|

市場調查報告書

商品編碼

1689724

汽車溫度控管:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Automotive Thermal Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

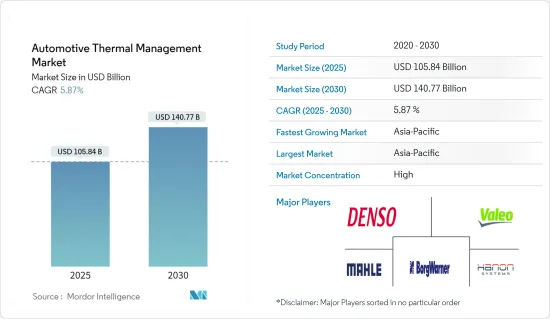

預計2025年汽車溫度控管市場規模為1,058.4億美元,2030年將達到1,407.7億美元,預測期間(2025-2030年)的複合年成長率為5.87%。

新冠疫情期間的製造業停工、封鎖和貿易限制對汽車溫度控管產業產生了不利影響。此外,汽車產量下降和勞動力短缺也對市場產生了重大影響。例如,2019年全球汽車產量下降了15.69%。 2021年,全球汽車產量與受疫情影響的2020年相比大幅成長,但仍遠低於2019年的數據,主要原因是半導體短缺。

在汽車產業,人們越來越重視對隔熱材料的需求,以提高乘坐舒適度和內部舒適度,這大大增加了對溫度控管系統的需求。車輛內部電氣和電子元件數量的不斷增加也推動了對更好的溫度控管系統進行散熱的需求。

從長遠來看,隨著汽車產業向電動車轉型,內燃機的溫度控管系統預計將完全過時。然而,隨著重型電池和大電流馬達等重型電氣元件的興起,預計這方面的需求仍將保持高位。隨著自動化和動力傳動系統電氣化的不斷提高,汽車產業對乘用車和商用車的電氣和電子元件的需求呈指數級成長。

領先的目標商標產品製造商正專注於開發溫度控管系統,為電動車提供最佳行駛里程。例如

關鍵亮點

- 2021 年 12 月,沃爾沃測試了一種新的溫度控管系統,該系統使用電氣元件和電控系統來預熱卡車的電池。該熱感系統即使在極端天氣條件下也能可靠地保持溫度,這產生了巨大的需求。

隨著汽車電氣化進程的推進,汽車供應商正在加快步伐,加強在熱能管理市場的國際競爭力。例如

關鍵亮點

- 2022年2月,博格華納公司簽署契約,為寶馬集團的iX和i4全電動架構供應高壓冷卻液加熱器(HVCH)。此解決方案控制電池的溫度控管系統和車輛的內部加熱,顯著提高電池的續航里程和可靠性。

由於亞太地區擁有主要的汽車溫度控管系統OEM、中國、印度、日本和韓國等大型汽車市場以及發達的汽車製造業,預計該地區將成為最大的市場。

由於汽車持有量高、電動和自動駕駛汽車銷量不斷成長以及汽車製造業發達,北美和歐洲預計將成為下一個最大的市場。

因此,上述因素的結合有望推動汽車溫度控管系統的成長。

汽車溫度控管市場趨勢

電池溫度控管顯著成長

採用動力傳動系統的車輛動力傳動系統電池溫度控管系統。電池在特定溫度下運行,以最大限度地提高電荷儲存和利用率。因此,在研究期間,電池電動車和插電式混合動力汽車的興起可能會推動汽車溫度控管市場的發展。例如

- 2021年,歐洲多個國家的電動車銷量均達到兩位數成長,歐洲佔全球電動車銷量的34%左右,而2020年這一比例為43%。 2021年插電式汽車總銷量約227萬輛,而2020年為137萬輛。

銷售量激增是由於各個組織和政府收緊監管標準以控制排放氣體水平並促進零排放汽車的採用。

該公司正在投資為即將推出的電池式電動車生產更有效率的電池解決方案。例如

- 2022年9月,馬勒在德國漢諾威IAA交通展上發表了商用電動車的新型溫度控管系統。

因此,預計上述因素將在預測期內顯著擴大汽車熱感系統市場。

亞太地區繼續佔據主要市場佔有率

隨著印度和中國逐漸成為西方汽車巨頭的汽車零件製造地,亞太地區汽車產業的成長預計將推動該地區溫度控管系統市場的發展。

政府法規不斷加強,鼓勵採用電動車,該地區的OEM和供應商為滿足中國汽車行業日益成長的需求而採取的強勁業務擴張,預計將為預測期內的市場成長帶來積極的前景。例如

- 2022年8月,舍弗勒集團慶祝在中國的第500萬個溫度控管模組下線。

印度汽車工業規模排名世界第四,商用車產量高居世界第七。過去五年來,該國的汽車零件業務也出現了顯著成長。

- 2022 年 3 月,總部位於艾哈默德巴德、專注於提供面向未來的永續解決方案的科技創新Start-UpsMatter 揭露了新型高速中扭力電動馬達的開發情況。根據該公司介紹,MatterDrive 1.0馬達是一種新型智慧動力傳動系統,包含多項關鍵突破,其中包括整合式智慧溫度控管系統。

此外,中國、印度、日本和韓國等國家的電動和混合動力汽車銷量正在成長,這可能會進一步擴大亞太汽車熱感系統市場。

因此,預計亞太地區在預測期內仍將是最大的汽車熱感系統市場。

汽車溫度控管產業概況

汽車溫度控管市場適度整合,大型企業佔市場主導地位。這些參與企業包括電裝公司、法雷奧、馬勒有限公司、翰昂系統和博格華納公司。這些參與企業正在積極推出新產品、建立合資企業和擴大產能,以擴大其業務活動並鞏固其市場地位。

- 2022年11月,電裝公司在澳洲雪梨舉行的客車博覽會上推出了用於客車和長途客車的新型LD9電動零排放溫度控管裝置。

- 2022年3月,Hanon Systems在中國湖西開設了一家新工廠,生產電動車的暖氣、通風和空調(HVAC)模組。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 市場限制

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 應用

- 引擎冷卻

- 座艙溫度控管

- 變速箱溫度控管

- 廢熱回收/廢氣再循環(EGR)溫度控管

- 電池溫度控管

- 馬達和電力電子的溫度控管

- 汽車模型

- 搭乘用車

- 商用車

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 其他

- 南美洲

- 中東和非洲

- 北美洲

第6章競爭格局

- 供應商市場佔有率

- 公司簡介

- Robert Bosch GmbH

- Dana Incorporated

- MAHLE GmbH

- Gentherm Incorporated

- Hanon Systems

- Denso Corporation

- BorgWarner Inc.

- Valeo Group

- Modine Manufacturing Company

- Schaeffler Technologies AG & Co. KG

- Kendrion NV

- ZF Friedrichshafen

- Aptiv Inc.

第7章 市場機會與未來趨勢

The Automotive Thermal Management Market size is estimated at USD 105.84 billion in 2025, and is expected to reach USD 140.77 billion by 2030, at a CAGR of 5.87% during the forecast period (2025-2030).

Manufacturing shutdowns, lockdowns, and trade restrictions during the COVID-19 pandemic negatively affected the automotive thermal management industry. Furthermore, the fall in automotive production and lack of labor significantly impacted the market. For instance, worldwide automobile production fell by 15.69% in 2019. Although in 2021, global automotive production increased significantly compared to the pandemic hit 2020, it was well below the figures of 2019, primarily attributed to the semiconductor shortage.

The rising need for better ride quality and heat insulation for cabin comfort is greatly emphasized in the automotive industry, leading to a much higher demand for thermal management systems. The ever-increasing number of electrical and electronic components inside vehicles also drives the need for better thermal management systems due to heat dissipation.

Over the long term, as the automotive industry moves to electric mobility, thermal management systems for IC engines are expected to go completely obsolete. However, the increasing number of heavy-duty electrical components, such as heavy-duty batteries and high-current motors, is expected to continue keeping the high demand in these aspects. With increasing automation and powertrain electrification, the demand for electrical and electronic components exponentially increased, in both passenger cars and commercial vehicles, in the automotive industry.

Major original equipment manufacturers are focusing on the development of thermal management systems to offer the best possible travel range for their electric fleet. For instance,

Key Highlights

- In December 2021, Volvo tested its new thermal management system that pre-heats a truck's batteries using electrical components and electronic control units. The thermal system ensures the temperature is maintained under extreme weather conditions, thus increasing their demand to a large extent.

Auto parts suppliers are accelerating efforts to strengthen their global competitiveness in the thermal energy management market with the advancement of vehicle electrification. For instance,

Key Highlights

- In February 2022, Borgwarner Inc. secured an agreement to supply High-Voltage Coolant Heater (HVCH) to be used in BMW Group's iX and i4 fully electric architecture. The solution controls the battery's thermal management system and cabin heating and significantly increases the driving range and reliability of the battery.

Asia-Pacific is anticipated to be the largest market due to the presence of large OEMs for automotive thermal management systems, large markets for automobiles like China, India, Japan, and South Korea, and a well-developed automobile manufacturing industry.

North America and Europe are projected to be the next biggest markets due to high vehicle ownership rates, growing electric and autonomous vehicle sales, and extensive automobile manufacturing industries.

Thus, the confluence of the aforementioned factors is anticipated to drive the growth of automotive thermal management systems.

Automotive Thermal Management Market Trends

Battery Thermal Management to Witness Significant Growth

Vehicles that run on an all-electric powertrain or hybrid powertrain require a battery thermal management system. The battery is operated under a specific temperature for maximum charge storage and utilization efficiency. Hence, the increase in battery electric vehicles or plug-in hybrid vehicles is likely to drive the automotive thermal management market during the study period. For instance,

- In 2021, many European countries witnessed double-digit growth in EV sales, whereas the European region captured around 34% of global EV sales in 2021 compared to 43% in 2020. The overall plug-in vehicle sales reached about 2.27 million units in 2021 compared to 1.37 million in 2020.

This spike in sales is the result of an increase in regulatory norms by various organizations and governments to control emission levels and propagate zero-emissions vehicles.

Companies are investing in making more efficient battery solutions for the upcoming battery electric vehicles. For instance,

- In September 2022, Mahle launched its new thermal management systems for commercial electric vehicles at IAA Transportation in Hannover, Germany.

Thus, the above factors are estimated to significantly expand the market for automotive thermal systems during the forecast period.

Asia-Pacific Continues to Capture Major Market Share

The growing automobile sector in Asia-Pacific (with India and China emerging as automotive part manufacturing hubs for the western automobile giants) is expected to drive the market for thermal management systems in this region.

The growing government regulations improving electric vehicle adoption and robust expansion adopted by OEMs and suppliers in the region to accommodate the rising demand from the automotive industry in China are expected to create a positive outlook for market growth during the forecast period. For instance,

- In August 2022, Schaeffler Group celebrated the production of five million thermal management modules in China.

The Indian automotive industry is the fourth-largest in the world, and in terms of commercial vehicle production, the country ranks seventh globally. The auto component business in the country has also increased significantly over the past five years. For instance,

- In March 2022, the development of a new high-speed mid-torque electric motor was revealed by Matter, an Ahmedabad-based technological innovation start-up focusing on delivering futuristic sustainable solutions. The company says that Matter Drive 1.0 Motor is a new intelligent drive train that includes a variety of significant breakthroughs, such as the Integrated Intelligent Thermal Management System.

In addition, rising sales of electric and hybrid vehicles in counties like China, India, Japan, and South Korea will further augment the market for automotive thermal systems in the Asia-Pacific region.

Thus, the Asia-Pacific region is predicted to remain the largest market for automotive thermal systems in the world during the forecast period.

Automotive Thermal Management Industry Overview

The automotive thermal management market is moderately consolidated, with the major players dominating the market. Some of these players include Denso Corporation, Valeo, Mahle GmbH, Hanon System, and BorgWarner Inc. These payers engage in new product launches, joint ventures, and capacity expansions to expand their business activities and cement their market position. For instance,

- In November 2022, Denso Corp. launched a new LD9 electric zero emissions thermal management unit for buses and coaches at Bus & Coach Expo in Sydney, Australia.

- In March 2022, Hanon Systems inaugurated a new plant located in Huchai, China, to manufacture heating, ventilation, and air conditioning (HVAC) modules for electrified vehicles.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Engine Cooling

- 5.1.2 Cabin Thermal Management

- 5.1.3 Transmission Thermal Management

- 5.1.4 Waste Heat Recovery/ Exhaust Gas Recirculation (EGR) Thermal Management

- 5.1.5 Battery Thermal Management

- 5.1.6 Motor and Power Electronics Thermal Management

- 5.2 Vehicle Type

- 5.2.1 Passenger Car

- 5.2.2 Commercial Vehicle

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Robert Bosch GmbH

- 6.2.2 Dana Incorporated

- 6.2.3 MAHLE GmbH

- 6.2.4 Gentherm Incorporated

- 6.2.5 Hanon Systems

- 6.2.6 Denso Corporation

- 6.2.7 BorgWarner Inc.

- 6.2.8 Valeo Group

- 6.2.9 Modine Manufacturing Company

- 6.2.10 Schaeffler Technologies AG & Co. KG

- 6.2.11 Kendrion NV

- 6.2.12 ZF Friedrichshafen

- 6.2.13 Aptiv Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

中國新能源汽車熱管理系統市場(2025-2026)

中國新能源汽車熱管理系統市場(2025-2026) 電動汽車溫度控管市場預測至2032年:按動力類型、組件、車輛類型、技術、應用和地區分類的全球分析2032 年汽車溫度控管市場預測:按車型、推進類型、零件、應用和地區分類的全球分析

電動汽車溫度控管市場預測至2032年:按動力類型、組件、車輛類型、技術、應用和地區分類的全球分析2032 年汽車溫度控管市場預測:按車型、推進類型、零件、應用和地區分類的全球分析 汽車溫度控管市場(按產品、推進系統、最終用戶、分銷管道和車輛類型)—2025 年至 2030 年全球預測

汽車溫度控管市場(按產品、推進系統、最終用戶、分銷管道和車輛類型)—2025 年至 2030 年全球預測 2025年全球電動汽車溫度控管系統市場報告電動汽車溫度控管系統市場預測(至 2032 年):按類型、組件、車輛、推進系統、銷售管道、應用和地區進行的全球分析2032 年電動車 (EV)熱感系統市場預測:按組件、車輛類型、技術、最終用戶和地區進行的全球分析電動汽車溫度控管系統市場:2034 年市場機會與策略

2025年全球電動汽車溫度控管系統市場報告電動汽車溫度控管系統市場預測(至 2032 年):按類型、組件、車輛、推進系統、銷售管道、應用和地區進行的全球分析2032 年電動車 (EV)熱感系統市場預測:按組件、車輛類型、技術、最終用戶和地區進行的全球分析電動汽車溫度控管系統市場:2034 年市場機會與策略 全球汽車溫度控管市場

全球汽車溫度控管市場 電動車用溫度控管系統的全球市場:各技術類型,用途類別,推動類別,各地區,機會,預測,2018年~2032年

電動車用溫度控管系統的全球市場:各技術類型,用途類別,推動類別,各地區,機會,預測,2018年~2032年