|

市場調查報告書

商品編碼

1690106

法國資料中心市場:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)France Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

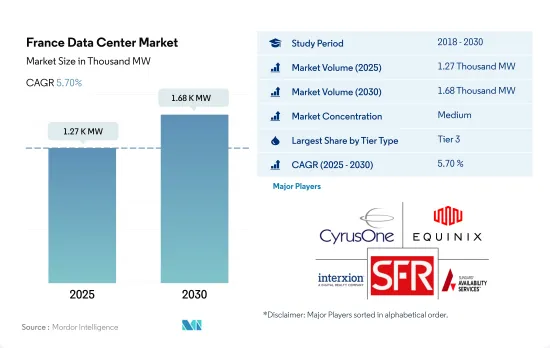

法國資料中心市場規模預計在 2025 年達到 1,270 千瓦,預計在 2030 年達到 1,680 千瓦,複合年成長率為 5.70%。

預計主機託管收益將在 2025 年達到 17.993 億美元,到 2030 年將達到 31.578 億美元,預測期內(2025-2030 年)的複合年成長率為 11.91%。

以容量計算,預計 2023 年 3層級資料中心將佔據大部分佔有率,並將在整個預測期內繼續佔據主導地位。

- 預計 2023 年層級 3資料中心容量將達到 782.67 MW,到 2029 年將超過 1,016.98 MW,複合年成長率為 4.46%。另一方面, 層級 4資料中心預計將成長,複合年成長率為 6.72%,到 2029 年容量將達到 283.98MW。

- 未來幾年,層級和層級設施的需求將逐漸減少,成長率也將放緩。預計到 2029 年,層級和層級設施的市場佔有率將保持在 2% 左右,且成長幅度很小。這是由於長時間且不穩定的停電造成的。由於對儲存、處理和分析資料的需求增加,大多數用戶最終將遷移到第 3層級和第 4 級設施,這兩項設施將分別佔市場佔有率的 76.5% 和 21.4%。

- 經濟體中的 BFSI 部門正在擴張。近年來,法國網路銀行和手機銀行的使用率增加。在歐洲市場中,法國的網路銀行普及率名列前15名。截至 2021 年,72% 的法國消費者使用網路銀行,高於 2017 年的 62%。由於電子銀行和線上交易的需求不斷成長,這需要建造符合層級 3 和 Tier 4 要求的批發和超大規模設施。

- 此外,預計未來幾年層級資料中心將大幅擴張。這是因為越來越多的公司提供雲端基礎的服務,從而導致更多公司建立提供採用最佳技術的主機託管空間的設施。

法國資料中心市場的趨勢

智慧型手機用戶數量的增加和無現金交易正在推動市場成長

- 2022 年,該國智慧型手機用戶總數為 5,420 萬,預計到 2029 年將達到 5,915 萬,預測期內複合年成長率為 1.25%。

- 法國的數位化應用正在迅速成長。網路和智慧型手機等技術在各行業的快速應用正在影響消費行為。例如,2018年至2021年間,法國的人均購買力從0.9%成長至2%。結果,更多的人能夠購買智慧型手機,導致智慧型手機用戶數量的增加。

- 該國的網路普及率從 2017 年的 80.05% 上升到 2020 年的 84.8%,智慧型手機用戶數量從 2017 年的 3,970 萬增加到 2020 年的 4,980 萬。如此廣泛的使用促進了數位付款服務的發展,而新冠疫情期間,數位支付的應用也隨之增加。此外,該國已將支付門檻從 30 歐元提高到 50 歐元,以減少病毒傳播的機會。人們越來越喜歡無現金交易,預計將對市場產生長期影響。因此,法國的智慧型手機用戶數量正在增加。

- 法國市場智慧型手機的普及導致資料不斷增加,需要增加儲存空間來容納需要即時處理和分析的無法控制的資料流。資料中心必須管理大量資料。因此,隨著智慧型手機用戶數量的增加,法國資料中心可能需要增加更多的機架。

電子商務、5G 基礎設施和新型銀行等數位銀行的日益普及將推動市場需求

- 2022年,法國的平均資料速度為59.66Mbps。法國於 2000 年代中期推出了 4G。法國於2020年推出5G服務。自兩項服務推出以來,4G在2022年達到86.72Mbps,5G在2022年達到201.3Mbps。法國四大行動服務供應商——Orange、SFR、Bouygues Telecom和Free Mobile——於2013年在巴黎、馬賽、里昂、裡爾和南特測試了4G服務。 4G覆蓋率從2018年初的45%擴大到2020年中期的76%。

- 在5G網路服務方面,Nokia、Orange Business Services、Free Mobile、愛立信和法國國家鐵路公司(SNCF)將於2020年在法國部署5G網路,用於商業和工業服務。根據法國政府的規劃,到2030年,5G將覆蓋法國全境。四大通訊業者都計劃在2022年在3000個地點安裝5G,到2024年在8000個地點安裝5G,到2025年在10500個地點安裝5G,這意味著在不久的將來,原始資料將以更指數級的速度成長。 2G服務將於2026年逐步淘汰,3G服務將於2029年逐步淘汰。

- 更高的通訊為最終用戶擴展其客戶的線上服務(例如電子商務和數位銀行)鋪平了道路。新銀行(純數位銀行)正在改變法國銀行業未來的運作方式。自 2018 年以來,在新銀行開設的活期帳戶數量增加了 2.5%,法國的活躍帳戶超過 350 萬個。也就是說,31% 的新銀行用戶希望未來能更頻繁地使用銀行服務。因此,更高的行動資料速度預計將在終端用戶產業中帶來更多面向服務的應用,預計這將在未來幾年帶來資料處理設施的成長。

法國資料中心產業概況

法國資料中心市場正在緩慢整合,前五大參與者佔60.47%的市場。市場的主要企業有:CyrusOne Inc.、Equinix Inc.、Interxion(Digital Reality Trust Inc.)、SOCIETE FRANCAISE DU RADIOTELEPHONE-SFR 和 Sungard Availability Services LP(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 市場展望

- 負載能力

- 占地面積

- 主機代管收入

- 安裝的機架數量

- 機架空間利用率

- 海底電纜

第5章 產業主要趨勢

- 智慧型手機用戶數量

- 每部智慧型手機的資料流量

- 行動資料速度

- 寬頻資料速度

- 光纖連接網路

- 法律規範

- 法國

- 價值鍊和通路分析

第6章市場區隔

- 熱點

- 巴黎(法國法蘭西島)

- 法國其他地區

- 資料中心規模

- 大規模

- 超大規模

- 中等規模

- 百萬

- 小規模

- 層級類型

- 1層級和2級

- 層級

- 層級

- 吸收量

- 未使用

- 使用

- 按主機託管類型

- 超大規模

- 零售

- 批發的

- 按最終用戶

- BFSI

- 雲

- 電子商務

- 政府

- 製造業

- 媒體與娛樂

- 電信

- 其他最終用戶

第7章競爭格局

- 市場佔有率分析

- 商業狀況

- 公司簡介.

- Cogent Communications

- CyrusOne Inc.

- Equinix Inc.

- Euclyde Data Centers

- Global Switch Holdings Limited

- Interxion(Digital Reality Trust Inc.)

- Scaleway SAS(Illiad Group)

- SOCIETE FRANCAISE DU RADIOTELEPHONE-SFR

- Sungard Availability Services LP

- Telehouse(KDDI Corporation)

- Thesee DataCenter

- Zenlayer Inc.

- LIST OF COMPANIES STUDIED

第8章:CEO面臨的關鍵策略問題

第9章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 全球市場規模和DRO

- 資訊來源及延伸閱讀

- 圖表清單

- 關鍵見解

- 資料包

- 詞彙表

The France Data Center Market size is estimated at 1.27 thousand MW in 2025, and is expected to reach 1.68 thousand MW by 2030, growing at a CAGR of 5.70%. Further, the market is expected to generate colocation revenue of USD 1,799.3 Million in 2025 and is projected to reach USD 3,157.8 Million by 2030, growing at a CAGR of 11.91% during the forecast period (2025-2030).

Tier 3 data center accounted for majority share in terms of volume in 2023, and is expected to dominate through out the forecasted period

- The tier 3 data center capacity is expected to reach 782.67 MW in 2023 and is further projected to register a CAGR of 4.46%, surpassing 1016.98 MW by 2029. On the other hand, the tier 4 data center is predicted to grow and register a CAGR of 6.72% to reach a capacity of 283.98 MW by 2029.

- Facilities in tier 1 and tier 2 gradually lose their demand and display a decrease in growth in the upcoming years. Tier 1 and 2 facilities are expected to hold a market share of nearly 2% by 2029 with minimal growth. This is a result of the prolonged and inconsistent outages. Most users will eventually switch to tier 3 and 4 facilities, holding 76.5% and 21.4% of the market share, respectively, owing to the increased demand for storing, processing, and analyzing data.

- The BFSI sector of the economy is expanding. In recent years, France has seen a rise in the use of online and mobile banking. In the European market, France has one of the top 15 best rates of online banking penetration. As of 2021, 72% of French consumers were using online banking, which increased from 62% in 2017. This necessitates the construction of wholesale and hyperscale facilities, which have tier 3 and 4 requirements and is driven by the rising demand for e-banking and online transactions.

- Additionally, tier 4 data centers are expected to expand significantly in the years to come. This is because more businesses are providing cloud-based services, which has caused more businesses to construct facilities to provide colocation space with the best technology.

France Data Center Market Trends

Rising smartphone users and cashless transactions boost the market growth

- The total number of smartphone users in the country was 54.20 million in 2022, which is expected to register a CAGR of 1.25% during the forecast period to reach a value of 59.15 million by 2029.

- Digital usage is expanding rapidly in France. The quick internet and smartphone technology adoption in various businesses has impacted consumer behavior. For instance, from 2018 to 2021, the per capita purchasing power per person in France increased from 0.9% to 2%. As a result, more people can purchase smartphones, leading to a growing number of smartphone users.

- The internet penetration of the country increased from 80.05% in 2017 to 84.8% in 2020, while the number of smartphone users increased from 39.7 million in 2017 to 49.8 million in 2020. Owing to such extensive use, digital payment services were promoted, and their application increased due to the COVID-19 pandemic. Additionally, the nation raised the payment threshold from EUR 30 to EUR 50 to lessen the chance of the virus spreading. People are now more inclined to prefer cashless transactions, which is predicted to have a long-term impact on the market. Consequently, there are more smartphone users in France.

- The rising use of smartphones in the French market results in a constant increase in data, necessitating a growing amount of storage space to accommodate this uncontrollable flow of data with the need for real-time processing and analysis. The data centers must manage the sheer amount of data. Thus, the requirement for extra racks in French data centers may increase as the number of smartphone users rises.

Rising adoption of e-commerce, 5G infrastructure and digital banking such as Neobank increases the adoption of market demand

- In 2022, the nation's average data speed was 59.66 Mbps. The mid-2000s saw the introduction of 4G in France. France launched its 5G services in 2020. Since the launch of both services, 4G reached 86.72 Mbps in 2022 and 5G reached 201.3 Mbps by 2022. Four French mobile service providers, Orange, SFR, Bouygues Telecom, and Free Mobile, tested their 4G offerings in 2013 in Paris, Marseille, Lyon, Lille, and Nantes, which are significant 4G hotspots. The 4G coverage has grown from 45% at the beginning of 2018 to 76% by the middle of 2020.

- In terms of 5G network services, France saw the deployments of these networks in 2020 for commercial and industrial services from Nokia, Orange Business Services, Free Mobile, Ericsson, and SNCF. According to French government plans, 5G should be available across the country by 2030. All four major operators had planned to install 5G in 3,000 locations by 2022, 8,000 by 2024, and 10,500 by 2025, which will further suggest the exponential generation of raw data in the near future. The 2G and 3G services will be decommissioned by 2026 and 2029, respectively.

- The increased average speed is paving the way for end users, such as e-commerce, and digital banking, to expand their online services for customers. Neobanks, or digital-only banks, are changing how France's banking industry functions in the future. The number of current accounts opened in neobanks has increased by 2.5% from 2018, and France has over 3.5 million active accounts. Nevertheless, 31% of Neobank users want to use banks' services more frequently in the future. Thus, the rise in mobile data speed is expected to lead to more service-oriented applications among end-user industries and is expected to lead to the growth of data processing facilities in the coming years.

France Data Center Industry Overview

The France Data Center Market is moderately consolidated, with the top five companies occupying 60.47%. The major players in this market are CyrusOne Inc., Equinix Inc., Interxion (Digital Reality Trust Inc.), SOCIETE FRANCAISE DU RADIOTELEPHONE - SFR and Sungard Availability Services LP (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 It Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 Key Industry Trends

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.6.1 France

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

- 6.1 Hotspot

- 6.1.1 Paris (Ile-De-France)

- 6.1.2 Rest of France

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.3.1 Cogent Communications

- 7.3.2 CyrusOne Inc.

- 7.3.3 Equinix Inc.

- 7.3.4 Euclyde Data Centers

- 7.3.5 Global Switch Holdings Limited

- 7.3.6 Interxion (Digital Reality Trust Inc.)

- 7.3.7 Scaleway SAS (Illiad Group)

- 7.3.8 SOCIETE FRANCAISE DU RADIOTELEPHONE - SFR

- 7.3.9 Sungard Availability Services LP

- 7.3.10 Telehouse (KDDI Corporation)

- 7.3.11 Thesee DataCenter

- 7.3.12 Zenlayer Inc.

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms

2025年資訊中心外包全球市場報告

2025年資訊中心外包全球市場報告 資料中心備用電源 HVO 的全球和區域市場:HVO 製造商、供應商、發電機製造商和資料中心營運商的分析和預測(2025-2034 年)

資料中心備用電源 HVO 的全球和區域市場:HVO 製造商、供應商、發電機製造商和資料中心營運商的分析和預測(2025-2034 年) 資料中心維修市場分析及預測(至 2034 年):類型、產品、服務、技術、組件、應用、部署、最終用戶、模組、安裝類型

資料中心維修市場分析及預測(至 2034 年):類型、產品、服務、技術、組件、應用、部署、最終用戶、模組、安裝類型 資料中心資產管理的全球市場:各零件,各部署模式,各用途,各終端用戶業界,各地區,機會,預測,2018年~2032年

資料中心資產管理的全球市場:各零件,各部署模式,各用途,各終端用戶業界,各地區,機會,預測,2018年~2032年 資料中心用水的美國市場:市場趨勢,機會,預測(2025年~2030年)AI資料中心的全球市場:各零件,資料中心類別,各部署,各終端用戶業界,各地區,機會,預測,2018年~2032年

資料中心用水的美國市場:市場趨勢,機會,預測(2025年~2030年)AI資料中心的全球市場:各零件,資料中心類別,各部署,各終端用戶業界,各地區,機會,預測,2018年~2032年 全球資料中心部署支出市場:市場規模(按資料中心類型、最終用戶和地區分類)、未來預測資訊中心外包市場規模、佔有率、按服務類型、部署類型、企業規模、最終用途、地區、細分預測的趨勢分析,2025 年至 2030 年全球資料中心能源儲存市場規模依資料中心類型、最終用戶、地區和預測:資料中心市場分析及預測(至 2034 年):類型、產品、服務、技術、組件、應用、部署、最終用戶、模組、功能

全球資料中心部署支出市場:市場規模(按資料中心類型、最終用戶和地區分類)、未來預測資訊中心外包市場規模、佔有率、按服務類型、部署類型、企業規模、最終用途、地區、細分預測的趨勢分析,2025 年至 2030 年全球資料中心能源儲存市場規模依資料中心類型、最終用戶、地區和預測:資料中心市場分析及預測(至 2034 年):類型、產品、服務、技術、組件、應用、部署、最終用戶、模組、功能