|

市場調查報告書

商品編碼

1687749

隔熱塗層:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Thermal Barrier Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

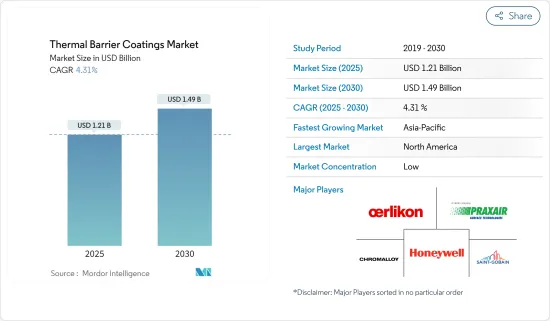

預計 2025 年隔熱障塗層市場規模將達到 12.1 億美元,預計到 2030 年將達到 14.9 億美元,預測期內(2025-2030 年)的複合年成長率為 4.31%。

2020年,由於新冠疫情以及被覆劑主要終端用戶的營運限制,市場受到宏觀經濟狀況的不利影響,導致需求疲軟。不過,目前市場估計已恢復至疫情前的水平,並有望穩定成長。

主要亮點

- 預計從燃煤發電到天然氣發電的轉變以及航太領域需求的不斷成長將推動隔熱塗層市場的需求。

- 另一方面,原物料價格波動預計會抑制市場需求。

- 預計預測期內各個終端用戶市場的技術進步將為市場提供新的成長途徑。

- 北美佔據全球市場主導地位。然而,預計亞太地區將在預測期內見證最高的成長率。

隔熱塗層市場趨勢

航太航太業佔市場主導地位

- 隔熱塗層通常用於保護鎳基高溫合金在航空渦輪機與冷氣流結合時免於熔化和熱循環。

- 隔熱塗層將允許的氣體溫度提高到高溫合金的熔點以上。它降低葉片合金溫度並保護其免受熱氣體引起的氧化和高溫腐蝕,從而提高渦輪機的性能、壽命和效率。

- 不斷成長的飛機持有和不斷增加的國防支出推動著全球飛機產量的增加,對用於保護引擎和渦輪機的 TBC 等塗料的需求巨大。

- 根據航空維修站協會發布的資料,預計未來十年全球飛機機持有將迅速擴大。預計將從 2023 年的 28,000 人成長到 2032 年的 38,100 人。

- 根據波音《2022-2041年商業展望》,全球航太服務業規模預計將達到3.6兆美元以上,其中美國和加拿大佔近30%的市場佔有率。緊隨其後的是歐洲,佔比為 23.5%,這可能會在未來幾年提振市場需求。

- 此外,根據波音公司《2022-2041年商業展望》,到2041年,中國將交付約8,485架新飛機,市場服務價值將達5,450億美元。從而促進市場成長。

- 總體而言,航太工業的隔熱塗層市場預計將逐步復甦,並在整個預測期內實現穩定成長。

北美佔據市場主導地位

- 由於航太、汽車、電力、石油和天然氣等各個終端用戶產業的巨大需求,北美地區在隔熱塗層市場佔據主導地位。

- 此外,美國佔據著最大的市場佔有率。除美國外,加拿大和墨西哥也佔據隔熱障塗層市場的大部分佔有率。

- 航太零件向法國、中國和德國等國的強勁出口,以及美國強勁的消費支出,正在推動航太製造業活動。這可能為市場帶來正面的動力。

- 在北美,根據波音公司《2022-2041年商業展望》,到2041年,新飛機交付總量將達到9,310架,市場服務價值將達到1.45兆美元。

- 根據OICA預測,2022年北美汽車產量將達到17,756,263輛,較2021年的16,190,835輛成長10%。此外,在北美,2022 年美國的產量超過 1,006 萬輛。

- 北美地區的主要國家繼續受到半導體微晶片短缺和進一步供應鏈中斷的影響。例如,根據美國全國汽車經銷商協會 (NADA) 的數據,2022 年年輕型汽車銷量是自 2011 年以來全年最低的。與 2021 年輕型汽車銷量相比,這一數字年減了 8.2%。

- 因此,預計預測期內所有上述因素都將對該地區隔熱塗層市場的需求產生重大影響。

隔熱塗層產業概況

隔熱障塗層市場較為分散。該市場的主要企業(不分先後順序)包括霍尼韋爾國際公司、OC Oerlikon Management AG、Praxair ST Technology, Inc.、Chromalloy Gas Turbine LLC 和聖戈班。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 航太領域的需求不斷成長

- 越來越依賴燃氣渦輪發電

- 其他

- 限制因素

- 原物料價格不穩定

- 其他

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 按產品

- 金屬(黏合層)

- 陶瓷(面漆)

- 金屬間化合物

- 其他(金屬玻璃複合材料)

- 按最終用戶產業

- 車

- 航太

- 發電廠

- 石油和天然氣

- 其他(船舶、鐵路)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 合併、收購、合資、合作和協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- A&A Thermal Spray Coatings

- Chromalloy Gas Turbine LLC

- CTS, Inc.

- Hayden Corp.

- Honeywell International Inc.

- KECO Coatings

- Metallic Bonds, Ltd.

- Northwest Mettech Corp.

- OC Oerlikon Management AG

- Praxair ST Technology, Inc.

- Saint-Gobain

- Tech Line Coatings LLC

- ZIRCOTEC

第7章 市場機會與未來趨勢

- 終端用戶市場的技術進步

- 其他機會

The Thermal Barrier Coatings Market size is estimated at USD 1.21 billion in 2025, and is expected to reach USD 1.49 billion by 2030, at a CAGR of 4.31% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020 due to the unfavorable macroeconomics and operational restrictions across major end users of these coatings pushed back the demand during this period. However, the market is now estimated to reach pre-pandemic levels and is expected to grow steadily.

Key Highlights

- The shift from coal to natural gas-fired power generation and increasing demand from the aerospace sector are expected to drive demand for the thermal barrier coatings market.

- On the flip side, volatile raw material prices are expected to restrain demand in the market studied.

- The technological advancements in various end-user markets will likely provide new growth avenues for the market studied during the forecast period.

- North America dominated the global market. However, Asia-Pacific will likely witness the highest growth rate during the forecast period.

Thermal Barrier Coatings Market Trends

Aerospace Sector to Dominate the Market

- Thermal barrier coatings are commonly used to protect nickel-based superalloys from melting and thermal cycling in aviation turbines combined with cool airflow.

- Thermal barrier coatings increase the allowable gas temperature above the superalloy melting point. They reduce the temperature of the blade alloy and protect against oxidation and hot corrosion from high-temperature gas, thus increasing turbine performance, life expectancy, and efficiency.

- The increasing aircraft fleet and the rising defense expenditure increased aircraft production worldwide, creating immense demand for coatings like TBCs to protect engines and turbines.

- According to the data released by the Aeronautical Repair Station Association, the global aircraft fleet is expected to expand rapidly in the coming decade. It is expected to reach 38,100 aircraft by 2032 from 28,000 in 2023.

- According to the Boeing Commercial Outlook 2022-2041, the worldwide aerospace services industry is predicted to reach over USD 3.6 trillion, with the United States and Canada accounting for almost 30% of the market. Europe follows it with 23.5%, which will likely boost the demand for the studied market in the coming years.

- Furthermore, according to the Boeing Commercial Outlook 2022-2041, in China, around 8,485 new deliveries will be made by 2041 with a market service value of USD 545 billion. Thus, boosting the market growth.

- Overall, the market for thermal barrier coatings in the aerospace industry is expected to recover gradually through the forecast period and grow consistently.

North American Region to Dominate the Market

- The North American region is dominating the thermal barrier coatings market, owing to the significant demand from various end-user industries such as aerospace, automotive, power, and oil and gas.

- Moreover, the United States includes the largest share of the market studied. Besides the United States, Canada and Mexico contain a sizeable share of the market for thermal barrier coatings.

- Strong exports of aerospace components to countries such as France, China, and Germany, along with robust consumer spending in the United States, are driving the manufacturing activities in the aerospace industry. It can induce positive momentum for the market.

- In North America, according to the Boeing Commercial Outlook 2022-2041, the total deliveries of new airplanes will account for 9,310 units by 2041, with a market service value of USD 1,045 billion.

- According to the OICA, automotive production in North America in 2022 accounted for 17,756,263 units, an increase of 10% compared to the production in 2021, which was reported to be 16,190,835 units. Additionally, in North America, Over 10.06 million vehicles manufactured in 2022 were produced in the United States.

- Major countries in the North American region continued to get affected by the semiconductor microchip shortage and additional supply chain disruptions. For instance, According to the National Automobile Dealers Association (NADA), Light vehicle sales in 2022 recorded the lowest full-year sales in 2022 since 2011. They experienced an 8.2% annual decline compared to light vehicle sales in 2021.

- Hence, all the factors above are expected to significantly impact the demand for the thermal barrier coatings market in the region over the forecast period.

Thermal Barrier Coatings Industry Overview

The thermal barrier coatings market is fragmented in nature. Some of the major players in the market ( not in any particular order) include Honeywell International Inc., OC Oerlikon Management AG, Praxair ST Technology, Inc., Chromalloy Gas Turbine LLC, and Saint-Gobain, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Aerospace Sector

- 4.1.2 Growing Dependence on Gas-Fired Turbines for Power Generation

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Volatile Raw Material Prices

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product

- 5.1.1 Metal (Bond Coat)

- 5.1.2 Ceramic (Top Coat)

- 5.1.3 Intermetallic

- 5.1.4 Other Products (Metal Glass Composites)

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace

- 5.2.3 Power Plants

- 5.2.4 Oil and Gas

- 5.2.5 Other End-user Industries (Marine and Railways)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 A&A Thermal Spray Coatings

- 6.4.2 Chromalloy Gas Turbine LLC

- 6.4.3 CTS, Inc.

- 6.4.4 Hayden Corp.

- 6.4.5 Honeywell International Inc.

- 6.4.6 KECO Coatings

- 6.4.7 Metallic Bonds, Ltd.

- 6.4.8 Northwest Mettech Corp.

- 6.4.9 OC Oerlikon Management AG

- 6.4.10 Praxair S.T. Technology, Inc.

- 6.4.11 Saint-Gobain

- 6.4.12 Tech Line Coatings LLC

- 6.4.13 ZIRCOTEC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Technological Advancements in the End-user Market

- 7.2 Other Opportunities

隔熱塗層市場(按應用、技術、材料、最終用途產業和製程階段分類)—2025-2032 年全球預測

隔熱塗層市場(按應用、技術、材料、最終用途產業和製程階段分類)—2025-2032 年全球預測 2032 年隔熱塗層市場預測:按產品類型、塗層材料、技術、應用、最終用戶和地區進行的全球分析

2032 年隔熱塗層市場預測:按產品類型、塗層材料、技術、應用、最終用戶和地區進行的全球分析 2025-2033年隔熱塗料市場報告(依產品(壓克力、環氧樹脂、聚氨酯、氧化釔穩定氧化鋯、莫來石)、應用和地區)

2025-2033年隔熱塗料市場報告(依產品(壓克力、環氧樹脂、聚氨酯、氧化釔穩定氧化鋯、莫來石)、應用和地區) 隔熱塗層市場(材料類型、技術、應用和地區)2026-2032

隔熱塗層市場(材料類型、技術、應用和地區)2026-2032 隔熱塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

隔熱塗料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 熱障塗層市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、按最終用戶產業、按地區和競爭進行細分,2020-2030 年預測

熱障塗層市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、按最終用戶產業、按地區和競爭進行細分,2020-2030 年預測 隔熱塗層市場規模、佔有率和成長分析(按產品、技術、塗層組合、應用和地區)- 2025-2032 年產業預測隔熱塗層市場:依產品類型、塗層材料、技術、應用和地區分類

隔熱塗層市場規模、佔有率和成長分析(按產品、技術、塗層組合、應用和地區)- 2025-2032 年產業預測隔熱塗層市場:依產品類型、塗層材料、技術、應用和地區分類 全球隔熱塗料市場:市場規模、佔有率、趨勢分析(按產品和應用分列)、區域展望、未來預測(2024-2031)

全球隔熱塗料市場:市場規模、佔有率、趨勢分析(按產品和應用分列)、區域展望、未來預測(2024-2031) 隔熱塗料市場機會、成長動力、產業趨勢分析及2024年至2032年預測

隔熱塗料市場機會、成長動力、產業趨勢分析及2024年至2032年預測