|

市場調查報告書

商品編碼

1687432

塑化劑-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Bio-plasticizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

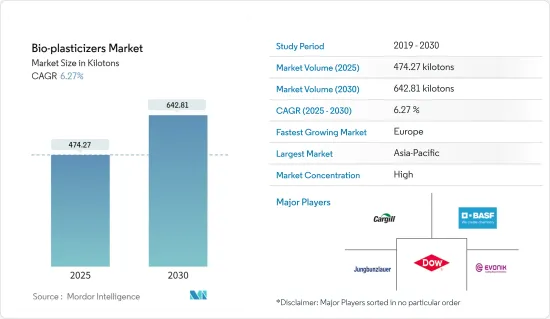

預計 2025 年塑化劑市場規模為 474.27 千噸,到 2030 年將達到 642.81 千噸,預測期內(2025-2030 年)的複合年成長率為 6.27%。

2020 年,新冠疫情對市場產生了負面影響。疫情期間,由於政府實施封鎖,建設活動暫時停止。這導致地板材料、牆壁材料、電線電纜等領域的生物塑化劑消費量下降,對生物塑化劑的需求產生負面影響。但在此情況下,食品和電商領域的包裝需求大幅增加,刺激了對含有生物塑化劑的包裝材料的需求,從而推動了市場成長。

主要亮點

- 短期內,軟性 PVC 生物塑化劑需求的增加以及鄰苯二甲酸酯塑化劑的禁令預計將推動市場成長。

- 與傳統塑化劑相比,塑化劑的成本較高,可能會阻礙市場成長。

- 對生物基塑化劑的持續研究可能會在預測期內為市場創造機會。

- 預計亞太地區將主導市場。此外,預計亞太地區在預測期內的複合年成長率最高。

塑化劑的市場趨勢

地板材料、屋頂和牆壁材料的需求增加

- 塑化劑有助於減少所需的水量,使混凝土更堅固、更易於加工。這些通常是有機材料,或有機和無機材料的組合,用於降低水分以提高可加工性。

- 塑化劑的加入量約為水泥重量的0.1~0.4%。此用量可將所需水量減少 5% 至 15%,同時還可提高可加工性,坍落度約為 3 至 8 公分。塑化劑一般會夾帶少於 2% 的空氣。

- 根據中國國家統計局的數據,2021年中國建築業產值達25.92兆元(4.02兆美元),而2020年為23.27兆元人民幣(3.37兆美元)。這增加了對地板材料和牆壁材料的需求,並擴大了生質塑膠的市場。

- 在印度,建築業是經濟成長的重要支柱。印度政府的目標是為約13億人提供住宅,並積極推動住宅建設。

- 此外,根據美國人口普查局的數據,2022 年美國年度新建築價值將達到 1.792 兆美元,而 2021 年為 1.626 兆美元。此外,2022 年美國住宅建築年價值為 9,080 億美元,比 2021 年的 8,030 億美元成長 13%。

- 因此,隨著節約水資源的要求不斷提高,地板材料和牆壁材料中塑化劑的使用量正在迅速增加。

- 由於這些因素,預計預測期內全球對塑化劑的需求將會成長。

亞太地區將主導市場成長

- 亞太地區建築業是世界上最大的建築業。隨著中階變得更加富裕以及越來越多的人遷入城市,這一數字正在以健康的速度成長。

- 基礎設施的改善以及主要企業進入中國利潤豐厚的市場也推動了該產業的發展。

- 近年來,隨著中央政府推動基礎設施投資以維持經濟成長,中國建設產業迅速發展。中國是建設產業的領導者,2022年建築業增加價值將達1.29兆美元。

- 此外,2022年日本新建住宅總占地面積約6,900萬平方公尺,低於2021年的7,000萬平方公尺。此外,2022年日本開工的住宅數量約為859,500套。這導致電線電纜、地板材料和牆壁材料等應用中塑化劑的消費量增加。

- 土地開發、豪華飯店、辦公大樓、國際會展中心、大型主題樂園建設營運等外商投資限制也已取消。未來幾年,由於基礎設施和運輸業的成長,該地區的生物塑膠市場預計將成長。

- 印度包裝工業協會(PIAI)也表示,印度正成為塑膠包裝產業的首選目的地。包裝產業是印度經濟第五大產業。

- 醫療健康產業穩定成長,全國醫療健康支出和醫療健康設施數量逐年增加。印度政府更開放的政策也允許100%的外國直接投資進入醫療設備市場。

- 印度政府推出了 NHP 計劃,這是世界上最大的政府資助醫療保健計劃。 《2022 年經濟調查》顯示,2021-22 年印度的醫療保健公共支出將佔 GDP 的 2.1%,而 2020-21 年這一比例為 1.8%。此外,印度政府計劃推出價值 5,000 億印度盧比(68 億美元)的信貸獎勵計劃,以加強該國的醫療保健基礎設施。

- 因此,預計上述因素將在預測期內對市場產生重大影響。

塑化劑產業概況

塑化劑市場本質上是部分整合的。市場上的主要企業(不分先後順序)包括陶氏化學、贏創工業股份公司、嘉吉公司、BASF股份公司和 Jungwanslauer Switzerland AG。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 軟性 PVC 需求不斷成長

- 更嚴格的鄰苯二甲酸酯法規促進塑化劑的使用

- 限制因素

- 塑化劑替代品的可用性

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 按類型

- 環氧大豆油(ESBO)

- 蓖麻油

- 檸檬酸鹽

- 琥珀酸

- 其他類型

- 按應用

- 電線電纜

- 薄膜和片材

- 地板材料、屋頂、牆壁材料

- 醫療設備

- 消費品

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 併購、合資、合作與協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- Avient Corporation

- BASF SE

- Cargill, Inc.

- DIC CORPORATION

- Dow

- Emery Oleochemicals

- Evonik Industries AG

- Hebei Jingu Plasticizer Co. Ltd.

- Jiangxi East Huge Dragon Chemical Co. Ltd.

- Jungbunzlauer Suisse AG

- LANXESS

- Matrica SpA

- OQ Chemicals gmbH

- Roquette Freres

第7章 市場機會與未來趨勢

- 擴大生物基塑化劑的研究

The Bio-plasticizers Market size is estimated at 474.27 kilotons in 2025, and is expected to reach 642.81 kilotons by 2030, at a CAGR of 6.27% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020. During the pandemic, construction activities were temporarily halted due to the government-imposed lockdown. This led to a decrease in the consumption of bio-plasticizers based on flooring and wall coverings, wires, and cables, which, in turn, negatively impacted the demand for bio-plasticizers. However, the demand for packaging from the food and e-commerce segment significantly increased during this situation, which, in turn, stimulated the demand for packaging materials made up of bio-plasticizers, thus enhancing the market growth.

Key Highlights

- Over the short term, the augmenting demand for bio-plasticizers for flexible PVC and the prohibition on phthalate-based plasticizers are expected to drive the growth of the market.

- The high cost of bio-plasticizers, when compared with conventional plasticizers, is likely to hinder the growth of the market.

- Ongoing research on bio-based plasticizers is likely to create opportunities for the market during the forecast period.

- The Asia-Pacific region is expected to dominate the market. It is also likely to witness the highest CAGR during the forecast period.

Bio Plasticizers Market Trends

Increasing Demand from Flooring, Roofing and Wall Covering

- Bio-plasticizers help reduce water requirements and make concrete strong and workable. These are generally organic substances or a combination of organic and inorganic substances that help reduce water content for workability.

- The quantity of plasticizers added is about 0.1%-0.4% by weight of cement. This amount reduces 5%-15% of the water requirement and also leads to an increase in workability from about a 3-8 cm slump. A plasticizer, in general, entrains less than 2% air.

- According to the National Bureau of Statistics of China, the output value of the construction works in the country accounted for CNY 25.92 trillion (USD 4.02 trillion) in 2021, compared to CNY 23.27 trillion (USD 3.37 trillion) in 2020. This led to an increase in the demand for flooring and wall covering, which, in turn, increased the demand for the bioplasticizers market.

- In India, the construction sector is an important pillar for the growth of the economy. The government is taking a number of steps to make sure that the country has good infrastructure by a certain date.The Indian government has been actively boosting housing construction as it aims to provide houses to about 1.3 billion people.

- Furthermore, according to the US Census Bureau, the annual value of new construction put in place in the United States accounted for USD 1,792 billion in 2022, compared to USD 1,626 billion in 2021. Moreover, the annual value of residential construction put in place in the United States was valued at USD 908 billion in 2022, an increase of 13% compared to USD 803 billion in 2021.

- Thus, with the growing demand for the conservation of water resources, the use of plasticizers is rapidly increasing in flooring and wall coverings.

- Owing to all these factors, the demand for bio-plasticizers is likely to grow across the world during the forecast period.

The Asia-Pacific Region to Dominate the Market Growth

- The Asia-Pacific construction industry is the largest in the world. It is growing at a healthy rate because the middle class is getting richer and more people are moving to cities.

- The expansion of the industry has also benefited from the addition of infrastructure and the entry of significant players from the European Union into China's lucrative market.

- China's construction industry has developed rapidly in the past few years, due to the central government's push for infrastructure investment as a means to sustain economic growth. China was leading in the construction industry, with an added value of USD 1.29 trillion in 2022.

- Also, the total floor space of new homes built in Japan in 2022 was about 69 million square meters, which was less than the 70 million square meters built in 2021. Additionally, in 2022, approximately 859,500 housing starts were initiated in Japan. This led to an increase in the consumption of bio-plasticizers for applications like wire, cables, flooring, and wall coverings.

- Foreign investment restrictions have also been lifted for land development, high-end hotels, office buildings, international exhibition centers, and building and running big theme parks. Over the next few years, the bioplasticizers market in the region is likely to grow due to growth in the infrastructure and transportation sectors.

- The Packaging Industry Association of India (PIAI) also says that India is becoming a place where the plastic packaging industry likes to be. The packaging industry is the fifth-largest sector in the Indian economy.

- The healthcare industry is growing steadily, with spending on healthcare and the number of medical facilities in the country going up every year. Indian government policies that have been made more open have also made it possible for 100% foreign direct investment in the medical devices market.

- In India, the government introduced the world's largest government-funded healthcare program, the NHP Scheme. In the Economic Survey of 2022, India's public expenditure on healthcare stood at 2.1% of GDP in 2021-22, compared with 1.8% in 2020-21. Additionally, the Indian government is planning to introduce a credit incentive program worth INR 500 billion (USD 6.8 billion) to boost the country's healthcare infrastructure.

- Therefore, the abovementioned factors are expected to have a significant impact on the market during the forecast period.

Bio Plasticizers Industry Overview

The bio-plasticizers market is partially consolidated in nature. Some major players in the market (not in any particular order) include Dow, Evonik Industries AG, Cargill, Inc., BASF SE, and Jungbunzlauer Suisse AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Flexible PVC

- 4.1.2 Stringent Phthalate Regulations to Boost the Use of Bio-Plasticizers

- 4.2 Restraints

- 4.2.1 Availability of Alternatives to bio-plasticizers

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Type

- 5.1.1 Epoxidized Soybean Oil (ESBO)

- 5.1.2 Castor Oil

- 5.1.3 Citrates

- 5.1.4 Succinic Acid

- 5.1.5 Other Types

- 5.2 By Application

- 5.2.1 Wire and Cables

- 5.2.2 Film and Sheet

- 5.2.3 Flooring, Roofing and Wall Covering

- 5.2.4 Medical Devices

- 5.2.5 Consumer Goods

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Avient Corporation

- 6.4.2 BASF SE

- 6.4.3 Cargill, Inc.

- 6.4.4 DIC CORPORATION

- 6.4.5 Dow

- 6.4.6 Emery Oleochemicals

- 6.4.7 Evonik Industries AG

- 6.4.8 Hebei Jingu Plasticizer Co. Ltd.

- 6.4.9 Jiangxi East Huge Dragon Chemical Co. Ltd.

- 6.4.10 Jungbunzlauer Suisse AG

- 6.4.11 LANXESS

- 6.4.12 Matrica SpA

- 6.4.13 OQ Chemicals gmbH

- 6.4.14 Roquette Freres

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Research In Bio-Based Plasticizers

2025-2033年生物塑化劑市場規模、佔有率、趨勢及預測(依產品、應用及地區)

2025-2033年生物塑化劑市場規模、佔有率、趨勢及預測(依產品、應用及地區) 2025年塑化劑全球市場報告

2025年塑化劑全球市場報告 塑化劑市場(按產品、最終用途和地區分類)

塑化劑市場(按產品、最終用途和地區分類) 塑化劑市場規模、佔有率和成長分析(按產品、應用和地區)- 產業預測 2025-2032

塑化劑市場規模、佔有率和成長分析(按產品、應用和地區)- 產業預測 2025-2032 塑化劑市場報告:2030 年趨勢、預測與競爭分析

塑化劑市場報告:2030 年趨勢、預測與競爭分析 全球塑化劑市場,2024-2028

全球塑化劑市場,2024-2028 全球生物塑化劑市場規模研究,按產品(環氧化大豆油、蓖麻油基塑化劑、檸檬酸鹽、琥珀酸等)、應用和區域預測2022-2032

全球生物塑化劑市場規模研究,按產品(環氧化大豆油、蓖麻油基塑化劑、檸檬酸鹽、琥珀酸等)、應用和區域預測2022-2032 生物塑化劑市場、佔有率、規模、趨勢、產業分析報告:依產品、應用、地區、細分市場預測,2024-2032

生物塑化劑市場、佔有率、規模、趨勢、產業分析報告:依產品、應用、地區、細分市場預測,2024-2032 生物塑化劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、應用、地區和競爭細分,2019-2029F生物塑化劑市場,按產品類型、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

生物塑化劑市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、應用、地區和競爭細分,2019-2029F生物塑化劑市場,按產品類型、應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測