|

市場調查報告書

商品編碼

1687341

金屬基複合材料:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Metal Matrix Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

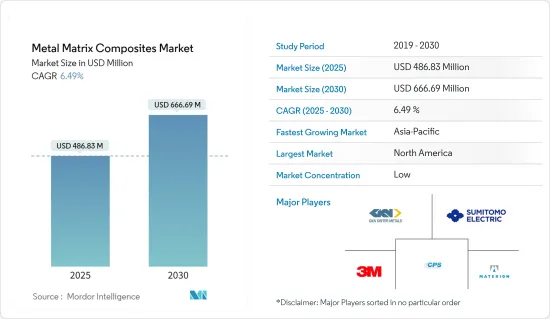

金屬基複合材料市場規模預計在 2025 年為 4.8683 億美元,預計到 2030 年將達到 6.6669 億美元,預測期內(2025-2030 年)的複合年成長率為 6.49%。

在 2020 年 COVID-19 疫情期間,全球封鎖和社交距離措施導致供應鏈中斷和各個製造業倒閉。這對市場產生了負面影響。但疫情過後,市場正重回正軌。

主要亮點

- 航太和國防工業對輕量材料以及比金屬具有更優異性能的金屬基複合材料的需求不斷成長,是市場的主要驅動力。

- 然而,複雜的製造流程可能會阻礙市場成長。

- 機車行業的擴大使用和電動車的日益普及預計將為市場創造新的機會。

- 北美佔有最高的市場佔有率。然而,預計亞太地區將在預測期內佔據市場主導地位。

金屬基複合材料的市場趨勢

電氣電子產業快速成長

- 金屬基複合材料廣泛應用於各種電氣和電子元件和設備。例如,鋁石墨複合材料因其優異的導熱性、可調節的熱膨脹係數和低密度而被用於電力電子模組。

- 鋁和銅經過碳化矽 (SiC) 強化,具有更好的熱性能,例如低熱膨脹係數 (CTE) 和高熱導率,以及更好的機械性能,例如更高的比強度、優異的耐磨性和高的比彈性模量,因此可用於各種行業。

- 戴馬合金(Dymalloy)由含有55%鑽石顆粒(體積分數)的銅銀合金基體組成,由於其高導熱性,被用作電子設備中高功率、高密度多晶片模組的基板。

- 此外,高體積分數的PRMMC(顆粒增強金屬基複合材料)在電子工業中具有廣泛的應用,例如散熱面板、功率半導體封裝、微波模組、電池套管、黑盒子機殼和印刷基板散熱器等。

- 根據日本電子情報技術產業協會(JEITA)發布的《世界電子統計》顯示,預計2021年全球電子及IT產業產值將達到3.3602兆美元,與前一年同期比較成長11%;2022年將達到3.5366兆美元,較上年成長5%。

- 預計行動電話、可攜式計算設備、遊戲系統和其他個人電子設備的生產將繼續推動對電子元件的需求,從而促進對金屬基複合材料的需求。

- 由於上述因素,預測期內市場對電氣和電子設備的需求可能會增加。

亞太地區佔市場主導地位

- 亞太地區佔全球電子產品產量的70%以上,韓國、日本和中國等國家參與製造各種電子元件並向全球各產業供應產品。

- 2021年前9個月,亞太地區汽車產量為3,267萬輛,較去年同期成長11%。

- 總體而言,中國、印度、日本和韓國等國家的持續需求成長可能會推動該地區金屬基複合材料市場的發展。

- 2021年12月,中國工業生產年增4.3%。因此,預測期內該國工業部門的擴張預計將有利於金屬基複合材料市場的成長。

- 中國工業與資訊化部資料顯示,2022年1-5月,電子資訊製造業維持穩定成長,規模以上電子資訊製造業增加價值年增9.9%。

- 印度政府推出了一項 PLI 計劃,該計劃將在五年內為在印度擴大生產的製造商提供 55 億美元的獎勵。預計這將促進該國的電子產品生產並對金屬基複合材料的需求產生積極影響。

- 在航太領域,根據印度品牌股權基金會 (IBEF) 的數據,印度航空業預計將在未來四年吸引 35,000 億印度盧比(49.9 億美元)的投資。

- 此外,2022年1-4月日本電子產業產值為36,564.40億日圓(約326億美元),較2021年同期成長約0.2%。

- 預計上述因素將增加亞太地區各應用產業對金屬基複合材料的需求。

金屬基複合材料產業概況

全球金屬基複合材料市場本質上是部分分散的,行業中有大量全球和本地參與者。市場的主要企業包括 GKN Sinter Metals Engineering GmbH、Materion Corporation、3M、住友電氣工業有限公司、CPS Technologies Corporation 等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 航太和國防工業對輕量材料的需求不斷增加

- 金屬基複合材料具有優於金屬的性能

- 限制因素

- 複雜的製造程序

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 技術簡介

第5章市場區隔

- 按類型

- 鎳

- 鋁

- 耐火材料

- 其他

- 填料

- 碳化矽

- 氧化鋁

- 碳化鈦

- 其他

- 按最終用戶產業

- 汽車和機車

- 電氣和電子

- 航太與國防

- 工業

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 併購、合資、合作與協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- 3A Composites

- 3M(Ceradyne Inc.)

- ADMA Products Inc.

- CPS Technologies Corp.

- DAT Alloytech

- Denka Company Limited

- GKN Sinter Metals Engineering GmbH

- Hitachi Metals Ltd

- Materion Corporation

- MTC Powder Solutions AB

- Plansee Group

- Sumitomo Electric Industries Ltd

- Thermal Transfer Composites LLC

- TISICS Ltd

第7章 市場機會與未來趨勢

- 擴大在機車產業的應用

- 電動車日益普及

The Metal Matrix Composites Market size is estimated at USD 486.83 million in 2025, and is expected to reach USD 666.69 million by 2030, at a CAGR of 6.49% during the forecast period (2025-2030).

During the pandemic period in 2020 due to COVID-19, there were nationwide lockdowns and social distancing mandates which led to supply chain disruption and the closure of various manufacturing industries. This impacted the market negatively. However, in the post-pandemic period, the market is getting back on track.

Key Highlights

- Increasing demand for lightweight materials in the aerospace and defense industry and superior properties of metal matrix composites over metals are the major driving factors for the market.

- However, the complicated manufacturing process is likely to hinder the market growth.

- Growing use in the locomotive industry and increasing adoption of electric vehicles are expected to provide new opportunities for the market.

- North America accounted for the highest market share. However, Asia-Pacific is projected to dominate the market during the forecast period.

Metal Matrix Composites Market Trends

Electrical and Electronics Segment to Register Fastest Growth

- Metal matrix composites are used in various electrical and electronic components and devices. For instance, aluminum-graphite composites are employed in power electronic modules due to their excellent thermal conductivity, tunable coefficient of thermal expansion, and low density.

- Al and Cu reinforced by SiC are used in various industries due to their excellent thermo-physical properties, such as low coefficient of thermal expansion (CTE), high thermal conductivity, and improved mechanical properties, such as higher specific strength, better wear resistance and specific modulus.

- Because of its high heat conductivity, dymalloy, a copper-silver alloy matrix containing 55% diamond particles (by volume), is utilized as a substrate for high-power, high-density multi-chip modules in electronics.

- In addition, PRMMCs (particulate reinforced metal matrix composites), with a high-volume fraction, have a wide range of applications in the electronics industry, including radiator panels, power semiconductor packages, microwave modules, battery sleeves, black box enclosures, printed circuit board heat sinks, and others.

- According to the global electronics statistics published by the Japan Electronics and Information Technology Industries Association (JEITA), the Production by the global electronics and IT industries is expected to grow 11% year on year in 2021 to reach USD 3,360.2 billion, with 2022 production too lifting 5% to USD 3,536.6 billion.

- The production of cellular phones, portable computing devices, gaming systems, and other personal electronic devices will continue to spark the demand for electronic components, which is expected to boost the demand for metal matrix composites.

- Owing to all the factors mentioned above, the demand for electrical and electronic equipment is likely to increase the demand in the market studied during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific accounts for more than 70% of global electronics production, with countries like South Korea, Japan, and China involved in manufacturing various electrical components and supplies to various industries globally.

- The Asia-Pacific region recorded 32.67 million of total automotive production in the nine months of 2021, an increase of 11% from the same period in 2020.

- Overall, the consistent growth in demand in countries like China, India, Japan, and South Korea is likely to boost the metal matrix composites market in the region.

- Industrial production in China increased by 4.3% year-on-year in December 2021. Thus, the expansion of the industrial sector in the country is anticipated to benefit the growth of the metal matrix composites market during the forecast period.

- According to China's data from the Ministry of Industry and Information Technology, the electronic information manufacturing sector maintained steady growth in the first five months of 2022. The value-added output of electronic information manufacturers with annual operating revenue of at least CNY 20 million (about USD 3 million) expanded 9.9 percent year-on-year during the period.

- The government launched the PLI scheme, which is likely to offer incentives as manufacturers increase production in India with USD 5.5 billion available over five years. This is likely to boost the production of electronics in the country, thus benefiting the demand for metal matrix composites.

- In the aerospace sector, according to the India Brand Equity Foundation (IBEF), the country's aviation industry is expected to witness INR 35,000 crore (USD 4.99 billion) investment in the next four years.

- Moreover, in the first four months of 2022, the production by the Japanese electronics industry accounted for JPY 3,656.44 billion (USD 32.60 billion), registering a growth rate of around 0.2% compared to the same period in 2021.

- The factors mentioned above are likely to ascend the demand for metal matric composites across the application industries in Asia-Pacific.

Metal Matrix Composites Industry Overview

The global metal matrix composites market is partially fragmented in nature, with the presence of a large number of global and local players in the industry. The major players in the market include GKN Sinter Metals Engineering GmbH, Materion Corporation, 3M, Sumitomo Electric Industries Ltd, and CPS Technologies Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Lightweight Materials in Aerospace and Defense Industry

- 4.1.2 Superior Properties of Metal Matrix Composites over Metals

- 4.2 Restraints

- 4.2.1 Compilicated Manufacturing Process

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Technological Snapshot

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Nickel

- 5.1.2 Aluminium

- 5.1.3 Refractory

- 5.1.4 Other Types

- 5.2 Fillers

- 5.2.1 Silicon Carbide

- 5.2.2 Aluminum Oxide

- 5.2.3 Titanium Carbide

- 5.2.4 Other Fillers

- 5.3 End-user Industry

- 5.3.1 Automotive and Locomotive

- 5.3.2 Electrical and Electronics

- 5.3.3 Aerospace and Defense

- 5.3.4 Industrial

- 5.3.5 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3A Composites

- 6.4.2 3M (Ceradyne Inc.)

- 6.4.3 ADMA Products Inc.

- 6.4.4 CPS Technologies Corp.

- 6.4.5 DAT Alloytech

- 6.4.6 Denka Company Limited

- 6.4.7 GKN Sinter Metals Engineering GmbH

- 6.4.8 Hitachi Metals Ltd

- 6.4.9 Materion Corporation

- 6.4.10 MTC Powder Solutions AB

- 6.4.11 Plansee Group

- 6.4.12 Sumitomo Electric Industries Ltd

- 6.4.13 Thermal Transfer Composites LLC

- 6.4.14 TISICS Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Use in Locomotive Industry

- 7.2 Increasing Adoption of Electric Vehicles

金屬複合材料市場:2026-2032年全球市場預測(按基體金屬類型、增強材料類型、加工方法、應用和最終用途行業分類)

金屬複合材料市場:2026-2032年全球市場預測(按基體金屬類型、增強材料類型、加工方法、應用和最終用途行業分類) 金屬複合材料市場規模:按類型、增強材料、增強形式、製造技術、終端應用產業和地區分類(2026-2034 年)金屬複合軸承市場:按軸承類型、材料、分銷管道、結構和應用分類的全球預測,2026-2032年

金屬複合材料市場規模:按類型、增強材料、增強形式、製造技術、終端應用產業和地區分類(2026-2034 年)金屬複合軸承市場:按軸承類型、材料、分銷管道、結構和應用分類的全球預測,2026-2032年 金屬陶瓷複合材料市場規模、佔有率和成長分析:按材料類型、應用、最終用戶、幾何形狀和地區分類-2026-2033年產業預測

金屬陶瓷複合材料市場規模、佔有率和成長分析:按材料類型、應用、最終用戶、幾何形狀和地區分類-2026-2033年產業預測 金屬複合材料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測

金屬複合材料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年預測 金屬基複合材料全球市場報告(2026)

金屬基複合材料全球市場報告(2026) 航太金屬複合材料市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、基體類型、增強體類型、地區和競爭格局分類,2021-2031年

航太金屬複合材料市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、基體類型、增強體類型、地區和競爭格局分類,2021-2031年 超輕金屬基複合材料市場預測至2032年:按材料類型、增強材料類型、製造流程、最終用戶和地區分類的全球分析

超輕金屬基複合材料市場預測至2032年:按材料類型、增強材料類型、製造流程、最終用戶和地區分類的全球分析 金屬鑽石複合材料:全球市佔率及排名、總收入及需求預測(2025-2031年)金屬基複合材料市場預測至2032年:全球按類型、基體類型、增強體類型、增強材料、技術、應用和地區分類的分析

金屬鑽石複合材料:全球市佔率及排名、總收入及需求預測(2025-2031年)金屬基複合材料市場預測至2032年:全球按類型、基體類型、增強體類型、增強材料、技術、應用和地區分類的分析