|

市場調查報告書

商品編碼

1689809

環氧固化劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Epoxy Curing Agent - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

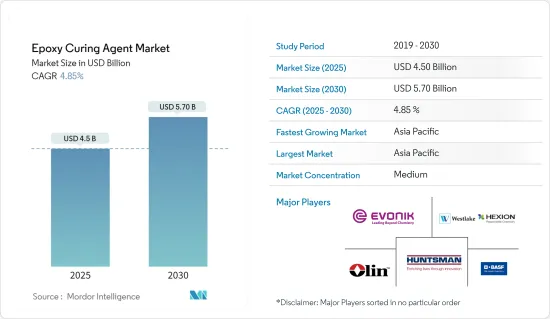

環氧硬化劑市場規模預計在 2025 年為 45 億美元,預計到 2030 年將達到 57 億美元,預測期內(2025-2030 年)的複合年成長率為 4.85%。

關鍵亮點

- 2020 年,新冠疫情對市場產生了負面影響。不過,目前市場已恢復至疫情前的水平,預計在預測期內將穩定成長。

- 建築業需求的不斷成長、新興市場對輕質複合材料的需求以及電子行業對環氧硬化劑的需求不斷成長是推動所調查市場需求的關鍵因素。

- 然而,針對胺基硬化劑的環境法規預計會阻礙市場成長。預計在預測期內,新型環保環氧硬化劑的開發將為製造商提供大量機會。

- 預計亞太地區將主導市場,其中中國和印度等國家將出現最顯著的消費趨勢。

環氧固化劑市場趨勢

油漆和塗料行業需求增加

- 環氧硬化劑用於與環氧基發生反應來固化環氧樹脂。環氧樹脂廣泛用於生產黏合劑和密封劑、油漆和被覆劑以及複合材料。

- 由於汽車、建築等領域的需求不斷成長,油漆和塗料行業在過去幾年中一直經歷著積極的成長。

- 需求的成長導致全球和國內公司在多個國家開展了多個擴張計劃,以縮小供需缺口。例如

- 2023 年 5 月,日本塗料控股公司透過其子公司日本塗料船舶塗料公司宣布將把塗料生產擴展到越南,以滿足不斷成長的市場需求。這些工廠位於越南北部、南部和中部工業帶,預計今年將開始生產船舶防腐和防護塗料。同時,預計2024-2025年船體和防污產品將加入生產線。

- 2022年7月,BASF塗料業務擴大了其位於中國南方廣東省江門市塗料基地的汽車修補被覆劑產能。隨著擴建工程的完成,BASF汽車修補漆的年產能將提升至3萬噸。

- 建築業的成長在增加油漆和被覆劑的需求方面發揮著重要作用。建設活動的增加將增加對油漆和被覆劑的需求,最終促進環氧硬化劑市場的發展。

- 根據英國土木工程師學會的數據,預計到2025年,中國、印度和美國將貢獻全球建築業擴張的近60%,推動該產業對環氧樹脂的市場需求。

- 預計所有上述因素都將在預測期內推動該行業的成長。

亞太地區佔市場主導地位

- 在亞太地區,中國憑藉其龐大的油漆和被覆劑生產基地,繼續在需求市場佔據主導地位。

- 根據歐洲塗料報告顯示,中國約有1萬家塗料製造商。儘管國內油漆和塗料製造商實力雄厚,但外資公司和合資企業也佔有相當大的市場佔有率。

- 截至2022年12月,中國塗料製造業市場規模為940億美元。 22 會計年度,印度塗料產業及相關產品出口額約 229.6 億印度盧比(2.8 億美元),高於一年前的 174.3 億印度盧比(2.1 億美元)。

- 據國家發展和改革委員會稱,中國政府已核准26 個基礎設施項目,總價值約 1,420 億美元,預計將於 2023 年完工。預計這將增加建築業對油漆和塗料的需求,從而推動環氧硬化劑市場的擴張。

- 隨著企業擴大投資建立多元化塗料生產設施,對環氧固化劑的需求正在蓬勃發展。 PPG最近決定投資1,300萬美元在中國嘉定建立一家油漆和塗料廠。投資包括安裝八條新的粉末塗料生產線和擴建粉末塗料技術中心。結果,該工廠的生產能力每年增加了8,000多噸。

- 此外,環氧樹脂廣泛用於塗覆和封裝電路元件和電子設備。根據日本電子情報技術產業協會(JEITA)統計,2022年11月電子產業總產值飆升至70.9834億美元。 2022年12月,日本電子設備出口總合達83.9545億美元。

- 在印度,對電子設備的需求激增,導致市場規模迅速擴大。 2022 年 12 月,印度電子產品出口額為 166.7 億美元,而 2021 年 12 月為 109.9 億美元。印度和中國快速發展的電子和家用電子電器產業有潛力進一步推動亞太地區的市場成長。

- 因此,預計上述因素將在預測期內推動該國環氧硬化劑市場的成長。

環氧固化劑產業概況

環氧硬化劑市場已部分整合,主要跨國公司均參與其中。研究涉及的市場主要企業包括贏創工業股份公司、亨斯邁國際有限責任公司、奧林公司、西湖公司、BASF公司等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 建築和建築業的需求增加

- 輕質複合材料的新開發

- 電子業對環氧固化劑的需求不斷成長

- 限制因素

- 胺類固化劑的環境法規

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 類型

- 胺

- 聚醯胺

- 無水

- 其他類型(醯胺胺、苯胺)

- 應用

- 複合材料

- 畫

- 黏合劑和密封劑

- 電氣和電子

- 其他用途(修理)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Atul Ltd.

- BASF SE

- Cardolite Corporation

- Epochemie-Epoxy Curing Agents

- Epoxy Division Aditya Birla Chemicals (Thailand) Limited (Aditya Birla Group)

- Evonik Industries AG

- Huntsman International LLC

- Kukdo Chemical Co. Ltd.

- Kumho P& B Chemicals Inc.

- Mitsubishi Chemical Corporation

- Olin Corporation

- Shandong Deyuan Epoxy Resin Co. Ltd.

- Toray Industries Inc.

- Westlake Corporation(Hexion)

第7章 市場機會與未來趨勢

- 新型環保低VOC或無VOC環氧固化劑的開發

- 其他機會

簡介目錄

Product Code: 68509

The Epoxy Curing Agent Market size is estimated at USD 4.50 billion in 2025, and is expected to reach USD 5.70 billion by 2030, at a CAGR of 4.85% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic had a negative impact on the market in 2020. However, the market has now reached pre-pandemic levels, and it is expected to grow at a steady pace in the forecast period.

- The increasing demand from the building and construction industry, new developments in lightweight composite materials, and growing demand for epoxy curing agents in the electronics industry are the major factors driving the demand for the studied market.

- However, environmental regulations on amine-based curing agents are expected to hinder the market's growth. Developing new eco-friendly epoxy curing agents will provide numerous opportunities for manufacturers over the forecast period.

- The Asia-Pacific region is expected to dominate the market, with the most prominent consumption trends registered in countries such as China and India.

Epoxy Curing Agent Market Trends

Increasing Demand from the Paints and Coatings Industry

- Epoxy-curing agents are used to cure epoxy resins by reacting with the epoxide groups. Epoxy resins are extensively used to manufacture adhesives and sealants, paints and coatings, and composites.

- The paints and coatings industry has been witnessing positive growth over the years owing to the increased demand from sectors like automotive, building and construction, and others.

- Such increased demand has led to several expansion projects by global and domestic players in several countries to reduce the demand and supply gap. For instance -

- In May 2023, Nippon Paint Holdings Company Ltd. announced that through its subsidiary Nippon Paint Marine Coatings Co., Ltd., the company is expanding its coatings production to Vietnam in response to the growing market demand. The facilities located in industrial zones in the north, south, and central regions of Vietnam are likely to begin the production of marine anticorrosion and protective coatings by this year. At the same time, the hull and antifouling products are set to be added to production lines by 2024-2025.

- In July 2022, BASF Coatings expanded the production capacity of automotive refinish coatings at its coatings site in Jiangmen, Guangdong Province, in South China. With the completion of the expansion, BASF's annual production capacity of automotive refinish coatings increased to 30,000 metric tons.

- The growing construction industry plays a keen role in the increasing demand for paints and coatings. The greater the increase in the number of construction activities, the greater the demand for paints and coatings, which will eventually boost the market for epoxy-curing agents.

- As per the Institution of Civil Engineers, China, India, and the United States are projected to contribute to nearly 60% of the worldwide expansion in the construction sector by 2025, consequently boosting the market demand for epoxy resins within the industry.

- All the factors mentioned above are expected to increase the industry's growth during the forecast period.

Asia-Pacific Region to Dominate the Market

- In the Asia-Pacific region, China continues to dominate in terms of demand in the market studied, which is attributed to its vast production base for paints and coatings.

- As reported by European Coatings, China hosts approximately 10,000 coatings manufacturers. Despite the significant presence of domestic paint and coatings producers, foreign companies and joint ventures also command a considerable market share.

- As of December 2022, the paint manufacturing industry in China had a market size of USD 94 billion. In FY 2022, the export value of India's paint industry and allied products was around INR 22.96 billion (USD 280 million), which increased from INR 17.43 billion (USD 210 million) in the previous year.

- As per the National Development and Reform Commission of China, the Chinese government has greenlit 26 infrastructure initiatives valued at approximately USD 142 billion, slated for completion by 2023. This is expected to drive up the need for paints and coatings in construction, consequently propelling the market expansion of epoxy curing agents.

- As companies ramp up investments in the construction of diverse coatings manufacturing facilities, the demand for epoxy curing agents is experiencing a surge. PPG recently finalized a USD 13 million investment in its paint and coatings plant situated in Jiading, China. This investment encompasses the installation of eight new powder coating production lines and the expansion of the Powder Coatings Technology Center. Consequently, the plant's capacity has been bolstered by over 8,000 metric tons annually.

- Furthermore, epoxy resins find extensive application in coating and encapsulating electrical circuit components and electronic devices. As per the Japan Electronics and Information Technology Industries Association (JEITA), the electronics industry's total production surged to USD 7,098.34 million in November 2022. Japan also exported a total of USD 8,395.45 million worth of electronics in December 2022.

- In India, the electronics market experienced a surge in demand, leading to a rapid expansion in market size. Electronic goods exports from India amounted to USD 16.67 billion in December 2022, compared to USD 10.99 billion in December 2021. The burgeoning electronics and appliances sector in both India and China has the potential to further propel market growth in the Asia-Pacific region.

- Therefore, the above-mentioned factors will provide a growing market for epoxy curing agents in the country during the forecast period.

Epoxy Curing Agent Industry Overview

The epoxy curing agents market is partially consolidated, with the presence of majorly multi-national players. The major companies of the market studied include Evonik Industries AG, Huntsman International LLC, Olin Corporation, Westlake Corporation, and BASF SE, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Building and Construction Industry

- 4.1.2 New Developments in Lightweight Composite Materials

- 4.1.3 Growing Demand for Epoxy Curing Agents in the Electronics Industry

- 4.2 Restraints

- 4.2.1 Environmental Regulations on Amine-based Curing Agents

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Amines

- 5.1.2 Polyamides

- 5.1.3 Anhydrides

- 5.1.4 Other Types (Amidoamine, Phenalkamine )

- 5.2 Application

- 5.2.1 Composites

- 5.2.2 Paints and Coatings

- 5.2.3 Adhesives and Sealants

- 5.2.4 Electrical and Electronics

- 5.2.5 Other Applications (Repairs)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Atul Ltd.

- 6.4.2 BASF SE

- 6.4.3 Cardolite Corporation

- 6.4.4 Epochemie - Epoxy Curing Agents

- 6.4.5 Epoxy Division Aditya Birla Chemicals (Thailand) Limited (Aditya Birla Group)

- 6.4.6 Evonik Industries AG

- 6.4.7 Huntsman International LLC

- 6.4.8 Kukdo Chemical Co. Ltd.

- 6.4.9 Kumho P&B Chemicals Inc.

- 6.4.10 Mitsubishi Chemical Corporation

- 6.4.11 Olin Corporation

- 6.4.12 Shandong Deyuan Epoxy Resin Co. Ltd.

- 6.4.13 Toray Industries Inc.

- 6.4.14 Westlake Corporation (Hexion)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of New Environmental Friendly Low or Non-VOC Epoxy Curing Agents

- 7.2 Other Opportunities

02-2729-4219

+886-2-2729-4219

環氧固化劑市場報告(按產品類型、應用、最終用戶和地區)2025-2033

環氧固化劑市場報告(按產品類型、應用、最終用戶和地區)2025-2033 雙氰胺市場按應用、等級、形態、分銷管道和包裝類型分類-2025-2032年全球預測環氧固化劑市場(按類型、形式、應用和最終用途產業)—2025-2030 年全球預測

雙氰胺市場按應用、等級、形態、分銷管道和包裝類型分類-2025-2032年全球預測環氧固化劑市場(按類型、形式、應用和最終用途產業)—2025-2030 年全球預測 全球 1-甲基咪唑市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測

全球 1-甲基咪唑市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測 環氧固化劑市場(按產品類型、應用和地區)

環氧固化劑市場(按產品類型、應用和地區) 環氧固化劑全球市場需求、預測分析(2018-2034)

環氧固化劑全球市場需求、預測分析(2018-2034) 全球胺固化劑市場雙氰胺市場按應用、最終用戶產業和地區分類:未來預測(2026-2032 年)

全球胺固化劑市場雙氰胺市場按應用、最終用戶產業和地區分類:未來預測(2026-2032 年) 環氧固化劑市場規模、佔有率及成長分析(按類型、應用和地區)- 產業預測 2025-2032

環氧固化劑市場規模、佔有率及成長分析(按類型、應用和地區)- 產業預測 2025-2032 雙氰胺市場報告:2030 年趨勢、預測與競爭分析

雙氰胺市場報告:2030 年趨勢、預測與競爭分析

▼