|

市場調查報告書

商品編碼

1687334

超級電腦:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Supercomputers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

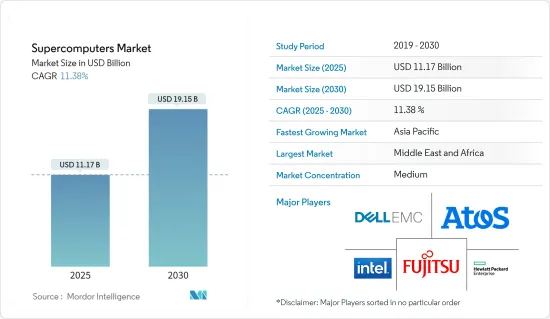

超級電腦市場規模預計在 2025 年為 111.7 億美元,預計到 2030 年將達到 191.5 億美元,預測期內(2025-2030 年)的複合年成長率為 11.38%。

超級電腦憑藉其高效能的處理能力,作為運行人工智慧(AI)程式的核心設備正變得越來越重要。其架構擅長處理人工智慧和機器學習應用的大量資料需求。

全球範圍內對高效能運算 (HPC) 應用的日益普及正在推動市場

主要亮點

- 超級電腦以其強大的運算能力和速度而聞名,在高效能運算 (HPC) 系統中發揮關鍵作用。由於其性能,它已成為 HPC 領域不可或缺的一部分。隨著科學研究轉向基於模擬的技術並且機器學習(ML)變得越來越重要,超級電腦的市場需求正在顯著增加。

- 此外,2024 年 10 月,受市場對其最新超級運算 AI 晶片 Blackwell 強勁需求的樂觀情緒推動,NVIDIA 股價創下歷史新高。這凸顯了超級電腦良好的成長軌跡,有助於推動整體市場擴張。

- 隨著組織處理複雜的資料和分析工作負載,對超級電腦的需求可能會成長。對於學術和研究機構來說,超級電腦變得越來越容易獲得且具有成本效益。此外,運算能力民主化的趨勢日益成長,特別是透過雲端運算的平台即服務模式,也正在進一步推動市場的發展。

超級運算系統初始成本高是市場成長的主要阻礙因素

主要亮點

- 高昂的擁有成本(包括設備價格、住房基礎設施和營運費用)使得超級電腦價格昂貴,並成為市場成長的障礙。例如,2024年3月,微軟與OpenAI聯合打造了一台價值約1000億美元的基於AI的超級電腦。這表明這種超級電腦主要面向大型企業,不適用於中小型企業。

國家之間的地緣政治衝突可能會影響市場成長

主要亮點

- 國防部門對超級電腦加強網路防禦和攻擊的需求正在支持政府部門的市場成長。此外,2024 年 4 月,美國國務院網路安全負責人檢測到異常活動,顯示中國已經開發出一台量子超級電腦。這種演變能夠破解所有西方加密,從而摧毀網路防禦。

超級電腦市場趨勢

商業業是最大的終端用戶

- 汽車公司正迅速擁抱商用超級電腦。全球供應商和汽車公司客製化這些應用程式以滿足特定產業需求。超級電腦在汽車領域的主要應用包括碰撞分析、結構分析和計算流體力學。這些顯著提高了產品質量,降低了成本,並使我們能夠應對以前無法克服的挑戰。鑑於業界競爭激烈,採用超級電腦已成為全球汽車產業供應商的必要條件。

- 例如,特斯拉在2024年2月宣布,將投資5億美元,將其Dojo超級電腦安置在紐約州水牛城的Riverbend Gigafactory。這超級電腦將訓練特斯拉的人工智慧(AI)系統,這對於自動駕駛至關重要。預計它將成為訓練機器學習模型和處理特斯拉電動車產生的大量資料的主要計算平台。

- 在能源領域,超級電腦,尤其是配備加速器的超級超級電腦,使高效能運算 (HPC) 工作負載更加節能。正在開發新的演算法來處理龐大的資料集並獲取更高解析度的圖像。這項進步將有助於確定地下碳氫化合物的位置,特別是在巴西、墨西哥灣、安哥拉和地中海東部等惡劣的地質環境中。透過更早評估探勘區塊和資產機會,公司可以更有選擇地開展業務。

亞太地區預計將顯著成長

- 亞太地區正在迅速崛起,成為技術進步的領導者,尤其是在超級運算系統的發展方面,中國和日本等國家做出了重大貢獻。

- 在亞太地區,快速的經濟成長、對研發 (R&D) 的大量投資以及對先進運算能力不斷成長的需求正在刺激高效能運算 (HPC) 的持續採用和發展。

- 中國研究人員團隊研發了一種量子電腦原型,可以透過隨機取樣高斯粒子來區分多達 76 個光子。中國研究人員正在挑戰Google、亞馬遜和微軟等美國巨頭,爭奪這項前沿技術的主導地位。印度在亞太舞台上也取得了顯著進展。該國已啟動國家超級運算任務,目標是到2023年建造一個擁有73個高效能運算設施的超級運算網格,預計投資額為7.3億美元。

- 2024 年 2 月,中國悄悄推出了名為「天河三號」的超級電腦,據稱它是世界上最強大的機器。該機器由廣州國家超級電腦計算中心開發,由於其神秘性質引發了許多猜測。天河三號超級電腦名為星儀,是中國國防科技大學建造的系列超級電腦中的最新一台。

- 2024年9月,印度推出Paraludra超級運算系統,標誌著其技術旅程取得重大飛躍。該先進設施由先進運算發展中心(C-DAC)開發,將增強印度的高效能運算能力,特別是在天氣和氣候運算方面。

- 新加坡政府於 2024 年 10 月宣布將撥款 2.7 億新元(2.017 億美元)用於加強國家的超級運算基礎設施。這項投資旨在加強新加坡國家超級計算中心(NSCC)的能力並確保對當地研究舉措的支持。這項消息是由該國副總理兼國家研究基金會 (NRF) 主席在 ASPIRE 2A 和 2A+ 系統正式發佈時宣布的。這些先進的研究超級電腦由 NSCC 管理。預計這些發展將在預測期內推動該地區超級電腦市場的成長。

超級電腦產業概況

該市場由多家全球和地區參與者組成,它們都在激烈的競爭中爭奪關注。然而,它主要由擁有巨大市場佔有率的大型供應商主導,它們競相在各個地理市場站穩腳跟並成為先驅。

供應商正在採取競爭策略,利用其創新能力和研發投資能力來鞏固其在市場上的地位。因此,這項策略將加劇市場競爭。

分銷管道、現有業務關係、更好的供應鏈知識以及高效能運算解決方案的開發使現有的科技巨頭比新參與企業擁有市場優勢。總體而言,供應商競爭激烈,預計在預測期內仍將保持這種狀態。

主要市場參與者包括 Atos SE、英特爾公司、惠普企業公司、戴爾 EMC(戴爾科技公司)和富士通有限公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 評估宏觀經濟因素對市場的影響

第5章市場動態

- 市場促進因素

- 對更高處理能力的需求不斷增加

- 增加研究投入

- 市場限制

- 初始設定成本高

- 安裝空間大

第6章市場區隔

- 按最終用戶

- 商業行業

- 政府

- 研究所

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- Atos SE

- Intel Corporation

- Hewlett Packard Enterprise

- Dell EMC(Dell Technologies Inc.)

- Fujitsu Ltd

- IBM Corporation

- Lenovo Group Limited

- NEC Corporation

第8章投資分析

第9章 市場機會與未來趨勢

The Supercomputers Market size is estimated at USD 11.17 billion in 2025, and is expected to reach USD 19.15 billion by 2030, at a CAGR of 11.38% during the forecast period (2025-2030).

Supercomputers, with their high-performance processing capabilities, are increasingly becoming the backbone for running artificial intelligence (AI) programs. Their architecture is adept at handling the extensive data requirements of AI and machine learning applications.

The Growth In The Usage Of High-performance Computing (HPC) Applications Worldwide Will Drive The Market

Key Highlights

- Supercomputers, known for their immense computational power and speed, play a crucial role in high-performance computing (HPC) systems. Their capabilities make them indispensable in the HPC landscape. With scientific research leaning more towards simulation-based techniques and the rising importance of machine learning (ML), the market demand for supercomputers has seen a notable uptick.

- Additionally, in October 2024, NVIDIA's shares reached an all-time high, fueled by rising optimism regarding the robust demand for its latest supercomputing AI chips, Blackwell. This underscores the promising growth trajectory of supercomputers, bolstering the overall market expansion.

- As organizations grapple with complex data sets and analytics workloads, the demand for supercomputers will rise. Supercomputers are now becoming more accessible and cost-effective for educational research institutions. Furthermore, the growing trend of democratizing computing power, especially through cloud-computing-enabled platform-as-service models, is set to boost the market further.

The High Initial Cost Of Supercomputing Systems Is The Major Hindrance To Market Growth

Key Highlights

- High ownership costs, encompassing the device's price, housing infrastructure, and operational expenses, render supercomputers expensive and challenge market growth. For example, in March 2024, Microsoft and OpenAI collaborated to build an AI-based supercomputer costing approximately USD 100 billion. This shows that such supercomputers cater predominantly to large corporations, making them unfeasible for small and medium-sized enterprises.

The Impact Of Geopolitical Conflicts Among Countries Can Impact The Market Growth

Key Highlights

- The demand for supercomputers in defense departments to increase cyber defense and attack supports the government sector's market growth. Additionally, in April 2024, a cybersecurity official at the US State Department detected unusual activity, revealing that China had developed a quantum supercomputer. This advancement can destroy all Western encryption, thereby nullifying their cyber defenses.

Supercomputers Market Trends

Commercial Industries to be the Largest End Users

- Automotive companies are rapidly utilizing commercial supercomputers in their applications. Global vendors and automobile companies have tailored these applications to cater to the industry's unique needs. Key applications of supercomputers in the automotive sector include crash analysis, structural analysis, and computational fluid dynamics. These have significantly enhanced product quality, reduced costs, and tackled previously insurmountable tasks. Given the industry's fierce competitiveness, the adoption of supercomputers has become essential for vendors in the global automotive sector.

- For instance, in February 2024, Tesla announced a USD 500 million investment to install a Dojo supercomputer at its Riverbend Gigafactory in Buffalo, New York. This supercomputer will train Tesla's Artificial Intelligence (AI) systems, crucial for autonomous driving. Anticipated as a major computing platform, it will train machine learning models and process vast data volumes from Tesla's electric vehicles.

- In the energy sector, supercomputers, especially those with attached accelerators, enhance energy efficiency in High-performance Computing (HPC) workloads. New algorithms are being developed to process extensive datasets, yielding higher-resolution images. This advancement aids in accurately locating hydrocarbons underground, particularly in challenging geological environments like Brazil, the Gulf of Mexico, Angola, and the Eastern Mediterranean. Companies can be more selective in their ventures by assessing exploration acreage and asset opportunities early.

Asia Pacific Expected to Witness Significant Growth

- Asia Pacific is rapidly emerging as a leader in technological advancements, particularly in the development of supercomputing systems, with significant contributions from nations like China and Japan.

- In the Asia-Pacific, rapid economic growth, substantial investments in research and development (R&D), and an increasing demand for advanced computational capabilities have fueled the region's consistent adoption and development of high-performance computing (HPC).

- Researchers in China have crafted a prototype quantum computer that can identify up to 76 photons via random sampling of Gaussian bosons. In a bid for dominance in this avant-garde technology, China's researchers are challenging major US firms such as Google, Amazon, and Microsoft. India is also making notable advancements in the Asia-Pacific arena. The nation has initiated the National Supercomputing Mission, targeting the creation of a supercomputing grid with 73 high-performance computing facilities, backed by a projected investment of USD 730 million by 2023.

- In February 2024, China discreetly unveiled the Tianhe-3 supercomputer, touted as the world's most powerful machine. Developed for the National Supercomputer Center in Guangzhou, the machine's secretive nature has fueled widespread speculation. Dubbed "Xingyi," Tianhe-3 is the latest addition to a series of supercomputers crafted by China's National University of Defense Technology.

- In September 2024, India launched the Param Rudra Supercomputing System, a significant leap in its technological journey. This advanced facility, crafted by the Centre for Development of Advanced Computing (C-DAC), bolsters India's high-performance computing prowess, especially in weather and climate computing.

- In October 2024, the Singapore government unveiled its commitment of SGD 270 million (USD 201.7 million) towards the enhancement of its national supercomputing infrastructure. This investment aims to bolster the capabilities of the National Supercomputing Centre (NSCC) in Singapore, ensuring robust support for local research initiatives. The announcement was made by the country's Deputy Prime Minister, who also chairs the National Research Foundation (NRF), during the official launch of the ASPIRE 2A and 2A+ systems. These advanced research supercomputers are under the management of NSCC. These developments are set to bolster the growth of the supercomputer market in the region during the forecast period.

Supercomputers Industry Overview

The market comprises several global and regional players vying for attention in a contested space. However, it is dominated by major vendors that cover a significant market share and compete to gain a foothold and become pioneers in different regional markets.

Vendors adopt competitive strategies to gain a foothold in the market with innovation and the capability to invest in R&D, which is on the higher side. Thus, this strategy intensifies the competition in the market.

Access to distribution channels, existing business relationships, better supply chain knowledge, and the development of high-performance computing solutions give established tech giants a market advantage over new competitors. Overall, the intensity of competitive rivalry among the vendors is expected to be high and remain the same during the forecasted period.

Some of the major market players are Atos SE, Intel Corporation, Hewlett Packard Enterprise Company, Dell EMC (Dell Technologies Inc.), and Fujitsu Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment Of The Impact Of Macroeconomic Factors On The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Higher Processing Power

- 5.1.2 Increasing Investments in Research

- 5.2 Market Restraints

- 5.2.1 High Initial Setup Cost

- 5.2.2 Large Installation Space

6 MARKET SEGMENTATION

- 6.1 By End User

- 6.1.1 Commercial Industries

- 6.1.2 Government Entities

- 6.1.3 Research Institutions

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Atos SE

- 7.1.2 Intel Corporation

- 7.1.3 Hewlett Packard Enterprise

- 7.1.4 Dell EMC (Dell Technologies Inc.)

- 7.1.5 Fujitsu Ltd

- 7.1.6 IBM Corporation

- 7.1.7 Lenovo Group Limited

- 7.1.8 NEC Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2026年全球人工智慧(AI)超級電腦市場報告

2026年全球人工智慧(AI)超級電腦市場報告 超級運算市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、最終使用者、部署類型及解決方案分類

超級運算市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、最終使用者、部署類型及解決方案分類 全球人工智慧超級運算平台市場:預測(至2034年)-按組件、部署方式、架構、人工智慧工作負載類型、最終用戶和地區進行分析

全球人工智慧超級運算平台市場:預測(至2034年)-按組件、部署方式、架構、人工智慧工作負載類型、最終用戶和地區進行分析 全球雲端OSS/BSS市場按組件、雲端類型、營運商類型和地區分類-預測至2032年

全球雲端OSS/BSS市場按組件、雲端類型、營運商類型和地區分類-預測至2032年 人工智慧運算能力伺服器市場按交付類型、伺服器類型、最終用戶、部署類型、元件和應用程式分類 - 全球預測 2026-2032超級電腦市場按高效能運算架構類型、最終用戶、部署方式、應用領域和冷卻技術分類-2025-2032年全球預測

人工智慧運算能力伺服器市場按交付類型、伺服器類型、最終用戶、部署類型、元件和應用程式分類 - 全球預測 2026-2032超級電腦市場按高效能運算架構類型、最終用戶、部署方式、應用領域和冷卻技術分類-2025-2032年全球預測 2025-2029年全球雲端運算人工智慧市場

2025-2029年全球雲端運算人工智慧市場 2025-2029年超級電腦人工智慧全球市場

2025-2029年超級電腦人工智慧全球市場 超級電腦市場規模、佔有率及成長分析(依作業系統、類型、最終用戶、應用及地區)-2025-2032 年產業預測

超級電腦市場規模、佔有率及成長分析(依作業系統、類型、最終用戶、應用及地區)-2025-2032 年產業預測 超級電腦市場規模、佔有率和趨勢分析報告:2024-2030 年按類型、應用、最終用途、地區和細分市場進行的預測

超級電腦市場規模、佔有率和趨勢分析報告:2024-2030 年按類型、應用、最終用途、地區和細分市場進行的預測