|

市場調查報告書

商品編碼

1690753

美國MEP 服務:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)United States (US) MEP Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

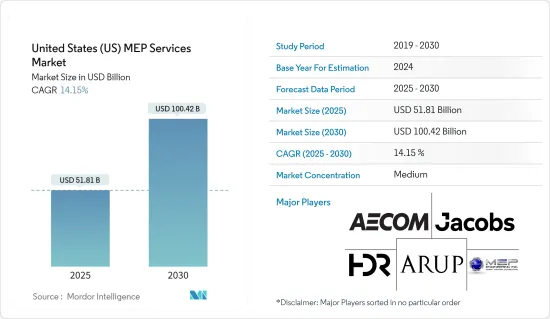

美國MEP 服務市場規模預計在 2025 年為 518.1 億美元,預計到 2030 年將達到 1,004.2 億美元,預測期內(2025-2030 年)的複合年成長率為 14.15%。

關鍵亮點

- 機械、電氣和管道 (MEP) 涉及建築物各種 MEP 系統的規劃、設計和管理,隨著 BIM 在建築施工、規劃和管理中的活性化普及,MEP 服務也越來越受到關注。

- 機電工程佔計劃建設成本的很大一部分。該地區的建設計劃正在增加,例如丹佛國際機場的維修和紐約市的交通升級,預計這些項目將推動市場成長。

- COVID-19 疫情爆發對 MEP 服務市場造成了供應鏈中斷的影響。工廠停工導致一些產品的前置作業時間延長。然而,隨著工廠目前滿載運作,生產水準開始顯著提高。

- 設計在 MEP 服務中發揮著至關重要的作用。對於任何服務供應商來說,收益的很大一部分來自於MEP設計。根據Consulting-Specifying Engineer的調查,2019年MEP巨頭們超過一半(58%)的總收益來自MEP設計,每家公司的平均MEP設計收益為8390萬美元,較前一年有大幅成長。

- 美國對 MEP 服務的需求是由新建和維修/重建需求推動的,這兩個部分都佔據了相當大的市場佔有率。不過,就該國的 MEP 服務市場佔有率而言,新建築領域略有優勢。

- 永續性的概念在建築設計產業中越來越受到重視。業界的共識是,實施環保系統最終將有利於環境和您的預算。根據美國環保署(EPA)的數據,美國發電量佔總能源消耗的40%。因此,當地供應商正在提供服務來滿足需求,利用太陽能集熱器和熱回收通風等 MEP 技術。

- 根據美國能源資訊署(EIA)的數據,商業建築的主要能源消耗是空調,佔建築物總能耗的35%,照明佔11%,冰箱、熱水器和冷凍庫等電器產品佔18%,其他電子設備佔剩餘部分。這時,MEP服務供應商就變得至關重要,他們可以開發出可以為消費者節省成本的強大設計。

- 但在目前的市場情勢下,新冠疫情對承接建築計劃的企業和政府機構的影響,導致部分建築計劃延期甚至取消。例如,終端用戶公司從中國進口的近30%的建築材料因供應鏈限制而減少了製造產量。這些案例顯示 MEP 服務市場存在一些負面前景,可能會阻礙市場成長。

美國MEP服務市場趨勢

新建設推動市場成長

- 據美國總承包商協會(AGC)稱,建築業是美國經濟的主要貢獻者。該行業擁有超過 733,000 名雇主,僱用超過 700 萬人,每年建築產值約為 1.4 兆美元。建設業是製造業、採礦業和各種 MEP 服務的主要客戶之一。在經濟衰退時期,它也是重要的經濟助推器。

- 住宅建築業一直是美國經濟從新冠疫情危機中復甦的領導人物,自2020年第三季以來一直保持兩位數的成長率,為經濟復甦和整體建築業成長做出了重大貢獻。許多計劃機會封鎖措施加快了進度,從而增加了新冠疫情期間的收入。在預測期內,市場預計將糾正承接計劃的急劇增加。

- 此外,企業收益穩定上升,但獲利壓力仍較大。該行業面臨的挑戰包括持續的成本壓力、影響生產力的持續勞動力短缺,以及固定競標計劃的趨勢,這些項目通常需要傳統系統難以實現的定價和業務準確性水平。持續採用數位技術可以緩解其中的一些問題。

- 在成功實施和提高員工技能以吸收技術方面可能還有其他障礙。儘管面臨這些挑戰,MEP 公司仍有望從該行業中的各種重大機會中受益,包括美國交通基礎設施改善計劃和智慧大型企劃的成長。

醫療機構的需求正在推動市場成長

- 該地區的衛生部門被認為是經濟最佳運作的關鍵部門之一。然而,它面臨著規劃效率低下和醫療設施資源匱乏的重大挑戰。例如,根據 2012 年 1 月至 2019 年 5 月的資料,Humana 和匹茲堡大學的研究人員報告稱,約 25% 的醫療保健支出效率低。

- 因此,醫療保健領域的最終用戶開始意識到 MEP 服務可以利用其設施內的低效率。此外,在醫療機構內,每個部門(例如手術室、婦科或小兒科)都有獨特的要求。此外,不良的設計可能會對患者護理產生毀滅性的影響。例如,室內空氣品質差會對患者的健康產生負面影響。透過這種方式,MEP 服務有可能支援醫療業務的核心系統。

- 此外,正在發生的新冠肺炎疫情暴露了該地區缺乏疫情防範,以及其衛生系統的低效和不公平現象。例如,衛生基礎設施無法容納新冠肺炎患者,人均病床數量低於其他已開發國家。

- 因此,該地區的政府機構已開始分配更多資源用於建立高效的醫療設施,預計案例將導致對 MEP 服務的需求激增。例如,2020 年 5 月,AECOM 宣布已完成紐約市設計和建設局 (DDC) 的計劃,該項目將建造兩所臨時醫院,作為 COVID-19 緊急設施。

美國MEP服務業概況

美國MEP 服務市場區隔程度適中。主要企業包括 Jacobs Engineering Group Inc、HDR Inc、AECOM 和 Arup Group。該市場的供應商正在利用夥伴關係和協作來獲取市場佔有率。近期市場走勢如下:

- 2020 年 6 月,AECOM 與全球另類資產管理公司 Canyon Partners, LLC 宣布,將與馬丁集團合作,開始開發以交通為導向的中層學生住宅計劃Wexler。該公司宣布已從太平洋西部銀行借入 7,330 萬美元的優先建設貸款融資。計劃預計於2020年秋季完工。

- 2020 年 10 月,加州大學舊金山分校 (UCSF) 選定奧雅納 (Arup) 和舊金山的醫療專家 Mazzetti 擔任新醫院——位於帕納蘇斯高地的 UCSF 海倫迪勒醫療中心的首席 MEP 工程師。 Arup 也可能為該計劃提供附加服務,如土木工程服務、聲學、振動和物流諮詢。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 對設計和工程服務業的影響評估

- 美國機電工程師當前就業指數

- 技術進步對 MEP 服務業的影響(CAD、BIM、MEP 軟體等)

第5章市場動態

- 市場促進因素

- 更重視外包 MEP 服務,進而實現核心服務的集中化

- 商業和醫療設施需求穩定

- 經營模式的演變以及公司和服務供應商之間的合作

- 市場限制

- 市場集中度高以及對端到端產品的需求不斷成長將為中小企業帶來挑戰

第6章市場區隔

- 按類型

- 新建築

- 維修整修

- 性能驗證活動

- 其他

- 按行業

- 醫療保健

- 商業辦公室

- 教育機構

- 公共空間和設施

- 工業設施和倉庫

- 其他商業設施(資料中心、研究等)

第7章競爭格局

- 公司簡介

- Jacobs Engineering Group Inc.

- HDR Inc

- Arup Group

- AECOM

- MEP Engineering

- Stantec Inc.

- Affiliated Engineers Inc.

- Macro Services

- WSP Group

- AHA Consulting

- Burns Engineering

- Wiley Wilson

第8章投資分析

第9章:市場的未來

簡介目錄

Product Code: 71420

The United States MEP Services Market size is estimated at USD 51.81 billion in 2025, and is expected to reach USD 100.42 billion by 2030, at a CAGR of 14.15% during the forecast period (2025-2030).

Key Highlights

- Mechanical electrical and plumbing (MEP) involves planning, designing, and managing various MEP systems of a building, and with the increasing incorporation of BIM in building construction, planning, and management, MEP services are further gaining traction.

- The MEP contribute to the significant portion of projects' construction cost. With the growing number of construction projects in the region, such as Denver International Airport renovation and New York City transit upgrades, it is expected to drive the growth of the market.

- The COVID-19 pandemic has impacted the MEP services market with respect to disruptions in the supply chain. Lead times for some products were increased due to factory shutdowns. However, now with factories functioning at full capacities, production levels are beginning to see significant improvements.

- Design plays a vital role in MEP services as a significant share of the revenue for any service provider is generated from MEP design. According to a study by Consulting-Specifying Engineer, over half (58%) of the revenue from all of MEP giants combined during 2019 was generated from MEP design, with an average MEP design revenue of USD 83.9 million per firm and observed a significant increase compared to the previous year.

- The US demand for MEP services is driven by new construction and retrofit and renovation demand with both segments, driving a prominent share of the market. However, the new construction segment commands a slight upper hand when it comes to the MEP services market share in the country.

- The concept of sustainability is gaining momentum in the construction design industry; the industry consensus is that installing eco-friendly systems would eventually benefit the environment and the budget. According to the EPA, electricity generation in the US accounts for 40% of the total energy consumption. Thereby vendors in the regions are leveraging the MEP technologies such as solar collectors and ventilation with heat recovery accompanied by their services to counter the demand.

- According to the US Energy Information Administration (EIA), in a commercial building, major energy-consuming sections are HVAC systems at 35% of the total building energy, lighting at 11%, appliances, such as refrigerators, water heaters, and freezers at 18%, and the remaining is shared among various other electronics. This is where MEP service providers become vital in developing robust designs that enable consumers to reduce costs.

- However, in the current market scenario, some of the construction projects have been delayed, and some resulted in cancellation as the result of the impact of COVID-19 on the companies and government bodies that commissioned them. For instance, nearly 30% of imported construction material deployed by the end-user firms from China due to supply chain constraints manufacturing output has declined. These instances showcase some of the negative outlooks of the MEP services market that holds the potential to hinder market growth.

US MEP Services Market Trends

New Construction to Drive the Market Growth

- As per the Associated General Contractors (AGC) of America, the construction industry is a major contributor to the US economy. The industry has more than 733,000 employers with over 7 million employees and creates nearly USD 1.4 trillion worth of structures each year. Construction is one of the major customers for manufacturing, mining, and a variety of MEP services. It is also seen as a significant economic reviver during the recession period.

- The residential construction sector has been the star performer of the United States' economic recovery from the COVID-19 crisis, posting double-digit growth rates since the third quarter of 2020 and making significant contributions to the rebound of the economy and the overall construction industry growth. Many construction projects were fast-tracked to utilize the opportunity of the lockdown and resulted in an increased revenue during the COVID-19 phase. Over the forecast period, the market is expected to correct the sudden increase in projects undertaken.

- Moreover, firm revenues are steadily rising, and the bottom lines are still under considerable pressure. Among the challenges that the industry face is sustained cost pressures, ongoing labor shortages that affect productivity, and trends toward fixed-bid projects that often demand a level of pricing and operations precision that is difficult to obtain with traditional systems. While the industry still trails broader digital acceptance maturity, the continued adoption of digital technologies could alleviate some of these issues.

- It can also present additional hurdles in terms of successful implementations and upskilling the workforce to absorb the technologies. Despite these challenges, MEP firms are poised to potentially benefit from various significant industry opportunities, including the US transportation and infrastructure upgrade initiative and the growth of smart city mega-projects.

Demand from Healthcare Institutions to Drive Market Growth

- The healthcare sector in the region is considered one of the crucial sectors for the optimal functioning of the economy. However, it faces the huge problem of inefficient planning and insufficient resources at the healthcare facilities. For instance, Humana and the University of Pittsburgh researchers reported that based on the data from January 2012 to May 2019, approximately 25% of healthcare spending could be characterized as inefficient.

- Thereby, end-user from the healthcare sector are starting to realize the potential offered by MEP services to leverage inefficiencies in the facilities. Moreover, In a healthcare facility, each department has its specific requirements: operation theatre, Gynaecological Department, or the Paediatrics Department. Additionally, incompetent designs could lead to a catastrophic effect on patient treatment. For instance, low internal air quality could cause adverse effects on the health of the patients. Thus, MEP services hold the potential to support the systems that are the backbone of healthcare operations.

- Furthermore, the ongoing pandemic COVID-19 has showcased the region's lack of preparation to counter the pandemic and has exposed the health system's inefficiencies and inequities. For instance, the healthcare infrastructure cannot accommodate COVID-19 patients and has fewer hospital beds per capita than other developed countries.

- Thereby these instances are expected to surge the demand for MEP service as the government bodies in the region are starting to allocate many resources into the construction of efficient medical facilities. For instance, In May 2020, AECOM announced it had completed the New York City Department of Design and Construction's (DDC) project to construct two temporary hospitals that are aimed to serve as COVID-19 emergency facilities.

US MEP Services Industry Overview

The United States MEP Services Market is moderately fragmented. The major companies include Jacobs Engineering Group Inc, HDR Inc, AECOM, and Arup Group. Vendors in the market are leveraging partnerships and collaborations to capture the market share. Some of the recent developments in the market are:

- June 2020: AECOM, in partnership with Canyon Partners, LLC, a global alternative asset management firm, announced a joint venture with The Martin Group to begin the transit-oriented development of Wexler, a mid-rise student housing project. The company announced that it had taken a USD 73.3 million senior construction loan from Pacific Western Bank. The project is scheduled to be completed by fall 2020.

- October 2020: The University of California, San Francisco (UCSF) selected Arup and San Francisco-based healthcare specialists Mazzetti as the lead MEP engineers of record for its new hospital, UCSF Helen Diller Medical Center at Parnassus Heights (Parnassus Heights). Arup could also be providing additional services for the project, including civil engineering services and acoustics/vibration and logistics consulting.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Design and Engineering Services Industry

- 4.4 Current Employment Index of MEP Engineers in the United States

- 4.5 Impact of Technological Advancements on the MEP Services Industry (CAD, BIM, MEP Software, etc.)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Emphasis on Outsourcing of MEP Services to Focus on Core Offering

- 5.1.2 Steady Demand from Commercial and Healthcare Institutions

- 5.1.3 Evolving Business Models and Nature of Collaboration between Firms and Service Vendors

- 5.2 Market Restraints

- 5.2.1 Operational Challenges in High Market Concentration and Growing Demand for End-to-end Offering Affect Smaller Firms

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 New Construction

- 6.1.2 Retrofit & Renovation

- 6.1.3 Commissioning Activity

- 6.1.4 Other Types

- 6.2 By End-user Vertical

- 6.2.1 Healthcare

- 6.2.2 Commercial Offices

- 6.2.3 Educational Institutions

- 6.2.4 Public Spaces and Institutions

- 6.2.5 Industrial establishments & Warehouses

- 6.2.6 Other Commercial entities (Data centers, Research, etc.)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Jacobs Engineering Group Inc.

- 7.1.2 HDR Inc

- 7.1.3 Arup Group

- 7.1.4 AECOM

- 7.1.5 MEP Engineering

- 7.1.6 Stantec Inc.

- 7.1.7 Affiliated Engineers Inc.

- 7.1.8 Macro Services

- 7.1.9 WSP Group

- 7.1.10 AHA Consulting

- 7.1.11 Burns Engineering

- 7.1.12 Wiley Wilson

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

全球機電管道服務市場-按服務類型、類型、最終用戶、地區和競爭格局分類的行業規模、佔有率、趨勢、機會和預測(2020-2030 年預測)

全球機電管道服務市場-按服務類型、類型、最終用戶、地區和競爭格局分類的行業規模、佔有率、趨勢、機會和預測(2020-2030 年預測) 按服務類型、組件、計劃類型、客戶群和最終用戶產業分類的機械、電氣和管道服務市場—2025-2032年全球預測

按服務類型、組件、計劃類型、客戶群和最終用戶產業分類的機械、電氣和管道服務市場—2025-2032年全球預測 2025年全球機械、電氣和管道軟體市場報告

2025年全球機械、電氣和管道軟體市場報告 全球機械、電氣和管道支援系統市場

全球機械、電氣和管道支援系統市場 機械電氣和管道支援系統市場,按組件、按應用、按材料、按最終用途、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

機械電氣和管道支援系統市場,按組件、按應用、按材料、按最終用途、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 全球 MEP 服務市場 2025-2029

全球 MEP 服務市場 2025-2029 2024 年至 2028 年商業建築 MEP 解決方案全球市場

2024 年至 2028 年商業建築 MEP 解決方案全球市場 北美機械、電氣和管道 (MEP) 服務市場規模、佔有率、趨勢分析報告:按服務類型、最終用途、類型、國家/地區、細分市場預測,2024-2030 年

北美機械、電氣和管道 (MEP) 服務市場規模、佔有率、趨勢分析報告:按服務類型、最終用途、類型、國家/地區、細分市場預測,2024-2030 年