|

市場調查報告書

商品編碼

1687912

藥用玻璃包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030年)Pharmaceutical Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

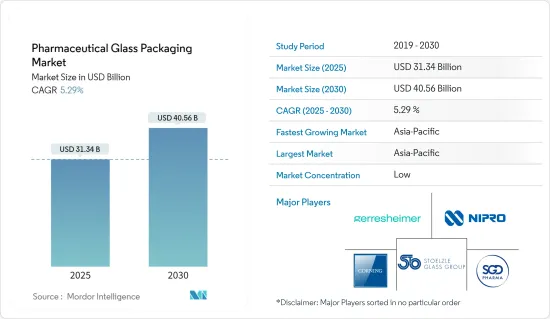

預計 2025 年藥用玻璃包裝市場規模為 313.4 億美元,到 2030 年將達到 405.6 億美元,預測期內(2025-2030 年)的複合年成長率為 5.29%。

關鍵亮點

- 玻璃包裝解決方案主要作為藥品的初級包裝,是製藥業的關鍵包裝材料之一。這主要是因為它永續、惰性、不滲透、可回收且品質不損失、可重複使用等優點。玻璃容器是製藥業中具有重要應用的主要包裝材料之一。

- 全球製藥業正在經歷顯著成長,對感染疾病和非感染疾病的治療包裝產生了需求。因此,藥品生產對玻璃包裝的需求日益增加,以保護藥品免受損壞、生物污染和外界影響。

- 此外,注射藥物需求的不斷成長也推動了製藥業玻璃瓶的成長。預計癌症治療和其他強效藥物(如抗體結合物和速效類固醇)的強勁需求以及人均藥品支出的增加將成為主要的成長動力。

- 然而,玻璃包裝面臨挑戰,因為原料價格和其他因素導致其昂貴,無法為大量消費的包裝產品提供經濟可行的解決方案。因此塑膠成為一種選擇。

- 新冠疫情導致藥品需求維持穩定成長。疫情期間藥品需求的激增對市場成長產生了正面影響。隨著不同國家的製藥商核准和逐步淘汰新藥和疫苗,玻璃包裝的應用範圍不斷擴大,預計玻璃包裝將進一步成長。

藥用玻璃包裝市場趨勢

新興國家製藥業推動成長

- 新興國家被描述為不斷發展、繁榮的國家,儘管存在巨大風險,但有望提高投資回報率。儘管許多已開發國家的藥品銷售成長緩慢,但新興市場的銷售模式顯示藥品銷售將持續擴張。多種經濟和人口變數影響著新興市場的趨勢。例如,現有市場繼續面臨嚴峻形勢,包括因專利到期導致的成長放緩、鼓勵學名藥替代的成本削減措施以及更嚴格的監管。

- 藥用玻璃包裝產業在中國等國家已具有顯著的滲透力。玻璃藥品包裝在已開發國家的應用越來越廣泛。自從新冠疫情爆發以來,新興國家的醫療保健和製藥業一直在成長,為藥用玻璃包裝市場創造了機會。

- 例如,2022年9月,肖特製藥擴大了在中國的墨盒生產。中國和匈牙利正在投資數百萬美元,以大幅提高藥用墨盒的生產能力。

- 此外,印度製藥業高度重視研發。印度預計在 2022 年成為全球醫療保健強國,其研發生態系統不斷擴大,藥品出口不斷增加,為國內各玻璃包裝供應商創造機會。

- 此外,東南亞和東亞的醫藥銷售額預計將達到 2,630 億美元,成為繼北美和歐洲之後的第三大地區。這些成長要素,加上現有公司因行業成長而進行的投資,預計將推動市場成長。

亞太地區成長強勁

- 中國多年來已建立了醫藥行業的標準體系,因此中國藥用玻璃包裝市場預計將快速成長。在國內,藥品包裝材料在保存期限內的穩定性以及使用過程中的安全性越來越受到重視。在此背景下,綠色、可分解、易使用的新型醫藥包裝材料和容器蓬勃發展。

- 由於大型跨國製藥公司的存在,中國醫療保健市場規模龐大且成長迅速,這為玻璃包裝市場帶來了明顯的機會。這些公司是中國醫藥市場最大的收益來源之一。

- 在印度,由於醫療保健產業對非專利注射藥物的使用日益增多,藥用玻璃包裝的需求也在增加。藥用玻璃包裝可容納多種藥物類型,包括注射劑和非注射劑。藥用玻璃包裝的關鍵屬性是高化學耐久性,以最大限度地提高產品可靠性。

- 印度在全球醫藥市場佔有重要地位,隨著市場規模的擴大,印度對玻璃包裝的需求預計將會成長。根據印度品牌資產基金會網站發佈的資料,印度是全球最大的學名藥供應國,佔全球供應量的20%,並滿足全球60%以上的疫苗需求。據印度評級與研究公司稱,預計2022年印度醫藥市場的收益將增加12%以上。

- 此外,日本是繼美國之後製藥業發展最快的國家之一,並始終注重持續創新和專利藥品。日本政府也透過放鬆對國際投資的管制促進了這一成長,從而推動了日本醫藥市場的發展。

- 亞太其他地區包括印尼、澳洲、新加坡、泰國、韓國和馬來西亞。推動市場發展的因素包括不斷擴大的國際夥伴關係、生物相似藥、不斷成長的成品藥出口以及強勁的學名藥市場。

藥用玻璃包裝產業概況

藥用玻璃包裝市場較為分散。政府措施的不斷增加以及對注射劑和其他藥品的需求不斷成長,為藥用玻璃包裝解決方案提供了豐厚的機會。整體來看,現有競爭對手之間的競爭十分激烈。大型公司正在各個醫藥產業積極擴張合併,推動市場需求。主要參與企業包括 Gerresheimer Glass Inc.、Corning Incorporated、Nipro Corporation、SGD SA 和 Stolzle-Oberglass GmbH。

- 2022 年 9 月:Gerresheimer AG 和 StevanatoGroup SpA 基於 Stevanato Group 市場領先的 EZ-fill 技術開發了高階即用型 (RTU) 解決方案平台,最初專注於管瓶。預計客戶將從此次夥伴關係中受益,包括提高生產力、提高品質標準、加快產品上市時間、降低整體擁有成本 (TCO) 和減少供應鏈風險。

- 2022 年 7 月:醫療設備製造商 Nipro Corporation Japan 已投資 1 億克羅埃西亞庫納(1,360 萬美元/1,330 萬歐元)在克羅埃西亞為製藥業建造新的玻璃包裝廠。 Nipro 的 Nipro PharmaPackaging 部門在薩格勒布郊外的運作開設了一家新工廠,生產用於包裝救命藥物的玻璃安瓿瓶和管瓶。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業價值鏈分析

- 產業吸引力-波特五力模型

- 供應商的議價能力

- 購買者和消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 工業影響評估

第5章市場動態

- 市場促進因素

- 新興國家製藥業的成長

- 提高可回收玻璃的商業價值

- 市場限制

- 替代材料的重要性日益增加

第6章市場區隔

- 按產品

- 瓶子

- 管瓶

- 安瓿

- 藥筒和注射器

- 更多產品

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 其他亞太地區

- 拉丁美洲

- 巴西

- 阿根廷

- 其他拉丁美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第7章競爭格局

- 公司簡介

- Gerresheimer AG

- Corning Incorporated

- Nipro Corporation

- SGD SA(SGD PHARMA)

- Stlzle-Oberglas GmBH(CAG Holding GmbH)

- Bormioli Pharma SpA

- West Pharmaceutical Services Inc.

- Schott AG

- Shandong Medicinal Glass Co. Ltd

- Beatson Clark

- Arab Pharmaceutical Glass Co.

- Piramal Glass Private Limited(Piramal Group)

- Sisecam Group

第8章投資分析

第9章 市場機會與未來趨勢

The Pharmaceutical Glass Packaging Market size is estimated at USD 31.34 billion in 2025, and is expected to reach USD 40.56 billion by 2030, at a CAGR of 5.29% during the forecast period (2025-2030).

Key Highlights

- Glass packaging solutions are offered mainly as the primary packaging for pharmaceutical products and are among the leading packaging materials for the pharmaceutical industry. This is primarily due to advantages such as being sustainable, inert, impermeable, recyclable with no loss in quality, and reusable. Glass containers are among the primary packaging materials that have found significant use in the pharmaceutical industries.

- The pharmaceutical industry is growing significantly worldwide, creating the need for packaging for communicable and non-communicable disease treatments. Thus, the demand for glass packaging in pharmaceutical manufacturing is increasing as it protects medicines from damage, biological contamination, and external influences.

- Furthermore, the growing demand for injectable pharmaceuticals is propelling the growth of glass bottles in the pharmaceutical industry. The strong demand for oncology and other high-potency drugs (such as antibody conjugates and steroids with a fast onset of action) and growth in the per capita pharmaceutical spending are expected to be the primary growth drivers.

- Over time, the market also faced challenges that included glass packaging getting expensive due to raw material prices and other factors, and it could not provide economically viable solutions for packaging products across mass consumption. That marked the advent of plastics as an option.

- The COVID-19 pandemic has left a steady growth rate with increased demand for medicines. The surge in the need for pharmaceutical drugs during the pandemic has positively impacted the market's growth. It is further expected to grow as new drugs and vaccines are being approved and phased out in different countries by pharmaceutical manufacturers, expanding the scope of glass packaging.

Pharmaceutical Glass Packaging Market Trends

Pharmaceutical Industry in Emerging Economies to Drive Growth

- Emerging markets are described as growing prosperous nations where investment is anticipated to increase profits despite significant risks. While pharmaceutical sales grow slowly in many developed nations, emerging market sales patterns indicate ongoing expansion. Several economic and demographic variables influence the trend in these markets, such as challenging conditions in established markets, with growth that has been flattened due to patent expiration, cost-cutting measures that encourage generic replacement, and strict enforcement of restrictions.

- The pharmaceutical glass packaging industry has seen significant penetration in nations like China. Glass pharmaceutical packaging is becoming more widely used in developed countries. After COVID-19, the healthcare and pharmaceutical sectors are growing in emerging nations, presenting opportunities for the pharmaceutical glass packaging market.

- For instance, in September 2022, SCHOTT Pharma expanded cartridge output in China. Several million investments are intended to significantly improve the manufacturing capabilities for pharmaceutical cartridges in China and Hungary.

- Moreover, R&D is highly valued in India's pharmaceutical sector. India became a worldwide medical giant in 2022 by enlarging its R&D ecosystem and raising pharmaceutical exports, creating opportunities for various domestic glass packaging vendors.

- Furthermore, Southeast & East Asia is expected to generate USD 263 billion in pharmaceutical sales and take the third position after North America and Europe. All the growth factors and investments by significant market incumbents due to the industry's growth are anticipated to drive the market's growth.

Asia-Pacific to Witness Significant Growth

- The Chinese pharmaceutical glass packaging market is expected to grow rapidly as China has built a standard system for the pharmaceutical industry over the years. The country pays more and more attention to the stability of pharmaceutical packaging materials during the drug storage period and safety when used. Against this background, new green, degradable, and easy-to-use pharmaceutical packaging materials and vessels are booming.

- China's large and rapidly growing healthcare market has been an obvious target of opportunity for the glass packaging market due to the presence of major multinational pharmaceutical companies. These companies are among the most significant revenue earners in the Chinese pharmaceutical market.

- In India, pharmaceutical glass packaging has been growing due to the increasing usage of generic injectable drugs in the healthcare industry. Pharmaceutical glass packaging is available in various drug types, such as injectable and non-injectable. The significant properties of pharmaceutical glass packaging include its high chemical durability, which maximizes the reliability of the products.

- The demand for glass packaging in India is expected to proliferate as India is a prominent and expanding player in the global medicines market. According to data published on the India Brand Equity Foundation website, India is the world's largest provider of generic pharmaceuticals, accounting for 20% of the worldwide supply and meeting over 60% of global vaccine demand. According to India Ratings & Research, the Indian pharmaceutical market revenue was predicted to increase by more than 12% in 2022.

- Furthermore, Japan has one of the fastest-growing pharmaceutical industries after the United States and constantly focuses on steady innovation and patented drugs. The Government of Japan also contributes to this growth through deregulations for international companies to invest, thereby driving the country's pharmaceutical market.

- The scope of the Rest of the Asia-Pacific region covers Indonesia, Australia, Singapore, Thailand, South Korea, and Malaysia. The market is driven by the growth in international partnerships, biosimilars, the expansion in the export of finished formulations, and a robust generics market.

Pharmaceutical Glass Packaging Industry Overview

The pharmaceutical glass packaging market is fragmented. The surge in government initiatives and increasing demand for injectables and other medicines provide lucrative pharmaceutical glass packaging solutions opportunities. Overall, the competitive rivalry among existing competitors is high. Large companies are actively involved in expansion and mergers in different pharmaceutical industries, driving the demand in the market. Key players include Gerresheimer Glass Inc., Corning Incorporated, Nipro Corporation, SGD SA, and Stolzle-Oberglass GmbH.

- September 2022: Gerresheimer AG and StevanatoGroup SpA developed a high-end ready-to-use (RTU) solution platform with an initial focus on vials built on Stevanato Group's market-leading EZ-fill technology. The customers are expected to benefit from the partnership in terms of increased productivity, higher quality standards, quicker time to market, lower total cost of ownership (TCO), and reduced supply chain risk.

- July 2022: Nipro Corporation Japan, a medical equipment manufacturing company, invested HRK 100 million (USD 13.6 million/EUR 13.3 million) in a new glass packaging plant for the pharmaceutical industry in Croatia. The new factory that produces glass ampoules and vials to package life-saving drugs was inaugurated in Zagreb's suburb Sesvete, Nipro's division, Nipro PharmaPackaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter Five Forces

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth of Pharmaceutical Industry in Emerging Economies

- 5.1.2 Commodity Value of Glass Increased with Recyclability

- 5.2 Market Restraints

- 5.2.1 Increased Relevance of Alternate Material

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Bottles

- 6.1.2 Vials

- 6.1.3 Ampoules

- 6.1.4 Cartridges and Syringes

- 6.1.5 Others Products

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.2.5 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 Rest of Asia-Pacific

- 6.2.4 Latin America

- 6.2.4.1 Brazil

- 6.2.4.2 Argentina

- 6.2.4.3 Rest of Latin America

- 6.2.5 Middle East and Africa

- 6.2.5.1 Saudi Arabia

- 6.2.5.2 South Africa

- 6.2.5.3 Rest of Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Gerresheimer AG

- 7.1.2 Corning Incorporated

- 7.1.3 Nipro Corporation

- 7.1.4 SGD SA (SGD PHARMA)

- 7.1.5 Stlzle-Oberglas GmBH (CAG Holding GmbH)

- 7.1.6 Bormioli Pharma SpA

- 7.1.7 West Pharmaceutical Services Inc.

- 7.1.8 Schott AG

- 7.1.9 Shandong Medicinal Glass Co. Ltd

- 7.1.10 Beatson Clark

- 7.1.11 Arab Pharmaceutical Glass Co.

- 7.1.12 Piramal Glass Private Limited (Piramal Group)

- 7.1.13 Sisecam Group

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年全球藥用玻璃包裝市場報告2025年全球低硼矽酸玻璃瓶市場報告2025年全球醫用玻璃疫苗瓶市場報告

2025年全球藥用玻璃包裝市場報告2025年全球低硼矽酸玻璃瓶市場報告2025年全球醫用玻璃疫苗瓶市場報告 全球藥用管瓶市場:市場規模(按數量、分銷類型、瓶蓋尺寸和地區分類)、未來預測

全球藥用管瓶市場:市場規模(按數量、分銷類型、瓶蓋尺寸和地區分類)、未來預測 2032 年藥用管瓶和安瓿瓶市場預測:按產品、材料、產能、應用、最終用戶和地區進行的全球分析

2032 年藥用管瓶和安瓿瓶市場預測:按產品、材料、產能、應用、最終用戶和地區進行的全球分析 藥用玻璃包裝市場報告(依產品(藥瓶、藥水瓶、安瓿瓶、藥筒、注射器等)、藥品類型(學名藥、品牌藥、生物製劑)、應用(口服、注射、鼻腔等)及地區分類)2025-2033

藥用玻璃包裝市場報告(依產品(藥瓶、藥水瓶、安瓿瓶、藥筒、注射器等)、藥品類型(學名藥、品牌藥、生物製劑)、應用(口服、注射、鼻腔等)及地區分類)2025-2033 硼矽酸管瓶市場報告:2031 年趨勢、預測與競爭分析

硼矽酸管瓶市場報告:2031 年趨勢、預測與競爭分析 藥用管瓶和安瓿瓶:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)

藥用管瓶和安瓿瓶:市場佔有率分析、產業趨勢和成長預測(2025-2030 年) 藥用玻璃包裝市場機會、成長動力、產業趨勢分析及2025-2034年預測

藥用玻璃包裝市場機會、成長動力、產業趨勢分析及2025-2034年預測 醫藥玻璃包裝世界:依產品類型、材料類型、應用和地區預測至2032年

醫藥玻璃包裝世界:依產品類型、材料類型、應用和地區預測至2032年