|

市場調查報告書

商品編碼

1689882

聚醚胺:市場佔有率分析、產業趨勢與成長預測(2025-2030)Polyetheramine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

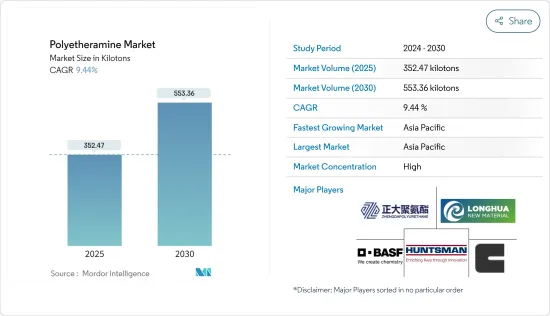

聚醚胺市場規模預計在 2025 年為 352.47 千噸,預計在 2030 年達到 553.36 千噸,預測期內(2025-2030 年)的複合年成長率為 9.44%。

聚醚胺市場受到了 COVID-19 疫情的負面影響。不過,2021年市場已經明顯復甦。預計到 2022 年和 2023 年,市場將恢復到接近疫情前的水平,這得益於汽車、建築和航太等各個終端用戶產業的消費成長。

主要亮點

- 在預計預測期內,黏合劑和密封劑行業投資的增加以及複合材料對聚醚胺的需求的增加將推動市場成長。

- 然而,預計與聚醚胺相關的環境問題和健康危害將在預測期內阻礙市場成長。

- 此外,鋰離子電池產業的新商機有望創造市場機會。

- 亞太地區是最大的市場,預計未來幾年將成長最快,這得益於中國、印度和日本等國家的消費不斷成長。

聚醚胺市場趨勢

複合材料應用需求不斷成長

- 聚醚胺是一種典型的固化劑,由聚醚和胺分子組成,用於增強最終產品,例如柔韌性、疏水性、親水性和韌性。

- 聚醚胺廣泛應用於複合材料應用,因為其獨特的性能提供了強度和柔韌性之間的關鍵平衡。

- 此外,聚醚胺基複合材料正在被設計為木材、金屬和混凝土的替代品。其輕量化設計、高介電強度和高抗環境劣化性能使其可用於航太、汽車零件和風力發電機葉片等要求嚴格的應用。

- 汽車產業是複合材料領域的主要貢獻者。根據國際汽車製造商協會(OICA)報告,預計2023年全球汽車產量將達到約9,354萬輛,高於2022年的8,483萬輛,成長率約10.26%。

- 中國仍然是全球汽車市場的主導者,在銷售和製造方面都處於領先地位。根據預測,2025年國內產量將達3,500萬輛。根據中國工業協會的資料,2023年中國汽車產量將超過3,016萬輛,與前一年同期比較增加11.6%。

- 美國是世界第二大汽車生產國。該國擁有主要的汽車製造商,不僅生產汽車,還向美洲、歐洲和亞太地區出口汽車。國際汽車工業組織(OICA)指出,美國汽車產量將從2022年的10,052,958輛增加到2023年的10,611,555輛。

- 根據美國能源局的數據,到 2022 年,風電將占美國新增電力容量的 22%。拜登總統的通膨控制法案將使 2026 年陸上風電裝置容量預計成長近 60%,從 11.5 吉瓦增至 18 吉瓦,足以為另外 200 萬戶家庭供電。

- 總體而言,預計這些因素將在預測期內推動該應用對聚醚胺的需求。

亞太地區佔市場主導地位

- 預計預測期內亞太地區將主導聚醚胺市場。由於風力發電、建築和建築應用的需求不斷增加,中國和印度等國家對聚醚胺的需求也在增加。

- 聚醚胺廣泛用作黏合劑,將葉片的兩個部分黏合在一起,並用作風力發電機葉片複合材料的添加劑。預計在預測期內,風力發電應用對聚醚胺的高需求將推動市場發展。

- 中國電力委員會預測,到2024年,中國的風電裝置容量將達到530吉瓦(GW)。透過在內蒙古、新疆、甘肅和沿海地區計劃,中國的目標是到2025年增加371吉瓦的裝置容量,將使全球風電容量增加近50%。

- 根據中國電力企業聯合會預測,2023年中國風電裝置容量將達440吉瓦,與前一年同期比較增加16.9%。這一成長不僅凸顯了中國在風力發電的領導地位,也增加了渦輪葉片製造對聚醚胺的需求。

- 到2024年,印度的經濟適用住宅預計將增加70%。據投資印度 (Invest India) 稱,到 2025 年,建築業的估值預計將達到 1.4 兆美元。預計到 2030 年,超過 30% 的人口將成為居住者,因此迫切需要超過 2,500 萬套中型和經濟適用住宅。最近的改革,如《房地產法》、《商品及服務稅》和《房地產投資信託》旨在加快核准速度、加強建設產業並刺激市場成長。

- 財政部長宣布將 Pradhan Mantri Awas Yojana 計畫的支出增加 66%,達到 7,900 億印度盧比(約 218.1 億美元),為 2023-2024 年預算中的經濟適用住宅提供大力推動。

- 亞洲是世界上最大的汽車製造地。特別是在中國,由於各種環境問題,許多政府計畫正在推動擺脫石化燃料,因此電動車的發展預計將繼續獲得動力。

- 汽車產業越來越注重減輕車輛重量,以提高燃油效率和排放氣體。聚醚胺用於複合材料中,以取代較重的傳統材料,支持汽車輕量化設計的趨勢。隨著中國汽車產量的成長,此類複合材料應用的需求預計將激增,進一步推動聚醚胺市場的發展。

- 根據國際貿易管理局(ITA)的數據,中國仍然是全球最大的汽車市場,無論按年銷售量或產量計算。預計2025年本土產量將達3,500萬輛。 2023年,中國汽車製造業取得了重要里程碑,創下了汽車產銷新高。根據中國工業協會的報告,2023年中國汽車產量將超過3,016萬輛,與前一年同期比較去年同期成長11.6%。

- 上述因素加上政府的支持,將推動預測期內對聚醚胺的需求增加。

聚醚胺產業概況

聚醚胺市場本質上是整合的。市場的主要企業(不分先後順序)包括亨斯邁國際有限責任公司、BASF歐洲公司、科萊恩、山東龍華新材料和淄博正大聚氨酯。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 增加對黏合劑和密封劑產業的投資

- 複合材料對聚醚胺的需求不斷成長

- 限制因素

- 過量使用聚醚胺引發的環境問題

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 類型

- 單胺

- 二胺

- 三胺

- 應用

- 聚脲

- 燃料添加劑

- 複合材料

- 環氧漆

- 黏合劑和密封劑

- 其他用途(殺蟲劑、印刷油墨添加劑、顏料分散體)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 併購、合資、合作與協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- BASF SE

- Clariant

- Huntsman International LLC

- Qingdao IRO Surfactant Co., Ltd.

- Shandong Longhua New Materials Co., Ltd.

- Wuxi Akeli Technology Co., Ltd.

- Yangzhou Chenhua New Materials Co., Ltd.

- Yantai Dasteck Chemicals Co., Ltd.

- Zibo Zhengda Polyurethane Co., Ltd.

第7章 市場機會與未來趨勢

- 鋰離子電池產業的新機會

The Polyetheramine Market size is estimated at 352.47 kilotons in 2025, and is expected to reach 553.36 kilotons by 2030, at a CAGR of 9.44% during the forecast period (2025-2030).

The polyetheramine market was negatively impacted by the COVID-19 pandemic. However, the market recovered significantly in 2021. In 2022 and 2023, the market has almost returned to pre-pandemic levels, owing to rising consumption from various end-user industries such as automotive, construction, aerospace, and others.

Key Highlights

- The increasing investments in the adhesive and sealant industry and the growing demand for polyetheramine from composites are expected to drive market growth during the forecast period.

- On the other hand, environmental concerns and health hazards associated with polyetheramine are expected to hinder the growth of the market during the forecast period.

- Further, emerging opportunities in the lithium-ion battery industry are projected to create market opportunities.

- The Asia-Pacific region is the biggest market and is expected to grow the fastest over the next few years owing to the increasing consumption from countries such as China, India, and Japan.

Polyetheramine Market Trends

Increasing Demand from Composite Application

- Polyetheramines are typical curing agents that comprise polyether and amine molecules and are used to enhance the properties of end products, such as flexibility, hydrophobicity, hydrophilicity, and toughness.

- Due to their unique properties, polyetheramines are widely used in composite applications as they provide a critical balance between strength and flexibility.

- Furthermore, polyether amine-based composites are designed to replace wood, metal, and concrete. Owing to their lightweight design, high dielectric strength, and high resistance to environmental degradation, they are useful in highly demanding applications such as aerospace, automotive parts, and wind turbine blades.

- The automotive industry significantly contributes to the composites segment. The Organisation Internationale des Constructeurs d'Automobiles (OICA) reported that global vehicle production in 2023 reached approximately 93.54 million, up from ~84.83 million in 2022, marking a growth rate of about 10.26 percent.

- China remains the dominant player in the global vehicle market, leading in both sales and manufacturing. Projections indicate domestic production will hit 35 million vehicles by 2025. Data from the China Association of Automobile Manufacturers shows that in 2023, China's car output surpassed 30.16 million units, reflecting an 11.6 percent year-on-year increase.

- The United States ranks as the second-largest automobile manufacturer worldwide. The nation boasts major automakers that not only produce but also export vehicles across the Americas, Europe, and the Asia-Pacific. The International Organization of Motor Vehicle Manufacturers (OICA) noted that U.S. vehicle production rose from 10,052,958 units in 2022 to 10,611,555 in 2023.

- According to the U.S. Department of Energy, wind power constituted 22% of the nation's new electricity capacity in 2022. Due to President Biden's Inflation Reduction Act, projections for land-based wind energy installations in 2026 have jumped nearly 60%, from 11,500 MW to 18,000 MW, enough to power an extra two million homes.

- Overall, all such factors are expected to boost the demand for polyetheramine in this application over the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for polyetheramine during the forecast period. In countries like China and India, owing to the increasing demand for wind energy and construction & building applications, the demand for polyetheramine has been increasing in the region.

- Polyetheramine is widely used as an additive in adhesives to adhere to two parts of blades and in composites used in wind turbine blades. A high demand for polyetheramine in wind energy applications will propel its market during the forecast period.

- China Electricity Council (CEC) forecasts that China will reach a wind power capacity of 530 gigawatts (GW) by 2024. With projects in Inner Mongolia, Xinjiang, Gansu, and coastal regions, China aims to add 371 GW by 2025, potentially expanding the global wind fleet by nearly 50%.

- In 2023, China's wind power capacity hit 440 GW, marking a 16.9% growth from the prior year, as reported by the CEC. This surge not only underscores the nation's leadership in wind energy but also amplifies the demand for polyetheramine in turbine blade manufacturing.

- In 2024, India is set to witness a 70% surge in the availability of affordable housing. According to Invest India, the construction sector is projected to attain a valuation of USD 1.4 trillion by 2025. With forecasts suggesting that over 30% of the population will be urban dwellers by 2030, there's a pressing need for 25 million more mid-end and affordable housing units. Recent reforms, such as the Real Estate Act, GST (Goods and Services Tax), and REITs (Real Estate Investment Trusts), aim to expedite approvals and strengthen the construction industry, driving market growth.

- The Finance Minister announced a significant 66% increase in the outlay for Pradhan Mantri Awas Yojana, raising it to over INR 7,90,000 million (~USD 21,810 million), marking a substantial boost for affordable housing in the 2023-2024 Budget.

- Asia is the largest automotive manufacturing hub in the world. The development of electric vehicles is expected to continue to gain momentum in the future, especially in China, where many government programs are promoting the move away from fossil fuels owing to various environmental concerns.

- The automotive industry is increasingly focused on reducing vehicle weight to improve fuel efficiency and reduce emissions. Polyetheramines are used in composite materials that replace heavier traditional materials, thus supporting the trend toward lightweight automotive designs. With vehicle production on the rise in China, the demand for these composite applications is set to surge, further propelling the polyetheramine market.

- According to the International Trade Administration (ITA), China remains the world's biggest car market, both in terms of yearly sales and production. Local manufacturing is anticipated to hit 35 million vehicles by 2025. In 2023, China's car manufacturing sector achieved a significant milestone, setting new car production and sales records. In 2023, China's car production surpassed 30.16 million vehicles, marking an increase of 11.6% compared to the previous year, as reported by the China Association of Automobile Manufacturers (CAAM).

- The aforementioned factors, coupled with government support, are contributing to the increasing demand for polyetheramine during the forecast period.

Polyetheramine Industry Overview

The polyetheramine market is consolidated in nature. Some of the major players in the market (not in any particular order) include Huntsman International LLC, BASF SE, Clariant, Shandong Longhua New Materials Co., Ltd., and Zibo Zhengda Polyurethane Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Investments in the Adhesives and Sealants Industry

- 4.1.2 Growing Demand for Polyetheramine from Composites

- 4.2 Restraints

- 4.2.1 Environmental Concern Due to Excessive Use of Polyetheramines

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Monoamine

- 5.1.2 Diamine

- 5.1.3 Triamine

- 5.2 Application

- 5.2.1 Polyurea

- 5.2.2 Fuel Additives

- 5.2.3 Composites

- 5.2.4 Epoxy Coatings

- 5.2.5 Adhesives and Sealants

- 5.2.6 Other Applications (agrochemicals, printing ink additives, and pigment dispersions)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Clariant

- 6.4.3 Huntsman International LLC

- 6.4.4 Qingdao IRO Surfactant Co., Ltd.

- 6.4.5 Shandong Longhua New Materials Co., Ltd.

- 6.4.6 Wuxi Akeli Technology Co., Ltd.

- 6.4.7 Yangzhou Chenhua New Materials Co., Ltd.

- 6.4.8 Yantai Dasteck Chemicals Co., Ltd.

- 6.4.9 Zibo Zhengda Polyurethane Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Opportunity In The Lithium-ion Battery Industry