|

市場調查報告書

商品編碼

1689897

硼 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Boron - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

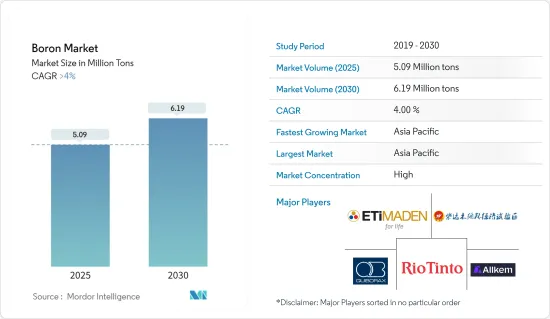

預計2025年硼市場規模為509萬噸,2030年將達到619萬噸,預測期間(2025-2030年)的複合年成長率將超過4%。

由於所有行業都停止了生產流程,COVID-19 對市場產生了負面影響。封鎖、社交隔離和貿易制裁已對全球供應鏈網路造成嚴重破壞。不過,2021年情況開始好轉,市場恢復成長軌跡。

主要亮點

- 推動市場研究的主要因素之一是各終端使用者產業對玻璃纖維的應用日益廣泛。此外,預測期內農業產業需求的增加可能會推動對硼的需求。

- 然而,人們對化合物稀缺性的日益擔憂可能會抑制市場的發展。

- 陶瓷行業需求的不斷成長可能為未來的市場成長提供機會。

- 由於汽車、建築等各行各業對硼的需求量大,亞太地區在硼市場佔據主導地位。

硼市場趨勢

玻璃領域佔市場主導地位

- 在玻璃工業中,硼主要應用於硼矽酸玻璃、編織玻璃纖維和絕緣玻璃纖維。添加硼會使玻璃製品變成耐熱和耐化學腐蝕的材料。在熔融玻璃中間體中添加硼可以提高最終產品的流動性、表面硬度和耐久性。

- 玻璃製造商在矽基中添加 5% 至 20% 的硼酸鹽,以顯著降低熔化溫度和黏度、防止玻璃結晶、調節熱膨脹並防止脫硝。最終產品足夠堅固,可以承受巨大的機械和熱衝擊,並且耐用且耐化學腐蝕。

- 根據國際玻璃年(2022),全球共有 650 家容器玻璃製造商,在 1,200 家工廠中營運,每年生產 9500 萬噸玻璃;320 家平板玻璃製造商,在 560 家工廠中營運,每年生產約 1.06 億噸平板玻璃;230 家工廠,在 400 萬噸工廠中營運餐具約 400 萬。

- 全球 1,200 家公司、2,160 家機構每年生產 2.09 億噸玻璃。但這些數字並不包括第二產業、玻璃纖維製造、美術、特殊玻璃製品和第二產業。

- 因此,在預測期內,玻璃產業很可能繼續佔據市場主導地位。

亞太地區佔市場主導地位

- 由於中國和印度等終端用戶行業的成長,預計亞太地區將在預測期內成為最大的硼市場。

- 受中產階級家庭清潔意識不斷增強的推動,亞太地區預計將擁有全球最大的清潔劑產業。中國和印度等國家是全球最大的清潔劑生產國之一。

- 硼酸、硼酸鹽等硼化合物可延長水泥的水化期。因此,硼化合物在建設產業中得到了有效的應用。

- 建築業是中國持續經濟發展的關鍵因素。中國正在經歷建築業的蓬勃發展。根據中國國家統計局的數據,建築業產值將從2021年的29.3兆元(4.2兆美元)成長到2022年的31.2兆元(4.5兆美元)。預計到2030年,中國的建築業支出將達到約13兆美元,硼的前景一片光明。

- 此外,印度擁有龐大的建築業,預計將成為世界第三大建築市場。印度政府實施的智慧城市計劃、全民住宅等各項政策預計將為印度建設產業提供急需的動力。

- 此外,中國是世界領先的陶瓷生產國和消費國之一。它是世界上最大的瓷磚生產商之一,年產量約84.7億平方公尺瓷磚。國內和出口市場的激烈競爭迫使陶瓷製造商改善生產過程和產品品質。

- 根據印度儲備銀行預測,受瓷磚和衛浴設備需求激增的推動,印度陶瓷和玻璃器皿出口額將在2022年創下2,580億印度盧比(31.5億美元)的歷史新高。

- 因此,由於亞太國家終端用戶產業的蓬勃發展,預測期內對硼的需求預計也將增加。

硼行業概況

硼市場高度整合,領先公司佔據相當大的市場佔有率。市場的主要企業(不分先後順序)包括 Eti Maden、力拓、Quiborax、Allkem Limited 和青海中天硼鋰礦業。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 玻璃纖維在各終端用戶產業的應用日益廣泛

- 農業領域需求不斷成長

- 其他促進因素

- 限制因素

- 對化合物稀缺性的擔憂日益加劇

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 應用

- 玻璃

- 陶瓷

- 農業

- 清潔劑和清潔劑

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- 3M

- ALLKEM Limited

- Boron Molecular

- ETI Maden

- Gujarat Boron Derivatives Pvt. Ltd

- Minera Santa Rita SRL(MSR)

- Qinghai Zhongtian Boron Lithium Mining Co. Ltd

- Quiborax

- Rio Tinto

- SB Boron Corporation

- Searles Valley Minerals

第7章 市場機會與未來趨勢

- 陶瓷產業需求不斷成長

- 其他機會

The Boron Market size is estimated at 5.09 million tons in 2025, and is expected to reach 6.19 million tons by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

COVID-19 negatively impacted the market as all the industries halted their manufacturing processes. Lockdowns, social distances, and trade sanctions triggered massive disruptions to global supply chain networks. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

Key Highlights

- One of the major factors driving the market study is the growing adoption of fiberglass in various end-user industries. Also, increasing demand from the agriculture industry will likely boost the demand for boron during the forecast period.

- However, rising concerns regarding the scarcity of the compound are likely to restrain the market.

- The growing demand from the ceramics industry is likely to act as an opportunity for market growth in the future.

- Asia-Pacific dominated the boron market, owing to high demand from various industries like automobiles, buildings, and construction in the region.

Boron Market Trends

Glass Segment to Dominate the Market

- In the glass industry, boron is particularly employed in borosilicate glass, textile-type fiberglass, and insulation-type fiberglass. With the addition of boron, glass goods are changed into materials that are resistant to heat and chemicals. The final product's fluidity, surface hardness, and durability enhance when boron is added to the intermediate molten glass product.

- In order to drastically lower the melting temperature and viscosity, prevent the glass from crystallizing, regulate thermal expansion, and prevent devitrification, glass producers add 5-20% boric oxide to the silica basis. The end products are strong enough to endure significant mechanical or thermal shock and have built-in durability and chemical resistance.

- According to the International Year of Glass 2022, around the world, there are 650 glass container manufacturers operating on 1200 sites, producing 95 million tonnes of glass annually; 320 flat glass manufacturers operating on 560 sites, producing about 106 million tonnes of flat glass annually; and 230 manufacturers operating on over 400 sites, melting nearly 8 million tonnes of glass annually for household glass/tableware.

- An astonishing 209 million tonnes of glass are produced worldwide each year by 1200 businesses across 2160 sites. Yet, these numbers do not account for secondary industries, glass fiber production, art, specialty glassware, or secondary industries.

- Hence, the glass segment will continue dominating the market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to be the largest market for boron during the forecast period owing to the growing end-user industries in China, and India, among others.

- Asia-Pacific is expected to include the largest detergent industry globally, owing to the increased awareness regarding cleanliness among middle-class families. Countries such as China and India are the top detergent producers globally.

- Boron compounds such as boric acid and borates extend the cement hydration period. Therefore, boron compounds are used effectively in the construction industry.

- The construction sector is a key player in China's continued economic development. China is amid a construction mega-boom. According to the National Bureau of Statistics of China, The value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.3 trillion (USD 4.2 trillion) in 2021. China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive outlook for boron.

- Furthermore, India has a huge construction sector and is expected to become the world's third-largest construction market. Various policies implemented by the Indian government, such as the Smart Cities project, Housing for All, etc., are expected to bring the needed impetus to the Indian construction industry.

- In addition, China is the leading producer and consumer of ceramics worldwide. It is one of the largest producers of ceramic tiles countries in the world and has produced around 8.47 billion square meters of ceramic tiles. The fierce competition in the domestic and export markets forces ceramic producers to improve their production process and product quality in the region.

- According to the Reserve Bank of India, the export of ceramics and glassware products in India for 2022 hit a record at INR 258 billion (~USD 3.15 billion) due to a surge in demand for ceramic tiles and sanitary wares.

- Hence, with the rapidly growing end-user industries in countries of the Asia-Pacific region, the demand for boron is also expected to increase over the forecast period.

Boron Industry Overview

The boron market is highly consolidated, with the major players accounting for a major market share. Some of the major companies in the market (not in any particular order) include Eti Maden, Rio Tinto, Quiborax, Allkem Limited, and Qinhai Zhontian Boron Lithium Mining Co. Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Adoption of Fiberglass in Various End-user Industries

- 4.1.2 Increasing Demand From the Agriculture Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Rising Concerns Regarding the Scarcity of the Compound

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Glass

- 5.1.2 Ceramics

- 5.1.3 Agriculture

- 5.1.4 Detergent and Cleaning

- 5.1.5 Other Applications

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 ALLKEM Limited

- 6.4.3 Boron Molecular

- 6.4.4 ETI Maden

- 6.4.5 Gujarat Boron Derivatives Pvt. Ltd

- 6.4.6 Minera Santa Rita SRL (MSR)

- 6.4.7 Qinghai Zhongtian Boron Lithium Mining Co. Ltd

- 6.4.8 Quiborax

- 6.4.9 Rio Tinto

- 6.4.10 SB Boron Corporation

- 6.4.11 Searles Valley Minerals

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand from Ceramics Industry

- 7.2 Other Opportunities