|

市場調查報告書

商品編碼

2044152

碳複合材料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Carbon Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

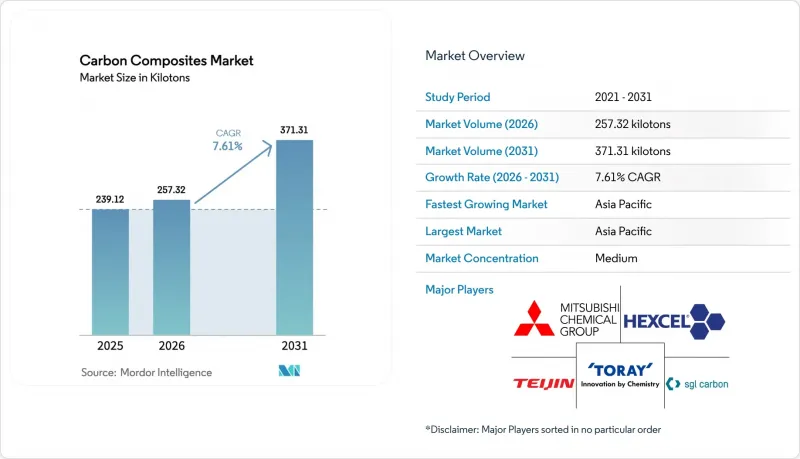

預計碳複合材料市場將從 2025 年的 239.12 千噸成長到 2026 年的 257.32 千噸,到 2031 年達到 371.31 千噸,2026 年至 2031 年的複合年成長率為 7.61%。

由於纖維價格下降、離岸風力發電快速發展以及交通運輸領域電氣化進程的推動,碳複合材料的潛在需求基礎正在擴大。預計到2024年底,中國大絲束的供應過剩將使T300級碳纖維的平均價格降至每公斤約12美元,這將加速其在風力發電機葉片和氫載體裝運船隻的應用,同時也擠壓現有企業的利潤空間。汽車製造商正在轉向高速循環熱塑性樹脂平台,以實現五分鐘以內的零件循環時間,從而能夠對結構電池托盤進行編程,而無需考慮高壓釜的瓶頸。航太領域憑藉一系列經過認證的預浸料保持著較高的市場佔有率,但六米以上大型高壓釜的產能限制正促使寬體飛機的編程轉向非高壓釜(OoA)樹脂系統。

全球碳複合材料市場趨勢及洞察

請求延長電動車的續航里程

電池式電動車車型配備的電池組重量在400至600公斤之間。碳纖維電池外殼比鋁製外殼輕40%至60%,每減重10公斤,續航里程即可增加15至25公里。 SGL Carbon公司的COOLBat演示樣機在整合主動冷卻通道的同時,將機殼重量減輕了35%。然而,BMW的2025年「新等級」計畫推遲了碳纖維的廣泛應用,因為在以煤炭為基礎的電網下,每公斤碳纖維仍會產生平均17.35公斤的二氧化碳排放。目前,由沙烏地基礎工業公司(SABIC)和考泰克斯公司(Kautex)共同開發的短纖維熱塑性外殼,成本約為每公斤8至10美元,正被應用於續航里程超過500公里的高階車型。這種兩極化表明,在可再生能源運作的纖維生產線將交付成本降低到每公斤約 10 美元之前,碳複合材料市場將依賴豪華汽車和高性能電動車。

大型離岸風力發電葉片(100公尺或更長)

對於長度超過100公尺的葉片,需要使用碳纖維尖帽以滿足25年的疲勞壽命要求。明陽馬達的143公尺原型機採用恆申纖維,使葉片尖端在額定風速下的撓度保持在8公尺以下。東方電氣的153米葉片與全玻璃纖維層壓板相比,重量減輕了18%,便於安裝在浮體式基礎上,而浮式基礎的起重船租賃費用通常超過每天50萬美元。根據維斯塔斯和西門子歌美颯的設計,葉片品質中的碳含量預計將從2025年的8-12%上升到2030年的約20%。由於長葉片的廣泛應用導致葉片價格上漲10%,TPI複合材料公司於2025年中期重新開放了位於愛荷華州的工廠。隨著離岸風力發電發電的加速發展,每安裝一台 12 至 15 兆瓦的風力渦輪機,需要 8 至 10 噸纖維,碳複合材料市場將從中受益。

鋁鋰合金被第三代先進高強度鋼取代所帶來的威脅

鋁鋰合金可將飛機機身重量減輕高達10%,同時由於可採用現有金屬加工技術進行維修,維護成本也可降低15-20%。第三代先進高強度鋼(AHSS)的強度為980-1180兆帕,延伸率超過15%,可使板材厚度減少20-25%,並顯著降低二氧化碳排放。寶馬公司決定在其「新等級」電動車中放棄大量使用碳纖維,正是基於這些生命週期和成本的考量。除非可再生能源發電能夠系統性地減少前驅排放,否則碳複合材料產業仍將面臨風險。

細分市場分析

預計到2025年,聚合物複合材料將佔碳複合材料市場佔有率的75.22%,並在預測期(2026-2031年)內以8.72%的複合年成長率成長。空中巴士公司用於支架的熱塑性PEEK(聚醚醚酮)和PPS(聚亞苯硫醚)零件,固化時間已縮短至5分鐘以內。同時,BMWi系列的結構部件在可回收性和損傷容限方面也展現出優勢。由於原料成本高昂,超過每公斤500美元,金屬基質和碳-碳複合材料的市佔率仍然較低。隨著聚醯胺6樹脂傳遞模塑製程將成型週期縮短至10分鐘以內,到2031年,熱塑性樹脂在聚合物領域的市佔率可望上升,並佔據碳複合材料市場規模的一小部分。

市場需求的強勁成長主要得益於汽車電池托盤、航太卡扣以及採用混合環氧-熱塑性樹脂中階的風力渦輪機葉片後緣等應用。 Gurit 的 98 公尺原型產品透過 500 萬次疲勞循環測試(符合 IEC 61400-23 標準)驗證了其設計的有效性,從根本上減少了分層問題的發生。可重熔的熱塑性樹脂廢料降低了一級模具製造商的廢料成本,進一步推動了碳複合材料市場長期永續性的發展。

《碳複合材料市場報告》按基體(混合基體、金屬基體、陶瓷基體、碳基體、聚合物基體)、工藝(預浸料層壓、拉擠成型和纏繞成型等)、應用領域(航太與國防、風力發電機、體育休閒、土木工程等)以及地區(亞太地區、北美地區、歐洲地區、南美地區、歐洲地區、歐洲地區細分市場和非洲地區。市場預測以噸為單位。

區域分析

預計到2025年,亞太地區將佔據碳複合材料市場39.12%的佔有率,並在預測期(2026-2031年)內以8.66%的複合年成長率成長。中國製造商如中復申鷹和廣維正在擴大大絲束的生產線,力爭2024年將國內自給率提高到80%以上,併計劃到2026年達到90%。到2025年,光是廣東省和江蘇省兩省就將消耗超過1萬噸碳纖維,以滿足離岸風力發電機葉片的需求。日本在高模量碳纖維(如T1000G和M60J)領域保持主導地位,其中東麗株式會社位於愛媛縣的工廠在高附加價值航空市場佔據主導地位。

北美佔據第二大市場佔有率,這主要得益於Hexel公司向波音、洛克希德·馬丁和諾斯羅普·格魯曼等公司供應預浸料。 TPI Composites公司計劃於2025年中期重啟其位於愛荷華州的工廠,這清楚地表明了Vineyardwind和South Fork項目對100米級風力渦輪機葉片的供需緊張。由於美國燃油經濟法規落後於歐洲二氧化碳排放標準,以及皮卡和SUV領域中成本效益高的鋼和鋁材料仍然佔據主導地位,汽車複合材料的應用仍然進展緩慢。

歐洲市場佔有率的成長主要得益於空中巴士項目以及多格班克和波羅的海之鷹離岸風力發電電場的建設。德國和法國在汽車複合材料市場佔據領先地位,但由於BMW公司正在進行策略評估,其產量預測較為保守。 Grit公司位於瑞士的工程中心和SGL Carbon公司位於德國的工廠已確保了熱塑性支架領域的充足產能。北歐國家的造船業應用,包括電動渡輪,正逐步吸收對複合材料的需求,但年需求量仍低於1,000噸。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 延長電動車續航里程的必要性

- 更大的離岸風力發電葉片(超過100公尺)

- 中國大型CF股票供應過剩對價格的影響(2026年及以後)

- 用於氫氣物流的 IV 型/V 型碳纖維增強複合材料 (CFRP) 容器

- 太空發射對可重複使用的碳纖維增強複合材料低溫儲槽的需求

- 市場限制因素

- 鋁鋰合金和第三代先進高強度鋼作為替代品的威脅。

- 全球高壓釜供應受限(寬體飛機)

- 禁止使用與 PFAS 相關的含氟上漿劑

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 矩陣

- 混合

- 金屬

- 陶瓷製品

- 碳

- 聚合物

- 熱固性

- 熱塑性樹脂

- 透過流程

- 預浸料層壓

- 拉擠成型與捲繞成型

- 濕式層壓和灌注

- 沖壓和射出成型工藝

- 其他

- 透過使用

- 航太/國防

- 車

- 風力發電機

- 運動休閒

- 土木工程

- 海洋

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Albany International

- China Composites Group Corporation Ltd

- Epsilon Composite

- Formosa Plastics Group

- GKN Aerospace

- Gurit Services AG

- Hexcel Corporation

- Huntsman International LLC

- Hyosung Advanced Materials

- Mitsubishi Chemical Group Corporation

- Nippon Carbon Co. Ltd

- Plasan

- Rockman

- SGL Carbon

- Syensqo

- Teijin Limited

- TORAY INDUSTRIES INC.

- TPI Composites

- Zoltek Corporation

第7章 市場機會與未來展望

The Carbon Composites Market size is expected to increase from 239.12 kilotons in 2025 to 257.32 kilotons in 2026 and reach 371.31 kilotons by 2031, growing at a CAGR of 7.61% over 2026-2031.

Falling fiber prices, rapid offshore-wind scale-up, and the electrification push in transportation are expanding the addressable volume base for the Carbon composites market. Large-tow overcapacity in China reset average T300-grade prices to about USD 12 per kilogram by late 2024, accelerating adoption in wind-turbine blades and hydrogen vessels while compressing margins for incumbents. Automakers are gravitating toward fast-cycle thermoplastic platforms that deliver sub-5-minute part takt times, enabling structural battery-tray programs without autoclave bottlenecks. Aerospace keeps its premium share on the back of certified prepreg pipelines, yet capacity constraints in 6-meter-plus autoclaves are steering wide-body programs toward Out-of-Autoclave (OoA) resin systems.

Global Carbon Composites Market Trends and Insights

EV Range-Extension Imperative

Battery-electric models carry 400-600 kg battery packs. Carbon-fiber battery housings deliver 40-60% mass savings versus aluminum, yielding 15-25 km extra range for every 10 kg trimmed. SGL Carbon's COOLBat demonstrator reduced enclosure weight by 35% while integrating active cooling paths. Yet BMW's 2025 Neue Klasse program sidelined widespread carbon fiber use because lifecycle emissions still average 17.35 kg CO2-eq per kg of fiber under coal-based grids. Cost-competitive short-fiber thermoplastic housings priced at USD 8-10 per kg, co-developed by SABIC and Kautex, are now aimed at premium 500 km-plus range cars. The bifurcation signals that the Carbon composites market will depend on luxury and performance EVs until renewable-powered fiber lines push delivered costs toward USD 10 per kg.

Upsized Offshore Wind Blades (more than or equal to 100 m)

Blade lengths above 100 m demand carbon spar caps to meet 25-year fatigue life. MingYang's 143 m prototype uses Hengshen fiber to keep tip deflection under 8 m at rated wind speed. Dongfang Electric's 153 m blade trims 18% mass versus an all-glass layup, easing installation for floating foundations where crane-vessel rates exceed USD 500,000 per day. Vestas and Siemens Gamesa designs indicate carbon content rising from 8-12% of blade mass in 2025 to about 20% by 2030. TPI Composites reopened its Iowa plant in mid-2025 after a 10% blade price uplift driven by the longer-blade mix. As offshore additions accelerate, the Carbon composites market will benefit from 8-10 tonnes of fiber per new 12-15 MW turbine.

Al-Li and 3rd-Gen AHSS Substitution Threat

Aluminum-lithium alloys trim up to 10% weight in fuselage frames while cutting maintenance outlays by 15-20% because repairs use established metal techniques. Third-generation AHSS delivers 980-1,180 MPa strength at over 15% elongation, supporting 20-25% mass-down-gauging at markedly lower CO2 footprints. BMW's decision to skip broad carbon-fiber use on Neue Klasse EVs reflects these lifecycle and cost realities. The Carbon composites industry will remain exposed until renewable electricity systematically cuts precursor emissions.

Other drivers and restraints analyzed in the detailed report include:

- Chinese Large-Tow Price Impact (2026+)

- Hydrogen Logistics Type-IV/Type-V CFRP Vessels

- Global Autoclave Bottleneck (Wide-Body Aero)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer composites commanded 75.22% of the Carbon Composites market share in 2025 and are projected to advance at an 8.72% CAGR during the forecast period (2026-2031). Thermoplastic PEEK (Polyetheretherketone) and PPS (Polyphenylene Sulfide) parts for Airbus brackets now cure in under five minutes, while BMW i-series structures demonstrate recyclability and damage tolerance advantages. Metal-matrix and carbon-carbon formats stay at a low share because of high raw-material costs that exceed USD 500 per kg. Thermoplastic content inside the Polymer segment could rise to a nominal slice of the Carbon Composites market size by 2031 as polyamide 6 resin-transfer molding drops cycle times below 10 minutes.

Demand momentum rests on automotive battery trays, aerospace clips, and wind-blade trailing edges deploying hybrid epoxy-thermoplastic interlayers. Gurit's 98-m prototype validated the design through 5-million fatigue cycles per IEC 61400-23, cutting delamination complaints in the root end. Re-meltable thermoplastic off-cuts reduce scrap cost for tier-1 molders, buttressing the long-term sustainability narrative of the Carbon composites market.

The Carbon Composites Market Report is Segmented by Matrix (Hybrid, Metal, Ceramic, Carbon, and Polymer), Process (Prepreg Lay-Up, Pultrusion and Winding, and More), Application (Aerospace and Defense, Wind Turbines, Sports and Leisure, Civil Engineering, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific retained 39.12% of the Carbon Composites market share in 2025, and is forecast to expand at an 8.66% CAGR during the forecast period (2026-2031). Chinese producers such as Zhongfu Shenying and Guangwei scaled large-tow lines to push domestic self-sufficiency beyond 80% in 2024, targeting 90% by 2026. Offshore-wind blade demand in Guangdong and Jiangsu alone consumed more than 10,000 tons of carbon fiber in 2025. Japan sustains leadership in T1000G and M60J high-modulus grades, with Toray's Ehime plant occupying the premium aviation niche.

North America ranks second in terms of the market share, underpinned by Hexcel prepreg supply into Boeing, Lockheed Martin, and Northrop Grumman. TPI Composites' Iowa re-opening in mid-2025 exemplifies supply-demand tightness for 100-m wind blades destined for Vineyard Wind and South Fork projects. Automotive composite uptake is moderate because the United States fuel-economy rules trail European CO2 norms, leaving cost-advantaged steel and aluminum prevalent in pickups and SUVs.

Europe's share, driven by Airbus programs and offshore-wind installations at Dogger Bank and Baltic Eagle. Germany and France lead automotive composites though BMW's strategy reset tempers volume forecasts. Gurit's Swiss engineering center and SGL Carbon's German plants secure critical mass in thermoplastic bracketry. Nordic marine applications, including electric ferries, absorb incremental composite tonnage but remain below 1,000 tons annually.

- Albany International

- China Composites Group Corporation Ltd

- Epsilon Composite

- Formosa Plastics Group

- GKN Aerospace

- Gurit Services AG

- Hexcel Corporation

- Huntsman International LLC

- Hyosung Advanced Materials

- Mitsubishi Chemical Group Corporation

- Nippon Carbon Co. Ltd

- Plasan

- Rockman

- SGL Carbon

- Syensqo

- Teijin Limited

- TORAY INDUSTRIES INC.

- TPI Composites

- Zoltek Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV range-extension imperative

- 4.2.2 Upsized offshore wind blades (more than or equal to 100 m)

- 4.2.3 Chinese large-tow CF over-capacity price impact (2026+)

- 4.2.4 Hydrogen logistics Type-IV/Type-V CFRP vessels

- 4.2.5 Space-launch demand for reusable CFRP cryo-tanks

- 4.3 Market Restraints

- 4.3.1 Al-Li and 3rd-gen AHSS substitution threat

- 4.3.2 Global autoclave bottleneck (wide-body aero)

- 4.3.3 PFAS-linked bans on fluorinated sizing agents

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Matrix

- 5.1.1 Hybrid

- 5.1.2 Metal

- 5.1.3 Ceramic

- 5.1.4 Carbon

- 5.1.5 Polymer

- 5.1.5.1 Thermosetting

- 5.1.5.2 Thermoplastic

- 5.2 By Process

- 5.2.1 Prepreg Lay-up

- 5.2.2 Pultrusion and Winding

- 5.2.3 Wet Lamination and Infusion

- 5.2.4 Press and Injection Processes

- 5.2.5 Other Processes

- 5.3 By Application

- 5.3.1 Aerospace and Defense

- 5.3.2 Automotive

- 5.3.3 Wind Turbines

- 5.3.4 Sports and Leisure

- 5.3.5 Civil Engineering

- 5.3.6 Marine

- 5.3.7 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Albany International

- 6.4.2 China Composites Group Corporation Ltd

- 6.4.3 Epsilon Composite

- 6.4.4 Formosa Plastics Group

- 6.4.5 GKN Aerospace

- 6.4.6 Gurit Services AG

- 6.4.7 Hexcel Corporation

- 6.4.8 Huntsman International LLC

- 6.4.9 Hyosung Advanced Materials

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 Nippon Carbon Co. Ltd

- 6.4.12 Plasan

- 6.4.13 Rockman

- 6.4.14 SGL Carbon

- 6.4.15 Syensqo

- 6.4.16 Teijin Limited

- 6.4.17 TORAY INDUSTRIES INC.

- 6.4.18 TPI Composites

- 6.4.19 Zoltek Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment