|

市場調查報告書

商品編碼

1689692

林業機械:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Forestry Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

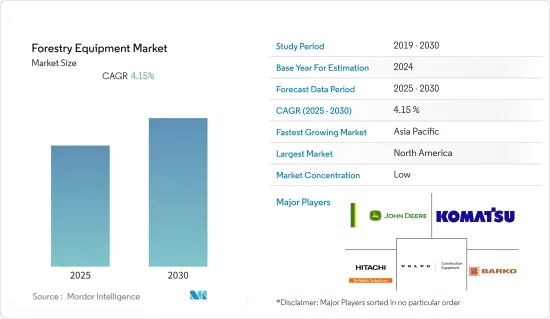

預計預測期內林業機械市場複合年成長率為 4.15%。

隨著已開發國家和新興國家對森林保護和管理的意識不斷增強,以及林業工作從手工向機械化和自動化轉變,這一市場正在成長。

關鍵亮點

- 隨著當前林業範圍的擴大,森林管理的角色正在迅速擴大,其目標是規劃和實施森林管理,並利用實踐實現特定的環境、經濟、社會和文化目標。管理目標各不相同,可能包括保護森林和自然保護區的資源保護,但主要目標往往是生產木製品。森林管理的基本概念是以木材生產為中心,以「永續採伐」為重點,即在不消耗森林蓄積量的情況下,不斷採伐增量木材。

- 這得到了政府大量投資的支持,因為健康的森林依賴健康的林產品產業。例如,2023年4月,美國政府宣布從拜登總統的兩黨基礎設施立法中撥款3,370萬美元,用於加強木製品經濟和促進永續森林管理。這項投資支持了有韌性、健康的森林與強大的農村經濟和林業部門就業之間的重要聯繫,特別是對依賴國家森林和草原的社區而言。

- 在拉丁美洲,林業因其在恢復曾經覆蓋巴西、巴拉圭和阿根廷大片地區的大西洋森林中所發揮的作用而受到重視。但五個世紀的伐木、農業擴張以及聖保羅和里約熱內盧等城市的持續發展使其支離破碎。因此,30多年來,各個組織一直致力於保護和恢復現存的文物。

- 根據聯合國統計,目前已恢復約70萬公頃森林,目標是到2030年保護和恢復100萬公頃,到2050年保護和恢復1500萬公頃。因此,預計拉丁美洲林業發展活動的增加將推動對重型林業機械的需求。

- 然而,高成本和缺乏與林業機械相關的認知預計將減緩市場成長。由於缺乏有關這些設備的資訊,它們尚未在開發中國家廣泛使用。

林業機械市場趨勢

削片機和研磨機在現場加工設備領域佔據主導地位

- 預計林業設備市場的現場加工設備部分將在整個預測期內顯著成長。這是由於用作發電廠原料的木質顆粒產量增加。

- 削片機是一種將木材變成木屑的機器。與研磨機不同,機器上的設定可產生大小均勻的碎屑。在林業中,削片機生產紙漿木材、顆粒、木柴燃料、木屑以及任何其他需要均勻削片的材料。削片機有多種配置,其典型特徵包括進料機構、一組旋轉刀、砧座和排放槽。

- 提供大規模伐木服務的伐木承包商使用森林削片機。許多企業依靠這些削片機有效率地將大樹變成木屑。世界各地快速的都市化摧毀了大片林地,為削片機創造了許多機會。根據人口實驗室預測,2022年全球都市化將達57%。北美都市化程度最高,達83%。

- 此外,種植園已成為木質能源生產的重要貢獻者,預計未來還會增加。預計用於推廣可再生能源發電廠的投資增加將促進木棧板的製造,從而推動對削片機和研磨機的需求。由於森林是木質顆粒的一級資訊來源,森林面積的擴大可能會導致對削片機的需求激增。

北美佔最大市場佔有率

- 預計北美在預測期內將出現顯著成長,主要原因是售後市場銷售的成長和向改進的伐木技術的轉變。

- 根據美國農業部的數據,美國林產品產業約佔美國製造業國內生產總值) 的 4%,每年生產超過 2,000 億美元的產品。該地區目前正在經歷木材開採活動的激增,木材和非木材林產品開採的擴大預計將為林業機械製造商提供增加產品供應的機會。

- 大量木材在建築設計中的使用越來越多,使得美國的森林管理得到了讚揚。因此,預計對木材產品(包括紙張和生質能能)的需求將激增,從而推動對一系列林業機械(如裝載機、覆蓋機和其他現場設備)的需求,以促進該地區林業的木材採伐。

- 林業是加拿大最重要的產業,對經濟和就業貢獻大。林產品總值每年超過 3.8 億加元(3.25 億美元),佔所有製成品的 10%。此外,加拿大是木材開採和生產的主要國家之一,因此伐木作業規模較大。

- 例如,2022 年末,美國北卡羅來納州伊登頓的 52 英畝原始森林被定為砍伐對象,用於採伐木材和切割原木,生產用於生質能源的木質顆粒。根據美國能源資訊署(EIA)的數據,美國2021年生產了約175億加侖生質燃料,消耗了約168億加侖。隨著生質能源發電需求的不斷成長,木質顆粒的需求也預計將大幅成長,為林業機械創造應用機會。

林業機械市場概況

林業機械市場高度細分,主要參與者包括迪爾公司、日本小松公司、沃爾沃建築設備公司 (ABVolvo)、日立建築機械 (HCM) 和 Barko Hydraulics LLC。市場參與企業正在採取夥伴關係和收購等策略來增強其產品供應並獲得永續的競爭優勢。

- 2023 年 5 月 - 小松推出了日本小松公司951XC,這是一款用於在陡坡和軟地面上進行最終砍伐的收割機。八輪設計與穩定的日本小松公司概念相結合,提供了穩定性、高效的機動性和低地面壓力。小松 951XC 也經過最佳化,可與小松 C164 搭配使用,小松 C164 是專為砍伐大樹而設計的收割機頭。此外,靜液壓傳動更容易充分利用引擎功率,在困難地形和高爬坡時具有很大的優勢。

- 2023 年 2 月 - 迪爾公司在履帶伐木裝載機系列中推出了新的中型機型。約翰迪爾新款 2956G 專為各種規模的伐木承包商而設計,對於尋求提供最佳引擎馬力和液壓功能組合,同時將機器重量保持在 90,000 磅以下的機器的客戶來說,它是理想的解決方案。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 產業價值鏈分析

- 新冠疫情和宏觀經濟趨勢對該產業的影響

第5章市場動態

- 市場促進因素

- 自動化程度提高推動林業機械需求

- 伐木公司更換老舊、低效率的林業機械

- 市場限制

- 林業機械高成本

- 缺乏林業機械資訊

第6章市場區隔

- 依產品類型

- 伐木設備

- 電鋸

- 收割機

- 伐木工

- 伐木機

- 貨運代理

- 集材機

- 其他提取設備

- 現場處理設備

- 削片機和研磨機

- 罪犯殺人狂

- 其他現場加工機器

- 其他林業機械

- 裝載機

- 穆爾徹

- 其他林業機械

- 選購零件和附件

- 鋸子、導板、鋸盤、鋸齒

- 收割頭和其他切割頭

- 其他零件和附件

- 伐木設備

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- Deere and Company

- Komatsu Ltd.

- Volvo CE(AB Volvo)

- Hitachi Construction Machinery Co. Ltd.(HCM)

- Barko Hydraulics LLC.

- Develon(HD Hyundai Infracore)

- Kesla Oyj

- Ponsse Oyj

- Rottne Industri AB.

- Eco Log Sweden AB

- Mahindra Group

- AGCO Corporation

- Caterpillar Inc.

- Kubota Corporation

- Bell Equipment Limited

第8章投資分析

第9章:市場的未來

The Forestry Equipment Market is expected to register a CAGR of 4.15% during the forecast period.

The market is growing owing to the rising awareness about forest preservation and management in several developed and developing countries and the transition in forestry operations from manual work to mechanized and automated modes of operation in forests.

Key Highlights

- With the present scope in the forest industry, the role of forest management has been growing rampantly with the aim of planning and implementing practices for the stewardship and use of forests to meet specific environmental, economic, social, and cultural objectives. While the objectives of management vary widely and include the protection of resources in protected forests and nature reserves, the primary objective has often been the production of wood products. A basic tenet of forest management has been a significant focus on wood production, which is 'sustained yield,' or harvesting the wood increment without drawing down on the forest capital.

- This has been largely supported by significant government investment as healthy forests depend on a healthy forest products industry. For instance, in April 2023, the US government announced USD 33.7 million from President Biden's Bipartisan Infrastructure Law for projecting funds to strengthen the wood products economy and promote sustainable forest management. This investment supports a crucial link between resilient, healthy forests and strong rural economies and jobs in the forestry sector, especially in communities that depend on national forests and grasslands to grow and thrive.

- In addition to this, the role of forestry is gaining prominence in Latin America to bring back the historic flourishing Atlantic Forest that once covered a vast swath of Brazil, Paraguay, and Argentina. But five centuries of logging, agricultural expansion, and the relentless growth of cities like Sao Paulo and Rio de Janeiro reduced it to fragments. Thus, various organizations have been working for more than three decades to preserve and restore what remains.

- As per the UN, approximately 700,000 ha of land have already been restored, and the goal is to protect and revive 1 million ha by 2030 and 15 million ha by 2050, an area bigger than all of Nepal, Greece, or Nicaragua. Thus, the increase in forestry maintenance activities in Latin America is expected to propel the demand for large forestry machines.

- However, the high cost and lack of awareness associated with forestry equipment is expected to slow down the growth of the market. Due to the lack of information about the equipment, the adoption is still not widespread in developing countries.

Forestry Equipment Market Trends

Chippers and Grinders to be the Largest On-site Processing Equipment Segment

- The on-site processing equipment segment within the forestry equipment market is projected to experience substantial growth throughout the forecast period. This can be attributed to the escalating production of wood pellets utilized as feedstock for power plants.

- Chippers are machines that can reduce trees into wood chips. They are distinct from grinders in that they generate chips of uniform size, contingent upon the equipment settings. Within the forestry industry, chippers produce material for pulpwood, pellets, hog fuel, landscaping, and any other application that necessitates uniform chips. Chippers are available in a diverse range of configurations, and their typical features comprise a feed mechanism, a set of rotating knives, an anvil, and a discharge chute.

- Lean clearing contractors employ forestry chippers and those providing large-scale tree-clearing services. Many contractors rely on these chippers to effectively reduce large trees into wood chips. Rapid urbanization worldwide destroyed vast forested areas, creating numerous opportunities for using chippers. According to the Population Reference Bureau, worldwide urbanization was 57% in 2022. North America registered the highest degree of urbanization, with 83%.

- Furthermore, it is anticipated that forest plantations may emerge as significant contributors to the production of wood energy, with a projected increase in the future. Escalating investments in promoting renewable power plants are expected to boost the manufacture of wooden pallets, thereby driving the demand for chippers and grinders. Since forests are the primary source of wooden pellets, expanding forest areas is likely to result in a surge in chipper demand.

North America Holds Largest Market Share

- North America is anticipated to experience significant growth during the projected period, primarily due to the rising aftermarket sales and the shift toward modified cut-to-length logging techniques in the region.

- As per the United States Department of Agriculture, the forest products industry in the United States contributes to roughly 4% of the nation's overall manufacturing Gross Domestic Product (GDP), generating an excess of USD 200 billion in products annually. The area is currently experiencing a surge in timber extraction activities, and the escalating extraction of both timber and Non-timber forestry products is anticipated to present opportunities for Forestry equipment manufacturers to augment their product offerings.

- The escalating use of mass timber in architectural design is propelling commendable forest management practices in the United States. The consequent surge in demand for wood products, including paper and biomass for energy, is anticipated to stimulate the need for various forestry equipment, such as loaders, mulchers, and other on-site equipment, to facilitate timber harvesting in the region's forest industry.

- Canada's foremost industry is forestry, with significant economic and employment contributions. Forest products' total worth surpasses CAD 38000 million (USD 32500 million) annually, representing 10% of all manufactured goods. Additionally, Canada ranks among the leading nations in timber extraction and production, resulting in extensive logging operations.

- For instance, in late 2022, a 52-acre indigenous woodland located in Edenton, North Carolina, United States, was subjected to clear-cutting for the purposes of timber harvesting and the chipping of whole trees to produce wood pellets for bioenergy. According to the Energy Information Administration (EIA), approximately 17.5 billion gallons of biofuels were manufactured in the United States in 2021, with approximately 16.8 billion gallons being consumed. As the demand for bioenergy generation continues to increase, the requirement for wood pellets is expected to escalate significantly, thereby creating opportunities for the application of forestry equipment.

Forestry Equipment Market Overview

The forestry equipment market is highly fragmented, with the presence of major players like Deere and Company, Komatsu Ltd., Volvo CE (AB Volvo), Hitachi Construction Machinery Co. Ltd. (HCM), and Barko Hydraulics LLC. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- May 2023 - Komatsu launched the Komatsu 951XC, a harvester for final logging in steep terrain and on soft ground. The eight-wheel design, integrated with the stable Komatsu concept, ensures a machine with stability, efficient maneuverability, and low ground pressure. The Komatsu 951XC is also optimized with the Komatsu C164 - a harvester head specially designed for logging large trees. Further, the hydrostatic transmission facilitates engine power to be utilized entirely, providing considerable advantages in difficult terrain and enhanced climbing ability.

- February 2023 - Deere and Company introduces a new mid-size model to its line-up of crawler log loaders. It is designed for logging contractors of all sizes; John Deere's new 2956G is an ideal solution for customers looking for a machine that provides the best combination of engine horsepower and hydraulics capability while maintaining a machine weight of less than 90,000 lbs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 and Macro Economic Trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Automation to Boost the Forestry Equipment Demand

- 5.1.2 Replacement of Older, Less Productive Forestry Machinery by Logging Firms

- 5.2 Market Restraints

- 5.2.1 High Cost of Forestry Equipment

- 5.2.2 Lack of Information About Forestry Equipment

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Felling Equipment

- 6.1.1.1 Chainsaws

- 6.1.1.2 Harvesters

- 6.1.1.3 Feller Bunchers

- 6.1.2 Extracting Equipment

- 6.1.2.1 Forwarders

- 6.1.2.2 Skidders

- 6.1.2.3 Other Extracting Equipment

- 6.1.3 On-Site Processing Equipment

- 6.1.3.1 Chippers and Grinders

- 6.1.3.2 Delimbers and Slashers

- 6.1.3.3 Other On-Site Processing Equipment

- 6.1.4 Other Forestry Equipment

- 6.1.4.1 Loaders

- 6.1.4.2 Mulchers

- 6.1.4.3 Other Forestry Equipment

- 6.1.5 Separately Sold Parts and Attachments

- 6.1.5.1 Saw Chain, Guide Bars, Discs, and Teeth

- 6.1.5.2 Harvesting and Other Cutting Heads

- 6.1.5.3 Other Parts and Attachments

- 6.1.1 Felling Equipment

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Deere and Company

- 7.1.2 Komatsu Ltd.

- 7.1.3 Volvo CE (AB Volvo)

- 7.1.4 Hitachi Construction Machinery Co. Ltd. (HCM)

- 7.1.5 Barko Hydraulics LLC.

- 7.1.6 Develon (HD Hyundai Infracore)

- 7.1.7 Kesla Oyj

- 7.1.8 Ponsse Oyj

- 7.1.9 Rottne Industri AB.

- 7.1.10 Eco Log Sweden AB

- 7.1.11 Mahindra Group

- 7.1.12 AGCO Corporation

- 7.1.13 Caterpillar Inc.

- 7.1.14 Kubota Corporation

- 7.1.15 Bell Equipment Limited

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026-2030年全球木片製造機市場

2026-2030年全球木片製造機市場 林業機械市場規模、佔有率及成長分析(依設備類型、驅動方式、操作模式、最終用戶及地區分類)-2026-2033年產業預測

林業機械市場規模、佔有率及成長分析(依設備類型、驅動方式、操作模式、最終用戶及地區分類)-2026-2033年產業預測 林業機械市場依產品類型、動力來源、材料及地區分類

林業機械市場依產品類型、動力來源、材料及地區分類 木材削片機 - 全球市場佔有率和排名、總銷售量和需求預測(2025-2031 年)

木材削片機 - 全球市場佔有率和排名、總銷售量和需求預測(2025-2031 年) 2025年林業機械全球市場報告

2025年林業機械全球市場報告 全球林業機械市場全球木材分割機市場全球伐木集材機市場

全球林業機械市場全球木材分割機市場全球伐木集材機市場 全球林業設備市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及預測(2025 年至 2033 年)

全球林業設備市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及預測(2025 年至 2033 年) 柴火劈柴機市場規模、佔有率和成長分析(按產品類型、燃料類型、產能、最終用途和地區)- 產業預測 2025-2032

柴火劈柴機市場規模、佔有率和成長分析(按產品類型、燃料類型、產能、最終用途和地區)- 產業預測 2025-2032