|

市場調查報告書

商品編碼

1690800

汽車智慧玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Automotive Smart Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

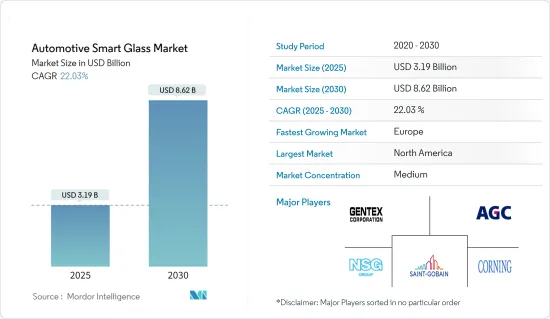

預計 2025 年汽車智慧玻璃市場規模為 31.9 億美元,到 2030 年將達到 86.2 億美元,預測期內(2025-2030 年)的複合年成長率為 22.03%。

由於技術進步和消費者對先進汽車功能的需求不斷增加,汽車智慧玻璃市場正在經歷顯著成長。智慧玻璃,也稱為可切換玻璃,具有色調調節、透明度控制和減少熱量等功能,可提高車輛的舒適度和能源效率。

開發人員不斷開發新材料和新技術,以提高智慧玻璃解決方案的性能和可靠性。例如,電致變色和懸浮顆粒裝置(SPD)技術的進步使得智慧玻璃產品具有更快的反應時間、更高的能源效率和更強的耐用性。

汽車製造商、玻璃製造商和技術供應商之間的合作也在推動市場擴張。利用玻璃製造商和汽車製造商的專業知識,我們將智慧玻璃解決方案整合到新車型中,滿足消費者對高級功能和舒適性的需求。

此外,隨著汽車製造商尋求透過改善用戶體驗、能源效率和環境永續性的創新功能來實現其產品的差異化,汽車智慧玻璃市場預計將繼續成長。這一演變凸顯了智慧玻璃技術在塑造未來汽車設計和功能方面日益成長的重要性。

汽車智慧玻璃市場的趨勢

車輛中懸浮顆粒裝置 (SPD) 的普及率日益提高

乘用車正在推動汽車智慧玻璃市場的主導地位,這從多個行業因素和趨勢中可見一斑。預計到 2023 年全球汽車銷量將從 2022 年的約 5,860 萬輛飆升至約 6,520 萬輛。汽車銷售的這一上升趨勢反映了對包括智慧玻璃解決方案在內的先進汽車技術的需求日益成長。

懸浮顆粒裝置(SPD)正成為汽車領域的重要創新。這些設備將汽車玻璃和塑膠轉變為動態可調的燈光管理系統,從而增強了駕駛體驗。這項技術對天窗、車窗和遮陽帽特別有益,顯著提高了使用者的舒適度和車輛的美觀度。

SPD智慧眼鏡因其高效性而脫穎而出,其每平方公尺僅消耗1.5瓦電能,而PDLC智慧眼鏡每平方公尺消耗3瓦電能。低能耗意味著提高燃料效率並減少對環境的影響。例如,大陸集團報告稱,SPD智慧玻璃可以每公里減少4克二氧化碳排放,並將行駛里程提高5.5%。

此外,SPD智慧玻璃可大幅降低車內的熱量,帶來更舒適、更豪華的駕駛體驗。梅賽德斯-奔馳在其 S-Class 轎車和 SL 跑車等高階車型中採用了 SPD 玻璃,可將車內溫度降低多達 10 攝氏度(18 華氏度)。這種減少不僅提高了乘客的舒適度,而且還保護了內部裝潢建材免受紅外線和紫外線輻射引起的過早老化。

隨著智慧玻璃技術的進步和主要汽車製造商的採用,預計乘用車將在汽車智慧玻璃市場保持主導地位。隨著大陸集團等公司和梅賽德斯·奔馳等高階品牌對研發的持續投資以及其實際優勢的展示,智慧玻璃將繼續成為汽車行業競爭格局中的關鍵特徵。

這種融合不僅滿足了消費者對舒適性和效率的需求,也滿足了更廣泛的環境和永續性目標,進一步鞏固了乘用車的市場領先地位。

歐洲可望成為成長最快的市場

近年來,尤其是在疫情之後,全部區域對豪華汽車的需求飆升。這種成長的推動因素是從傳統功能轉向天窗和自動著色玻璃等先進便利功能的巨大轉變。這一趨勢與消費者對汽車舒適性和豪華性的日益偏好相吻合。

推動市場成長的關鍵因素有幾個,包括主要歐洲市場的乘用車銷售量增加、豪華車銷售上升以及汽車天窗的偏好日益提升。幾十年來,德國汽車業一直是歐洲工業的支柱,並發展成為高科技汽車生產和創新的領導者。尤其是德國,汽車研發支出淨成長超過60%,凸顯了其作為推動汽車智慧玻璃需求的關鍵創新地點的作用。例如

- 韓國大型化學公司 LG 化學在贏得向德國汽車零件供應商 Webasto SE 供應可調嵌裝玻璃膜的合約後,已進入汽車智慧玻璃膜市場。

- 根據 2024 年 4 月宣布的協議,LG 化學將向 Webasto 供應用於生產汽車天窗系統的先進可切換玻璃薄膜。這些配備 LG Chem 技術的系統將供應給歐洲各地的汽車製造商。

微軟和大眾於 2022 年 5 月聯手將擴增實境眼鏡融入汽車。此次合作旨在使擴增實境(未來移動概念的關鍵元素)更接近現實。大眾汽車正在與微軟合作,將 HoloLens 2混合實境眼鏡引入行駛中的車輛,展示移動出行的未來。

搭載智慧眼鏡的新車陸續發布,廠商們也正在尋求拓展該領域的業務。奧迪、寶馬、日產和探測車等知名汽車製造商分別在其 Q 系列、X 系列、逍客和 Evoque 等熱銷車型上提供天窗選項。這一趨勢凸顯了先進的便利功能在汽車產業,特別是高階汽車領域日益成長的重要性。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 配備智慧玻璃技術的豪華和高級汽車越來越受歡迎

- 市場限制

- 預計較高的初始成本將抑制市場成長

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場區隔

- 依技術類型

- 電致變色

- 聚合物分散液晶元件(PDLC)

- 懸浮顆粒物檢測裝置 (SPD)

- 按應用程式類型

- 後側窗

- 天窗玻璃

- 前後玻璃

- 按車型

- 搭乘用車

- 商用車

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 世界其他地區

- 巴西

- 南非

- 其他國家

- 北美洲

第6章 競爭格局

- 供應商市場佔有率

- 公司簡介

- Corning Inc.

- Guardian Industries

- Saint-Gobain SA

- AGP Glass

- Hitachi Chemical Co. Ltd

- Research Frontiers Inc.

- Nippon Sheet Glass Co. Ltd

- AGC Inc.

- Gentex Corporation

- Gauzy Ltd.

第7章 市場機會與未來趨勢

- 與車輛連接和電子設備整合

The Automotive Smart Glass Market size is estimated at USD 3.19 billion in 2025, and is expected to reach USD 8.62 billion by 2030, at a CAGR of 22.03% during the forecast period (2025-2030).

The Automotive Smart Glass Market is witnessing significant growth, driven by technological advancements and increasing consumer demand for advanced vehicle features. Smart glass, also known as switchable glass, offers functionalities such as tinting, transparency control, and heat reduction, enhancing both comfort and energy efficiency in automobiles.

Manufacturers are continually developing new materials and technologies to improve the performance and reliability of smart glass solutions. For instance, advancements in electrochromic and SPD (Suspended Particle Device) technologies have enabled faster response times, better energy efficiency, and enhanced durability of smart glass products.

Collaborations between automotive manufacturers, glass suppliers, and technology providers are also driving market expansion. Partnerships enable the integration of smart glass solutions into new vehicle models, leveraging the expertise of both glass manufacturers and automotive OEMs to meet consumer demands for advanced functionality and comfort.

Furthremore, the Automotive Smart Glass Market is poised for continued growth as automakers seek to differentiate their products with innovative features that enhance user experience, energy efficiency, and environmental sustainability. This evolution underscores the increasing importance of smart glass technologies in shaping the future of automotive design and functionality.

Automotive Smart Glass Market Trends

Rise in penetration of suspended particle devices (SPD) in vehicles

Passenger cars are driving the dominance of the Automotive Smart Glass Market, as evidenced by multiple factors and trends in the industry. In 2023, global car sales surged to approximately 65.2 million units, a significant increase from around 58.6 million in 2022. This upward trend in car sales reflects the growing demand for advanced automotive technologies, including smart glass solutions.

Suspended particle devices (SPD) are emerging as a critical innovation within the automotive sector. These devices enhance the driving experience by transforming car glass or plastic into a dynamically adjustable light-management system. This technology is particularly beneficial for sunroofs, windows, and visors, significantly improving user comfort and vehicle aesthetics.

SPD smart glasses stand out for their efficiency, consuming only 1.5 watts per square meter, compared to the 3 watts per square meter required by PDLC smart glass. This lower energy consumption translates into better fuel efficiency and reduced environmental impact. For example, Continental reports that SPD smart glass can reduce carbon dioxide emissions by 4 grams per kilometer and extend the driving range by 5.5%.

Moreover, SPD smart glass contributes to a more comfortable and luxurious driving experience by significantly reducing heat inside the vehicle. Mercedes-Benz has implemented SPD glass in high-end models like the S-class sedan and SL roadster, which has shown a reduction in interior temperature by up to 10 degrees Celsius (18 degrees Fahrenheit). This reduction not only enhances passenger comfort but also protects interior materials from premature aging caused by infrared and ultraviolet radiation.

Given the advancements in smart glass technology and its adoption by leading automotive manufacturers, passenger cars are positioned to continue their dominance in the Automotive Smart Glass Market. The ongoing investment in research and development by companies like Continental and the practical benefits demonstrated by luxury brands such as Mercedes-Benz ensure that smart glass will remain a key feature in the competitive landscape of the automotive industry.

This integration not only caters to consumer demand for comfort and efficiency but also aligns with broader environmental and sustainability goals, further solidifying the role of passenger cars in driving the market forward.

Europe is Expected to Grow at the Fastest Rate in the Market

The demand for luxury cars has surged across the region in recent years, particularly post-pandemic. This growth is driven by a significant shift from traditional features towards advanced convenience features, such as sunroofs and automatic tinted glass. This trend aligns with the increasing consumer preference for enhanced comfort and luxury in vehicles.

Several key factors are propelling the market's growth, including a rise in passenger car sales in major European markets, increasing sales of luxury cars, and a growing preference for vehicle sunroofs. The German automotive sector has been the backbone of the European industry for decades, evolving into a leader in high-tech automotive production and innovation. Notably, Germany has seen a net growth of over 60% in automotive R&D, highlighting its role as a critical innovation hub driving the demand for automotive smart glass. For instance,

- LG Chem Ltd., a leading South Korean chemical company, has entered the automotive smart glass film market by securing a contract to supply switchable glazing films to German auto parts supplier Webasto SE.

- Under the agreement announced in April 2024, LG Chem will provide its advanced switchable glass films to Webasto for use in manufacturing automotive sunroof systems. These systems, equipped with LG Chem's technology, will be supplied to car manufacturers across Europe.

Microsoft and Volkswagen collaborated to integrate augmented reality glasses into vehicles in May 2022. This partnership aims to bring augmented reality, a key element of future mobility concepts, closer to reality. Volkswagen has worked with Microsoft to make the HoloLens 2 mixed-reality glasses available in mobile vehicles, showcasing the future of mobility.

The market is further encouraged by several new car launches featuring smart glass, prompting manufacturers to expand their operations in this segment. Prominent car manufacturers like Audi, BMW, Nissan, and Range Rover are offering sunroof options in popular models such as the Q-series, X-series, Qashqai, and Evoque, respectively. This trend underscores the growing importance of advanced convenience features in the automotive industry, particularly within the luxury car segment.

Automotive Smart Glass Industry Overview

The automotive smart glass market is moderately consolidated, with a few major players such as Saint Gobin, AGC Inc., Nippon Sheet Glass Co. Ltd., Gentex Corporation, and Cornering Inc. having significant shares in the market due to their well-established and developed products among various automakers. The companies are focusing on innovative technologies and following strategies, like acquisition, licensing the technology, and partnership, to expand, sustain, and capture the potential demand for rapid adoption of technological trends in the automotive industry. For instance,

- In January 2023, Asahi India Glass partnered with Enormous Brands to create impactful brand films for AIS Windows, its doors and windows solutions brand. This move comes as the Indian system windows and doors market evolves, driven by changing lifestyles, urbanization, and smart city construction. AIS Windows caters to customer preferences with a range of aluminum and uPVC framing materials and diverse glass solutions, positioning itself to significantly impact the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Adoption Of Luxury And Premium Vehicles Equipped With Smart Glass Technologies

- 4.2 Market Restraints

- 4.2.1 High Initial Cost Is Anticipated To Restrain The Market Growth

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD Million)

- 5.1 By Technology Type

- 5.1.1 Electrochromic

- 5.1.2 Polymer Dispersed Liquid Device (PDLC)

- 5.1.3 Suspended Particle Device (SPD)

- 5.2 By Application Type

- 5.2.1 Rear and Side Windows

- 5.2.2 Sunroof Glass

- 5.2.3 Front and Rear Windshield

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 Brazil

- 5.4.4.2 South Africa

- 5.4.4.3 Other Countries

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Corning Inc.

- 6.2.2 Guardian Industries

- 6.2.3 Saint-Gobain SA

- 6.2.4 AGP Glass

- 6.2.5 Hitachi Chemical Co. Ltd

- 6.2.6 Research Frontiers Inc.

- 6.2.7 Nippon Sheet Glass Co. Ltd

- 6.2.8 AGC Inc.

- 6.2.9 Gentex Corporation

- 6.2.10 Gauzy Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Integration with Vehicle Connectivity and Electronics