|

市場調查報告書

商品編碼

1689876

工業鼓:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Industrial Drums - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

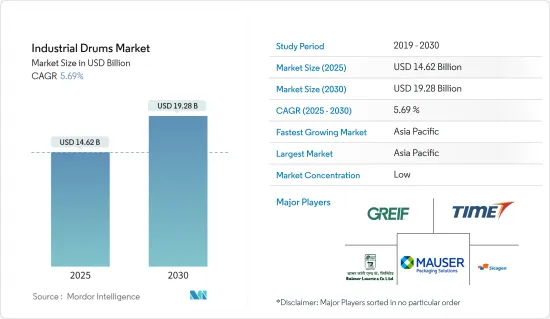

工業滾筒市場規模預計在 2025 年為 146.2 億美元,預計到 2030 年將達到 192.8 億美元,預測期內(2025-2030 年)的複合年成長率為 5.69%。

主要亮點

- 化學和石化潤滑劑市場對工業桶的需求日益增加。它的吸引力在於其堅固性、阻氣性和易用性,預計這將在預測期內推動整個產業的需求。

- 石化產業尤其強調安全包裝對保護產品的必要性。同時,新興市場的塗料、染料和油墨產量快速成長,加上對安全供應鏈的日益重視,預計將進一步刺激需求。特別是,隨著生產設施投資的增加,工業滾筒市場提供了巨大的成長機會。

- 雖然亞太地區可望主導滾筒需求,但中東和東歐等地區正日益影響全球格局,尤其是東歐地區的進步尤其顯著。例如,Mouser Packaging Solutions 於 2023 年 3 月在中國上海附近的海鹽經濟開發區開設了一家最先進的製造工廠,彰顯了這一趨勢。此舉恰逢該地區日益成長的工業包裝需求,使公司能夠滿足當前和未來的市場需求。

- 工業桶在化學品、製藥、食品和飲料等關鍵產業的中間製造過程中發揮著至關重要的作用。它們能夠實現安全高效的儲存、運輸和物料輸送,並透過確保密封性和完整性來增強生產工作流程和法規遵循。

- 此外,紙板桶在化學和化肥行業中越來越受歡迎,有助於提高生產力並降低成本。隨著化肥和化學品國際貿易的快速成長,各種工業桶的需求預計將擴大。

- 監管變化推高了工業桶的價格,影響了消費和市場成長,同時製造商擴大轉向環保包裝材料。纖維和紙板具有環保性和高可回收率,因此在各個地區迅速採用。

工業滾筒市場趨勢

化工、化肥和石油潤滑油產業的需求不斷成長,推動市場

- 工業桶在危險和非危險物質的運輸和儲存中發揮著至關重要的作用。主要用於化工、化肥、石油、油脂工業。過去十年,工業桶市場一直快速成長,這主要得益於工業產業的持續擴張和國際貿易的不斷加強。

- 根據《經濟時報》 2024 年 5 月報道,印度化學品市場價值在 2023 年為 2,200 億美元,預計到 2030 年將達到 3,830 億美元,2021 年至 2030 年的複合年成長率為 8.1%。印度是世界化學品銷售第六大國家,已成為外國直接投資 (FDI) 的磁石,2000 年 4 月至 2023 年 9 月期間共吸引了 217 億美元。該國的石油、化學和石化投資區 (PCPIR) 預計將吸引總計 4,200 億美元的投資,證實了該行業強勁的潛力,從而導致對化學桶的需求增加。

- 此外,化學工業中紙板桶的應用越來越廣泛,成為市場成長的主要驅動力。這些桶子用於裝各種產品,如黏合劑、染料甚至危險化學品,其突出特點是環保、可回收,而且通常比塑膠桶或鋼桶更具成本效益。

- 國際貨幣基金組織(IMF)根據其2024年4月《世界石油》報告預測,OPEC及其合作夥伴的石油產量將從7月起逐步增加。這項轉變將使沙烏地阿拉伯再次躋身世界成長最快的經濟體之列。國際貨幣基金組織預測,沙烏地阿拉伯的石油產量到2025年初將升至1000萬桶/日,而目前,其產量徘徊在三年來的最低水平,約為900萬桶/日。值得注意的是,沙烏地阿拉伯聲稱其石油產能約為1,200萬桶/日,這一水準在過去十年中基本保持不變。

- 此外,化學和化肥行業擴大使用紙板桶來提高生產力並降低成本。隨著各國之間化肥和化學品貿易的激增,包括石油潤滑油行業在內的各個行業對桶的需求預計將成長。

亞太地區佔最大市場佔有率

- 亞太地區的工業和製造業正在經歷快速發展,對工業滾筒的興趣日益濃厚。這種轉變是由製造商向中國、印度和印尼等新興經濟體的擴張所推動的。尤其是中國紙板桶產量成長迅速,金額已超過馬來西亞、新加坡等國家。

- 認知到對精緻包裝的需求,本地和領先的製造商正在提高紙板桶的品質。零售業的快速成長以及對可回收紙板桶等輕質、環保產品的明顯偏好進一步推動了這一趨勢。可回收紙板桶是關鍵優勢,亞太地區紙板桶市場的前景光明。

- 由於葡萄酒和植物油出口的增加,該地區的工業桶市場預計將繼續成長。尤其是包括中國和印度在內的亞洲石油出口國,更青睞工業桶而非其他散裝包裝方式。此外,這些國家的大量棕櫚油出口預計將進一步刺激對工業桶的需求。

- 亞洲國家,尤其是以製造業產出聞名的中國和印度,正在增加出口。透過採用高效的儲存、運輸和包裝解決方案可以實現這一點。例如,根據印度貿易門戶網站報道,2022-2023會計年度印度化學品和石化產品出口額為82.4億美元。如此強勁的出口量直接轉化為對容器需求的增加,對工業桶市場產生了正面影響。

- 根據印度品牌股權基金會的報告,2023年印度的工業實力生產了1.2532億噸粗鋼。如此可觀的鋼鐵產量不僅透過確保建築和維護需求的穩定供應來增強工業滾筒市場,而且在包裝行業中也發揮著至關重要的作用。鋼材的供應將為該行業提供可靠的來源,以製造耐用、可回收的包裝,促進永續發展。

工業鼓產業概況

工業桶市場的特徵是差異化、產品滲透率不斷提高、競爭日益激烈。永續的競爭優勢是透過設計、產能和應用的創新來獲得。由於最終用戶擴大採用這些產品(包括化學物質和肥料),它們的滲透率正在成長,預計在預測期內將進一步成長。市場的主要企業包括 Greif Inc.、Schutz GmbH &Co.KGaA 和 Mauser Group BV。

- 2023 年 2 月 Mouser Packaging Solutions 透過投資最先進的塑膠桶製造工廠,擴大了其在南非的產品供應。這條新生產線位於南非德班,將生產經聯合國認證的 210 公升、232 公升和 250 公升緊蓋聚乙烯桶。塑膠桶有單壁或多壁形式,非常適合化學、食品、油和潤滑劑應用。

- 2023 年 1 月為增加開口鋼桶的產量,Schutz Container Systems 正在擴大其位於美國休士頓的鋼桶製造工廠。此次擴張和服務將為當地客戶提供全新和翻新的 IBC、PE 和鋼桶的完整選擇。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 產業價值鏈分析

第5章 市場動態

- 市場促進因素

- 化工、化肥和石油潤滑油產業對工業桶的需求不斷增加

- 更重視最終用戶供應鏈能力

- 市場挑戰

- 環境惡化

- 原物料價格波動

第6章 市場細分

- 依產品類型

- 鋼桶

- 塑膠桶

- 紙板桶

- 按最終用戶產業

- 飲食

- 化學品和肥料

- 藥品

- 石油和潤滑油

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 亞洲

- 中國

- 日本

- 印度

- 澳洲和紐西蘭

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 埃及

- 北美洲

第7章 競爭格局

- 公司簡介

- Greif Inc.

- Sicagen India Ltd

- Balmer Lawre & Co. Ltd

- Time Technoplast Ltd

- Schutz GmbH & Co. KGaA

- Mauser Packaging Solutions

- TPL Plastech Limited

- Peninsula Drums

- Eagle Manufacturing Company

- US Coexcell Inc.

第8章投資分析

第9章 市場機會與未來趨勢

The Industrial Drums Market size is estimated at USD 14.62 billion in 2025, and is expected to reach USD 19.28 billion by 2030, at a CAGR of 5.69% during the forecast period (2025-2030).

Key Highlights

- Industrial drums are increasingly in demand in the chemical and petrochemical lubricants market. Their appeal lies in their robustness, gas barrier capabilities, and ease of use, which are expected to propel demand across the industry during the forecast period.

- The petrochemical sector, in particular, is emphasizing the need for secure packaging to safeguard its products. Concurrently, the surge in paints, dyes, and ink production in emerging markets, coupled with a heightened emphasis on secure supply chains, is expected to further bolster demand. Notably, as investments in production equipment rise, the industrial drum market stands to gain significant growth opportunities.

- While the APAC region is poised to dominate drum demand, regions like the Middle East and Eastern Europe are increasingly influencing the global landscape, especially with notable advancements in Eastern Europe. For example, in March 2023, Mauser Packaging Solutions underscored this trend by inaugurating a state-of-the-art manufacturing plant in China's Haiyan Economic Development Zone near Shanghai. This move aligned with the region's escalating industrial packaging needs, ensuring readiness for both current and future market demands.

- Industrial drums play a pivotal role in the intermediate manufacturing processes of key sectors like chemicals, pharmaceuticals, and food and beverages. They not only enable safe and efficient storage, transport, and handling of materials but also ensure containment and integrity, thereby enhancing production workflows and regulatory compliance.

- Furthermore, fiber drums are gaining traction in the chemical and fertilizer sectors, offering enhanced productivity and cost savings. With a surge in fertilizer and chemical trade between nations, the demand for diverse industrial drums is set to escalate.

- While regulatory changes are nudging industrial drum prices upwards, impacting consumption and market growth, manufacturers are increasingly turning to eco-friendly packaging materials. Fiber and paperboard, with their eco-conscious appeal and high recyclability rates, are witnessing a surge in adoption across regions.

Industrial Drums Market Trends

Increasing Demand from the Chemical and Fertilizers and Petroleum Lubricant Industry to Drive the Market

- Industrial drums play a pivotal role in the transportation and storage of hazardous and non-hazardous materials. They are primarily used in the chemical, fertilizer, oil, and petroleum sectors. The market for industrial drums is witnessing a surge, largely propelled by the sustained expansion of these industries and the escalating international trade over the last decade.

- As reported by The Economic Times in May 2024, the Indian chemicals market, valued at USD 220 billion in 2023, is on a trajectory to reach USD 383 billion by 2030, boasting an anticipated CAGR of 8.1% from 2021 to 2030. India, ranking sixth globally in chemical sales, has been a magnet for substantial foreign direct investments (FDI), amassing a total of USD 21.7 billion from April 2000 to September 2023. The nation's Petroleum, Chemical, and Petrochemical Investment Regions (PCPIRs) are poised to attract investments totaling USD 420 billion, underscoring the sector's robust potential and, consequently, bolstering the demand for chemical drums.

- Additionally, the chemical industry's increasing adoption of fiber drums is a significant driver of market growth. These drums, used for a variety of goods such as adhesives, dyes, and even hazardous chemicals, stand out for their eco-friendliness, being recyclable, and often a more cost-effective choice compared to their plastic and steel counterparts.

- According to a report by World Oil in April 2024, the International Monetary Fund predicts a gradual rise in oil production by OPEC and its partners starting in July. This shift is poised to propel Saudi Arabia back into the league of the world's fastest-growing economies. The IMF projects that Saudi oil production, currently hovering near a three-year low of 9 million barrels per day (MMbbl), will climb to 10 MMbbl in early 2025. Notably, Saudi Arabia asserts its production capacity stands at around 12 MMbbl, a level seldom touched in the past decade.

- Furthermore, the chemical and fertilizer industries are increasingly turning to fiber drums to enhance productivity and trim costs. With a surge in fertilizer and chemical trade between nations, the demand for various industrial drums, including those in the petroleum lubricant sector, is expected to escalate.

Asia-Pacific Accounts for the Largest Market Share

- Asia-Pacific's industry and manufacturing sector is in a phase of rapid evolution and is increasingly turning to industrial drums. This shift is driven by manufacturers expanding into emerging economies like China, India, and Indonesia. Notably, China is witnessing a surge in fiber drum production, establishing its dominance in value over countries like Malaysia and Singapore.

- Local and prominent players, recognizing the need for sophisticated packaging, are elevating the quality of fiber drums. This trend is further fueled by a burgeoning retail sector and a clear preference for lightweight, eco-friendly options like recyclable fiber drums. Their recyclability stands as a key advantage, painting a positive outlook for the Asia-Pacific fiber drums market.

- With a rising export of wines and vegetable oils, the industrial drums market in the region is poised for continued growth. Notably, Asian oil exporters, including those from China and India, favor industrial drums over other bulk packaging options. Moreover, the substantial palm oil exports from these nations are expected to further boost the demand for industrial drums.

- Asian nations, particularly China and India, known for their manufacturing output, are ramping up their export volumes. This is being facilitated by the adoption of efficient storage, transport, and packaging solutions. For instance, during FY 2022-2023, India's chemical and petrochemical exports reached USD 8.24 billion, as reported by the India Trade Portal. Such robust export figures are directly translating into heightened demand for containers, thereby positively influencing the industrial drum market.

- Highlighting India's industrial prowess, the country produced a substantial 125.32 million metric tons of crude steel in 2023, as per the India Brand Equity Foundation. This significant steel output not only bolstered the industrial drums market by ensuring a steady supply for construction and maintenance needs but also played a pivotal role in the packaging industry. With steel's availability, the industry gains a reliable source for crafting durable and recyclable packaging, furthering sustainability initiatives.

Industrial Drums Industry Overview

The industrial drums market is characterized by differentiation, growing levels of product penetration, and high levels of competition. Sustainable competitive advantage can be gained through innovation in design, capacity, and application. The penetration rates of these products grow due to their increasing adoption by end-users, including chemicals and fertilizers, and the rates are expected to grow further during the forecast period. Some of the key players in the market include Greif Inc., Schutz GmbH & Co. KGaA, and Mauser Group BV.

- February 2023: Mauser Packaging Solutions expanded its product offering in South Africa by investing in state-of-the-art plastic drum manufacturing equipment. Based in Durban, South Africa, the new line manufactures UN-certified, tight-head polyethylene barrels in sizes 210 l, 232 l, and 250 l. Plastic barrels are available in mono-layer or multi-layer formats and are ideal for chemical, food, oil, and lubricant use.

- January 2023: To increase the output of open-head steel drums, SCHUTZ Container Systems expanded its steel drum manufacturing facility in Houston, United States. This expansion and service offering provide local customers with a complete selection of new and reconditioned IBCs, PE, and steel drums.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Industrial Drum from the Chemical and Fertilizers and Petroleum Lubricant Industry

- 5.1.2 Increasing Focus on Strengthening Supply Chain Capabilities Among End Users

- 5.2 Market Challenges

- 5.2.1 Environmental Degradation

- 5.2.2 Fluctuating Raw Material Price

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Steel Drum

- 6.1.2 Plastic Drum

- 6.1.3 Fiber Drum

- 6.2 By End-user Industry

- 6.2.1 Food and Beverage

- 6.2.2 Chemicals and Fertilizers

- 6.2.3 Pharmaceuticals

- 6.2.4 Petroleum and Lubricants

- 6.2.5 Other End User Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.5.1 Brazil

- 6.3.5.2 Mexico

- 6.3.6 Middle East and Africa

- 6.3.6.1 United Arab Emirates

- 6.3.6.2 Saudi Arabia

- 6.3.6.3 South Africa

- 6.3.6.4 Egypt

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Greif Inc.

- 7.1.2 Sicagen India Ltd

- 7.1.3 Balmer Lawre & Co. Ltd

- 7.1.4 Time Technoplast Ltd

- 7.1.5 Schutz GmbH & Co. KGaA

- 7.1.6 Mauser Packaging Solutions

- 7.1.7 TPL Plastech Limited

- 7.1.8 Peninsula Drums

- 7.1.9 Eagle Manufacturing Company

- 7.1.10 U.S. Coexcell Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球工業鼓市場

全球工業鼓市場 2032 年工業桶市場預測:按產品、類型、產能、最終用戶和地區進行的全球分析

2032 年工業桶市場預測:按產品、類型、產能、最終用戶和地區進行的全球分析 工業桶市場機會、成長動力、產業趨勢分析與預測 2025 - 2034

工業桶市場機會、成長動力、產業趨勢分析與預測 2025 - 2034 2024 年至 2028 年全球倉庫鼓和桶市場

2024 年至 2028 年全球倉庫鼓和桶市場 倉儲桶的全球市場規模:按產品、按應用、按地區、範圍和預測

倉儲桶的全球市場規模:按產品、按應用、按地區、範圍和預測