|

市場調查報告書

商品編碼

1687348

抗反射膜:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Anti-Reflective Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

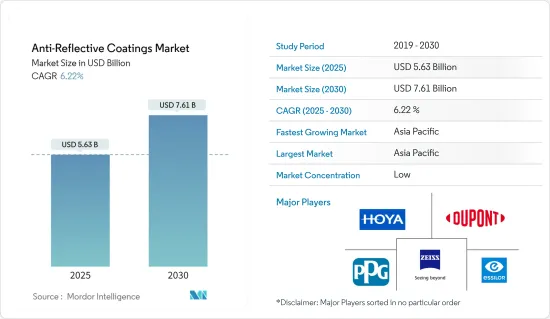

抗反射膜市場規模預計在 2025 年為 56.3 億美元,預計到 2030 年將達到 76.1 億美元,預測期內(2025-2030 年)的複合年成長率為 6.22%。

由於各國實施某些規則和規定,新冠疫情期間各行業的需求放緩。不過,2021年產業復甦,市場需求回升。

主要亮點

- 短期內,眼鏡應用需求的增加以及太陽能產業需求的增加預計將推動市場成長。

- 此外,抗反射膜的高成本和嚴格的環境法規預計將阻礙市場成長。

- 然而,薄膜製造技術的發展可能為市場提供有利的成長機會。

- 預計亞太地區將主導抗反射膜市場,並成為預測期內成長最快的市場。

抗反射膜市場趨勢

眼鏡需求不斷成長

- 防反射玻璃提供了一種經濟實惠的解決方案,可以減少各種電子顯示器(包括電腦螢幕、電視和平板)的眩光。

- 這些塗層可減少眩光、增強顯示可讀性、減輕眼睛疲勞並提高視覺清晰度。

- 根據美國衛生與公眾服務部的數據,美國40 歲以上人口中約有 23.9% 患有近視(約 3,400 萬人)。

- 根據世界衛生組織(WHO)的數據,截至2023年8月,全球約有22億人患有近視或遠視。此外,全球因視力障礙造成的生產力損失估計為 4,110 億美元。

- 美國視覺委員會估計,到 2023 年,美國眼鏡市場的價值將達到 656 億美元,這進一步凸顯了其重要性。美國擁有約 44,850 家實體店,93% 的美國成年人經常戴著某種類型的眼鏡產品。

- 因此,解決這些障礙有望刺激對相應眼鏡片的需求,從而進一步刺激該國對抗反射膜的需求。

中國可望主宰亞太地區

- 由於對半導體、電子設備、太陽能板和其他製造業務的需求不斷增加,亞太地區在全球市場佔據主導地位。中國的太陽能產業蓬勃發展,但卻受到產能過剩和貿易緊張局勢升級的困擾。西方國家擔心可能出現供應過剩,並向北京施壓,要求限制出口。根據國家能源局的資料,2023年中國安裝的太陽能板數量超過其他國家。這項成就進一步鞏固了中國在全球可再生能源領域的主導地位。令人驚訝的是,中國預計將在 2023 年增加 216.9 吉瓦的太陽能發電量,高於 2022 年的 87.4 吉瓦。

- 截至 2024 年第一季,中國仍保持著太陽能板安裝的勢頭,但與 2023 年 154% 的增幅相比有所放緩。根據國家能源局報告,到 2024 年 3 月,中國的累積太陽能裝置容量將達到 660 吉瓦,而到 2023 年底,美國的累計太陽能裝置容量將達到 179 吉瓦。

- 中國是全球最大的電子產品生產基地,其電子產業成長最為迅速,包括智慧型手機、電視、電線電纜、可攜式運算設備、遊戲系統和其他個人電子設備等電子產品。該國不僅滿足國內對電子設備的需求,也向其他國家出口電子產品。

- 2023年,中國半導體產業成長強勁,積體電路(IC)產量總計達3,514億塊,與前一年同期比較去年同期成長6.9%(據工業及資訊化部)。

- 此外,半導體產業協會也強調了中國在半導體製造業的進步。預測顯示,到 2024 年,中國在全球半導體產能的佔有率可能會飆升 13%,達到每月 860 萬片晶圓。

- 因此,由於上述因素,中國有望保持在亞太市場的主導地位。

抗反射膜產業概況

抗反射膜市場由杜邦、PPG工業公司、豪雅視力保健公司、蔡司國際和依視路等主要企業(排名不分先後)瓜分。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 眼鏡需求增加

- 太陽能產業需求不斷成長

- 其他

- 限制因素

- 抗反射膜成本高

- 嚴格的環境法規

- 其他

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 依成膜方法

- 化學沉澱沉積

- 電子束沉澱

- 濺鍍

- 其他

- 按應用

- 半導體

- 電子設備

- 眼鏡

- 太陽能板

- 車載顯示螢幕

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介(概況、財務狀況、產品與服務、最新發展)

- AccuCoat Inc.

- AGC Inc.

- Beneq

- DuPont

- Edmund Optics Inc.

- EKSMA Optics UAB

- ESSILOR OF AMERICA INC.

- Honeywell International Inc.

- HOYA

- Majestic Optical Coatings LLC

- Optical Coatings Japan

- Optics Balzers AG

- Optimum RX Group

- PPG Industries Inc.

- Spectrum Direct

- Torr Scientific Ltd

- ZEISS

- Zygo

第7章 市場機會與未來趨勢

- 薄膜製造技術的發展

- 其他機會

The Anti-Reflective Coatings Market size is estimated at USD 5.63 billion in 2025, and is expected to reach USD 7.61 billion by 2030, at a CAGR of 6.22% during the forecast period (2025-2030).

Due to specific rules and regulations imposed by countries, the demand in various sectors slowed during the COVID-19 pandemic. However, the industry recovered in 2021, rebounding the demand in the market.

Key Highlights

- Over the short term, the increasing demand for eyewear applications and rising demand from the solar power generation industry are expected to boost the market's growth.

- Additionally, the high cost of anti-reflective coatings and stringent environmental regulations are expected to hinder the market's growth.

- However, developing thin-film fabrication technologies will likely create lucrative growth opportunities in the market.

- Asia-Pacific is expected to dominate the anti-reflective coatings market and be the fastest-growing market during the forecast period.

Anti-Reflective Coatings Market Trends

The Demand for Eyewear Applications is Increasing

- Anti-reflective glasses offer an affordable solution to glare from various electronic displays, including computer screens, televisions, and flat panels.

- These coatings reduce glare, enhance display readability, lessen eye strain, and improve visual clarity.

- According to the US Department of Health & Human Services, nearsightedness affects about 23.9% of the United States's population over 40 (about 34 million people).

- According to the World Health Organization (WHO), as of August 2023, around 2.2 billion people worldwide had near or distant vision impairment. Moreover, the global costs of productivity losses associated with vision impairment are estimated to be USD 411 billion.

- The Vision Council highlights that the United States optical market was valued at USD 65.6 billion in 2023, further underlining its significance. The country boasts approximately 44,850 brick-and-mortar optical retail outlets, with a striking 93% of US adults regularly sporting some form of eyewear.

- This is expected to enhance the demand for respective eye lenses while addressing these impairments, further enhancing the demand for anti-reflective coatings in the country.

China is Expected to Dominate the Asia-Pacific Region

- Asia-Pacific has dominated the global market due to the increasing demand for semiconductors, electronics, solar panels, and other manufacturing operations. While China's solar industry is experiencing a boom, it grapples with overcapacity and escalating trade tensions. Western nations are pressuring Beijing to limit exports, fearing a potential oversupply. According to data from the National Energy Administration (NEA), in 2023, China installed more solar panels than any other nation. This achievement bolstered its already leading position in the global renewable energy landscape. In a remarkable display, China added 216.9 gigawatts of solar power in 2023, surpassing its 2022 record of 87.4 gigawatts.

- Also, as of the first quarter of 2024, China maintained its momentum in solar panel installations, albeit slower than the 154% surge seen in 2023. In March 2024, China's cumulative solar capacity reached 660 gigawatts, a stark contrast to the United States' 179 gigawatts by the end of 2023, as reported by the NEA.

- China has the world's largest electronics production base, which includes electronic products, such as smartphones, TVs, wires, cables, portable computing devices, gaming systems, and other personal electronic devices, and recorded the highest growth in the electronics segment. The country serves the domestic demand for electronics and exports electronic output to other countries.

- In 2023, China's semiconductor industry witnessed robust growth, with the total output of integrated circuits (ICs) reaching 351.4 billion pieces, marking a 6.9% increase from the previous year, as per the Ministry of Industry and Information Technology.

- Additionally, the Semiconductor Industry Association highlights China's strides in semiconductor manufacturing. Projections suggest that China's global semiconductor capacity share could surge by 13% in 2024, reaching 8.6 million monthly wafers.

- Thus, due to the above-mentioned factors, China is poised to maintain its dominance in the Asia-Pacific market.

Anti-Reflective Coatings Industry Overview

The anti-reflective coatings market is fragmented due to major players, including DuPont, PPG Industries Inc., Hoya Vision Care Company, Zeiss International, and Essilor (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Eyewear Applications

- 4.1.2 Rising Demand from the Solar Power Generation Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Anti-reflective Coatings

- 4.2.2 Stringent Environmental Regulations

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Deposition Method

- 5.1.1 Chemical Vapor Deposition

- 5.1.2 Electronic Beam Deposition

- 5.1.3 Sputtering

- 5.1.4 Other Deposition Methods

- 5.2 By Application

- 5.2.1 Semiconductors

- 5.2.2 Electronic Devices

- 5.2.3 Eyewear

- 5.2.4 Solar Panels

- 5.2.5 Automotive Displays

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 AccuCoat Inc.

- 6.4.2 AGC Inc.

- 6.4.3 Beneq

- 6.4.4 DuPont

- 6.4.5 Edmund Optics Inc.

- 6.4.6 EKSMA Optics UAB

- 6.4.7 ESSILOR OF AMERICA INC.

- 6.4.8 Honeywell International Inc.

- 6.4.9 HOYA

- 6.4.10 Majestic Optical Coatings LLC

- 6.4.11 Optical Coatings Japan

- 6.4.12 Optics Balzers AG

- 6.4.13 Optimum RX Group

- 6.4.14 PPG Industries Inc.

- 6.4.15 Spectrum Direct

- 6.4.16 Torr Scientific Ltd

- 6.4.17 ZEISS

- 6.4.18 Zygo

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Thin Film Fabrication Technologies

- 7.2 Other Opportunities

全球抗反射膜市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球抗反射膜市場規模、佔有率、趨勢和成長分析報告(2026-2034) 抗反射膜市場:按應用和地區分類

抗反射膜市場:按應用和地區分類 抗反射膜市場報告:按技術、層類型、應用和地區分類(2026-2034 年)

抗反射膜市場報告:按技術、層類型、應用和地區分類(2026-2034 年) 抗反射膜市場:依材料體系、沉積製程、塗層結構、基材類型、商業模式及最終用途產業分類-2026-2032年全球市場預測

抗反射膜市場:依材料體系、沉積製程、塗層結構、基材類型、商業模式及最終用途產業分類-2026-2032年全球市場預測 2026-2030年全球抗反射膜市場

2026-2030年全球抗反射膜市場 抗反射膜市場規模、佔有率和成長分析(按層類型、技術、基板、樹脂類型、應用和地區分類)—產業預測(2026-2033 年)

抗反射膜市場規模、佔有率和成長分析(按層類型、技術、基板、樹脂類型、應用和地區分類)—產業預測(2026-2033 年) 抗反射膜市場:全球產業分析、市場規模、佔有率、成長、趨勢與預測(2025-2032)全球抗反射膜市場規模(按應用、技術、地區和預測)

抗反射膜市場:全球產業分析、市場規模、佔有率、成長、趨勢與預測(2025-2032)全球抗反射膜市場規模(按應用、技術、地區和預測)