|

市場調查報告書

商品編碼

1687703

GDPR 服務 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)GDPR Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

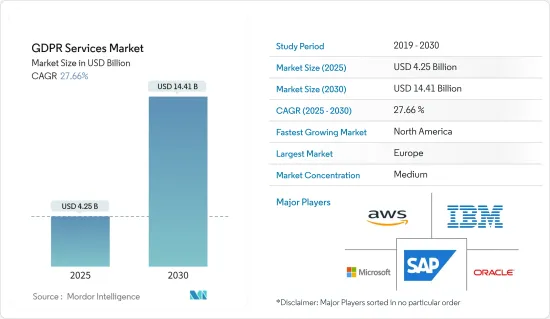

預計 2025 年 GDPR 服務市場規模為 42.5 億美元,預計到 2030 年將達到 144.1 億美元,預測期內(2025-2030 年)的複合年成長率為 27.66%。

由於連結性數位化的提高,企業正在產生大量資料。當人們造訪某個地點、網站,甚至打電話時,他們都會以資料的形式留下數位足跡,這是企業可以利用的寶貴資源,用於與客戶互動並提供更好的用戶體驗。隨著組織營運和品質監控對隱私性、安全性、真實性、合法性、可靠性、通用性和擴充性等特性的要求越來越高,GDPR服務業有著巨大的發展空間。

主要亮點

- 阿根廷公共資訊局已啟動修改《個人資料保護法》的諮詢程序。此次改革主要基於歐盟《一般資料保護條例》的規定。同樣,澳洲第二大電信業者Optus 在 9 月遭遇重大資料洩露,導致議員去年通過了《隱私權法改革法案》。

- 針對企業用戶的社交工程網路攻擊正在增加。迄今為止,網路上發現的一些較引人注目且範圍廣泛的宣傳活動包括冒充世界衛生組織 (WHO) 和美國疾病管制中心 (CDC) 的詐騙電子郵件。該網域與 CDC 官方網站相似,旨在竊取密碼,甚至要求比特幣「捐款」來資助假疫苗。此類案例增加了市場研究的需求。

- 此外,近年來連接設備的數量也在增加。據Cisco稱,預計去年M2M連線數量將達21億台。隨著資料傳輸技術的不斷進步,雲端服務變得越來越容易取得。公有雲已經登場。這項技術進步加速了網路釣魚電子郵件、機器人和勒索軟體的傳輸,凸顯了它們所帶來的漏洞。

- 為因應疫情並引發 GDPR 服務,網路安全預算變化增加。根據微軟公司在疫情初期對800名企業領導人進行的調查,36%的受訪者提案將網路安全預算增加1-25%,約22%的受訪者表示已將預算增加25%以上以應對疫情。這場疫情讓人們更加關注 GDPR 在個人權利和社會權利之間所取得的平衡。世界各地的當局正在改變其指導方針以解決資料保護和隱私問題。

- 另一方面,歐盟《一般資料保護規範》(GDPR)對雲端服務供應商和客戶提出了新的要求,例如刪除權、更正權和可攜性權,這不僅在技術角度,而且在實施和執行方面都帶來了挑戰。另一個新方面是整個雲端供應鏈中保護個人資料的共享責任模型。簡而言之,雲端客戶必須滿足 GDPR 的要求,這使得他們對資料主體負有一定課責。

一般資料保護規範(GDPR)服務市場趨勢

資料外洩後對資料安全和隱私的需求

- 據 SurfShark 稱,去年第三季度,全球約有 1500 萬筆資料記錄遭到資料外洩。與上一季相比,這一數字成長了37%。不遵守法規的巨額罰款也推動了對資料管治、資料映射和資料管理服務的需求,以減少資料外洩的數量並保護敏感資訊。資料外洩事件的增加可能會推動 GDPR 服務市場的發展。

- 資料外洩可能導致成本急劇增加,並造成寶貴的客戶資訊遺失。根據身分盜竊資源中心統計,2021年第三季美國銀行業和金融業資料外洩受害者數量達到1.6億,高於2021年第一季和第二季的總和1.21億。網路攻擊者正在尋求最明顯的途徑,對多個金融服務機構發動利潤豐厚的攻擊。

- 近年來,醫療保健產業已成為網路犯罪分子最感興趣的目標。這些寶貴資料的產生使得醫療保健系統近年來容易受到網路攻擊。根據 HIPAA 雜誌的報告,2021 年醫療保健機構發生了 56 起資料外洩事件,涉及資料超過 500 則。此外,報告發現,暴露或未經授權披露的記錄數量增加了約 24.5%,截至 2021 年 12 月,由於資料洩露,暴露或未經授權披露的記錄數量為 295 萬筆。

- 根據律師事務所 DLA Piper 的報告,GDPR 罰款上漲了近 40%,GDPR 罰款總額達到 1.915 億美元。此外,資料保護機構記錄了 121,165 起資料外洩報告,比去年同期成長了 19%。疫情期間,數位轉型的支出增加,這推動了對隱私的需求。根據為全球企業提供企業軟體的開發商工業金融系統公司(IFS)的一項調查顯示,70%的企業在疫情期間增加或維持了在數位轉型方面的支出。

- 在能源和石油等受到嚴格監管的行業中,資料外洩的成本很高。根據Leidos的資料,能源產業每筆記錄的成本為237美元,明顯高於平均的201美元。監控石油和天然氣分配和生產中的數量、速度、位置和其他關鍵活動的操作技術(OT) 系統不僅會產生大量敏感和專有資訊,而且對公司、設施和員工的經濟健康和人身安全也至關重要。

預計歐洲將佔大部分市場佔有率

- 歐洲對 GDPR 的接受度越來越高,因此 GDPR 服務預計將佔據很大的市場佔有率。隨著該地區努力發展成為資料驅動型地區,對 GDPR 的高度接受度已使各個組織廣泛採用 GDPR 服務。該法規要求這些國家的公司遵守GDPR。

- 自歐盟新資料保護法生效以來,歐洲資料保護機構已收到約 65,000 份資料外洩通知。此外,歐洲11個國家的監管機構已根據GDPR規定處以總計6,300萬美元的罰款。據年利達律師事務所稱,向資料保護機構發出的資料外洩通知大幅增加,與歐盟 GDPR 實施第一年相比平均成長了 66%。

- 隨著資料收集和共用加速利用人工智慧和其他新興技術,政府、企業和其他組織面臨著探索和採用完善的資料管理工具的需要,以在努力實現通用目標的同時保護資料所有者的權利。因此,各國政府正在探索新的途徑,以促進各資料生態系統相關人員之間的道德和公平資料共用。

- 該地區對物聯網汽車的需求日益成長。它包含可追溯到個人的個人資料。此外,還有利用家庭能源消耗模式的個人資料的智慧電錶。隨著 GDPR 在該地區生效,擁有一系列部署互聯解決方案的最終用戶的公司將需要保護其用戶的資料。預計這將增加對 GDPR 服務的需求。

- 去年 2 月,Google分析 (Google Analytics) 在法國被判定違反了歐盟資料保護法,此前奧地利也做出了類似的裁決。法國資料保護監管機構 CNIL 表示,這家未具名的本地網站對 Google Analytics 的使用違反了歐盟《一般資料保護規範》(GDPR),特別是第 44 條,該條款涵蓋將個人資料傳輸到歐盟以外的所謂第三國,而這些第三國本身並不具有同等的隱私權保護。

一般資料保護規範 (GDPR) 服務業概覽

GDPR 服務市場相當集中,主要企業包括 IBM、微軟和 AWS 等。此類參與者的市場滲透率很高。市場參與者正在創新,提供策略解決方案,以擴大其市場佔有率和基本客群。這將使您能夠贏得新契約並開拓新市場。市場的一些關鍵發展包括:

- 2022 年 9 月:Anritsu A/S 宣布與 SecuPi 進行最新合作,為客戶提供全球資料保護和 GDPR 合規性。最先受益於這項新聯盟的將是全球擁有最嚴格資料保護要求的一級通訊業者。安立與 SecuPi 合作,以市場領先的效率和靈活性滿足安全性和合規性要求。此次合作將使營運商能夠節省成本、簡化安裝並與安立的服務保障技術整合。

- 2022 年 4 月:Transcend 是一個一站式隱私平台,可以輕鬆地在公司的整個 IT 堆疊中對隱私進行編碼,並宣布資料映射將成為隱私程式的實用補充。 Transcend 的資料映射透過自動掃描、資料孤島發現和進階內容分類為現代企業實現統一資料管理。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 對 GDPR 服務市場的影響

第5章市場動態

- 市場促進因素

- 市場限制

第6章市場區隔

- 依實施類型

- 本地

- 雲

- 透過提供

- 資料管理

- 資料發現和映射

- 資料管治

- API 管理

- 按組織規模

- 大型企業

- 中小企業

- 按最終用戶

- 銀行、金融服務和保險(BFSI)

- 通訊和 IT

- 零售和消費品

- 醫療保健和生命科學

- 製造業

- 其他最終用戶產業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- IBM Corporation

- Veritas Technologies LLC

- Amazon Web Services Inc.

- Microsoft Corporation

- Micro Focus International PLC

- Oracle Corporation

- SAP SE

- Capgemini SE

- SecureWorks Inc.

- Wipro Limited

- DXC Technology Company

- Accenture PLC

- Atos SE

- Tata Consultancy Services Limited

- Larsen & Toubro Infotech Limited

- Infosys Limited

第8章投資分析

第9章:市場的未來

The GDPR Services Market size is estimated at USD 4.25 billion in 2025, and is expected to reach USD 14.41 billion by 2030, at a CAGR of 27.66% during the forecast period (2025-2030).

As a result of increased connection and ongoing digitization, businesses are producing an exponential amount of data. People who visit places and websites or even make phone calls leave a digital footprint as data, a valuable resource businesses can utilize to engage with customers and provide a better user experience. Because of the increased demand for characteristics such as privacy, security, authenticity, legality, trust, universality, and scalability in organizational operations and quality monitoring, the GDPR services industry has a lot of room to develop.

Key Highlights

- Argentina's Access to Public Information Agency has begun the consultation process to update its Personal Data Protection Law. The reforms are heavily based on the rules of the EU General Data Protection Regulation. Similarly, in September, Australia's second-largest telecommunications firm, Optus, had a significant data breach, prompting MPs to pass the Privacy Legislation Amendment Bill of the last year, which boosts fines to AUD 50 million when companies suffer repeated data breaches.

- Socially engineered cyber attacks targeting enterprise users are growing significantly. Among some of the significantly widespread campaigns spotted on the internet to date have been fraudulent emails indicated to be coming from the World Health Organization (WHO) and the US Center for Disease Control (CDC). The building domain names that look similar to the CDC's official web address aim at stealing passwords and even request bitcoin "donations" to fund a fake vaccine. Such instances have been increasing the demand for market studies.

- Further, there has been a rise in connected devices over the last few years. According to Cisco Systems, M2M connections are expected to reach 2.1 billion units in the last year. Cloud services are becoming more familiar with technological advancements in data transfers. The public cloud has been emerging. This technological advancement has resulted in the faster transfer of phishing emails, bots, and ransomware, indicating the vulnerabilities that they bring in.

- There has been a rise in the cybersecurity budget changes in response to the pandemic, triggering GDPR services. According to a survey by Microsoft Corporation of 800 business leaders during a pandemic, 36% of the respondents suggested an increase in the cybersecurity budget by 1-25%, and about 22% said that the budget increased by over 25% to combat the pandemic. The pandemic has brought a sharp focus to the balance that GDPR strikes between the rights of individuals and society. The global authorities are changing their guidelines to deal with data protection and privacy.

- On the flip side, the European Union General Data Protection Regulation (GDPR) confronts cloud service providers and customers with new requirements, such as the right to erasure, rectification, and portability, which is challenging to implement and implement not only from a technical perspective. Another new aspect appears with the model for shared responsibility regarding protecting personal data along the whole cloud supply chain. In a nutshell, the cloud customer remains accountable towards the data subject to an extent as they must fulfill the GDPR requirements.

General Data Protection Regulation (GDPR) Services Market Trends

Need for data security and privacy in the wake of a data breach

- According to SurfShark, Approximately 15 million data records were exposed globally due to data breaches in the third quarter of last year. Compared to the previous quarter, this amount had climbed by 37%. The rise in the need for data governance, data mapping, and data management services to mitigate the number of breaches and protect sensitive information has also been due to the significant fines levied for non-compliance with the regulation. Such a rise in data breaches would drive the GDPR service market.

- Data breaches lead to an exponential cost increase and loss of valuable customer information. According to Identity Theft Resource Center, the number of data breaches in the banking and financial sector of the United States the number of data compromise victims increased to 160 million in Q3 2021, which increased from Q1 and Q2 2021 combined (121 million). Cyber attackers pursue the most straightforward path possible to engineer a financial gain attack targeting several financial services organizations.

- Over the past few years, the healthcare sector has become a target of significant interest among cybercriminals. Due to its generation of valuable data, healthcare has recently become vulnerable to cyber-attacks. Per a HIPAA Journal report, healthcare institutions had 56 data breaches of 500 or more records in 2021. Moreover, the report also stated that the number of records exposed or impermissibly disclosed increased by approximately 24.5%, and data breaches left 2.95 million records exposed or impermissibly disclosed as of December 2021.

- According to a report from a law firm, DLA Piper, the GDPR fines rose by nearly 40%, and penalties under GDPR totaled USD 191.5 million. Also, allied data protection authorities recorded 121,165 breach notifications (19% more than the previous 12-month period). The spending on digital transformation increased during the pandemic, which has propelled a need for privacy. According to a survey conducted by Industrial and Financial Systems (IFS), a developer of enterprise software for companies worldwide, 70% of businesses have increased or maintained digital transformation spending during the pandemic.

- Costs of data breaches in heavily regulated industries, including energy and oil, have higher costs. The energy sector's USD 237 per record is significantly above the USD 201 average, according to Leidos data. The Operational Technology (OT) systems that oversee the volume, velocity, location, and other vital activities in the distribution and production of oil and gas not only produce a wealth of sensitive and proprietary information but are also essential to the economic health and physical safety of the company, its facilities, and its people.

Europe is Expected to Hold Major Share of the Market

- Europe is anticipated to witness a significant share of GDPR services due to the region's high acceptance of the GDPR. The region strives to develop as a data-driven region and exhibit significant adoption of GDPR services across organizations, owing to high acceptance of the GDPR. The regulation mandates the companies in these countries to comply with the GDPR.

- European privacy authorities have received nearly 65,000 data breach notifications since the EU's new privacy law was implemented. Also, regulators in 11 European countries imposed USD 63 million in GDPR fines. According to Linklaters, there has been a significant increase in data breach notifications to data protection authorities, with an average increase of 66% compared to the first year of the EU GDPR.

- In accelerating data collection and sharing to harness artificial intelligence and other emerging technologies, governments, businesses, and other organizations face the increasing need to explore and deploy sound data management tools to protect data owners' rights while addressing common goals. Therefore, governments are exploring new instruments to facilitate ethical and fair data sharing between different data ecosystem actors.

- The region is witnessing an increased demand for IoT-connected cars. This consists of individual data using which a person can be tracked. Then there is smart metering, whereby personal data on household energy consumption patterns is leveraged. With the GDPR being effect in the region, it has become necessary to secure the user's data for the companies with various end-users which deploy connected solutions. This is anticipated to drive the demand for GDPR services.

- In February last year, Google Analytics was found to violate European Union privacy legislation in France, following a similar ruling in Austria. The French data protection watchdog, the CNIL, stated that an unnamed local website's use of Google Analytics violates the EU's General Data Protection Regulation (GDPR) - specifically, Article 44, which covers personal data transfers outside the EU to so-called third countries that do not have essentially equivalent privacy protections.

General Data Protection Regulation (GDPR) Services Industry Overview

The GDPR Services Market is moderately consolidated, with some major players such as IBM, Microsoft, AWS, and others. The level of market penetration is high for such players. The players in the market are innovating in providing strategic solutions to increase their market presence and customer base. This enables them to secure new contracts and tap new markets. Some of the key developments in the market are:

- September 2022: Anritsu A/S has announced its latest collaboration with SecuPi to provide customers with global data protection and GDPR compliance. The first to benefit from this new alliance is a Tier-1 telecoms provider with some of the most demanding data protection requirements of any operator globally. Anritsu has teamed with SecuPi to fulfill security and compliance requirements with market-leading efficiency and flexibility. The collaboration will also provide operators with cost savings, ease of installation, and integration with Anritsu's Service Assurance technologies.

- April 2022: Transcend, the one-stop privacy platform that makes it simple to encode privacy across a company's IT stack has unveiled Data Mapping as an actionable addition to a privacy program. Transcend Data Mapping enables unified data management for modern businesses through automated scanning, data silo discovery, and advanced content classification-all in an easy-to-use and collaborative platform where users can easily assign system owners, delegate tasks, and generate compliance records.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/ Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact Of COVID-19 On the GDPR Services Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.2 Market Restraints

6 MARKET SEGMENTATION

- 6.1 By Type of Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Offering

- 6.2.1 Data Management

- 6.2.2 Data Discovery and Mapping

- 6.2.3 Data Governance

- 6.2.4 API Management

- 6.3 By Organization size

- 6.3.1 Large Enterprises

- 6.3.2 Small and Medium-sized Enterprises

- 6.4 By End User

- 6.4.1 Banking, Financial Services, and Insurance (BFSI)

- 6.4.2 Telecom and IT

- 6.4.3 Retail and Consumer Goods

- 6.4.4 Healthcare and Life Sciences

- 6.4.5 Manufacturing

- 6.4.6 Other End-user Industries

- 6.5 Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia-Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Veritas Technologies LLC

- 7.1.3 Amazon Web Services Inc.

- 7.1.4 Microsoft Corporation

- 7.1.5 Micro Focus International PLC

- 7.1.6 Oracle Corporation

- 7.1.7 SAP SE

- 7.1.8 Capgemini SE

- 7.1.9 SecureWorks Inc.

- 7.1.10 Wipro Limited

- 7.1.11 DXC Technology Company

- 7.1.12 Accenture PLC

- 7.1.13 Atos SE

- 7.1.14 Tata Consultancy Services Limited

- 7.1.15 Larsen & Toubro Infotech Limited

- 7.1.16 Infosys Limited

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球 GDPR 身分層市場:預測至 2032 年 - 按組件、部署類型、組織規模、最終用戶和地區進行分析

全球 GDPR 身分層市場:預測至 2032 年 - 按組件、部署類型、組織規模、最終用戶和地區進行分析 全球 GDPR 服務市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測

全球 GDPR 服務市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測 GDPR 服務市場報告(按產品、部署類型、組織規模、最終用戶和地區)2025 年至 2033 年

GDPR 服務市場報告(按產品、部署類型、組織規模、最終用戶和地區)2025 年至 2033 年 2025 年全球 GDPR 服務市場報告

2025 年全球 GDPR 服務市場報告 GDPR 服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按部署模式、按產品、按組織規模、按最終用戶行業、按地區、按競爭,2019-2029F

GDPR 服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分,按部署模式、按產品、按組織規模、按最終用戶行業、按地區、按競爭,2019-2029F GDPR 服務市場:按服務、組織規模和最終用戶分類 - 2025-2030 年全球預測GDPR合規服務的市場規模 - 按部署類型、提供的服務、組織規模和最終用戶 - 區域前景、競爭策略和細分市場預測(~2033年)

GDPR 服務市場:按服務、組織規模和最終用戶分類 - 2025-2030 年全球預測GDPR合規服務的市場規模 - 按部署類型、提供的服務、組織規模和最終用戶 - 區域前景、競爭策略和細分市場預測(~2033年)