|

市場調查報告書

商品編碼

2044153

透明顯示器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Transparent Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

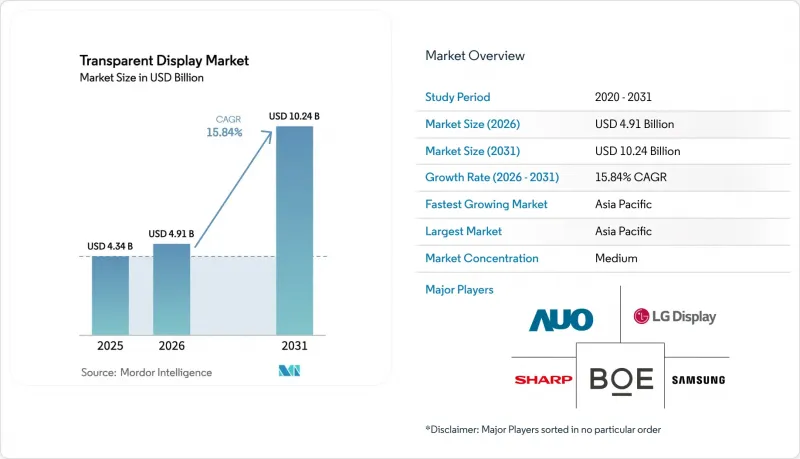

2025年透明顯示器市值為43.4億美元,預計到2031年將達到102.4億美元,而2026年為49.1億美元,預測期(2026-2031年)複合年成長率為15.84%。

汽車原始設備製造商(OEM)正在整合擴增實境(AR)抬頭顯示器,奢侈品零售商正在利用互動式櫥窗吸引消費者重返實體店,國防相關企業正在測試透明裝甲駕駛座,使飛行員能夠觀察周圍環境。 2026年2月「四方安全對話」(Quad Alliance)的成立表明,一級供應商開始將透明面板視為可擴展的平台,而非小眾的附加功能。垂直整合的製造商仍在承擔8.6代有機發光二極體晶圓廠的資本負擔,這些晶圓廠的初始良率可能低至50%。在中國以外,氧化銦錫(ITO)的價格超過每公斤400美元,這給沒有長期供應合約的一體化製造商帶來了壓力。這些因素共同造就了一個市場,在這個市場中,規模、穩定的採購和先進的光學技術決定著競爭優勢。

全球透明顯示器市場趨勢及洞察

在汽車抬頭顯示器和叢集顯示器領域的應用日益廣泛。

汽車製造商正在將透明顯示器整合到擋風玻璃和儀錶板中,以便駕駛員無需將視線從道路上移開即可接收導航訊息和碰撞警報。由蔡司、德莎、聖戈班世科瑞特和現代摩比斯於2026年2月成立的四方聯盟(Quad Alliance)的目標是在2029年前實現全像抬頭顯示器(HUD)的量產,併計劃將垂直視場角擴大至現有系統的三倍。 2025年9月,偉世通與FUTURUS合作,將擴增實境(AR)抬頭顯示器引入中型轎車。這圖透過提高產量來降低單位成本。監管方面的進展也十分顯著,聯合國歐洲經濟委員會第125號法規要求前向設備的透明度至少達到70%,而ISO/TS 21957:2023標準則規範了檢驗程序,並將核准週期縮短了數月。 2025年3月,科思創推出了一款透過ISO 16750-3機械衝擊測試的聚碳酸酯中階,讓供應商更有信心提供多年保固。隨著標準的明確、供應商之間的合作以及抗衝擊材料的出現,預計到2028年,透明抬頭顯示器將成為許多主流車型的標準配備。

身臨其境型店面零售數位電子看板的需求

奢侈品牌和購物中心營運商正透過採用透明顯示螢幕,將豐富的多媒體內容疊加在實體商品上,從而將櫥窗轉變為動態廣告媒介。 2025年9月,LG Display在東京一家精品店安裝了一塊55吋的透明有機發光二極體面板,測試結果顯示顧客停留時間提升了30%至40%。 2025年11月,Glass-Media推出了透光率高達85%的超薄透明LED海報,使零售商能夠在不遮擋視線的情況下每隔幾秒鐘切換宣傳活動。快餐店和交通樞紐也逐步採用類似的技術,因為這種顯示器可以直接安裝在傳統螢幕無法安裝的玻璃門和隔間牆上。低功耗有機發光二極體面板(每平方公尺功耗低於50瓦)有助於連鎖店滿足LEED能源認證的要求。隨著內容管理平台向雲端遷移,本地加盟商可以遠端更新數百家門市的商店顯示螢幕,從而加速將這項技術推廣到旗艦店以外的更多門市。

透明面板製造廠的收益率低、資本投入高。

第八代有機發光二極體和microLED製造工廠需要無塵室、噴墨頭和多層封裝設備,這使得資本投資超過40億美元,並限制了新進業者。 TCL華星光電於2025年10月開始興建這類工廠,預算為41.5億美元,但該公司承認,投產第一年的良率將維持在50%左右。 Universal Display 2025年第三季財報強調了運轉率將對整個供應鏈的利潤率構成壓力的風險。良率下降的原因在於透明陰極的顆粒污染以及水蒸氣的侵入會劣化有機材料。只有多元化集團才能承受多年的投資回收期,這將抑制全球產能的擴張,並導致面板價格持續高企,直到2028年以後良率超過80%。

細分市場分析

液晶顯示器(LCD)憑藉成熟的製造流程和低於每平方公尺100美元的面板價格,預計到2025年仍將維持45.13%的最大市場佔有率。然而,其透光率上限約為70%,亮度很少超過500尼特,限制了其在戶外的應用。有機發光二極體(OLED)正以15.84%的複合年成長率快速發展,其自發光像素無需背光即可達到1000尼特的亮度,已符合聯合國歐洲經濟委員會(UNECE)針對汽車抬頭顯示器(HUD)的發光強度標準。隨著零售商和汽車製造商為更高的對比度支付溢價,預計到2029年, 有機發光二極體面板的透明顯示市場規模將超過LCD面板的銷售量。 MicroLED預計將擁有更長的使用壽命,並得益於流體自組裝和雷射傳質技術,這些技術可將缺陷率控制在10ppm以下,預計到2031年,MicroLED將以15.93%的複合年成長率保持最高成長率。透明投影膜和電致變色膜則適用於一些特殊安裝環境和智慧窗戶,在這些應用中,動態不透明度和低成本比影像解析度更為重要。

製造商正據此調整產品系列。韓國企業利用其專有的有機發光二極體堆疊技術來鎖定高利潤的細分市場,而中國製造商則向室內指示牌供應低成本的LCD顯示單元。隨著時間的推移,第8.6代有機發光二極體生產線良率的提高可望縮小與LCD的成本差距,進而促進中型零售商的升級。同時,航太領域的客戶更傾向微型LED,其透光率接近90%,亮度遠超過5000尼特——這些都是有機發光二極體無法企及的。這種市場分化使得供應商能夠專注於特定的應用場景,而不是追求「通用」策略。

零售數位電子看板佔最大佔有率,預計到2025年將佔銷售額的30.47%,這主要得益於身臨其境型商店的蓬勃發展,這些商店將實體產品與數位故事敘述相結合。汽車領域預計將以16.29%的複合年成長率實現最高成長,抬頭顯示器和叢集顯示器正從豪華車的選配逐漸成為量產車型的標準配置。隨著ISO和UNECE標準的實施降低了型式認證的風險,預計從2027年起,汽車透明顯示器的市佔率將穩定成長。消費性電子和智慧電子產品仍然是一個規模雖小但充滿活力的細分市場,微型有機發光二極體技術的進步顯著降低了光學串擾,並提高了在明亮環境下的可視性。

由於採購週期較長,航太和國防專案進展緩慢,但高利潤率彌補了產量不足的問題。在能夠提高生產效率的領域,工業和企業應用(例如倉庫揀貨指示燈系統和醫療圖像疊加顯示)正穩步成長。在醫療和教育領域,透明螢幕正被用於手術規劃和博物館展覽,但由於情境察覺,原始設備製造商 (OEM) 正在設計符合業界特定標準的透明顯示器,例如 SAE J1757/1 和 IEC 62471。這增加了認證成本,但獲得核准可以加強供應商的鎖定作用。

區域分析

預計到2025年,亞太地區將佔全球銷售額的40.38%,年複合成長率高達16.56%,成為成長最快的地區,這主要得益於中國強大的LCD和有機發光二極體基礎設施以及韓國的高階有機發光二極體技術。京東方(BOE)在2024年國際消費電子展(CES 2024)上展示了一款55英寸4K透明有機發光二極體顯示螢幕,旨在實現量產和出貨,以此挑戰韓國老牌製造商的地位。 LG Display和三星也推出了售價在五位數區間的透明有機發光二極體和MicroLED原型產品,目標客戶為高階零售商和汽車製造商。日本透過夏普和JAPAN DISPLAY等公司提供工業解決方案,但由於面板產能有限,印度市場對透明OLED的接受度仍處於起步階段。

北美和歐洲是成熟市場,但它們受監管主導。 2024年9月,美國對中國銦徵收25%的關稅,迫使整合商要麼確保長期供應,要麼接受利潤率下降的局面。聯合國歐洲經濟委員會第125號法規明確了70%透明度標準,加速了歐洲汽車製造商對該標準的採用。聖戈班SageGlass等智慧窗戶供應商正在為升級建築外圍護結構的業主提供LEED(能源與環境設計先鋒獎)積分。在中東,一種兼具發電和串流播放功能的雙用途外牆玻璃正在被推廣應用,以符合淨零排放的要求。

南美洲和非洲的市場仍處於起步階段。巴西零售業和南非智慧城區試點計畫的實施表明了可行性,但受到進口關稅和有限資金預算的限制。總體而言,亞太地區仍然是生產中心,而北美和歐洲已建立了貫穿整個供應鏈的績效和永續性標竿。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車抬頭顯示器和叢集顯示器的應用日益廣泛

- 對身臨其境型零售數位電子看板的需求

- AR/ VR頭戴裝置的快速普及

- MicroLED透明面板成本降低藍圖

- 雙用途幕牆玻璃,整合透明光伏顯示螢幕

- 國防投資透明裝甲駕駛座

- 市場限制因素

- 透明面板製造廠的收益率低、資本投入高。

- 與傳統顯示器相比,亮度和對比度不足

- 氧化銦錫(ITO)供應風險與價格波動

- 由於汽車眩光安全法規,實施工作有所延誤。

- 價值/供應鏈分析

- 監理情勢

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭程度

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 透過技術

- LCD

- OLED

- 微型LED

- 透明投影(LCoS/DLP)

- 其他

- 按最終用戶行業分類

- 零售數位電子看板

- 家用電器和智慧電器

- 車

- 航太/國防

- 產業與公司

- 其他(醫療保健、教育)

- 透過使用

- 互動式商店與展示

- 抬頭顯示器(HUD)

- 擴增實境(AR)穿戴式設備

- 智慧窗戶和建築玻璃

- 展覽和博物館展品

- 按顯示尺寸

- 10吋或更小(微型)

- 10吋至39吋(中號)

- 40吋或更大(大號)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 亞太其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- LG Display Co., Ltd.

- Samsung Electronics Co., Ltd.

- BOE Technology Group Co., Ltd.

- Leyard Optoelectronic Co., Ltd.(Planar Systems Inc.)

- Panasonic Holdings Corporation

- Sharp Corporation

- AU Optronics Corporation

- Sony Group Corporation

- Crystal Display Systems Ltd.

- Pro Display UK Ltd.

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Nexnovo Technology Co., Ltd.

- Shenzhen AuroLED Technology Co., Ltd.

- Tianma Micro-electronics Co., Ltd.

- Visionox Technology Inc.

- Japan Display Inc.

- 2Point0 Concepts LLC

- Xiaomi Inc.

- Visteon Corporation

- Continental AG

第7章 市場機會與未來展望

The Transparent display market size was valued at USD 4.34 billion in 2025 and is estimated to grow from USD 4.91 billion in 2026 to reach USD 10.24 billion by 2031, at a CAGR of 15.84% during the forecast period (2026-2031). Automotive original equipment manufacturers are embedding augmented-reality head-up displays, luxury retailers are adopting interactive storefronts to draw consumers back into physical stores, and defense contractors are testing transparent-armor cockpits that keep pilots aware of their surroundings. The formation of the QuadAlliance in February 2026 signals that Tier-1 suppliers now view transparent panels as a scalable platform rather than a niche add-on. Vertically integrated manufacturers continue to absorb the capital burden of Gen 8.6 organic light-emitting diode fabs where initial yields can be as low as 50%. Indium-tin-oxide prices above USD 400 per kilogram outside China are squeezing integrators that lack long-term supply contracts. These converging forces are shaping a market in which scale, secure sourcing, and advanced optics define competitive advantage.

Global Transparent Display Market Trends and Insights

Rising Adoption in Automotive HUD and Cluster Displays

Original equipment manufacturers are embedding transparent displays in windshields and instrument panels so drivers can receive navigation cues and collision alerts without shifting their gaze. The QuadAlliance formed in February 2026 by ZEISS, tesa, Saint-Gobain Sekurit, and Hyundai Mobis is targeting 2029 mass production of holographic head-up displays, tripling vertical field of view compared with today's systems. Visteon partnered with FUTURUS in September 2025 to migrate augmented-reality HUDs into mid-tier sedans, a move that will lower unit costs through higher volumes. Regulatory momentum is visible as UNECE Regulation 125 requires at least 70% transparency for forward-vision devices, while ISO/TS 21957:2023 harmonizes test procedures, cutting approval time by months. Covestro introduced polycarbonate interlayers in March 2025 that pass ISO 16750-3 mechanical-shock tests, giving suppliers confidence to offer multi-year warranties. Collectively, standards clarity, supplier alliances, and ruggedized materials point to transparent HUDs becoming standard on many mainstream vehicles by 2028.

Retail and Digital-signage Demand for Immersive Storefronts

Luxury labels and mall operators are installing transparent displays that overlay rich media onto physical products, turning windows into dynamic advertising canvases. LG Display deployed 55-inch transparent organic light-emitting diode panels across Tokyo boutiques in September 2025 and reported a 30% to 40% lift in dwell time during pilots. Glass-Media introduced ultra-thin transparent LED posters in November 2025 with 85% transparency, enabling retailers to rotate campaigns every few seconds while maintaining unobstructed views. Quick-service restaurants and transit hubs are following suit because transparent panels attach directly to glass doors or partition walls where conventional screens cannot fit. Low-power organic light-emitting diode variants consuming under 50 watts per square meter help chains meet LEED energy prerequisites. As content-management platforms move to the cloud, regional franchises can update hundreds of storefronts remotely, accelerating roll-outs beyond flagship locations.

Low Yield and High CAPEX of Transparent Panel Fabs

Gen 8.6 organic light-emitting diode and micro-LED fabs demand cleanrooms, inkjet printing heads, and multilayer encapsulation tools that push capital expenditure above USD 4 billion, limiting new entrants. TCL CSOT broke ground on such a facility in October 2025 with a USD 4.15 billion budget yet acknowledged yields will hover near 50% during the first production year. Universal Display's third-quarter 2025 results underscored the risk when lower utilization drags on margins across the supply chain. Yield losses originate from particulate contamination in transparent cathodes and water-vapor ingress that degrades organics. Only conglomerates with diversified earnings can endure multi-year payback periods, which curbs global capacity expansion and keeps panel prices elevated until yields climb above 80% post-2028.

Other drivers and restraints analyzed in the detailed report include:

- Rapid AR and VR Headset Proliferation

- Cost-down Roadmap for Micro-LED Transparent Panels

- Indium-tin-oxide Supply Risk and Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid-crystal display retained the largest 45.13% revenue share in 2025 due to mature tooling and panel prices under USD 100 per square meter. Transparency, however, tops out near 70% and brightness rarely exceeds 500 nits, which restricts outdoor use. Organic light-emitting diode is advancing at a 15.84% CAGR and already meets UNECE photometric criteria for automotive HUDs because self-emissive pixels hit 1,000 nits without a backlight. The transparent display market size for organic light-emitting diode panels is projected to overtake liquid-crystal display revenue by 2029 as retailers and automakers pay premiums for higher contrast. Micro-LED promises even longer lifetimes and is forecast to post the fastest 15.93% CAGR through 2031, supported by fluidic self-assembly and laser mass-transfer techniques that drive defect rates below 10 ppm. Transparent projection and electrochromic films serve specialty installations and smart windows, where imagery resolution is less critical than dynamic opacity or low cost.

Manufacturers segment their portfolios accordingly. Korean firms leverage proprietary organic light-emitting diode stacks to defend high-margin niches, while Chinese producers ship low-cost liquid-crystal display units for indoor signage. Over time, rising yields from Gen 8.6 organic light-emitting diode lines narrow the cost gap with liquid-crystal display, encouraging mid-tier retailers to upgrade. Conversely, aerospace customers favor micro-LED for cockpit transparency near 90% and brightness well above 5,000 nits, performance unattainable with organic light-emitting diode. This bifurcation lets suppliers target discrete use cases rather than pursuing a one-size-fits-all strategy.

Retail and digital signage generated the largest slice of 2025 revenue at 30.47%, driven by immersive storefronts that merge physical goods with digital storytelling. Automotive is on course for the sharpest 16.29% CAGR because head-up and cluster displays are transitioning from luxury options to standard features across volume models. The transparent display market share for automotive applications is expected to rise steadily after 2027 as ISO and UNECE standards reduce homologation risk. Consumer electronics and smart appliances remain a smaller but vibrant niche where micro-organic light-emitting diode advances slash optical crosstalk, improving readability in bright rooms.

Aerospace and defense projects progress slowly under extended procurement cycles, yet high margins compensate for low volumes. Industrial and enterprise deployments such as warehouse pick-to-light systems and medical imaging overlays grow steadily where situational awareness pays productivity dividends. Healthcare and education adopt transparent screens for surgical planning and museum exhibits, though budgets limit unit sales. Overall, OEMs design transparent displays to meet sector-specific standards like SAE J1757/1 and IEC 62471, which elevates certification cost but reinforces vendor lock-in once approvals are secured.

The Transparent Display Market Report is Segmented by Technology (LCD, OLED, Micro-LED, and More), End-User Industry (Retail and Digital Signage, Consumer Electronics and Smart Appliances, and More), Application (Interactive Storefronts, HUD and More), Display Size (Less Than 10", 10"-39", and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific generated 40.38% of 2025 sales and will log the highest 16.56% CAGR thanks to China's liquid-crystal display and organic light-emitting diode base and South Korea's premium organic light-emitting diode prowess. BOE demonstrated a 55-inch 4K transparent organic light-emitting diode at CES 2024 and aims to ship in volume, challenging Korean incumbents. LG Display and Samsung unveiled transparent organic light-emitting diode and MicroLED prototypes that cost five-figure sums yet address premium retail and automotive clients. Japan contributes industrial solutions through Sharp and Japan Display, whereas India's adoption is still nascent given limited panel-making capacity.

North America and Europe are mature but regulation driven. The United States imposed a 25% tariff on Chinese indium in September 2024, pushing integrators to lock long-term supply or absorb margin erosion. UNECE Regulation 125 provides clarity on 70% transparency thresholds, accelerating European automaker adoption. Smart-window providers such as Saint-Gobain SageGlass secure Leadership in Energy and Environmental Design points for building owners upgrading their envelopes. The Middle East pursues dual-use facade glass that generates power while streaming media, aligning with net-zero mandates.

South America and Africa remain early-stage markets. Pilot deployments in Brazil's retail sector and South Africa's smart-city corridors demonstrate feasibility but are constrained by import duties and limited capital budgets. Overall, Asia Pacific remains the production powerhouse, while North America and Europe set performance and sustainability benchmarks that reverberate through the supply chain.

List of Companies Covered in this Report:

- LG Display Co., Ltd.

- Samsung Electronics Co., Ltd.

- BOE Technology Group Co., Ltd.

- Leyard Optoelectronic Co., Ltd. (Planar Systems Inc.)

- Panasonic Holdings Corporation

- Sharp Corporation

- AU Optronics Corporation

- Sony Group Corporation

- Crystal Display Systems Ltd.

- Pro Display UK Ltd.

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Nexnovo Technology Co., Ltd.

- Shenzhen AuroLED Technology Co., Ltd.

- Tianma Micro-electronics Co., Ltd.

- Visionox Technology Inc.

- Japan Display Inc.

- 2Point0 Concepts LLC

- Xiaomi Inc.

- Visteon Corporation

- Continental AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption in Automotive HUD and Cluster Displays

- 4.2.2 Retail and Digital-signage Demand for Immersive Storefronts

- 4.2.3 Rapid AR/VR Headset Proliferation

- 4.2.4 Cost-down Roadmap for Micro-LED Transparent Panels

- 4.2.5 Dual-use Facade Glass Integrating Transparent PV-displays

- 4.2.6 Defense Investment in Transparent Armoured Cockpits

- 4.3 Market Restraints

- 4.3.1 Low Yield and High CAPEX of Transparent Panel Fabs

- 4.3.2 Sub-optimal Brightness / contrast Versus Conventional Displays

- 4.3.3 Indium-tin-oxide (ITO) Supply Risk and Price Volatility

- 4.3.4 Automotive Glare-safety Regulations Delaying Roll-outs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

- 4.7 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 LCD

- 5.1.2 OLED

- 5.1.3 Micro-LED

- 5.1.4 Transparent Projection (LCoS / DLP)

- 5.1.5 Other Technologies

- 5.2 By End-user Industry

- 5.2.1 Retail and Digital Signage

- 5.2.2 Consumer Electronics and Smart Appliances

- 5.2.3 Automotive

- 5.2.4 Aerospace and Defense

- 5.2.5 Industrial and Enterprise

- 5.2.6 Others (Healthcare, Education)

- 5.3 By Application

- 5.3.1 Interactive Storefronts and Showcases

- 5.3.2 Head-Up Displays (HUD)

- 5.3.3 Augmented-Reality Wearables

- 5.3.4 Smart Windows and Architectural Glass

- 5.3.5 Exhibition and Museum Installations

- 5.4 By Display Size

- 5.4.1 Less than 10" (Micro)

- 5.4.2 10" - 39" (Medium)

- 5.4.3 Greater than or equal to 40" (Large)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 LG Display Co., Ltd.

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 BOE Technology Group Co., Ltd.

- 6.4.4 Leyard Optoelectronic Co., Ltd. (Planar Systems Inc.)

- 6.4.5 Panasonic Holdings Corporation

- 6.4.6 Sharp Corporation

- 6.4.7 AU Optronics Corporation

- 6.4.8 Sony Group Corporation

- 6.4.9 Crystal Display Systems Ltd.

- 6.4.10 Pro Display UK Ltd.

- 6.4.11 Hangzhou Hikvision Digital Technology Co., Ltd.

- 6.4.12 Nexnovo Technology Co., Ltd.

- 6.4.13 Shenzhen AuroLED Technology Co., Ltd.

- 6.4.14 Tianma Micro-electronics Co., Ltd.

- 6.4.15 Visionox Technology Inc.

- 6.4.16 Japan Display Inc.

- 6.4.17 2Point0 Concepts LLC

- 6.4.18 Xiaomi Inc.

- 6.4.19 Visteon Corporation

- 6.4.20 Continental AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

透明顯示器市場:按技術、面板尺寸、應用和最終用途分類-2026-2032年全球市場預測

透明顯示器市場:按技術、面板尺寸、應用和最終用途分類-2026-2032年全球市場預測 透明顯示器市場規模、佔有率和趨勢分析報告:按解析度、顯示器尺寸、技術、應用、地區和細分市場預測(2026-2033 年)

透明顯示器市場規模、佔有率和趨勢分析報告:按解析度、顯示器尺寸、技術、應用、地區和細分市場預測(2026-2033 年) 透明顯示器市場按產品類型、解析度類型、最終用戶和地區分類

透明顯示器市場按產品類型、解析度類型、最終用戶和地區分類 2026年全球透明顯示器市場報告

2026年全球透明顯示器市場報告 透明顯示器市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、解析度、最終用戶、地區和競爭格局分類,2021-2031年

透明顯示器市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、解析度、最終用戶、地區和競爭格局分類,2021-2031年 透明顯示器市場規模、佔有率及成長分析(按類型、技術、解析度、尺寸、最終用戶和地區分類)-2026-2033年產業預測

透明顯示器市場規模、佔有率及成長分析(按類型、技術、解析度、尺寸、最終用戶和地區分類)-2026-2033年產業預測 全球透明顯示器市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032)

全球透明顯示器市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032) 透明顯示器:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

透明顯示器:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 透明顯示器市場、機會、成長動力、產業趨勢分析與預測,2024-2032

透明顯示器市場、機會、成長動力、產業趨勢分析與預測,2024-2032