|

市場調查報告書

商品編碼

1689874

無菌醫療包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Sterile Medical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

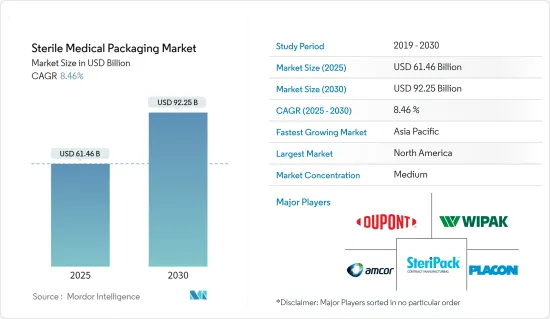

預計 2025 年無菌醫療包裝市場規模為 614.6 億美元,到 2030 年將達到 922.5 億美元,預測期內(2025-2030 年)的複合年成長率為 8.46%。

滅菌是醫療保健產業的關鍵過程。因此,無菌包裝產品和無菌屏障系統在業界變得越來越重要。無菌醫療包裝不可重複使用,可作為防止微生物感染的屏障。使用塑膠或紙張具有重量輕、可回收和耐用等優點。

主要亮點

- 醫療和製藥業對保護產品在運輸過程中免受潮濕等環境因素影響的包裝的需求日益成長。此外,對包裝技術的投資不斷增加,包括使用先進設備來提高效率,正在推動對確保醫療設備和藥品完整性和無菌性的包裝解決方案的需求。

- 塑膠材料的進步正在推動市場的發展,塑膠被用於醫療設備和消耗品,包括個人防護設備。塑膠在基本醫療用品的生產、包裝和分銷中也發揮著至關重要的作用。各製藥和醫療設備包裝製造商正在透過引入更好的無菌包裝解決方案不斷改進產品系列。

- 2024 年 1 月,全球微生物解決方案專家 Cherwell 宣布推出其突破性的 Redipor Beta Bag。這種創新的多用途塑膠袋可以降低與環境監測 (EM) 程序相關的風險、成本和時間,同時能夠持續生產無菌藥品。最近推出的轉移袋已經過全面檢驗,設計用於與隔離器和 RABS 系統中常見的 190 毫米 Getinge Alpha 端口無縫配合。這確保了債權人電鍍介質的無污染轉移,從而實現了高效生產並顯著降低了風險。

- 處方藥成本的上漲和日益成長的安全擔憂導致非處方藥(OTC)的流行。此外,疼痛、壓力和皮膚病等某些疾病的增加也導致成藥消費量的增加。成藥的需求可能會增加整個製藥業對無菌包裝的需求。

- 醫療無菌包裝產業不能容忍任何污染或感染的可能性。因此,該行業在世界範圍內受到嚴格監管,以確保產品免受污染或篡改,並準確顯示劑量、製造和有效期等關鍵資訊。但在一個病人安全至關重要的行業中,遵守管理包裝的詳細標準有時會變得過於重要。包裝法規的動態性質給該行業的製造商帶來了挑戰。

無菌醫療包裝市場趨勢

製藥業佔主要市場佔有率

- 過去幾年,全球製藥業取得了顯著成長,這主要歸功於技術進步和市場創新。根據美國國家醫學圖書館的數據,FDA 預計在 2023 年核准55 種新藥,這將推動市場成長。

- 根據世界衛生組織(WHO)的資料,2019年60歲以上人口數為10億,預計2030年將增加至14億,到2050年將增加至21億。人口老化加劇和醫療產品使用率高推動了製藥業對無菌包裝的需求。癌症、糖尿病、腸道疾病等需要長期使用藥物的疾病的增加正在推動市場的成長。

- 藥品無菌包裝可確保產品在整個供應鏈中無污染、無塵且安全,進而推動市場成長。熱成型托盤、泡殼包裝和小袋等包裝有助於防止患者使用時有害細菌的傳播。

- 主要企業致力於透過無菌包裝提供最高等級的保護。杜邦公司等公司提供具有高強度和微生物阻隔性能的無菌藥品包裝,以幫助在運輸和儲存過程中保持無菌。

- 此外,根據IQVIA 2023年1月發布的報告,全球醫療保健和製藥支出不斷增加,2022年將達到約1.482兆美元。

亞太地區將經歷大幅成長

- 由於人們對醫療保健和醫療行業的關注度日益提高,預計亞太無菌包裝市場將會成長。醫療產業需求的不斷成長導致醫療設備和手術器械包裝的繁榮。

- 該地區無菌包裝產業的發展歸功於新興的滅菌技術和智慧設計的包裝解決方案推動市場成長。

- 隨著人口老化、慢性病增加以及醫療技術進步導致全球醫療保健產業持續成長,對無菌醫療設備包裝的需求也預計將相應增加。這種成長進一步受到對感染控制和患者安全的日益關注的推動,這使得醫療設備製造商優先使用無菌包裝來確保產品的完整性和無菌性。

- 對病人安全的日益關注和對一次性醫療產品的需求不斷增加,推動了對高品質無菌包裝解決方案的需求。增強耐用性和阻隔性的無菌包裝解決方案的創新也是全部區域的趨勢。

無菌醫療包裝市場概況

無菌醫療包裝市場半固體,影響市場的因素多種多樣,例如品牌識別、強大的競爭策略和透明度。由於強大的品牌意味著卓越的業績,老字型大小企業有望佔據優勢。此外,大規模投資也提高了現有企業的退出門檻,推動產業競爭更加激烈。此外,供應商也不斷提高技術力,加劇了市場競爭。該市場的參與企業包括 Amcor Group GmbH、Dupont De Nemours Inc.、Steripack Group Limited、Wipak Group 和 Placon Corporation。

- 2024 年 4 月,杜邦宣布推出Tyvek Protec PSU 即剝即貼襯墊作為新型屋頂襯墊產品。這款新產品旨在提供高性能、耐高溫和抗紫外線、防滑步行表面、易於使用的分隔襯墊、ICC-ES 代碼報告和著名的 FL/Miami-Dade 認證。

- 2024 年 2 月, 頻譜宣布計劃擴建其哥斯達黎加工廠,以包括無菌杜邦Tyvek醫療包裝能力並加強其醫療導管業務。埃雷迪亞工廠面積從 36,000 平方英尺擴建至 52,000 平方英尺旨在提高生產能力並加快服務交付速度。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 當前地緣政治情勢如何影響市場

第5章市場動態

- 市場促進因素

- 預計嚴格的感染控制法規將推動對無菌產品的需求

- 近期產能增加

- 塑膠領域的材料進步

- 市場挑戰

- 法規的動態性質要求製造商解決造成材料供應問題的當地因素

第6章市場區隔

- 依材料類型

- 塑膠

- 聚丙烯(PP)

- 聚酯纖維

- 聚苯乙烯(PS)

- 聚氯乙烯(PVC)、高密度聚苯乙烯(HDPE)等。

- 紙和紙板

- 玻璃

- 其他材料

- 塑膠

- 依產品類型

- 熱成型托盤

- 無菌瓶子和容器

- 袋子和包包

- 泡殼包裝

- 管瓶和安瓿瓶

- 預填充式注射器

- 裹

- 按應用

- 製藥

- 手術和醫療器械

- 體外診斷(IVD)

- 其他用途

- 按滅菌類型

- 化學滅菌

- 放射線殺菌

- 壓力和溫度滅菌

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- Amcor Group GmbH

- Dupont De Nemours Inc.

- Steripack Group Limited

- Wipak Group

- Placon Corporation

- Riverside Medical Packaging Company Ltd

- Tekni-Plex Inc.

- BillerudKorsnas AB

- Sonoco Products Co

- DWK Life Sciences

- Technipaq Inc.

- 3M Company

- Nelipak Healthcare Packaging

- Oliver Healthcare Packaging

- Beacon Converting Inc.

- Paxxus Inc.

- Spectrum Plastics Group

- Sterimed Holdings SaS

- Sigma Medical Supplies Corporation

- Charter Next Generation

- Berry Global Inc.

- Sealed Air Corporation

第8章 市場展望

The Sterile Medical Packaging Market size is estimated at USD 61.46 billion in 2025, and is expected to reach USD 92.25 billion by 2030, at a CAGR of 8.46% during the forecast period (2025-2030).

Sterilization is an important processing step in the healthcare industry. Therefore, sterile packaging products or sterile barrier systems are becoming increasingly important in the industry. Sterile medical packaging is non-reusable and acts as a barrier against microbial infection. Using plastic and paper offers lightweight, recyclability, and durability advantages.

Key Highlights

- The medical and pharmaceutical industries are experiencing a growing need for packaging to safeguard products from environmental factors like moisture while in transit. Additionally, the rising investments in packaging technologies, including the use of advanced equipment to enhance efficiency, are driving up the demand for packaging solutions that guarantee the integrity and sterility of medical devices and pharmaceuticals.

- Material advancements in plastics drive the market, using plastics in medical devices and supplies, including personal protective equipment. Plastics are also crucial in essential medical production, packaging, and distribution. Various pharmaceutical and medical device packaging manufacturers are constantly improving their product portfolio by introducing better sterile packaging solutions.

- In January 2024, global microbiology solution expert Cherwell announced the launch of the groundbreaking Redipor Beta Bag. This innovative plastic bag for multiple uses has the potential to decrease risk, expenses, and time involved in environmental monitoring (EM) procedures while continuously manufacturing sterile medicinal products. The recently introduced transfer bags have been thoroughly validated and are designed to work seamlessly with 190mm Getinge Alpha Ports commonly found in isolators and RABS systems. This ensures a contamination-free transfer of creditor-plated media, allowing for efficient production and a notable decrease in risk.

- The over-the-counter (OTC) popularity is growing because of the rising prescription drug costs and increasing concerns over safety. Further, the increase in certain disorders, such as those related to pain, stress, and skin conditions, contributes to the growing consumption of OTC drugs. The demand for OTC drugs will likely increase the demand for sterile packaging across the pharmaceutical industry.

- The medical sterile packaging sector doesn't allow any room chances for contamination and infections. Therefore, the sector is strictly regulated globally to guarantee the safety of products from contamination and tampering and to ensure that vital information regarding dosage, usage, manufacturing, expiration dates, and other details is accurately presented. However, in an industry where patient safety is paramount, following detailed criteria that control the packaging sometimes becomes overly critical. The dynamic nature of packaging regulations makes it challenging for the manufacturers in the industry.

Sterile Medical Packaging Market Trends

Pharmaceutical Sector to Hold Major Market Share

- The global pharmaceutical industry has experienced significant growth in the past years, mainly due to technological advancements and innovations in the market. According to the National Library of Medicine, the FDA approved 55 new drugs in 2023, which drives the market's growth.

- According to data from the World Health Organization, the number of people aged 60 years and older in 2019 was 1 billion, which is likely to increase to 1.4 billion by 2030 and 2.1 billion by 2050, rspectively. The demand for sterile packaging in the pharmaceutical industry is attributable to the rising aging population with high medical product use. Growth in diseases, including cancer, diabetes, and bowel diseases, requires long-term use of medicines and drugs, thus boosting the market's growth.

- The pharmaceutical sterile packaging for drugs and medicines ensures the products are contamination, dust-free, and secure during the supply chain, propelling the market growth. Packaging such as thermoform trays, blister packs, and pouches help prevent the spread of harmful germs used by patients.

- Major players strive to provide the highest level of protection through sterile packaging. Companies such as DuPont de Nemours Inc. provide pharmaceutical sterile packaging with high strength and microbial barriers to help preserve sterility during shipping and storage.

- Furthermore, according to the IQVIA report published on January 2023, global spending on medicine and pharmaceuticals is constantly growing, with approximately USD 1.482 trillion in 2022; encouragingly, the pharmaceutical and medical expenditure is expected to increase to around 1.917 trillion by 2027.

Asia Pacific to Register Major Growth

- The sterile packaging market in Asia Pacific, is estimated to rise due to the growing emphasis on the healthcare and medical industry. The rising demand for the medical industry has resulted in a boom in the packaging of medical devices and surgical instruments.

- The development in the sterile packaging industry in the region is attributable to the rising advancements in sterilization technologies and intelligent design packaging solutions that boost the market's growth.

- As the healthcare industry continues to grow globally, driven by an aging population, increasing prevalence of chronic diseases, and advancements in medical technology, the demand for sterile medical device packaging is expected to rise correspondingly. This growth is further driven by the heightened emphasis on infection control and patient safety, prompting medical device manufacturers to prioritize the use of sterile packaging to ensure the integrity and sterility of their products.

- Increasing emphasis on patient safety and rising demand for single-use medical products has resulted in a growing demand for high-quality sterile packaging solutions. Technological innovation in sterile packaging solutions with enhanced durability and barrier properties is also trending across the region.

Sterile Medical Packaging Market Overview

The sterile medical packaging market is semi-consolidated with various factors affecting the market, such as brand identity, powerful competitive strategy, and degree of transparency. Strong brands are synonymous with good performance, so long-standing players are expected to have the upper hand. Moreover, the involvement of large-scale investment also increases the barriers to exit for existing players, thereby pushing the industry toward improved competition. Additionally, vendors are enhancing their technological capabilities, thereby intensifying market competition. Some of the players in the market are Amcor Group GmbH, Dupont De Nemours Inc.,Steripack Group Limited, Wipak Group, Placon Corporation

- In April 2024, DuPont announced the launch of the addition of its roofing underlayment product line, the Tyvek Protec PSU peel-and-stick underlayment. The new product is designed to provide high-performance, high-temperature, and UV resistance, a slip-resistant walking surface, a split liner for easy installation, an ICC-ES code report, and prestigious FL/Miami-Dade certification.

- In February 2024, Spectrum announced plans to expand its facility in Costa Rica, incorporating sterile DuPont Tyvek medical packaging capabilities and enhancing its medical tubing operations. The expansion of the Heredia facility from 36,000 square feet to 52,000 square feet aims to increase capacity and expedite service delivery.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4 Impact of the Current Geo-political Scenarios on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Stringent Regulations Toward Infection Control Expected to Aid Demand for Sterile-based Products

- 5.1.2 Recent Increase in Utilization Capacity

- 5.1.3 Material Advancements in the Field of Plastics

- 5.2 Market Challenges

- 5.2.1 Dynamic Nature of Regulations Makes it Challenging for Manufacturers to Comply with Local Factors with Issues Related to Material Availability

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Plastic

- 6.1.1.1 Polypropylene (PP)

- 6.1.1.2 Polyester

- 6.1.1.3 Polystyrene (PS)

- 6.1.1.4 Polyvinyl Chloride (PVC), High-density Polyethylene (HDPE), etc

- 6.1.2 Paper and Paperboard

- 6.1.3 Glass

- 6.1.4 Other Material Types

- 6.1.1 Plastic

- 6.2 By Product Type

- 6.2.1 Thermoform Trays

- 6.2.2 Sterile Bottles and Containers

- 6.2.3 Pouches and Bags

- 6.2.4 Blisters Packs

- 6.2.5 Vials and Ampoules

- 6.2.6 Pre-Filled Syringes

- 6.2.7 Wraps

- 6.3 By Application Type

- 6.3.1 Pharmaceutical

- 6.3.2 Surgical and Medical Appliances

- 6.3.3 In Vitro Diagnostics (IVD)

- 6.3.4 Other Applications

- 6.4 By Sterilization Type

- 6.4.1 Chemical Sterilization

- 6.4.2 Radiation Sterilization

- 6.4.3 Pressure/Temperature Sterilization

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia

- 6.5.4 Australia and New Zealand

- 6.5.5 Latin America

- 6.5.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Dupont De Nemours Inc.

- 7.1.3 Steripack Group Limited

- 7.1.4 Wipak Group

- 7.1.5 Placon Corporation

- 7.1.6 Riverside Medical Packaging Company Ltd

- 7.1.7 Tekni-Plex Inc.

- 7.1.8 BillerudKorsnas AB

- 7.1.9 Sonoco Products Co

- 7.1.10 DWK Life Sciences

- 7.1.11 Technipaq Inc.

- 7.1.12 3M Company

- 7.1.13 Nelipak Healthcare Packaging

- 7.1.14 Oliver Healthcare Packaging

- 7.1.15 Beacon Converting Inc.

- 7.1.16 Paxxus Inc.

- 7.1.17 Spectrum Plastics Group

- 7.1.18 Sterimed Holdings SaS

- 7.1.19 Sigma Medical Supplies Corporation

- 7.1.20 Charter Next Generation

- 7.1.21 Berry Global Inc.

- 7.1.22 Sealed Air Corporation

8 MARKET OUTLOOK

醫療包裝市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、包裝類型、應用、地區和競爭格局分類,2020-2030 年預測

醫療包裝市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料、包裝類型、應用、地區和競爭格局分類,2020-2030 年預測 醫療包裝薄膜市場規模、佔有率和成長分析(按產品類型、材料類型、應用、最終用途產業和地區分類)-2025-2032年產業預測

醫療包裝薄膜市場規模、佔有率和成長分析(按產品類型、材料類型、應用、最終用途產業和地區分類)-2025-2032年產業預測 醫用包裝薄膜市場分析與預測(至2034年):按類型、產品、服務、技術、應用、材料類型、最終用戶、功能和安裝類型分類

醫用包裝薄膜市場分析與預測(至2034年):按類型、產品、服務、技術、應用、材料類型、最終用戶、功能和安裝類型分類 無菌醫療包裝市場按產品類型、滅菌方法、材料、最終用戶、應用和分銷管道分類-2025-2032年全球預測醫療包裝薄膜市場按產品類型、材料類型、應用、技術和最終用戶分類-2025-2032 年全球預測

無菌醫療包裝市場按產品類型、滅菌方法、材料、最終用戶、應用和分銷管道分類-2025-2032年全球預測醫療包裝薄膜市場按產品類型、材料類型、應用、技術和最終用戶分類-2025-2032 年全球預測 2025年全球無菌醫療包裝市場報告

2025年全球無菌醫療包裝市場報告 全球無菌醫療包裝市場:預測(至 2032 年)—按產品類型、材料類型、滅菌方法、應用、最終用戶和地區進行分析

全球無菌醫療包裝市場:預測(至 2032 年)—按產品類型、材料類型、滅菌方法、應用、最終用戶和地區進行分析 全球醫療包裝市場:2024-2031年

全球醫療包裝市場:2024-2031年 全球醫用紙市場全球醫療無菌包裝市場:未來預測(2025-2030)

全球醫用紙市場全球醫療無菌包裝市場:未來預測(2025-2030)