|

市場調查報告書

商品編碼

1687774

石墨電極:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Graphite Electrode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

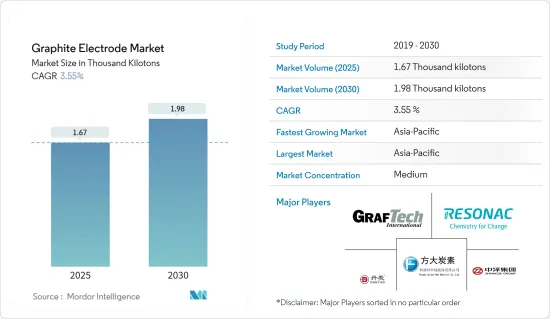

石墨電極市場規模預計在 2025 年為 1,670 千噸,預計在 2030 年達到 1,980 千噸,預測期內(2025-2030 年)的複合年成長率為 3.55%。

新冠疫情阻礙了石墨電極市場的發展,多個國家實施全國停工和嚴格的社交距離措施,影響了粗鋼和粗鋁的生產。然而,由於粗鋼和粗鋁製造業的需求增加,市場在放鬆管制後實現了顯著的成長率。

主要亮點

- 短期內,預計中國對電弧爐煉鋼技術的強勁需求和廢鋼供應量的增加將推動市場需求。

- 另一方面,對鋼鐵業的高度依賴預計將阻礙市場成長。

- 石墨電極在鋼鐵以外應用領域的使用日益增多,可能為所研究市場的成長提供各種機會。

- 預計亞太地區將主導市場並在預測期內呈現最高的複合年成長率。

石墨電極市場趨勢

電弧爐領域佔市場主導地位

- 石墨電極主要應用於電弧爐(EAF)煉鋼,約佔總消費量的70-80%。

- 在電弧爐內,石墨電極可作為電能的導管。石墨電極在廢鐵的熔化和提煉中起著至關重要的作用,最終生產出高品質的鋼。這些電極由特殊等級的針狀焦和其他原料製成,具有優異的導熱性和導電性。這使得它能夠承受煉鋼過程中所遇到的極端溫度和惡劣條件。

- 石墨電極有利於電弧爐高效、環保地煉鋼,在現代鋼鐵工業中發揮至關重要的作用。隨著鋼鐵製造商越來越接受技術進步並優先考慮永續性,對高品質石墨電極的需求可能會保持強勁。預計這將推動未來幾年電爐煉鋼的創新和進步。

- 塔塔鋼鐵英國公司於 2024 年 1 月宣布將關閉兩座高排放氣體高爐,標誌著公司向更環保的煉鋼方向轉變。該公司計劃於 2027 年在塔爾伯特港投入使用電弧爐,這是 12.5 億英鎊(15.9 億美元)重大投資的一部分。

- 日本第二大鋼鐵製造商 JFE 鋼鐵公司在其位於日本西部的倉敷廠破土動工,建造一座大型電弧爐(EAF),預計於 2027 年左右完工。此舉旨在減少碳排放並應對氣候變遷問題。 2023 年 6 月,安賽樂米塔爾盧森堡公司宣佈在其貝爾瓦爾工廠投資一座新的電弧爐 (EAF),作為其脫碳努力的一部分。

- 中國是世界鋼鐵大國,佔全球鋼鐵產量的55%。世界鋼鐵協會強調,中國的鋼鐵產量穩定,2023 年產量將達到 10.191 億噸,與 2022 年的數字一致。其中,2023年1-10月產量達8.747億噸,比2022年同期成長1.4%。由於中國鋼鐵企業計畫透過產能置換機制每年新增產能高達1.18億噸,預計2023年中國粗鋼產能將緩慢成長。

- 因此,由於上述因素,預計預測期內電弧爐應用領域將主導石墨電極市場。

亞太地區佔市場主導地位

- 預計預測期內亞太地區將主導石墨電極市場。中國和印度等國家的鹼性氧氣轉爐和電弧爐對石墨電極的需求正在增加。

- 在中國,鋼鐵生產中電弧爐(EAF)的採用率不斷提高,推動了對石墨電極的需求。中國製造商認知到國家致力於透過電弧爐技術提高鋼鐵生產率。這種轉變主要是受環境問題和對更永續的煉鋼方法的追求所推動。

- 石墨電極不僅用於煉鋼,還用於加工鋁和矽。中國是全球最大的鋁和矽生產國,2023年中國鋁年產量將大幅成長。根據中國國家統計局的報告,產量與前一年同期比較增3.43%,達到4159萬噸,創歷史新高。這一成長是由新生產能力的增加和電力供應限制的放寬所推動的。根據美國地質調查局預測,2023年中國矽產量將達660萬噸。

- 印度對石墨電極的需求正在快速成長,這主要歸因於近年來鋼鐵產量的穩定成長。這些電極在鋼鐵和非鐵金屬生產中發揮著至關重要的作用,並用於電弧爐和鋼包爐製程。

- 印度是世界第二大鋼鐵生產國,年鋼鐵產能超過1.61億噸,超過中國。其中,高爐-鹼性氧氣轉爐(BF-BoF)路線產能為6,700萬噸,電弧爐(EAF)路線產能3,600萬噸,感應爐(IF)路線產能5,800萬噸。

- 韓國鋼鐵業滿足汽車、建築和造船等行業的需求,在推動國家經濟成長方面發揮關鍵作用。根據韓國鋼鐵協會報告,鋼鐵業佔韓國GDP的1.5%,佔製造業的4.9%。其中,韓國是世界第六大鋼鐵生產國。

- 由於上述因素,預計亞太地區石墨電極市場在預測期內將大幅成長。

石墨電極產業概況

石墨電極市場部分整合。市場的主要企業(不分先後順序)包括 Resonac Holdings Corporation、GrafTech International、方大炭素新材料、中澤集團和遼寧丹炭科技集團(丹炭)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 電弧爐煉鋼技術需求強勁

- 中國廢鋼供應量不斷增加

- 限制因素

- 對鋼鐵業的依賴程度較高

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 電極級

- 高功率(UHP)

- 高功率(SHP)

- 正常輸出(RP)

- 按應用

- 電弧爐

- 轉爐

- 有色金屬應用

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 阿拉伯聯合大公國

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 合併、收購、合資、合作和協議

- 市場佔有率(%)分析

- 主要企業策略

- 公司簡介

- EL 6 LLC

- Fangda Carbon New Material Technology Co. Ltd

- GrafTech International

- Graphite India Limited

- HEG Limited

- Kaifeng Pingmei New Carbon Materials Technology Co. Ltd

- Liaoning Dantan Technology Group Co. Ltd(Dan Carbon)

- Nantong Yangzi Carbon Co. Ltd

- Nippon Carbon Co. Ltd

- Sangraf International Inc.

- SEC Carbon Limited

- Resonac Holdings Corporation

- Tokai Carbon Co. Ltd

- Zhongze Group

第7章 市場機會與未來趨勢

- 石墨電極在有色金屬應用中的使用日益增多

The Graphite Electrode Market size is estimated at 1.67 thousand kilotons in 2025, and is expected to reach 1.98 thousand kilotons by 2030, at a CAGR of 3.55% during the forecast period (2025-2030).

The COVID-19 pandemic hampered the graphite electrodes market, as nationwide lockdowns in several countries and strict social distancing measures affected the production of crude steel and crude aluminum. However, the market registered a significant growth rate after the restrictions were lifted due to the increasing demand from crude steel and aluminum manufacturing industries.

Key Highlights

- In the short term, the strong demand for EAF technology for steelmaking and the rising availability of steel scrap in China is expected to drive the market demand.

- On the other hand, high dependency on the steel industry is expected to hinder the market's growth.

- The rising usage of graphite electrodes in non-steel applications may offer various opportunities for the growth of the market studied.

- Asia-Pacific is expected to dominate the market and is anticipated to witness the highest CAGR during the forecast period.

Graphite Electrode Market Trends

The Electric Arc Furnace Segment to Dominate the Market

- Graphite electrodes find their primary application in electric arc furnace (EAF) steelmaking, accounting for around 70% to 80% of their total consumption.

- Within the EAF, graphite electrodes serve as conduits for electrical energy. They play a crucial role in the melting and refining scrap steel, ultimately yielding high-quality steel. These electrodes, crafted from specialized grades of needle coke and other raw materials, boast exceptional thermal and electrical conductivity. This enables them to withstand the extreme temperatures and demanding conditions encountered during steelmaking.

- Graphite electrodes play a pivotal role in the contemporary steel industry, facilitating efficient and eco-conscious steelmaking in electric arc furnaces. As steel producers increasingly embrace technological advancements and prioritize sustainability, the demand for high-quality graphite electrodes is poised to remain robust. This, in turn, is expected to drive innovation and progress in EAF steelmaking in the years ahead.

- Tata Steel UK, in January 2024, announced the closure of two high-emission blast furnaces, signaling a shift toward greener steelmaking. The company plans to commence operations at its proposed electric arc furnace in Port Talbot by 2027, with a substantial investment of GBP 1.25 billion (~USD 1.59 billion).

- Japan's second-largest steelmaker, JFE Steel, broke ground on a large-scale electric arc furnace (EAF) at its Kurashiki plant in western Japan, slated for completion around 2027. This move is aimed at curbing carbon dioxide emissions and addressing climate change concerns. In June 2023, ArcelorMittal Luxembourg, as part of its decarbonization efforts, announced an investment in a new electric arc furnace (EAF) at its Belval site.

- China, the global steel giant, accounts for 55% of the world's steel production. The World Steel Association highlights China's consistent output, with 1,019.1 million tons in 2023, matching the 2022 figure. Notably, the country's production in the first 10 months of 2023 reached 874.7 million metric tons, marking a 1.4% uptick from the same period in 2022. China's crude steel capacity witnessed modest growth in 2023, driven by plans from Chinese steelmakers to introduce up to 118 million MT/year of new capacity through a capacity swap mechanism.

- Hence, owing to the above-mentioned factors, the electric arc furnace application segment is expected to dominate the graphite electrode market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominate the graphite electrode market during the forecast period. The demand for graphite electrodes is increasing from basic oxygen furnaces and electric arc furnaces in countries like China and India.

- The demand for graphite electrodes is increasing in China due to the rising adoption of electric arc furnaces (EAFs) in steel production. Chinese manufacturers recognize the country's commitment to higher steel production rates via EAF technology. This shift was primarily driven by environmental concerns and the push for more sustainable steelmaking methods.

- Graphite electrodes find applications not only in steelmaking but also in aluminum and silicon processing. China, being the world's largest producer of both aluminum and silicon, witnessed a significant surge in its annual aluminum output in 2023. The output climbed by 3.43% from the previous year, hitting a record high of 41.59 million tonnes, as reported by the National Bureau of Statistics of China. This growth was fueled by the addition of new capacities and the relaxation of power supply restrictions. According to the US Geological Survey, China's silicon production in 2023 was estimated at 6.6 million metric tons.

- India is witnessing a robust surge in the demand for graphite electrodes, primarily driven by the steady uptick in iron and steel production over recent years. These electrodes play a pivotal role in steel and non-ferrous metal production and are employed in both the electric arc furnace and ladle furnace processes.

- India, the world's second-largest steel producer, has a steel capacity of over 161 million tons annually, trailing only China. This capacity is distributed with 67 million tons via the blast furnace-basic oxygen furnace (BF-BoF) route, 36 million tons via electric arc furnace (EAF), and 58 million tons via the induction furnace (IF) route.

- The steel sector in South Korea holds significance, driving the nation's economic growth by catering to industries like automotive, construction, and shipbuilding. As reported by the Korean Iron & Steel Association, the steel industry accounts for 1.5% of the nation's GDP and 4.9% of its manufacturing sector. Notably, South Korea ranks as the sixth-largest steel producer globally.

- Owing to the factors mentioned above, the market for graphite electrodes in Asia-Pacific is projected to grow significantly during the forecast period.

Graphite Electrode Industry Overview

The graphite electrode market is partially consolidated. Some of the major players (not in any particular order) in the market include Resonac Holdings Corporation, GrafTech International, Fangda Carbon New Material Co. Ltd, Zhongze Group, and Liaoning Dantan Technology Group Co. Ltd (Dan Carbon).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Strong Demand for EAF Technology for Steelmaking

- 4.1.2 Rising Availability of Steel Scrap in China

- 4.2 Restraints

- 4.2.1 High Dependency on the Steel Industry

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Electrode Grade

- 5.1.1 Ultra High Power (UHP)

- 5.1.2 High Power (SHP)

- 5.1.3 Regular Power (RP)

- 5.2 Application

- 5.2.1 Electric Arc Furnace

- 5.2.2 Basic Oxygen Furnace

- 5.2.3 Non-steel Application

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Egypt

- 5.3.5.5 South Africa

- 5.3.5.6 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 EL 6 LLC

- 6.4.2 Fangda Carbon New Material Technology Co. Ltd

- 6.4.3 GrafTech International

- 6.4.4 Graphite India Limited

- 6.4.5 HEG Limited

- 6.4.6 Kaifeng Pingmei New Carbon Materials Technology Co. Ltd

- 6.4.7 Liaoning Dantan Technology Group Co. Ltd (Dan Carbon)

- 6.4.8 Nantong Yangzi Carbon Co. Ltd

- 6.4.9 Nippon Carbon Co. Ltd

- 6.4.10 Sangraf International Inc.

- 6.4.11 SEC Carbon Limited

- 6.4.12 Resonac Holdings Corporation

- 6.4.13 Tokai Carbon Co. Ltd

- 6.4.14 Zhongze Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Usage of Graphite Electrodes in Non-steel Applications

石墨電極市場按產品類型、電極直徑、等級、應用和最終用戶產業分類 - 全球預測 2025-2032

石墨電極市場按產品類型、電極直徑、等級、應用和最終用戶產業分類 - 全球預測 2025-2032 2025年全球石墨電極市場報告

2025年全球石墨電極市場報告 全球石墨電極市場規模(按直徑、電極等級、應用、地區和預測)

全球石墨電極市場規模(按直徑、電極等級、應用、地區和預測) 按產品類型(超高功率 (UHP)、高功率 (HP)、常規功率 (RP))、應用(電弧爐、鋼包爐、非鋼應用)和地區分類的石墨電極市場報告 2025-2033

按產品類型(超高功率 (UHP)、高功率 (HP)、常規功率 (RP))、應用(電弧爐、鋼包爐、非鋼應用)和地區分類的石墨電極市場報告 2025-2033 石墨電極市場規模、佔有率、成長分析、按電極等級、按應用、按地區 - 產業預測,2024-2031

石墨電極市場規模、佔有率、成長分析、按電極等級、按應用、按地區 - 產業預測,2024-2031 2030 年石墨電極市場預測:按電極等級、電極尺寸、金屬類型、應用、最終用戶和地區進行的全球分析石墨電極市場-2024年至2029年預測

2030 年石墨電極市場預測:按電極等級、電極尺寸、金屬類型、應用、最終用戶和地區進行的全球分析石墨電極市場-2024年至2029年預測 2024-2028年石墨電極全球市場

2024-2028年石墨電極全球市場 石墨電極市場 - 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢與預測

石墨電極市場 - 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢與預測