|

市場調查報告書

商品編碼

1687360

高純度氧化鋁(HPA):市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)High-Purity Alumina (HPA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

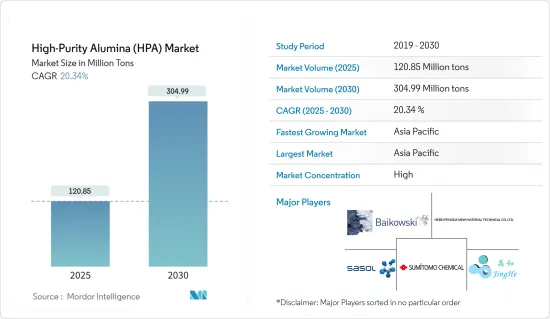

預計2025年高純度氧化鋁市場規模為1.2085億噸,2030年將達到3.0499億噸,預測期內(2025-2030年)的複合年成長率為20.34%。

新冠疫情阻礙了高純度氧化鋁市場的發展。最初,由於航太、汽車和電子等各行業為應對封鎖措施而縮減生產或暫停營運,對高純度氧化鋁的需求下降。這一趨勢減少了 LED 照明、半導體製造和鋰離子電池等應用對基於 HPA 的產品的需求。然而,隨著封鎖和限制的放鬆以及經濟活動的恢復,包括 LED 照明、半導體製造和鋰離子電池在內的一系列行業對基於 HPA 的材料的需求都在回升。

主要亮點

- LED照明和鋰離子電池需求的不斷成長是推動高純度氧化鋁市場發展的主要因素。

- 然而,高純度氧化鋁的高成本預計將阻礙高純度氧化鋁市場的成長。

- 由於HPA在智慧型手機和手錶的防刮玻璃和光學鏡片製造中的應用日益廣泛,預計高純度氧化鋁市場將在預測期內提供巨大的成長機會。

- 亞太地區是高純度氧化鋁的最大市場,預計在預測期內將以最高的複合年成長率成長。中國、日本和東南亞等國家對高純度氧化鋁的高需求推動了亞太地區的主導地位。

高純度氧化鋁(HPA)市場趨勢

LED照明領域可望佔據市場主導地位

- 高純度氧化鋁用作製造LED(發光二極體)晶片的基板材料。 LED 晶片通常安裝在基板上,以進行機械支撐和溫度控管。 HPA 具有高導熱性,可有效散熱,提高 LED 設備的性能和使用壽命。

- LED 照明越來越受歡迎,因為它比白熾燈和螢光等傳統照明技術更節能、壽命更長、更環保。住宅、商業和工業應用中對 LED 照明產品的需求不斷增加,推動了對高純度氧化鋁基板的需求。

- 根據美國能源局的數據,LED照明消費量在戶外領域最高,預計2025年將成長93%。

- 根據國際能源總署(IEA)的數據,LED比白熾燈可節省80-90%的能源。

- 根據國際能源總署 (IEA) 的數據,幾乎所有螢光都將於 2023 年逐步淘汰,歐盟 (EU) 也更新了《生態設計指令》和《限制有害物質指令》中的規定。在非洲,南部非洲發展共同體的16個國家已經採用了區域統一的照明標準,以便在未來幾年內將所有LED照明推向市場。

- 根據LED Lighting Supply預測,到2030年,LED預計將佔全球照明光源的87%。全球LED市場規模預計到2030年將成長至近1,000億美元。

- 根據TrendForce最新報告,2024年將是全球LED照明市場的關鍵一年,預計將有58億盞LED燈和燈具達到使用壽命。到2026年,市場規模預計將達到930億美元以上。隨著全球社會努力實現淨零排放,對節能 LED 轉換的需求預計將會增加。

- 考慮到上述事實和因素,預計預測期內基於 LED 的照明應用對 HPA 的需求將會增加。

亞太地區預計將主導市場

- 亞太地區是高純度氧化鋁及其最終用途產品的中心製造地。中國、日本、韓國和台灣等國家已經建立了強大的生產和加工高純度氧化鋁的製造基礎設施和供應鏈。

- 該地區正在經歷快速的都市化和工業化,推動汽車、電子、航太和醫療保健領域對高純度氧化鋁等先進材料的需求。這些產業對高純度氧化鋁產品的需求不斷成長,增強了該區域市場的主導地位。

- 此外,根據中國乘用車市場資訊聯席會(CPCA)的報告,中國正在推動電動車的普及,這可能會增加未來對鋰離子電池的需求。 2023年中國純電動車和插電式混合動力汽車銷量約950萬輛。

- 根據《經濟時報》發布的資料,2023年第三季印度電動車銷量達23,900輛。

- 2024 年 3 月,塔塔電子私人有限公司 (TEPL) 宣布計劃與台灣力晶半導體製造公司 (PSMC) 合作在古吉拉突邦建立半導體代工廠 (SFC)。計劃總投資預計為9兆印度盧比(1,097.1億美元)。力積電是台灣六大半導體代工廠之一。生產能力將涵蓋28nm製程高效能運算(HPC)晶片、處理器電源管理(PPM)晶片、電動車(EV)、通訊、國防、汽車、消費性電子(顯示器、電力電子)等領域。

- 預計預測期內亞太高純度氧化鋁市場的成長將受到上述因素的支持。

高純度氧化鋁(HPA)產業概況

高純度氧化鋁市場本質上是一體化的,市場領導者之間的競爭非常激烈。市場的主要企業(不分先後順序)包括河北鵬達新材料科技、住友化學、沙索、Baikowski、宣城精瑞新材料等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- LED照明需求不斷成長

- 鋰離子電池市場的需求

- 限制因素

- 高純度氧化鋁高成本

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 按類型

- 4N

- 5N

- 6N

- 依技術

- 水解

- 鹽酸浸出

- 按應用

- LED照明

- 磷光體

- 半導體

- 鋰離子電池

- 技術陶瓷

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 市場佔有率(%)分析

- 主要企業策略

- 公司簡介

- Baikowski

- Bestry Performance Materials Co. Ltd

- Hebei Pengda New Material Technology Co. Ltd

- Honghe Chemical

- Nippon Light Metal Co. Ltd

- Polar Sapphire

- Rusal

- Sasol(USA)Corporation

- Shandong Keheng Crystal Material Technology Co. Ltd

- Sumitomo Chemical Co. Ltd

- Wuxi Tuobada Titanium Dioxide Products Co. Ltd

- Xuancheng Jingrui New Materials Co. Ltd

第7章 市場機會與未來趨勢

- 防止智慧型手機、手錶和眼鏡刮傷的應用

- 擴大光學鏡頭製造的應用

The High-Purity Alumina Market size is estimated at 120.85 million tons in 2025, and is expected to reach 304.99 million tons by 2030, at a CAGR of 20.34% during the forecast period (2025-2030).

The COVID-19 pandemic hampered the high-purity alumina market. Initially, the demand for high-purity alumina declined as various industries, including aerospace, automotive, and electronics, scaled back production or temporarily shut down operations in response to lockdown measures. This trend reduced the demand for HPA-based products in applications such as LED lighting, semiconductor manufacturing, and lithium-ion batteries. However, as lockdown and restrictions eased and economic activities resumed, there was pent-up demand for HPA-based products in various industries, such as LED lighting, semiconductor manufacturing, and lithium-ion batteries.

Key Highlights

- The increased demand for LED-based lighting and lithium-ion batteries is the major factor driving the market for high-purity alumina.

- However, the high cost of high-purity alumina is expected to hamper the growth of the high-purity alumina market.

- Enormous opportunities are expected for the growth of the high-purity alumina market during the forecast period due to the growing use of HPA in scratch-resistant glasses for smartphones and watches and in the manufacture of optical lenses.

- Asia-Pacific has become the biggest market for high-purity alumina and is projected to register the highest CAGR over the forecast period. The high demand for high-purity alumina in countries such as China, Japan, and Southeast Asia is driving the dominance of Asia-Pacific.

High-Purity Alumina (HPA) Market Trends

The LED Lighting Segment is Expected to Dominate the Market

- High-purity alumina is used as a substrate material to produce LED (light-emitting diode) chips. LED chips are typically mounted on a substrate to provide mechanical support and thermal management. HPA's high thermal conductivity helps dissipate heat efficiently, thus improving the performance and lifespan of LED devices.

- LED lighting has gained widespread adoption due to its energy efficiency, long lifespan, and environmental benefits compared to traditional lighting technologies such as incandescent and fluorescent bulbs. The increasing demand for LED lighting products in residential, commercial, and industrial applications drives the demand for high-purity alumina substrates.

- According to the US Department of Energy, the outdoor segment holds the maximum consumption of LED lighting, which is expected to grow by 93% by 2025.

- According to the International Energy Agency, LEDs save 80-90% more energy than incandescent light bulbs.

- According to the International Energy Agency, in addition to removing virtually all fluorescent lighting in 2023, the European Union updated its regulations under the Ecodesign Directive and the Restriction of Hazardous Substances Directive. In Africa, a regionally harmonized lighting standard has been adopted in 16 countries of the Southern African Development Community in order to introduce all LED lighting to the market in the next few years.

- According to the LED Lighting Supply, LEDs are expected to increase up to 87% of global lighting sources by 2030. The global LED market is expected to grow to almost USD 100 billion in 2030.

- According to TrendForce's most recent reports, the year 2024 will be crucial for the global LED lighting market, with an estimated 5.8 billion LED lamps and luminaires reaching their end-of-life. In 2026, the market is expected to reach a value of more than USD 93 billion. As the global community attempts to achieve net zero emissions, the demand for energy-saving LED conversion is expected to increase.

- Considering all the abovementioned facts and factors, the demand for HPA for LED-based lighting applications is expected to increase during the forecast period.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is a central manufacturing hub for high-purity alumina and its end-use products. Countries like China, Japan, South Korea, and Taiwan have established robust manufacturing infrastructures and supply chains for high-purity alumina production and processing.

- The region has experienced rapid urbanization and industrialization, thus driving the demand for advanced materials like high-purity alumina in the automotive, electronics, aerospace, and healthcare sectors. The growing demand for high-purity alumina-based products in these sectors fuels the regional market's dominance.

- In addition, China is promoting the use of electric vehicles, which may increase the demand for lithium-ion batteries in the future, according to the China Passenger Car Association (CPCA) report. In China, around 9.5 million battery-electric cars and plug-in hybrids were sold in 2023.

- The electric vehicle sales in India reached 23,900 units in Q3 2023, according to the data released by the Economic Times.

- In March 2024, Tata Electronics Private Limited (TEPL), in collaboration with Powerchip Semiconductor Manufacturing Corporation (PSMC) Taiwan, announced its plans to set up a semiconductor fabrication plant (SFC) in the state of Gujarat. The total investment amount of the project is estimated at INR 9,000 billion (USD 109.71 billion). PSMC is one of the six largest semiconductor foundry companies in Taiwan. The capacity will cover segments like high-performance computing (HPC) chips with 28nm technology, processor power management (PPM) chips, electric vehicles (EVs), telecommunication, defense, automobile, and consumer electronics (display, power electronics).

- The growth of the Asia-Pacific high-purity alumina market is expected to be supported by the abovementioned factors over the forecast period.

High-Purity Alumina (HPA) Industry Overview

The high-purity alumina market is consolidated in nature, with intense competition among the top market players. The key players in the market (not in any particular order) include Hebei Pengda New Material Technology Co. Ltd, Sumitomo Chemical Co. Ltd, Sasol, Baikowski, and Xuancheng Jingrui New Materials Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for LED-based Lighting

- 4.1.2 Demand from Lithium-ion Battery Markets

- 4.2 Restraints

- 4.2.1 High Cost of High-purity Alumina

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 4N

- 5.1.2 5N

- 5.1.3 6N

- 5.2 Technology

- 5.2.1 Hydrolysis

- 5.2.2 Hydrochloric Acid Leaching

- 5.3 Application

- 5.3.1 LED Lighting

- 5.3.2 Phosphor

- 5.3.3 Semiconductor

- 5.3.4 Lithium-ion (Li-Ion) Batteries

- 5.3.5 Technical Ceramics

- 5.3.6 Other Applications

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share (%) Analysis

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Baikowski

- 6.3.2 Bestry Performance Materials Co. Ltd

- 6.3.3 Hebei Pengda New Material Technology Co. Ltd

- 6.3.4 Honghe Chemical

- 6.3.5 Nippon Light Metal Co. Ltd

- 6.3.6 Polar Sapphire

- 6.3.7 Rusal

- 6.3.8 Sasol (USA) Corporation

- 6.3.9 Shandong Keheng Crystal Material Technology Co. Ltd

- 6.3.10 Sumitomo Chemical Co. Ltd

- 6.3.11 Wuxi Tuobada Titanium Dioxide Products Co. Ltd

- 6.3.12 Xuancheng Jingrui New Materials Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Application in Scratch-resistant Glasses for Smartphones and Watches

- 7.2 Growing Applications in Manufacturing Optical Lenses

高純度氧化鋁市場按產品類型、形式、生產技術、應用和最終用戶分類-2025-2030 年全球預測

高純度氧化鋁市場按產品類型、形式、生產技術、應用和最終用戶分類-2025-2030 年全球預測 2025年高純度氧化鋁全球市場報告

2025年高純度氧化鋁全球市場報告 高純度氧化鋁市場規模、佔有率、趨勢及預測(按純度等級、生產方法、應用和地區),2025 年至 2033 年

高純度氧化鋁市場規模、佔有率、趨勢及預測(按純度等級、生產方法、應用和地區),2025 年至 2033 年 全球高純度氧化鋁市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測

全球高純度氧化鋁市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測 全球高純度紫杉葉素市場:市場佔有率和排名、總銷售量和需求預測(2025-2031)2026-2032年高純度氧化鋁市場(按等級、技術、應用和地區)

全球高純度紫杉葉素市場:市場佔有率和排名、總銷售量和需求預測(2025-2031)2026-2032年高純度氧化鋁市場(按等級、技術、應用和地區) 高速奈米研磨市場報告:趨勢、預測與競爭分析(至2031年)

高速奈米研磨市場報告:趨勢、預測與競爭分析(至2031年) 高純度氧化鋁市場規模、佔有率、趨勢分析報告:產品、應用、地區、細分市場預測,2025-2030

高純度氧化鋁市場規模、佔有率、趨勢分析報告:產品、應用、地區、細分市場預測,2025-2030 全球高純度氧化鋁市場:市場規模、市場佔有率、趨勢、行業分析(依產品、技術、應用和地區)、未來預測(2025-2034年)

全球高純度氧化鋁市場:市場規模、市場佔有率、趨勢、行業分析(依產品、技術、應用和地區)、未來預測(2025-2034年) 高純度氧化鋁市場規模、佔有率、成長分析、按產品類型、按技術、按應用、按最終用戶、按地區 - 產業預測,2024-2031年

高純度氧化鋁市場規模、佔有率、成長分析、按產品類型、按技術、按應用、按最終用戶、按地區 - 產業預測,2024-2031年