|

市場調查報告書

商品編碼

1689938

導電矽膠:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Conductive Silicone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

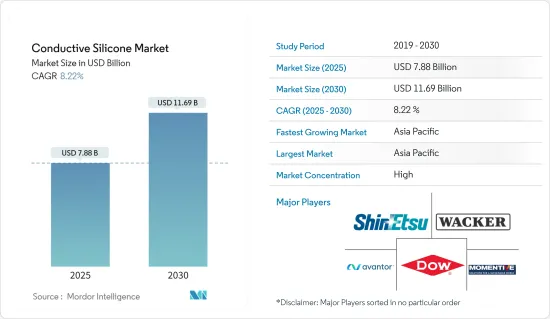

導電矽膠市場規模預計在 2025 年為 78.8 億美元,預計到 2030 年將達到 116.9 億美元,預測期內(2025-2030 年)的複合年成長率為 8.22%。

COVID-19 疫情最初擾亂了導電矽膠的供應鏈。隨後,快速數位化以及遠距學習和遠距工作的引入導致電子設備的需求激增。因此,導電矽膠市場輕鬆恢復到疫情前的水平。

主要亮點

- 電子設備對導電矽膠的需求不斷增加以及太陽能電池產業對導電矽膠的使用量不斷增加,預計將推動導電矽膠的市場需求。

- 然而,預計 EMI 屏蔽中導電矽膠的替代將在預測期內抑制市場成長。

- 微流體設備等醫療設備技術的進步為市場開闢了新的可能性。

- 由於汽車、電子和通訊行業的需求不斷增加,亞太地區在導電矽膠市場佔據主導地位。

導電矽膠市場趨勢

電子產業成長導致需求增加

- 導電矽膠因具有導電性、導熱性、柔韌性和耐腐蝕性等優異的性能,廣泛應用於電氣和電子應用領域。

- 導電矽膠具有優異的導電性,使其成為電氣設備的理想材料。矽膠中的導電顆粒可以傳輸電流,使其適用於需要傳輸訊號、資料和電力的應用。

- 中國是世界上最大的電子設備製造基地。智慧型手機、電視和其他個人電子設備等電子產品是電子產業中成長最快的產品。

- 該國對電子產品的需求很高。為了滿足這項普遍需求,中國已啟動「中國製造2025」計畫等戰略措施。根據該計劃,中國政府宣布了2030年實現產出3,050億美元、滿足80%國內需求的目標。此外,中國是智慧型手機的製造中心,大大增加了對導電矽膠的需求。

- 日本電子情報技術產業協會(JEITA)發布的資料顯示,2022年日本電子產業總產值將達到約11.1243兆日圓(約843.4億美元),較前一年成長近8%。

- 德國是歐洲最大的電子國家。德國是歐洲最大的電氣電子產品市場,也是世界第五大電氣電子產品市場。據德國電氣電子協會稱,預計2022年該市場規模將達到2,200億歐元以上(2,348.4億美元)。

- 德國電氣與電子相關企業在國內外僱用了160多萬名員工。此外,全國30%的研發人員從事電子和微技術領域的工作。

- 此外,電子產品佔德國出口總額的13%。德國電子和數位產業名目出口將年增7.0%,到2023年4月將達到190億歐元(約209.3億美元)。今年前四個月,該產業的海外交付額達842億歐元(約927.5億美元),年增10.7%。

- 作為法國2030投資計畫的一部分,法國政府計劃在2030年投資約8億歐元(8.8億美元),支持各種電子技術發展的學術研究生態系統。

- 因此,預計上述因素將在不久的將來推動導電矽膠的需求。

亞太地區佔市場主導地位

- 亞太地區是導電矽膠最大且成長最快的市場。電子、汽車和發電產業的應用日益增多,推動了亞太地區對導電矽膠的需求。

- 中國、印度、日本、印尼和越南等該地區的國家正在加大對發電工程的投資,從而推動導電矽膠市場的成長。

- 此外,防靜電包裝變得越來越重要,為了防止灰塵積聚並保持電氣和電子設備的功能和長壽命,電子設備中導電矽膠的使用預計會增加。亞洲是最大的電氣和電子設備生產地區,其中中國、日本、印度和東南亞國協佔據領先地位。

- 中國是全球最大的電子產品製造基地。智慧型手機、電視和其他個人設備等電子產品的成長最為顯著。

- 官方資料顯示,2023年華虹集團無錫規劃興建12吋特殊製程產線,製程等級涵蓋65/55-40nm,月產能達8.3萬片。

- 此外,晶圓代工巨頭晶圓半導體公司將於2023年投資約29億美元用於12吋晶圓製造計劃。

- 近年來,由於能源需求不斷成長,中國一直在投資各種可再生能源計劃。 2023年11月,中國政府計畫安裝230GW風電和太陽能發電容量。該國已在 2023 年向各種風能和太陽能發電工程共投資 1,400 億美元,目標是到 2060 年實現碳中和目標。

- 2021-2025年的電網投資預算為4,550億美元,比前十年增加60%。此外,併網儲能容量將比2020年增加一倍,到2023年達到67GW。

- 因此,預計上述因素將在預測期內推動該地區對導電矽膠的需求。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章 調查範圍

- 研究範圍

- 研究假設和市場定義

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 電子產業需求不斷成長

- 擴大太陽能電池產業的應用

- 限制因素

- EMI 屏蔽中導電矽膠的替代品

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔

- 依產品類型

- 合成橡膠

- 樹脂

- 凝膠

- 其他產品類型(糊劑、填縫劑、黏合劑、油脂)

- 按應用

- 黏合劑和密封劑

- 熱界面材料

- 封裝和灌封化合物

- 三防膠

- 其他用途(生物醫學、光催化)

- 按最終用戶產業

- 車

- 建造

- 發電

- 電氣和電子

- 其他終端用戶產業(工業機械、消費品、航太)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作、協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- 3M

- Avantor Inc.

- CHT Germany GmbH

- Dongguan City Betterly New Materials Co. Ltd

- Dow

- Elkem ASA

- Euro Technologies

- Henkel AG & Co. Kgaa

- Momentive

- Parker Hannifin Corporation

- Polymax Ltd

- Shin-Etsu Chemical Co. Ltd

- Silicone Solutions

- Soliani Emc Srl

- Specialty Silicone Products Inc.

- Wacker Chemie AG

第7章 市場機會與未來趨勢

- 醫療設備新技術發展

The Conductive Silicone Market size is estimated at USD 7.88 billion in 2025, and is expected to reach USD 11.69 billion by 2030, at a CAGR of 8.22% during the forecast period (2025-2030).

The COVID-19 outbreak initially disrupted the conductive silicone supply chain. Later on, demand for electronics surged due to rapid digitization and the adoption of distance learning and remote work. Thus, the conductive silicone market readily recovered to its pre-pandemic stage.

Key Highlights

- The increasing demand for conductive silicone in electronic devices and its increasing usage in the solar industry are expected to raise the market demand for conductive silicone.

- On the other hand, the alternative to conductive silicone in EMI shielding is anticipated to restrain market growth during the forecast period.

- Advancements in medical device technology, such as microfluidic devices, are opening up new possibilities within the market.

- The Asia-Pacific region dominates the conductive silicone market, owing to rising demand from the automotive, electronics, and telecommunications industries.

Conductive Silicone Market Trends

Growth in the Electronics Segment to Augment the Demand

- Conductive silicone is extensively used in electrical and electronics applications because of its superior properties such as electrical conductivity, thermal conductivity, flexibility, and corrosion resistance.

- The superior electrical conductivity associated with the use of conductive silicone makes it the ideal material for electric devices. Silicone's conductive particles enable the transfer of electrical current, making it useful for applications that require the transmission of signals, data, and power.

- China is the largest base for electronics production in the world. Electronic products such as smartphones, TVs, and other personal electronic devices recorded the highest growth in the electronics segment.

- The country has a large demand for electronic products. To benefit from this extensive demand, China has embarked on strategic initiatives like the "Made in China 2025" plan. Under this plan, the Chinese government has announced its goal to reach an output of USD 305 billion by 2030 and, therefore, meet 80% of its domestic demand. Moreover, China is an industrial hub for smartphone production, significantly boosting the demand for conductive silicone.

- According to the data released by the Japan Electronics and Information Technology Industries Association (JEITA), in 2022, the total production value of the electronics industry in Japan amounted to around JPY 11,124.3 billion (USD 84.34 billion), showcasing a rise of nearly 8% from the previous year.

- Germany has the largest electronic industry in Europe. The German market is Europe's largest and the world's fifth-largest electrical and electronics market. It had registered more than EUR 220 billion (USD 234.84 billion) in 2022, according to the Germany Electrical and Electronics Association.

- Electrical and electronic companies in Germany employ a workforce of more than 1.6 million at home and abroad. Also, 30% of all R&D employees in the country are working in the field of electronics and microtechnology.

- Additionally, electronics constitute up to 13% of the country's overall exports. The nominal exports of the German electro and digital industry witnessed an annual growth of 7.0% to reach EUR 19.0 billion (USD 20.93 billion) in April 2023. In the first four months of this year, the sector's aggregated deliveries abroad experienced a Y-o-Y growth of 10.7%, reaching a value of EUR 84.2 billion (USD 92.75 billion).

- As part of the France 2030 investment plan, the French government plans to invest nearly EUR 800 million (USD 880 million) to support the academic research ecosystem for the development of various electronic technologies by 2030.

- Therefore, the aforementioned factors are projected to boost the demand for conductive silicone in the near future.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region stands to be the largest and fastest-growing market for conductive silicone. Factors such as the increasing utilization in the electronics, automotive, and power generation industries have been driving the demand for conductive silicone in Asia-Pacific.

- Countries in the region, such as China, India, Japan, Indonesia, and Vietnam, are witnessing increasing investments in power generation projects, boosting the growth of the conductive silicone market.

- The heightened significance of anti-static packaging for dust control during electric charge and sustaining functionality and longevity of electrical and electronic devices is anticipated to increase the utilization of conductive silicone in electronics. Asia is the largest producer of electrical and electronic devices, with countries like China, Japan, India, and ASEAN countries leading production.

- China is the most extensive base for electronics production in the world. Electronic products such as smartphones, TVs, and other personal devices recorded the highest growth.

- According to official data, in 2023, Huahong Group's Wuxi planned to build a 12-inch specialty process production line with a process grade covering 65/55-40 nm and a monthly production capacity of 83,000 pieces.

- Furthermore, Nexchip Semiconductor Corporation invested around USD 2.9 billion in 2023 in the 12-inch wafer manufacturing project.

- Recently, China has been investing in various renewable energy projects due to the growing demand for energy in the country. In November 2023, the Government of China planned to install 230 GW of wind and solar capacity. The country invested a total of USD 140 billion in 2023 in various wind and solar projects with the aim of achieving its 2060 carbon-neutral target.

- The country has budgeted USD 455 billion in grid investments from 2021-2025, an increase of 60% from the previous decade. It also doubled its grid-connected energy storage capacity from 2020 to reach 67 GW in 2023.

- Hence, the factors mentioned above are expected to drive the demand for conductive silicone in the region during the forecast period.

Conductive Silicone Industry Overview

The conductive silicone market is consolidated in nature. The major players operating in the market (not in any particular order) include Wacker Chemie AG, DOW, Shin-Etsu Chemical Co. Ltd, Momentive, and Avantor Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 SCOPE OF THE REPORT

- 1.1 Scope of the Study

- 1.2 Study Assumptions and Market Definition

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Electronics Industry

- 4.1.2 Increasing Usage in the Solar Industry

- 4.2 Restraints

- 4.2.1 Alternative to Conductive Silicone in EMI Shielding

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 By Product Type

- 5.1.1 Elastomers

- 5.1.2 Resins

- 5.1.3 Gels

- 5.1.4 Other Product Types (Pastes, Gap Fillers, Adhesives, and Greases)

- 5.2 By Application

- 5.2.1 Adhesives and Sealants

- 5.2.2 Thermal Interface Materials

- 5.2.3 Encapsulant and Potting Compounds

- 5.2.4 Conformal Coatings

- 5.2.5 Other Applications (Biomedical and Photocatalysis)

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Construction

- 5.3.3 Power Generation

- 5.3.4 Electrical and Electronics

- 5.3.5 Other End-user Industries (Industrial Machinery, Consumer Goods, and Aerospace)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Avantor Inc.

- 6.4.3 CHT Germany GmbH

- 6.4.4 Dongguan City Betterly New Materials Co. Ltd

- 6.4.5 Dow

- 6.4.6 Elkem ASA

- 6.4.7 Euro Technologies

- 6.4.8 Henkel AG & Co. Kgaa

- 6.4.9 Momentive

- 6.4.10 Parker Hannifin Corporation

- 6.4.11 Polymax Ltd

- 6.4.12 Shin-Etsu Chemical Co. Ltd

- 6.4.13 Silicone Solutions

- 6.4.14 Soliani Emc Srl

- 6.4.15 Specialty Silicone Products Inc.

- 6.4.16 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New Technological Developments in Medical Devices