|

市場調查報告書

商品編碼

1689911

脂肪酸酯:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Fatty Acid Ester - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

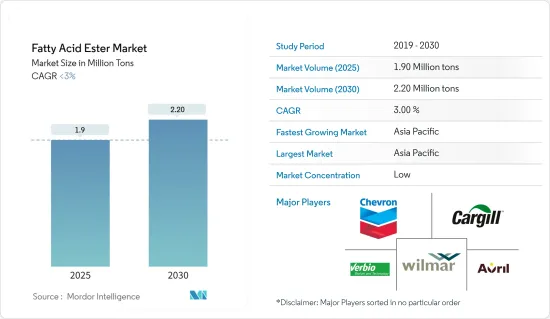

脂肪酸酯市場規模預計在 2025 年為 190 萬噸,預計在 2030 年達到 220 萬噸,預測期內(2025-2030 年)的複合年成長率低於 3%。

主要亮點

- 推動脂肪酸酯市場發展的主要因素是對生物柴油的偏好日益成長以及對個人保健產品的需求不斷增加。

- 然而,與脂肪酸酯相關的性能限制可能會在預測期內阻礙市場成長。

- 脂肪酸酯的新應用和回收可能為未來幾年的市場研究帶來機會。

- 預計亞太地區將在預測期內實現最高的複合年成長率,成為成長最大的市場。

脂肪酸酯市場趨勢

生質燃料應用對脂肪酸酯的需求不斷增加

- 生質柴油比石油柴油產生更多的有害污染物和溫室氣體。生物柴油由多種可再生資源生產,包括脂肪酸酯。常用的可再生資源包括脂肪酸甲酯和乙酯。

- 這些脂肪酸酯可以純淨形式使用,也可以與石油柴油混合使用。燃料混合物包括 B2(2% 生質柴油、98% 石油柴油)、B5(5% 生質柴油、95% 石油柴油),以及更高濃度的 B20 和 B100。特別是,大型卡車運輸公司經常使用最純淨的生物柴油 B100。

- 據美國能源資訊署稱,到2023年美國生物柴油產量將達到約17億加侖。

- 大約在同一時間,巴西成為南美洲領先的生質燃料生產國。根據能源研究所的《世界能源統計評論》,預計2023年石油產量將達到每天45.5萬桶,成長18.5%。

- 為了滿足日益成長的生物柴油需求,各企業正在提高生產能力。例如,巴西著名的生物柴油生產商 Binatural 於 2023 年 12 月宣布計劃將年產量提高 20%,到 2026年終達到每年 6.5 億公升。

- 這些發展表明生質燃料生產對各種脂肪酸酯的需求強勁。

預計亞太地區將主導市場

- 由於對生質燃料、合成潤滑油和其他應用的需求龐大,亞太地區是脂肪酸酯 (FAE) 最大的市場。

- 根據2024年世界能源統計評論,亞太地區已成為生物柴油的主要生產國。到 2023 年,該地區的生物柴油產量將佔全球的 33% 以上,日產量約 32 萬桶,高於 2022 年的 29 萬桶。

- 脂肪酸酯也用於生產合成潤滑油,如潤滑脂和液壓油。

- 最近,各公司正在投資建立生產工廠,以滿足印度對各種潤滑油日益成長的需求。例如,埃克森美孚在2023年3月宣布將投資1.1億美元在印度孟買建立潤滑油生產工廠。該廠預計將於 2025年終運作,每年成品潤滑油的生產能力為 159,000 千噸。

- 2024 年 5 月,另一家全球潤滑油製造商克魯勃潤滑劑公司宣布將投資 1,560 萬歐元(1,720 萬美元)擴建其位於印度邁索爾的潤滑油製造廠。

- 2024年3月,殼牌印尼宣布將在印度建立第一家潤滑脂製造廠。該工廠的潤滑脂年生產能力為 12 千噸,將生產用於軸承、齒輪和其他應用的殼牌佳度 (Gadus) 品牌潤滑脂產品。

- 預計此類投資將對亞太地區的脂肪酸酯消費產生正面影響。

脂肪酸酯產業概況

脂肪酸酯市場本質上是分散的,只有少數幾家大公司佔據市場主導地位。一些主要企業(不分先後順序)包括 Wilmar International Ltd、Avril、Chevron Corporation、Verbio Vereinigte Bioenergie AG 和 Cargill Corporation。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 生質柴油偏好

- 個人保健產品需求不斷成長

- 市場限制

- 脂肪酸酯的性能限制

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔

- 按類型

- 脂肪酸甲酯 (FAME)

- 多元醇酯

- 山梨糖醇酯

- 蔗糖酯

- 其他類型(乙酯、丙酯、蔗糖酯等)

- 按應用

- 合成潤滑油

- 藥品

- 個人保健產品

- 食物

- 生質燃料

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 合併、收購、合資、合作和協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- Avril

- Cargill Incorporated

- Chevron Corporation

- Cremer Oleo Gmbh & Co. KG

- Croda International PLC

- DuPont

- Granol

- Inolex Incorporated

- IOI Corporation Berhad

- KLK Oleo

- P&G Chemicals

- Sasol

- Stepan Company

- Verbio Vereinigte Bioenergie AG

- Wilmar International Ltd

第7章 市場機會與未來趨勢

- 脂肪酸酯的新用途及回收利用

簡介目錄

Product Code: 69276

The Fatty Acid Ester Market size is estimated at 1.90 million tons in 2025, and is expected to reach 2.20 million tons by 2030, at a CAGR of less than 3% during the forecast period (2025-2030).

Key Highlights

- The major factors driving the fatty acid ester market are a growing preference for biodiesels and a rising demand for personal care products.

- On the other hand, performance limitations associated with fatty acid esters are likely to hamper the market's growth during the forecast period.

- Emerging applications and recycling of fatty acid esters are likely to act as opportunities for the market studied in the coming years.

- Asia-Pacific is expected to be the largest and fastest-growing market, registering the highest CAGR during the forecast period.

Fatty Acid Ester Market Trends

Increasing Demand for Fatty Acid Ester from Biofuel Applications

- Biodiesel produces a higher level of toxic pollutants and greenhouse gases than petroleum diesel. It is made from a wide range of renewable sources, such as fatty acid esters. Some of the commonly used renewable sources are fatty acid methyl and ethyl esters.

- These fatty acid esters can be utilized in their pure form or blended with petroleum diesel. Blends include B2 (2% biodiesel, 98% petroleum diesel), B5 (5% biodiesel, 95% petroleum diesel), and larger concentrations like B20 and B100. Notably, large trucking companies often use biodiesel in its purest form, B100.

- According to the United States Energy Information Administration, biodiesel production in the United States reached approximately 1.7 billion gallons in 2023.

- At the same time, Brazil emerged as South America's leading biofuel producer. In 2023, daily oil production hit 455 thousand barrels, marking an 18.5% rise, according to the Energy Institute's Statistical Review of World Energy.

- In response to rising biodiesel demand, companies are ramping up production capacities. For example, Binatural, a prominent Brazilian biodiesel producer, announced plans in December 2023 to boost its annual output by 20%, targeting 650 million liters per annum by the end of 2026.

- These developments indicate a robust demand for various kinds of fatty acid esters in biofuel production.

Asia-Pacific Projected to Dominate the Market

- Asia-Pacific is the biggest market for fatty acid esters (FAEs) owing to the huge demand for biofuels, synthetic lubricants, and other applications.

- As per the 2024 Statistical Review of World Energy, Asia-Pacific emerged as the dominant biodiesel producer. In 2023, the region accounted for over 33% of global biodiesel output, churning out approximately 320,000 barrels daily, up from 290,000 barrels in 2022.

- Fatty acid esters are also used in the production of synthetic lubricants such as greases, hydraulic fluids, and others.

- In recent times, various companies have invested in setting up production plants to meet the growing demand for various lubricants in India. For instance, in March 2023, Exxon Mobil announced the investment of USD 110 million in setting up a lubricant production plant in Mumbai, India. The plant is expected to be operational by the end of 2025 and will have a production capacity of 159,000 kilotons of finished lubricants every year.

- In May 2024, Kluber Lubrication, another global manufacturer of lubricants, announced an investment of EUR 15.6 million (USD 17.20 million) in expanding its lubricant manufacturing plant in Mysore, India.

- In March 2024, Shell Indonesia announced that it would set up its first grease manufacturing plant in India. The plant is expected to have a production capacity of 12 kilotons of grease every year and will produce grease products under the trademark of Shell Gadus, which are used in applications such as bearings and gears.

- Such investments are expected to have a positive impact on the consumption of fatty acid esters in Asia-Pacific.

Fatty Acid Ester Industry Overview

The fatty acid ester market is fragmented in nature, with only a few major players dominating it. Some of the major companies (not in a particular order) are Wilmar International Ltd, Avril, Chevron Corporation, Verbio Vereinigte Bioenergie AG, and Cargill Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Preference toward Biodiesel

- 4.1.2 Rising Demand for Personal Care Products

- 4.2 Market Restraints

- 4.2.1 Performance Limitations Associated with Fatty Acid Ester

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Type

- 5.1.1 Fatty Acid Methyl Esters (FAME)

- 5.1.2 Polyol Esters

- 5.1.3 Sorbitan Esters

- 5.1.4 Sucrose Esters

- 5.1.5 Other Types (Ethyl Esters, Propyl Esters, Sucrose Esters, etc.)

- 5.2 By Application

- 5.2.1 Synthetic Lubricants

- 5.2.2 Pharmaceuticals

- 5.2.3 Personal Care Products

- 5.2.4 Food

- 5.2.5 Biofuel Applications

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Avril

- 6.4.2 Cargill Incorporated

- 6.4.3 Chevron Corporation

- 6.4.4 Cremer Oleo Gmbh & Co. KG

- 6.4.5 Croda International PLC

- 6.4.6 DuPont

- 6.4.7 Granol

- 6.4.8 Inolex Incorporated

- 6.4.9 IOI Corporation Berhad

- 6.4.10 KLK Oleo

- 6.4.11 P&G Chemicals

- 6.4.12 Sasol

- 6.4.13 Stepan Company

- 6.4.14 Verbio Vereinigte Bioenergie AG

- 6.4.15 Wilmar International Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications and Recycling of Fatty Acid Ester