|

市場調查報告書

商品編碼

1690774

歐洲生質柴油 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Europe Biodiesel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

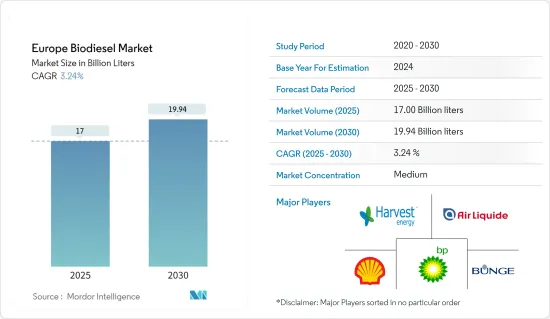

預計2025年歐洲生質柴油市場規模為170億公升,到2030年將達到199.4億升,預測期內(2025-2030年)的複合年成長率為3.24%。

關鍵亮點

- 從中期來看,預計政府支持政策法規和能源安全問題等因素將在預測期內推動市場發展。

- 另一方面,預測期內植物油和動物脂肪等原料的供應和價格預計將阻礙市場成長。

- 研究和開發工作主要集中在尋找生物柴油生產的替代原料。藻類和廢油等先進原料具有提高永續性、減少土地影響和增加原料可用性的潛力,為生物柴油生產創造了新的機會。

- 預計在預測期內德國將佔據市場主導地位。這是因為政府的政策支持它。

歐洲生質柴油市場趨勢

棕櫚油可望主導市場

- 棕櫚油是世界上產量最廣泛的植物油之一。印尼和馬來西亞等主要棕櫚油生產國擁有大片人工林和高效的提取工藝,從而擁有大量可靠的棕櫚油供應。充足的供應使得棕櫚油在可用性和成本方面比其他原料更具競爭優勢。

- 棕櫚油能量含量高,是生產生質柴油的高效原料。其高能量密度使得單位原料的生質柴油產量高,使生產具有成本效益。棕櫚油的能源效率使其對生物柴油製造商具有吸引力,並可能為其帶來市場優勢。

- 此外,棕櫚油具有低黏度和高潤滑性等有利於生物柴油生產的特性。這些特性提高了生物柴油在柴油引擎中的性能,並使其與現有的柴油基礎設施更加相容。棕櫚油基生物柴油的優良性能使其具有極強的市場潛力和競爭力。

- 2021-2022年歐洲生質柴油進口量大幅增加。據Statista稱,生物柴油進口總量增加了36%以上,顯示該地區生物柴油消費量增加。

- 2022年12月,歐盟達成初步協議,將引入法規,要求企業提供證據證明其在歐盟銷售的棕櫚油和其他商品與森林砍伐無關。

- 因此,鑑於上述幾點,棕櫚油產業很可能在預測期內佔據市場主導地位。

德國佔據市場主導地位

- 德國推出了扶持政策和措施,推動包括生質柴油在內的可再生能源發展。該國制定了雄心勃勃的可再生能源目標,並為生物柴油生產提供財政獎勵和補貼。這種支持鼓勵了生物柴油產業的投資和成長,使德國成為關鍵參與企業。

- 德國以其先進的工程和技術專長而聞名。德國擁有強大的研發基礎設施,使其能夠開發和實施創新的生物柴油生產技術。德國公司在開發高效、經濟的生物柴油生產流程方面處於領先地位,這使它們在市場上具有競爭優勢。

- 2022 年 2 月,再生能源集團宣布計劃增加其位於德國埃姆登的生物柴油精製的預處理能力。此次擴建的目的是為了能夠獲得可再生燃料原料,包括通常難以轉化的原料。

- 德國擁有完善的生物柴油生產、分銷和使用基礎設施。該國擁有許多生物柴油生產廠、廣泛的混合設施和加油站網路。現有的基礎設施為德國生質柴油市場的成長和主導地位提供了堅實的基礎。

- 2022年德國生質柴油消費量將為251.6萬噸(約7.55億加侖),低於2021年的256兆噸(約7.685億加侖)。同時,混合乙醇的使用量將增加近2.9%,從115.3萬噸(約3.86億加侖)增加到118.6兆噸(約3.97億加侖)。

- 因此,如上所述,德國很可能成為歐洲生質柴油市場的重要參與企業。

歐洲生質柴油產業概況

歐洲生質柴油市場呈半細分狀態。市場上的主要企業(不分先後順序)包括殼牌公司、英國石油公司、邦吉有限公司、液化空氣集團和 Harvest Energy。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究範圍

- 市場定義

- 調查前提

第2章執行摘要

第3章調查方法

第4章 市場概述

- 介紹

- 2028 年市場規模與需求預測

- 政府法規和政策

- 近期趨勢和發展

- 市場動態

- 驅動程式

- 政府支持措施和政策

- 能源安全

- 限制因素

- 原料的供應和價格波動;

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 原料

- 菜籽油

- 棕櫚油

- 廢棄食用油

- 其他成分

- 生質柴油混合物

- B5

- B20

- B100

- 地區

- 德國

- 西班牙

- 英國

- 法國

- 其他歐洲國家

第6章 競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- Shell PLC

- BP PLC

- Bunge Limited

- Air Liquide SA

- Harvest Energy

- Abengoa Bioenergia SA

- Envien Group

- Greenergy International Ltd.

- GBF German Biofuels GMBH

第7章 市場機會與未來趨勢

- 新型先進原料

簡介目錄

Product Code: 71558

The Europe Biodiesel Market size is estimated at 17.00 billion liters in 2025, and is expected to reach 19.94 billion liters by 2030, at a CAGR of 3.24% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as government-supportive policies and regulations and concerns over energy security are expected to drive the market during the forecasted period.

- On the other hand, the availability and price of feedstocks, such as vegetable oils and animal fats, are expected to hinder the market's growth during the forecasted period.

- Nevertheless, research and development efforts focus on finding alternative biodiesel production feedstocks. Advanced feedstocks, such as algae and waste oils, offer the potential for improved sustainability, reduced land-use impact, and increased feedstock availability, creating new opportunities for biodiesel production.

- Germany is expected to dominate the market during the forecasted period. Due to supportive government policies.

Europe Biodiesel Market Trends

Palm Oil Is Likely To Dominate The Market

- Palm oil is one of the most widely produced vegetable oils globally. Major palm oil-producing countries, such as Indonesia and Malaysia, have large-scale plantations and efficient extraction processes, leading to a significant and reliable palm oil supply. This abundant supply gives palm oil a competitive advantage in terms of availability and cost compared to other feedstocks.

- Palm oil has a high energy content, making it an efficient feedstock for biodiesel production. Its energy density allows for higher biodiesel yields per unit of feedstock, resulting in cost-effective production. The energy efficiency of palm oil contributes to its attractiveness for biodiesel manufacturers and can potentially drive its dominance in the market.

- Moreover, palm oil possesses favorable properties for biodiesel production, such as its low viscosity and high lubricity. These properties enhance the performance of biodiesel in diesel engines and make it compatible with existing diesel infrastructure. The favorable properties of palm oil-based biodiesel contribute to its market potential and competitiveness.

- The value of biodiesel imported into Europe has increased significantly between 2021 and 2022. According to Statista, the total import value for biodiesel increased by more than 36%, signifying increased biodiesel consumption in the regions.

- In December 2022, the European Union reached a preliminary agreement to introduce a regulation that would mandate companies to provide evidence that their palm oil and other commodities sold within the EU are not linked to deforestation.

- Therefore, per the points discussed above, the palm oil segment will likely dominate the market during the forecasted period.

Germany to Dominate the Market

- Germany has implemented supportive policies and regulations to promote renewable energy, including biodiesel. The country has ambitious renewable energy targets and offers financial incentives and subsidies for biodiesel production. This support encourages investment and growth in the biodiesel industry, positioning Germany as a key player.

- Germany is known for its advanced engineering and technological expertise. The country has a strong research and development infrastructure, enabling innovative biodiesel production technologies to be developed and implemented. German companies are at the forefront of developing efficient and cost-effective biodiesel production processes, giving them a competitive advantage in the market.

- In February 2022, Renewable Energy Group announced its plans to enhance the pretreatment capacity at its biodiesel refinery in Emden, Germany. This expansion aims to enable the processing of challenging feedstocks into renewable fuel feed, including those that are typically difficult to convert.

- Germany has a well-developed infrastructure for producing, distributing, and using biodiesel. The country has many biodiesel production plants, an extensive blending facility network, and fueling stations. This existing infrastructure provides a solid foundation for the growth and dominance of the biodiesel market in Germany.

- In 2022, Germany's biodiesel consumption amounted to 2.516 million metric tons (around 755 million gallons), decreasing from 2.560 million tons (approximately 768.5 million gallons) in 2021. In contrast, ethanol utilization in blends grew nearly 2.9 percent, rising from 1.153 million tons (386 million gallons) to 1.186 million tons (approximately 397 million gallons).

- Therefore, as per the points mentioned above, Germany is likely to be a significant player in the biodiesel market in Europe.

Europe Biodiesel Industry Overview

Europe's biodiesel market is semi fragmented. Some of the major players in the market (in no particular order) include Shell PLC, BP PLC, Bunge Limited, Air Liquide SA, Harvest Energy, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, until 2028

- 4.3 Government Policies and Regulations

- 4.4 Recent Trends and Developments

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Supportive Policies and Regulations

- 4.5.1.2 Energy Security

- 4.5.2 Restraints

- 4.5.2.1 Feedstock Availability and Price Volatility

- 4.5.1 Drivers

- 4.6 Supply-Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Feedstock

- 5.1.1 Rapeseed Oil

- 5.1.2 Palm Oil

- 5.1.3 Used Cooking Oil

- 5.1.4 Other Feedstocks

- 5.2 Biodiesel Blends

- 5.2.1 B5

- 5.2.2 B20

- 5.2.3 B100

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 Spain

- 5.3.3 United Kingdom

- 5.3.4 France

- 5.3.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Shell PLC

- 6.3.2 BP PLC

- 6.3.3 Bunge Limited

- 6.3.4 Air Liquide SA

- 6.3.5 Harvest Energy

- 6.3.6 Abengoa Bioenergia SA

- 6.3.7 Envien Group

- 6.3.8 Greenergy International Ltd.

- 6.3.9 GBF German Biofuels GMBH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Advanced Feedstocks

02-2729-4219

+886-2-2729-4219

生物柴油市場機會、成長要素、產業趨勢分析及2026-2035年預測

生物柴油市場機會、成長要素、產業趨勢分析及2026-2035年預測 2026-2034年全球生物柴油催化劑市場規模、佔有率、趨勢和成長分析報告全球生物柴油市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026-2034年全球生物柴油催化劑市場規模、佔有率、趨勢和成長分析報告全球生物柴油市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球綠色柴油市場報告2026年全球可再生柴油市場報告2026年全球生質柴油市場報告生質柴油市場-2026-2031年預測可再生柴油市場機會、成長要素、產業趨勢分析及預測(2026-2035)

2026年全球綠色柴油市場報告2026年全球可再生柴油市場報告2026年全球生質柴油市場報告生質柴油市場-2026-2031年預測可再生柴油市場機會、成長要素、產業趨勢分析及預測(2026-2035) 可再生柴油市場規模、佔有率和成長分析(按類型、原料、應用、最終用戶和地區分類)-2026-2033年產業預測

可再生柴油市場規模、佔有率和成長分析(按類型、原料、應用、最終用戶和地區分類)-2026-2033年產業預測 日本生質柴油市場報告:按原料、應用、類型、生產技術和地區分類(2026-2034 年)

日本生質柴油市場報告:按原料、應用、類型、生產技術和地區分類(2026-2034 年)

▼