inc.

- 6.4.9 Bain & Company, Inc.

- 6.4.10 Roland Berger Holding GmbH & Co. KGaA

- 6.4.11 A.T. Kearney, Inc.

- 6.4.12 Simon-Kucher & Partners Strategy & Marketing Consultants GmbH

- 6.4.13 OC&C Strategy Consultants LLP

- 6.4.14 Gartner, Inc.

- 6.4.15 Tata Consultancy Services Limited

- 6.4.16 IBM Consulting (International Business Machines Corporation)

- 6.4.17 Booz Allen Hamilton Holding Corporation

- 6.4.18 CGI Inc.

- 6.4.19 Infosys Consulting (Infosys Limited)

- 6.4.20 Oliver Wyman Group (Marsh McLennan)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球IT諮詢市場報告2026年全球公司秘書服務市場報告2026年全球房地產諮詢服務市場報告2026年全球精算諮詢服務市場報告2026年全球設計、研究、促銷與諮詢服務市場報告

2026年全球IT諮詢市場報告2026年全球公司秘書服務市場報告2026年全球房地產諮詢服務市場報告2026年全球精算諮詢服務市場報告2026年全球設計、研究、促銷與諮詢服務市場報告 2026-2030年全球行銷諮詢市場

2026-2030年全球行銷諮詢市場 東南亞諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)永續發展諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

東南亞諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)永續發展諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 諮詢服務技術市場-全球產業規模、佔有率、趨勢、機會、預測:按服務類型、應用、地區和競爭格局分類,2021-2031年歐洲諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

諮詢服務技術市場-全球產業規模、佔有率、趨勢、機會、預測:按服務類型、應用、地區和競爭格局分類,2021-2031年歐洲諮詢服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)