|

市場調查報告書

商品編碼

1689949

纖維增強塑膠(FRP)回收-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Fiber-reinforced Plastic (FRP) Recycling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

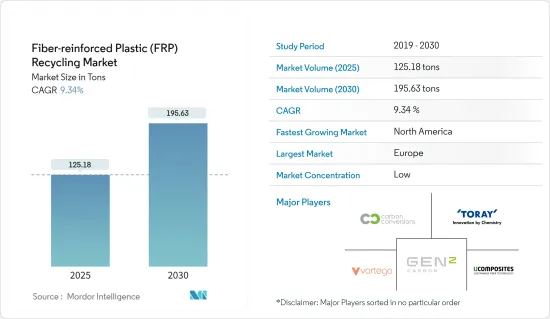

預計 2025 年纖維增強塑膠回收再利用市場規模為 125.18 噸,到 2030 年將達到 195.63 噸,預測期內(2025-2030 年)的複合年成長率為 9.34%。

由於各種貿易和業務限制,COVID-19 疫情對 2020 年的市場產生了不利影響。然而,在 2021 年下半年限制措施放寬、疫情消退之後,由於汽車、建築等各個終端用戶行業對再生纖維塑膠複合材料的使用增加,市場實現了正成長率。

關鍵亮點

- 從中期來看,複合材料廢棄物的不斷增加、複合材料處理的嚴格規定以及促進碳纖維增強塑膠(CFRP)再利用的新策略預計將推動市場成長。

- 然而,回收過程中面臨的困難、缺乏適當的 CFRP 回收技術以及由於 CFRP 使用壽命長而導致的複合材料廢棄物供應有限,預計將阻礙市場的成長。

- 複合材料回收的持續發展可能為研究市場提供機會。

- 歐洲佔據市場主導地位。然而,預計北美將在預測期內經歷最快的成長。

纖維增強塑膠市場趨勢

建築和施工佔據市場主導地位

- 建築業是利用再生纖維增強塑膠 (FRP)廢棄物進行各種應用的主要行業之一。再生玻璃鋼在建築業的使用包括使用100%再生玻璃鋼和使用任意比例的再生玻璃鋼。

- 回收的玻璃鋼重量輕、易於加工、具有熱穩定性、電絕緣性和在腐蝕環境中的耐久性,使其在建築和施工領域有廣闊的應用前景。玻璃纖維增強塑膠(FRP)再生材料以及碳纖維增強塑膠(FRP)再生材料是建築領域使用的主要再生材料。

- 再生玻璃鋼在建築業的常見應用是替代鋼材和混凝土等傳統建築材料。

- 預計冠狀病毒疫情過後,全球建築業支出將增加約 13 兆美元,年增率為 3%。根據世界銀行預測,2022年全球建築業支出為13.4兆美元。

- 根據美國人口普查局的數據,2022年美國私人建築支出增加,幾乎是政府建築支出的四倍。當談到美國的建築支出時,德克薩斯州和加利福尼亞州處於領先地位。

- 回收的玻璃鋼可用於製造結構梁、柱等承重結構構件,以及覆層、面板、建築幕牆等非結構構件,以及門窗等預製建築構件。

- 此外,人們對機械回收的玻璃鋼廢料在波特蘭水泥等新型複合材料中的潛在應用進行了大量研究,希望這些回收材料可以用作增強材料、骨材和填充材的替代品。

- 預計所有上述因素都將推動建築業的發展,並在預測期內增加對纖維增強塑膠 (FRP) 回收的需求。

歐洲主導市場

- 由於德國、義大利和英國等主要國家的需求不斷成長,預計歐洲將主導全球市場。

- 包括德國在內的歐洲國家禁止掩埋,正在加速再生塑膠/複合材料的採用。回收的玻璃鋼在建築、航太和風力發電行業中具有潛在用途。

- 回收的玻璃纖維用於製造風力渦輪機葉片。風能是德國可再生能源轉型最重要的驅動力之一。預計德國和西班牙將退役最多數量的葉片,其次是丹麥。德國漢莎航空已永久退役 40 多架飛機,並關閉了其德國之翼廉價航空部門。

- 歐洲風能組織 (WindEurope) 提議在2025年前在全歐洲範圍內禁止報廢舊風力發電機葉片。歐洲風電企業積極致力於對退役葉片進行100%的再利用、再循環和回收。此前,多家行業領先公司宣布了雄心勃勃的葉片回收和再利用計劃。掩埋禁令可以加速環保回收技術的發展。

- 根據海上再生能源彈射中心的數據,德國預計到 2050 年將除役超過 10 吉瓦的離岸風力發電機,以及約 80 吉瓦的陸上風力發電機。風力發電機除役的增加導致風電產業產生的玻璃鋼廢棄物數量增加。加強歐盟框架以確保有效實施、掩埋和焚燒,以及加強有關 FRP廢棄物管理的措施,正在推動 FRP 回收市場的發展。

- 2021年11月,英國首個開發風力發電機葉片回收利用的重大舉措獲得批准,該計畫為期三年,耗資20億歐元(21.4億美元)。此外,政府也頒布了有關廢棄物處理的嚴格環境法規。

- 此外,義大利積極參與玻璃鋼回收市場,包括建立試驗工廠。 Karborek Recycling Carbon Fibers 是一家專門從事碳纖維回收和再利用的義大利先驅公司。該公司的再生產品主要用於航太、汽車、工業、軍事和體育產業。

- 預計所有上述因素都將對未來幾年的市場需求產生重大影響。

纖維增強塑膠產業概況

纖維增強塑膠(FRP)回收市場高度細分。大型回收公司與複合材料製造商和OEM合作,收集和回收廢棄物。主要回收商(排名不分先後)包括東麗工業公司、Vartega 公司、Gen 2 Carbon Limited、Ucomposites AS 和 Carbon Conversions。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 混合廢棄物增加

- 其他促進因素

- 限制因素

- 缺乏適合CFRP的回收技術,FRP的回收過程困難

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 產品類型

- 玻璃纖維增強塑膠

- 碳纖維增強塑膠

- 其他

- 回收技術

- 熱感/化學回收

- 焚燒/共焚燒

- 機械回收(尺寸減少)

- 最終用戶產業

- 工業的

- 運輸

- 建築與施工

- 運動的

- 其他

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 其他

- 南美洲

- 中東和非洲

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 生產者-回收商夥伴關係

- 主要企業策略

- 公司簡介

- Aeron Composite Pvt. Ltd

- Carbon Conversions

- Carbon Fiber Recycle Industry Co. Ltd

- Carbon Fiber Recycling

- Conenor Ltd

- Eco-Wolf Inc.

- Gen 2 Carbon Limited

- Global Fiberglass Solutions

- Karborek Recycling Carbon Fibers

- MCR Mixt Composites Recyclables

- Mitsubishi Chemical Advanced Materials GmbH

- Neocomp GmbH

- Procotex

- Toray industries Inc.

- Ucomposites AS

- Vartega Inc.

第7章 市場機會與未來趨勢

- 再生複合材料板塊的發展

The Fiber-reinforced Plastic Recycling Market size is estimated at 125.18 tons in 2025, and is expected to reach 195.63 tons by 2030, at a CAGR of 9.34% during the forecast period (2025-2030).

The COVID-19 pandemic adversely impacted the market in 2020 due to various trade and operational restrictions. However, after the loosening of restrictions and retracting the pandemic in the latter half of 2021, the market recorded a positive growth rate due to the increased use of recycled fiber plastic composites in various end-user industries, such as automotive, building and construction, and others.

Key Highlights

- Over the medium term, the growing accumulation of composite waste, stringent regulations on composite disposal, and new strategies to promote the reuse of carbon-fiber-reinforced plastic (CFRP) are expected to drive the market's growth.

- On the flip side, difficulties faced during the recycling process, lack of proper recycling techniques for CFRP, and the long service life of CFRP resulting in the limited composite waste availability, are expected to hinder the growth of the market studied.

- Nevertheless, continuous developments in the recycling composites will likely act as an opportunity for the studied market.

- The European region dominated the market. However, the North American region will likely witness the fastest growth during the forecast period.

Fiber Reinforced Plastic Market Trends

Building and Construction Dominates the Market

- The construction industry is among the major industries utilizing recycled fiber-reinforced plastics (FRPs) waste for different applications. Utilization of recycled FRPs in the construction industry includes using 100% recycled FRPs and recycled FRPs in any percentage.

- Recycled FRPs are lightweight, easy to install, and possess thermal and stability, electrical insulation, and durability in very corrosive environments, making these recycled FRPs useful for application in the building and construction industry. Recyclates of glass FRPs are the majorly used recyclates in construction, along with recyclates of carbon FRPs in certain significant amounts.

- The common application of recycled FRPs in the construction industry includes its use as an alternative to traditional building materials such as steel and concrete.

- After the coronavirus pandemic, the global construction industry increased to a spending value of around USD 13 trillion, predicted to rise by 3% annually. According to the World Bank, the construction industry spending worldwide in 2022 was USD 13.4 trillion.

- According to the US Census Bureau, in the United States, private construction spending increased in 2022 and was roughly four times more than governmental construction spending. Regarding construction spending throughout the 50 United States, Texas, and California came out on top.

- Recycled FRPs can be used to create structural beams, columns, and other load-bearing elements, as well as non-structural elements such as cladding, panels, and facades, and used in manufacturing prefabricated building components, such as doors and windows.

- Furthermore, the potential applications of mechanically recycled FRP waste in new composite materials, on which a significant amount of research is carried out, include Portland cement, where these recyclates are expected to use as reinforcement, aggregate, or filler replacement.

- All the factors above are expected to drive the building and construction segment, enhancing the demand for fiber-reinforced plastic (FRP) recycling during the forecast period.

Europe to Dominate the Market

- The European region is expected to dominate the global market due to the increasing demand from major countries like Germany, Italy, and the United Kingdom.

- In European countries, including Germany, landfilling is prohibited, so adopting recycled plastics/composites is gaining momentum. Recycled FRPs may be used in the construction, aerospace, and wind power industries.

- Recycled FRPs find applications in windmill blades. Wind power is one of the most important drivers of Germany's transition to renewable energy. The biggest number of decommissioned blades is expected in Germany and Spain, followed by Denmark. Lufthansa permanently decommissioned more than 40 aircraft and axed its Germanwings low-cost arm.

- Wind Europe advocated a waste ban on obsolete wind turbine blades throughout Europe by 2025. The wind business in Europe is aggressively committed to reusing, recycling, or recovering 100% of decommissioned blades. It follows the announcement of ambitious blade recycling and recovery plans by numerous industry-leading companies. A landfill ban may hasten the development of environment-friendly recycling technology.

- According to the Offshore Renewable Energy Catapult, Germany's projected offshore wind turbine decommissioning is more than 10 W, and the projected onshore wind turbine decommissioning is about 80 GW by 2050. These rising decommissions of wind turbines increase the amount of FRP waste from the wind sector. The rising EU framework to ensure effective implementation, landfill, and incineration, coupled with more policies on FRP waste management, is driving the market for FRP recycling.

- In November 2021, for the first time in the United Kingdom, a large initiative to develop wind turbine blade recycling was granted the go-light, costing EUR 2 billion (USD 2.14 billion) over three years. Furthermore, the government initiated strict environmental legislation regarding waste disposal in the country.

- Furthermore, Italy is active in the FRP recycling market, including an established pilot plant. Karborek Recycling Carbon Fibers is a pioneer in Italy and specializes in recycling and recovering carbon fibers. The company's recycled products are majorly used in the aerospace, automotive, industrial, military, and sports industries.

- All the factors mentioned above are likely to significantly impact the demand in the market in the years to come.

Fiber Reinforced Plastic Industry Overview

The fiber-reinforced plastic (FRP) recycling market is highly fragmented. Major recycling companies partner with composites and OEM manufacturers to collect and recycle the waste. Some major recycling companies (not in a particular order) include Toray Industries Inc., Vartega Inc., Gen 2 Carbon Limited, Ucomposites AS, and Carbon Conversions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Accumulation of Composite Waste

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Lack Of Proper Recycling Techniques For CFRP And Difficult Recycling Process Of FRP

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Glass Fiber-reinforced Plastic

- 5.1.2 Carbon Fiber-reinforced Plastic

- 5.1.3 Other Product Types

- 5.2 Recycling Technique

- 5.2.1 Thermal/chemical Recycling

- 5.2.2 Incineration and Co-incineration

- 5.2.3 Mechanical Recycling (Size Reduction)

- 5.3 End-user Industry

- 5.3.1 Industrial

- 5.3.2 Transportation

- 5.3.3 Building And Construction

- 5.3.4 Sports

- 5.3.5 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest Of Asia-pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle East & Africa

- 5.4.1 Asia-pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Producer Recycler Partnerships

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aeron Composite Pvt. Ltd

- 6.4.2 Carbon Conversions

- 6.4.3 Carbon Fiber Recycle Industry Co. Ltd

- 6.4.4 Carbon Fiber Recycling

- 6.4.5 Conenor Ltd

- 6.4.6 Eco-Wolf Inc.

- 6.4.7 Gen 2 Carbon Limited

- 6.4.8 Global Fiberglass Solutions

- 6.4.9 Karborek Recycling Carbon Fibers

- 6.4.10 MCR Mixt Composites Recyclables

- 6.4.11 Mitsubishi Chemical Advanced Materials GmbH

- 6.4.12 Neocomp GmbH

- 6.4.13 Procotex

- 6.4.14 Toray industries Inc.

- 6.4.15 Ucomposites AS

- 6.4.16 Vartega Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developments in the Field of Recycling Composites

纖維增強塑膠市場:依纖維類型、樹脂類型和終端用戶產業分類-2026-2032年全球預測

纖維增強塑膠市場:依纖維類型、樹脂類型和終端用戶產業分類-2026-2032年全球預測 FRP管材市場報告:按類型、製造流程、應用和地區分類(2026-2034年)FRP貨櫃市場:按貨櫃類型、製造流程和應用分類-2026-2032年全球市場預測FRP儲槽市場:按類型、容量、製造流程、材質等級、應用和最終用戶分類-2026-2032年全球市場預測FRP橋樑市場:按橋樑類型、纖維類型、樹脂類型、組件和應用分類-2026-2032年全球市場預測FRP格柵市場:2026-2032年全球市場預測(依成型製程、樹脂類型、應用及終端用戶產業分類)

FRP管材市場報告:按類型、製造流程、應用和地區分類(2026-2034年)FRP貨櫃市場:按貨櫃類型、製造流程和應用分類-2026-2032年全球市場預測FRP儲槽市場:按類型、容量、製造流程、材質等級、應用和最終用戶分類-2026-2032年全球市場預測FRP橋樑市場:按橋樑類型、纖維類型、樹脂類型、組件和應用分類-2026-2032年全球市場預測FRP格柵市場:2026-2032年全球市場預測(依成型製程、樹脂類型、應用及終端用戶產業分類) 玻璃纖維增強塑膠管道市場機會、成長要素、產業趨勢分析及預測(2026-2035年)

玻璃纖維增強塑膠管道市場機會、成長要素、產業趨勢分析及預測(2026-2035年) 2026年全球FRP儲槽市場報告2026年全球FRP容器市場報告2026年全球玻璃纖維增強塑膠(GRP)管道市場報告

2026年全球FRP儲槽市場報告2026年全球FRP容器市場報告2026年全球玻璃纖維增強塑膠(GRP)管道市場報告