|

市場調查報告書

商品編碼

1689701

滴灌-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Drip Irrigation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

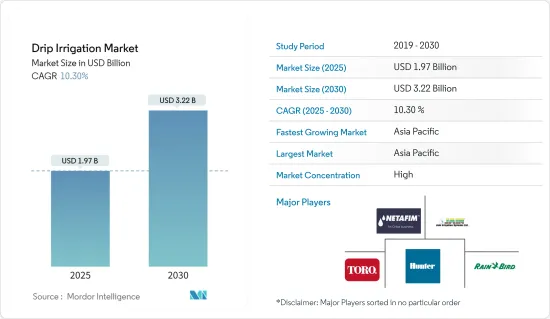

滴灌市場規模預計在 2025 年為 19.7 億美元,預計到 2030 年將達到 32.2 億美元,預測期內(2025-2030 年)的複合年成長率為 10.3%。

關鍵亮點

- 灌溉是農業和作物生產的重要組成部分。製造商已經創造了設備和技術,為農民提供最必要的滴灌系統。政府補貼和政策、技術創新以及對水資源短缺日益成長的擔憂等因素正在推動市場的發展。

- 隨著水資源短缺問題日益嚴重,滴灌系統的需求也越來越大。農民正在尋找創新思路,以便用同樣的水量種植更多的作物。預計這將促進所研究市場的成長。例如,滴灌技術的應用正在加拿大各地擴大,特別是在水資源匱乏且農業生產用水量高的省份。加拿大統計局的數據顯示,2022 年加拿大農民用於農作物灌溉的用水量與 2020 年相比增加了 23%。

- 近年來,各地採用滴灌的現像日益增加。亞太地區是滴灌產業最大的市場。亞太地區最大的滴灌市場是印度。 2021年2月,印度農業和農民福利部表示,該國淨灌溉面積為68,649,000公頃。農地微灌面積12908440公頃,其中滴灌面積6112050公頃,噴水灌溉6796390公頃。換句話說,全國只有19%的灌溉土地是微灌溉。滴灌系統可以幫助減少種植甘蔗、香蕉、秋葵、木瓜、苦瓜和其他幾種作物所需的水量高達 60%。

- 滴灌系統市場的參與企業主要市場參與者包括 Jain Irrigation Systems Limited、Netafim Limited、Toro Company 等,使得全球滴灌市場成為一個整合的市場。這些市場參與企業參與了多項策略計劃、產品開發活動和併購,促進了市場的成長。最近,Rivulis Irrigation India Ltd 和 Jain Irrigation Systems Limited 於 2022 年 6 月合併,成為全球最大的滴灌系統供應商之一。

滴灌市場趨勢

按作物類型分類,大田作物是主要部分

根據糧農組織統計,約70%的可耕地用於種植穀物。這是因為許多穀物,例如米和玉米,都是耗水量很大的作物。全球人口的成長迫使全球農民加強農作物生產,導致該領域精準灌溉的使用增加。根據糧農組織報告,預計2022年世界穀物產量將達30.596億噸,高於2020年的30.036億噸,創歷史新高。

米、小麥和玉米是世界主要種植的穀物。這些作物傳統上依靠雨水生長,但為評估灌溉的正面影響而進行的各種實地測試和研究導致對灌溉系統的需求增加。例如,2023年波蘭進行的一項研究表明,與傳統灌溉方法相比,玉米平均產量增加了25%。在同一試驗中,也實施了滴灌,結果每公頃平均產量增加了 2.35 噸,證明了這種方法的效率的重要性。

科學技術的進步使得物聯網和自動化技術在田間滴灌系統中得到應用。這樣的時刻對農民和滴灌供應商和公司很有吸引力,因為它提供了灌溉的便利性和省時的好處。政府也採取舉措,透過節約用水實現永續發展。最近,印度啟動了一項名為 PMKSY(Pradhan Mantri Krishi Sinchayi Yojana)的特別計劃,透過提高農民的用水意識和向他們提供補貼來促進精準灌溉。此外,2022年,耐特菲姆啟動了在日本旱田引進滴灌水稻種植的計劃。該系統減少了水和肥料的浪費,並鼓勵向減少甲烷排放的永續生產轉變。

亞太地區佔市場主導地位

近年來,亞太地區農業領域滴灌的應用呈現顯著成長。這主要是由於微灌計劃的擴大,減少了水資源消費量,從而增加了灌溉面積。根據印度國家計劃委員會預測,到2022-2023年,灌溉面積將達7,300萬公頃,佔印度農業用地總面積的52%。同樣,根據中國國家統計局的數據,預計2021年中國灌溉面積將達到6,961萬公頃,2022年將增加7,036萬公頃。

此外,安得拉邦的滴灌面積最多,其次是馬哈拉斯特拉邦、古吉拉突邦和旁遮普邦。為了在這些州促進有利的農業環境並實施成功的滴灌模式,Netafim 正在提供滴灌系統。 2023年,Netafim透過位於中央邦Shivpuri區的Khajuri、Kolaras和Pokhari地區的四個Better Life Farming (BLF)中心為番茄種植者提供滴灌系統。這項措施使馬哈拉斯特拉邦的番茄產量提高了 40%,並推動了滴灌系統的採用。

中國是世界上最大的滴灌設備市場和消費國之一。這主要是因為政府制定了五年計劃,要在農場引入高效節水灌溉技術和系統,到2030年至少在75%的總灌溉面積上引入微灌系統。此外,政府經常與滴灌公司合作,以增加對農民的節水設備供應。例如,2022年11月,昆明市元木地方政府與大禹灌溉集團簽署協議,以官民合作關係計劃模式合作,到2038年投放滴灌管道333萬餘公尺、滴頭120萬隻。

滴灌行業概況

全球滴灌市場正在整合,領先公司佔據大部分市場佔有率。市場上主要企業包括 Netafim Limited、Jain Irrigation Systems Limited、The Toro Company、Hunter Industries、Rain Bird Corporation 等。最常用的策略是透過在市場上推出創新新產品來擴大產品系列。其他主要企業也透過聯盟和合併鞏固了其地位。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概覽

- 市場促進因素

- 缺水威脅

- 優惠的政府政策和補貼

- 擴大灌溉應用

- 市場限制

- 初始資本投入高

- 複雜的設定可能會損害滴灌

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 應用

- 地面滴灌

- 地下滴灌

- 作物類型

- 田間作物

- 蔬菜作物

- 果園作物

- 葡萄園

- 其他

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 西班牙

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東和非洲地區

- 北美洲

第6章競爭格局

- 最受歡迎的策略

- 市場佔有率分析

- 公司簡介

- Jain Irrigation Systems Ltd

- The Toro Company

- Netafim Limited

- Rain Bird Corporation

- Chinadrip Irrigation Equipment Co. Ltd

- Antelco Pty Ltd

- TL Irrigation

- Sistema Azud

- Metzer Group

- Hunter Industries Inc.

第7章 市場機會與未來趨勢

The Drip Irrigation Market size is estimated at USD 1.97 billion in 2025, and is expected to reach USD 3.22 billion by 2030, at a CAGR of 10.3% during the forecast period (2025-2030).

Key Highlights

- Irrigation is a critical component of agriculture and crop production. Manufacturers have created equipment and techniques to provide farmers with paramount drip irrigation systems. Factors such as government subsidies and policies, technological innovations, and increasing concern over water scarcity drive the market.

- The drip irrigation system is witnessing high demand as water has increasingly become scarce. Farmers have been seeking novel ideas to grow more crops with the same quantity of water. This is anticipated to augment the growth of the market studied. For instance, the adoption of drip irrigation is growing across Canada, particularly in provinces with water scarcity and high water usage for agricultural production. According to Statistics Canada, Canadian farmers increased their water usage for crop irrigation by 23% in 2022 compared to 2020, which is majorly attributed to the drier climatic conditions in various regions throughout the country.

- In recent years, drip irrigation implementation has increased in different regions. The Asia-Pacific has the largest market for the drip irrigation industry. India is the largest market in Asia-Pacific for drip irrigation. In February 2021, the Ministry of Agriculture and Farmers Welfare, India, showed that the net irrigated area in the country is 68,649 thousand ha. The agricultural land covered under micro-irrigation is 12,908.44 thousand ha, in which drip irrigation is 6,112.05 thousand ha and sprinkler irrigation is 6,796.39 thousand ha. This means that out of the total irrigated land in the country, only 19% is under micro-irrigation. Up to 60% of water used for sugarcane, banana, okra, papaya, bitter gourd, and a few other crops could be saved if a drip irrigation system is employed for cultivation.

- The major market players operating in the drip irrigation systems market include Jain Irrigation Systems Limited, Netafim Limited, the Toro Company, etc., making the global drip irrigation market a consolidated marketplace. These market players are involved in several strategic planning, product development activities, and mergers and acquisitions, catalyzing the market's growth. Recently, in June 2022, Rivulis Irrigation India Ltd and Jain Irrigation Systems Limited merged their business and will be one of the largest global drip irrigation system providers.

Drip Irrigation Market Trends

Field Crops is the Significant Segment by Crop Type

According to the FAO, about 70% of the cultivated land was used to grow cereals, as most cereals, such as rice and maize, are water-intensive crops. The increasing global population is pressuring farmers to enhance cereal production worldwide, thus leading to the increased use of precision irrigation in this segment. As per the FAO report, world cereal production in 2022 reached a record high of 3,059.6 million metric tons from 3,003.6 million metric tons in 2020.

Rice, wheat, and maize account for the prominent cereal crops cultivated around the globe. Though these crops were grown as rainfed traditionally, results of various field trials and studies conducted to evaluate the positive impacts of irrigating these crops have strengthened the demand for irrigation systems. For instance, in a study conducted in Poland in 2023, the average yield of maize was increased by 25% compared to traditional irrigation methods. In the same experiment, fertigation through drip was also practiced, increasing the average yield by 2.35 metric tons per hectare, concluding the significance of this method's efficiency.

Advances in science and technology led to the application of IoTs and automation in drip systems at the field level. These moments attract farmers, creating a scope for drip irrigation suppliers and companies where the point of attraction is easier irrigation with no labor and time boundness. Governments are also taking initiatives for sustainable growth practices by conserving water. Recently, in India, Pradhan Mantri Krishi Sinchayi Yojana (PMKSY) is a special scheme that promotes precision irrigation practices by subsidizing and improving farmers' awareness of water use efficiency. Besides, in 2022, Netafim started an introductory rice cultivation project in dry fields in Japan using drip irrigation. The system reduces water and fertilizer waste and encourages a shift to sustainable production that reduces methane gas emissions.

Asia-Pacific Dominates the Market

The drip irrigation usage in the Asia Pacific agriculture sector witnessed significant growth during recent years, which is majorly due to the growing area under irrigation due to the expansion of micro-irrigation projects, which can reduce water consumption. In 2022-2023, the area under irrigation was expected to reach 73 million hectares, accounting for 52% of the total agricultural land, which is 41% higher than in 2016, according to the Niti Aayog. Likewise, according to the National Bureau of Statistics of China, the irrigated area in China accounted for 69.61 million hectares in 2021 and had risen by 70.36 million hectares in 2022, thereby delivering high demand for drip irrigation in the market.

Besides, the area under drip irrigation was higher in Andra Pradesh, followed by Maharashtra, Gujarat, and Punjab. To encourage a conductive farming environment and implement the successful drip irrigation model across these states, Netafim is providing drip irrigation systems. In 2023, under the initiative, Netafim provided drip irrigation systems for tomato growers through four Better Life Farming (BLF) Centers present in the Khajuri, Kolaras, and Pohari regions of the Shivpuri district in Madhya Pradesh. This initiative increased the tomato crop yield by 40%, resulting in higher adoption of drip irrigation systems in Maharashtra.

China is one of the world's largest markets and consumers of drip irrigation equipment. This is mainly attributed to the government's aim to equip farms with highly efficient water-saving irrigation technology and systems as part of its five-year plans to equip at least 75% of the total irrigated area with micro-irrigation systems by 2030. Further, The government often works with drip irrigation companies to increase the availability of water-saving equipment to farmers. For instance, in November 2022, the Local Government of Yuanmou in Yunnan Province partnered with Dayu Irrigation Group Co. Ltd, which will work together in a PPP (Public-Private Partnership) Project mode for the distribution of drip irrigation pipes of over 3.33 million meters and 1.2 million drippers till 2038.

Drip Irrigation Industry Overview

The global drip irrigation market is consolidated, with major players occupying most of the market share. Some key players in the market include Netafim Limited, Jain Irrigation Systems Limited, The Toro Company, Hunter Industries, and Rain Bird Corporation. The most adopted strategy is broadening the product portfolio by introducing new and innovative products into the market. The other prominent players are strengthening their position through partnerships and mergers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Threat of Water Scarcity

- 4.2.2 Favorable Policies and Subsidies from the Government

- 4.2.3 Increasing Adaptation of Fertigation

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Investments

- 4.3.2 Damages in Drip Irrigation Due to the Complex Set-up

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Surface Drip Irrigation

- 5.1.2 Subsurface Drip Irrigation

- 5.2 Crop Types

- 5.2.1 Field Crops

- 5.2.2 Vegetable Crops

- 5.2.3 Orchard Crops

- 5.2.4 Vineyards

- 5.2.5 Other Crops

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of the Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of the Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Jain Irrigation Systems Ltd

- 6.3.2 The Toro Company

- 6.3.3 Netafim Limited

- 6.3.4 Rain Bird Corporation

- 6.3.5 Chinadrip Irrigation Equipment Co. Ltd

- 6.3.6 Antelco Pty Ltd

- 6.3.7 T-L Irrigation

- 6.3.8 Sistema Azud

- 6.3.9 Metzer Group

- 6.3.10 Hunter Industries Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年滴灌全球市場報告

2025年滴灌全球市場報告 滴灌市場規模、佔有率、趨勢分析報告:按組件、方法、作物和區域細分的預測,2025-2030 年

滴灌市場規模、佔有率、趨勢分析報告:按組件、方法、作物和區域細分的預測,2025-2030 年 滴灌系統市場:全球 2025-2029滴水盤市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

滴灌系統市場:全球 2025-2029滴水盤市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 滴灌市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、按作物類型、按噴射器類型、按應用、按最終用戶、按地區和競爭進行細分,2020-2030 年

滴灌市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、按作物類型、按噴射器類型、按應用、按最終用戶、按地區和競爭進行細分,2020-2030 年 滴灌市場:按組成部分、類型、應用和最終用途 - 2025-2030 年全球預測全球滴灌灌水器市場

滴灌市場:按組成部分、類型、應用和最終用途 - 2025-2030 年全球預測全球滴灌灌水器市場 到 2030 年發送器市場預測:按作物類型、發送器類型、組件、材料、形狀、流量、直徑、應用、最終用戶和地區進行的全球分析

到 2030 年發送器市場預測:按作物類型、發送器類型、組件、材料、形狀、流量、直徑、應用、最終用戶和地區進行的全球分析 滴灌管市場聚乙烯,規模、佔有率、趨勢、行業分析報告:按類型、按管道類型、按地區 - 市場預測,2024-2032

滴灌管市場聚乙烯,規模、佔有率、趨勢、行業分析報告:按類型、按管道類型、按地區 - 市場預測,2024-2032 中國滴灌市場:依成分、作物、應用、最終用戶、地區、機會、預測,2017-2031年

中國滴灌市場:依成分、作物、應用、最終用戶、地區、機會、預測,2017-2031年