|

市場調查報告書

商品編碼

1687985

物聯網專業服務-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)IoT Professional Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

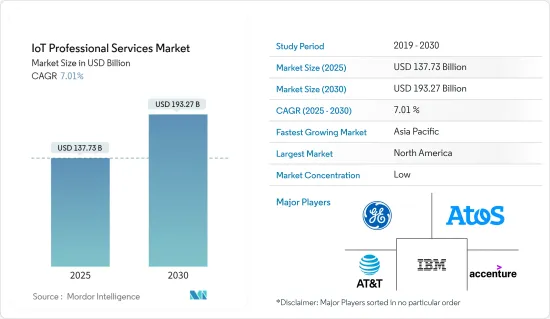

物聯網專業服務市場規模預計在 2025 年達到 1,377.3 億美元,預計到 2030 年將達到 1,932.7 億美元,預測期內(2025-2030 年)的複合年成長率為 7.01%。

預計智慧城市計畫將在未來幾年帶動物聯網的發展。物聯網設備和系統預計將日益成為交通運輸、公共工程和基礎設施的一部分。預計政府措施將推動物連網設備的採用率,更多組織將轉向專業服務進行部署和進一步管理。

關鍵亮點

- 新的用例、經營模式和設備成本的下降正在幫助推動物聯網的採用,從而導致全球連網設備和端點的數量增加。大型物聯網技術NB-IoT和Cat-M1持續在全球部署。大規模物聯網技術預計將超越寬頻物聯網蜂窩連接,佔所有蜂巢式物聯網連接的 51%。

- 物聯網專業服務包括顧客需求分析、框架建構、高階設計、成果檢驗、轉型準備、方案規劃、適配準備、開發實施、業務績效評審、價值實現等幾個階段。

- 雖然此類服務在已開發國家越來越受歡迎,但許多新興國家網路基礎設施不足預計將暫時阻礙全球物聯網專業服務市場的擴張。

- 增加多個設備(例如在物聯網中)會增加網路的表面積,並在此過程中增加潛在的攻擊媒介。即使連接到網路的一個不安全設備也可能成為主動網路攻擊的門戶。因此,資料安全問題已成為企業尋求加強安全產品以贏得客戶信任和防止違規行為的關鍵挑戰。

物聯網專業服務市場趨勢

連網型設備的全球普及推動市場成長

- 連網型設備的激增產生了大量的資料。物聯網專業服務提供者幫助組織管理資料,包括收集、儲存、處理和分析數據。物聯網專業服務提供者可以幫助您制定資料分析策略並實施工具和技術,以從物聯網產生的資料中獲得可行的見解。高階分析使組織能夠做出明智的決策、最佳化流程並推動創新。

- 工業領域連網型設備的日益普及對所研究的市場產生了正面的影響。愛立信預計,大規模物聯網連線數量將增加一倍,達到近2億。據同一消息來源稱,到 2027 年底,40% 的蜂巢式物聯網連接將是寬頻物聯網,其中 4G 將提供大部分連接。然而,隨著 5G 新無線電 (NR) 在新舊頻段的引入,該領域的吞吐資料速率預計將大幅提高。

- 連網型設備的普及並不局限於任何特定產業,而是涉及製造業、醫療保健、運輸、能源和農業等多個領域。每個行業對物聯網都有自己的要求和使用案例。擁有專業行業知識的物聯網專業服務提供者可以提供量身定做的解決方案,以應對每個行業獨特的挑戰和機會。他們了解產業特定物聯網實施的複雜性,並可提供專家指導和支援。

- 此外,在工業領域,應用正在各個產業中蔓延。例如,根據阿魯巴 Networks 的數據,物聯網設備正變得越來越普及,預計 85% 的企業已經部署了該技術。

- 總體而言,連網設備的激增帶來了複雜性、整合挑戰、可擴展性需求、安全問題和資料管理要求,從而推動了對物聯網專業服務的需求。物聯網專業服務提供者在幫助組織解決這些複雜問題並最大化其物聯網投資價值方面發揮關鍵作用。

預計北美將佔據最大的市場佔有率

- 由於 AT&T、IBM 和通用電氣等通訊業主要企業不斷投資建設和改進基礎設施以跟上技術進步,北美預計將佔據主要市場佔有率。預計這將在預測期內推動物聯網專業服務的採用。

- 高速、安全的 5G 連線有望加速物聯網設備的採用,並實現敏捷的營運和靈活的生產。該技術促進了自動化組裝、倉儲、連網物流、包裝、產品處理和自動推車的發展。此外,北美對物聯網和工業數位解決方案的認知度明顯更高。 Mendix 最近的一項調查發現,78% 的美國製造業工人歡迎數位化。此外,十分之八的製造業工人有興趣學習新的數位技能。

- 此外,隨著智慧電網計畫控制該國的整個能源產業,物聯網公共產業預計將在預測期內獲得發展動力。例如,專門從事智慧電錶部署的Landis+Gyr和思科用於物聯網的Catalyst路由器正在協助企業管理電網並收集和管理大量資料。最新的 5G 工業路由器為公共產業公司提供的產品將支援其端點未來 15 至 20 年的使用壽命。

- 物聯網設備的普及,加上稅收優惠和住宅保險折扣,正在鼓勵消費者和公用事業公司提供適合新時代住宅建築商和業主的智慧服務,以在這個不斷發展的市場中保持競爭力。根據電力效率研究所的數據,到 2022 年底,美國將安裝約 1.24 億個智慧電錶,比 2007 年增加 1.17 億個。隨著智慧電錶安裝量的增加,預測期內物聯網服務的採用趨勢可能會大幅增加。

- 根據 CDW 加拿大的一項調查,幾乎所有加拿大組織(96%)都在評估物聯網和新興技術,但超過三分之一(37%)尚未實施這些技術。人工智慧、物聯網和 ServiceNow 等業務流程轉型工具是獲得投資最多的三大新興技術(分別為 60%、59% 和 58%)。隨著商業和工業領域數位化和連網型設備的使用日益增加,該地區的物聯網應用和銷售預計將上升。向數位化和基於物聯網的產品的轉變將導致部署和諮詢等專業服務的增加。

物聯網專業服務概覽

在物聯網專業服務市場,由於各種全球和本地公司的存在,競爭對手之間的競爭仍然很激烈。著名參與企業包括 IBM 公司、通用電氣公司、AT&T 公司和 GE。透過策略夥伴關係、合併和收購,市場參與企業正在積極地獲得更大的影響力。

2023年4月,瑞典通訊設備製造商愛立信將其物聯網加速器(IoT-A)和連網汽車雲端(CVC)業務轉讓給知名物聯網解決方案供應商Aeris。兩家公司相信,他們的綜合能力將使物聯網專案在全球範圍內的部署和管理達到新的規模、可靠性和安全性水準。

2023 年 1 月,總部位於英國曼徹斯特的物聯網軟體工程服務供應商 Mobica 同意被美國著名 IT 服務公司 Cognizant 收購。 Mobica 的服務涵蓋整個軟體開發生命週期,專注於客戶的策略內部研發舉措以及內建軟體開發、實施、測試和部署方面的核心專業知識。此次收購極大地擴展了 Cognizant 的物聯網嵌入式軟體工程能力,為客戶提供了更廣泛的端到端支持,以加速他們的數位轉型。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 監管狀況

- 物聯網生態系統(涵蓋物聯網開發服務、物聯網邊緣技術、物聯網雲端後端即服務和物聯網電信堆疊服務供應商的純、雙重和三重播放供應商格局)

- 評估新冠疫情對市場的影響

第5章市場動態

- 市場促進因素

- 全球連網型設備的普及

- 企業對物聯網數位轉型的需求日益成長

- 市場限制

- 資料隱私和安全問題

- 缺乏物聯網採用的標準化通訊協定和框架

- 物聯網專業服務提供(各服務內容的定性資訊、各產業的趨勢以及服務供應商的策略發展)

- 物聯網諮詢

- 部署服務

- 託管服務

- 大型和小型公司在物聯網諮詢和實施方面的趨勢

第6章市場區隔

- 按服務類型

- 物聯網諮詢

- 物聯網基礎設施

- 系統設計整合

- 支援和維護

- 教育和培訓

- 按組織規模

- 中小企業

- 大型企業

- 依實施類型

- 雲端基礎

- 本地

- 按最終用戶產業

- 製造業

- 零售

- 醫療保健

- 能源公共產業

- 運輸和物流

- 其他

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- IBM Corporation

- General Electric Company

- AT& T Inc.

- Atos SE

- Accenture PLC

- Oracle Corporation

- Cognizant Technology Solutions Corporation

- Capgemini SE

- DXC Technology Company

- Tata Consultancy Services Limited

- Virtusa Corporation

- Wipro Technologies

第8章投資分析

第9章 市場機會與未來趨勢

The IoT Professional Services Market size is estimated at USD 137.73 billion in 2025, and is expected to reach USD 193.27 billion by 2030, at a CAGR of 7.01% during the forecast period (2025-2030).

Smart city initiatives are expected to spearhead IoT growth over the coming years. IoT devices and systems are expected to increase as part of transportation, utilities, and infrastructure. Government initiatives are expected to boost the adoption rates of IoT devices, leading to more organizations relying on professional services for deployment and further management.

Key Highlights

- Emerging applications, business models, and falling device costs have been instrumental in driving IoT adoption, consequently increasing the number of connected devices and endpoints globally. The massive IoT technologies NB-IoT and Cat-M1 continue to be rolled out globally. The massive IoT technologies are anticipated to comprise 51% of all cellular IoT connections overtaking broadband IoT cellular connections.

- The IoT professional services involve several stages including customer needs analysis, creating a framework, designing at a high level, validating outcomes, preparing for transformation, developing a program plan, preparing for adaptation, carrying out deployment, reviewing business performance, and achieving value.

- Despite the increasing popularity of these services in developed nations, the inadequate network infrastructure in many developing countries is expected to impede the expansion of the worldwide IoT professional services market in the foreseeable future.

- Adding several devices, like IoT, increases the surface area of a network, thereby creating more potential attack vectors in the process. Even a single unsecured device connected to a network may serve as a point of entry for an active attack on the web. Data security concern has, thus, presented themselves as a significant challenge as players navigate to strengthen their security offering to gain customer confidence and prevent breaches.

IoT Professional Services Market Trends

The Proliferation of Connected Devices across the World to Drive the Market Growth

- The proliferation of connected devices generates massive amounts of data. IoT professional services providers help organizations manage data, including data collection, storage, processing, and analysis. They assist in developing data analytics strategies and implementing tools and technologies to derive actionable insights from IoT-generated data. Organizations can make informed decisions, optimize processes, and drive innovation by leveraging advanced analytics.

- The growing trend of adopting connected devices in the industrial sectors positively influences the market studied. According to Ericsson, the number of massive IoT connections is expected to have doubled, reaching nearly 200 million contacts. According to the same source, by the end of 2027, 40% of cellular IoT connections will be broadband IoT, with 4G connecting the majority. However, with the introduction of 5G New Radio (NR) in the old and new spectrum, this segment's throughput data rates are expected to increase substantially.

- The proliferation of connected devices is not limited to a specific industry but spans various sectors, including manufacturing, healthcare, transportation, energy, and agriculture. Each industry has unique requirements and uses cases for IoT. IoT professional services providers with industry-specific expertise can offer tailored solutions to address each sector's specific challenges and opportunities. They understand the intricacies of industry-specific IoT implementations and can provide specialized guidance and support.

- Moreover, in the industrial sector, the adoption has penetrated across industries. For instance, according to Aruba Networks, IoT devices have become increasingly pervasive, with 85% of businesses expected to have implemented the technology.

- Overall, the proliferation of connected devices fuels the demand for IoT professional services by introducing complexity, integration challenges, scalability needs, security concerns, and data management requirements. IoT professional services providers play a critical role in helping organizations navigate these complexities and maximize the value of their IoT investments.

North America is Expected to Hold the Largest Market Share

- The North America region is expected to hold significant market shares owing to the presence of prominent players in the telecom industry, such as AT&T, IBM, and General Electric, which continuously invest in building up and advancing their infrastructure to keep pace with technological advancements. This is expected to boost the adoption of IoT professional services over the forecast period.

- Fast and secure 5G connectivity is expected to accelerate the adoption of IoT devices, allowing agile operations and flexible production. This technology will facilitate automated assembly, warehouses, connected logistics, packing, product handling, and autonomous carts. Moreover, North America's awareness of IoT and digital solutions in industries is significantly higher. According to a recent study by Mendix, 78% of US manufacturing workers welcome digitalization. In addition, eight in 10 manufacturing workers are interested in learning new digital skills.

- Additionally, with smart grids planning to take over the entire energy industry in the country, IoT utilities are expected to gain traction over the forecast period. For instance, Landis+Gyr, which specializes in smart meter deployments, and Cisco's Catalyst routers for IoT are helping companies manage their grids and collect and make sense of large volumes of data. The latest 5G industrial routers will give utilities an offering to support the next 15-20 years of an endpoint's life.

- The popularity of IoT devices, combined with tax incentives and home insurance discounts, has encouraged consumers and utility companies to make their services intelligent and suitable for the new age of home builders and owners and remain competitive in such an evolving market. According to the Institute for Electric Efficiency, by the end of 2022, around 124 million smart meters were recorded to be installed in the United States, an increase of 117 million units compared to 2007. With the increasing installation of smart meters, the tendency for IoT services adoption might increase significantly during the forecast period.

- Nearly all (96%) Canadian organizations value IoT and new technologies, according to a CDW Canada survey, yet more than one-third (37%) are not implementing them. Artificial intelligence, the Internet of Things, and business process transformation tools like ServiceNow were the top three most heavily invested new technologies (60 percent, 59 percent, and 58 percent, respectively). With the growing digitalization and usage of connected devices in business and industry, IoT applications and sales are anticipated to increase in the region. As the company moves toward digitalization and IoT-based products, professional services such as deployment and consulting will increase.

IoT Professional Services Industry Overview

The competitive rivalry in the IoT professional services market remains high due to the presence of various global and local players. A few of the prominent players include IBM Corporation, General Electric Company, AT&T Inc., and GE. Through strategic partnerships, mergers, and acquisitions, the players in the market are actively gaining a more substantial footprint.

In April 2023, Ericsson, a Swedish telecom equipment manufacturer, finished transferring its IoT Accelerator (IoT-A) and Connected Vehicle Cloud (CVC) operations to Aeris, a prominent IoT solution provider. The firms believe that the combined capabilities allow for the global deployment and management of IoT programs at a new level of scale, reliability, and security.

In January 2023, Mobica, a provider of IoT software engineering services with its headquarters in Manchester, United Kingdom, agreed to be acquired by Cognizant, a prominent American IT services firm. Mobica's services include the whole software development life cycle, focusing on clients' strategic internal research and development initiatives and core expertise in embedded software development, implementation, testing, and deployment. This acquisition considerably broadens Cognizant's IoT-embedded software engineering capabilities and offers clients a broader range of end-to-end support to facilitate digital transformation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Regulatory Landscape

- 4.4 IoT Ecosystem (Coverage on Pure, Dual, and Triple Play Vendor Landscape across Service Providers for IoT Development Services, IoT Edge Technologies, IoT Cloud Backend-as-a-service, and IoT Telco Stacks)

- 4.5 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Proliferation of Connected Devices Across the Globe

- 5.1.2 Increasing Demand for IoT-enabled Digital Transformation of Enterprises

- 5.2 Market Restraints

- 5.2.1 Concerns Associated With Data Privacy And Security

- 5.2.2 Lack of Standardized Protocols and Frameworks for IoT Deployments

- 5.3 IoT Professional Service Offerings (Qualitative Information Covering What Each Service Entails, Trends Across Industries, and Strategic Developments by Service Providers)

- 5.3.1 IoT Consulting

- 5.3.2 Deployment Services

- 5.3.3 Managed Services

- 5.4 Trend across Large Enterprise and SMEs vis-a-vis IoT Consulting and Implementation

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 IoT Consulting

- 6.1.2 IoT Infrastructure

- 6.1.3 System Designing and Integration

- 6.1.4 Support and Maintenance

- 6.1.5 Education and Training

- 6.2 By Organization Size

- 6.2.1 Small and Medium Enterprises (SMEs)

- 6.2.2 Large Enterprises

- 6.3 By Deployment Type

- 6.3.1 Cloud-based

- 6.3.2 On-premises

- 6.4 By End-user Industry

- 6.4.1 Manufacturing

- 6.4.2 Retail

- 6.4.3 Healthcare

- 6.4.4 Energy and Utilities

- 6.4.5 Transportation and Logistics

- 6.4.6 Other End-user Industries

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia

- 6.5.4 Australia and New Zealand

- 6.5.5 Latin America

- 6.5.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 General Electric Company

- 7.1.3 AT&T Inc.

- 7.1.4 Atos SE

- 7.1.5 Accenture PLC

- 7.1.6 Oracle Corporation

- 7.1.7 Cognizant Technology Solutions Corporation

- 7.1.8 Capgemini SE

- 7.1.9 DXC Technology Company

- 7.1.10 Tata Consultancy Services Limited

- 7.1.11 Virtusa Corporation

- 7.1.12 Wipro Technologies

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年全球物聯網通訊服務市場報告

2025年全球物聯網通訊服務市場報告 全球物聯網專業服務市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測

全球物聯網專業服務市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測 物聯網 (IoT)專業服務市場規模、佔有率及成長分析(按服務類型、組織規模、部署類型、應用和地區)-2025 年至 2032 年產業預測2025年全球物聯網專業服務市場報告

物聯網 (IoT)專業服務市場規模、佔有率及成長分析(按服務類型、組織規模、部署類型、應用和地區)-2025 年至 2032 年產業預測2025年全球物聯網專業服務市場報告 物聯網通訊服務市場規模、佔有率、成長分析,按組件、連接性、應用程式、最終用戶、地區 - 產業預測,2025-2032 年

物聯網通訊服務市場規模、佔有率、成長分析,按組件、連接性、應用程式、最終用戶、地區 - 產業預測,2025-2032 年 物聯網系統整合與專業服務 2024-2030

物聯網系統整合與專業服務 2024-2030 物聯網電信服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、按服務類型、按應用、按地區、按競爭細分,2019-2029F

物聯網電信服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、按服務類型、按應用、按地區、按競爭細分,2019-2029F 物聯網專業服務市場:按服務類型、組織規模、部署、應用 - 2025-2030 年全球預測物聯網專業服務市場:按服務類型、部署類型、組織規模和應用程式分類 - 2025-2030 年全球預測物聯網通訊服務市場:按提供的服務、連接性和應用分類 - 2025-2030 年全球預測

物聯網專業服務市場:按服務類型、組織規模、部署、應用 - 2025-2030 年全球預測物聯網專業服務市場:按服務類型、部署類型、組織規模和應用程式分類 - 2025-2030 年全球預測物聯網通訊服務市場:按提供的服務、連接性和應用分類 - 2025-2030 年全球預測